Discussed it here in brief.

Today’s presentation has some very useful information

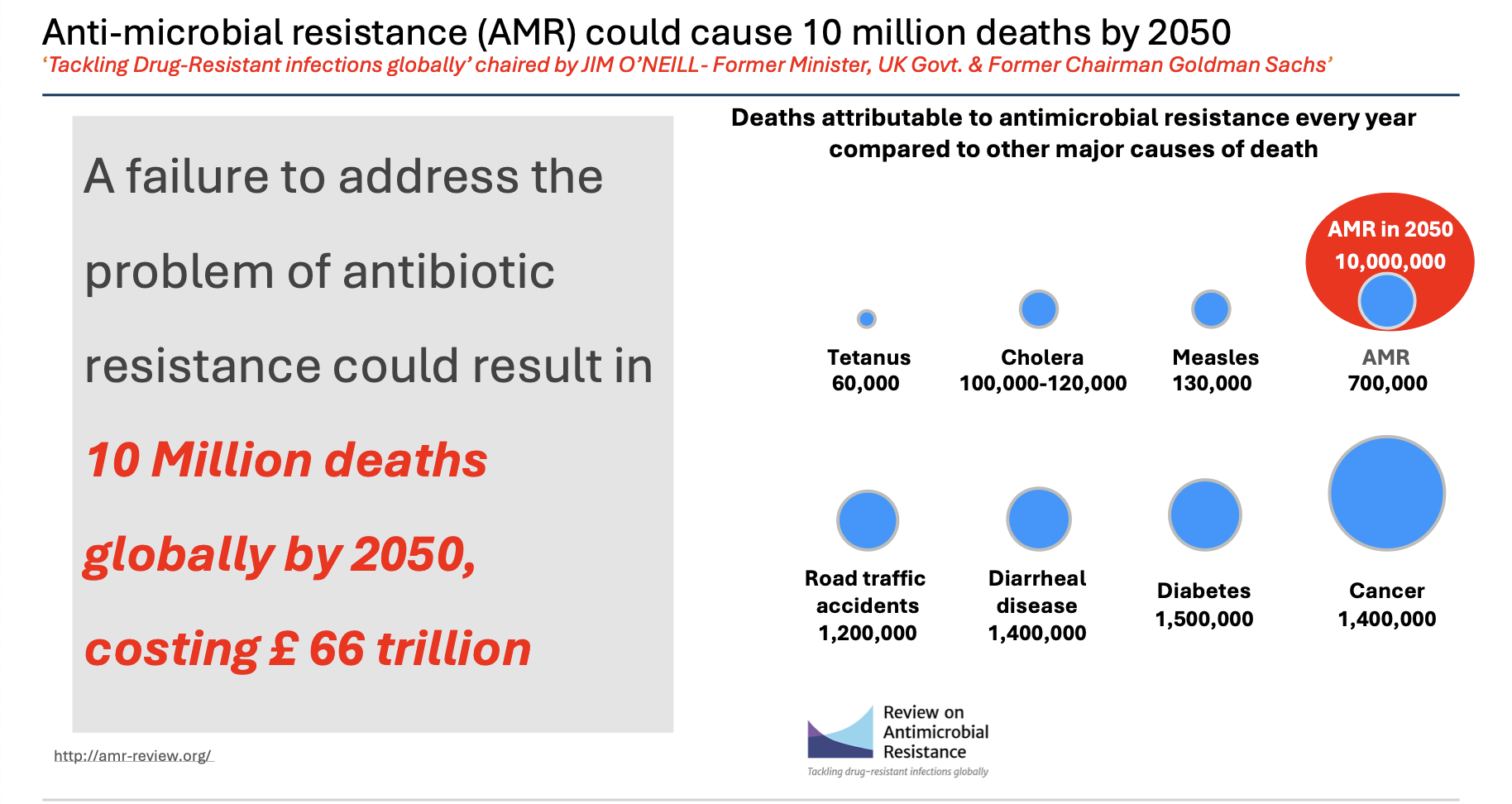

AMR deaths at 700k worldwide and could be 10 million by 2050.

I found the same information from multiple sources

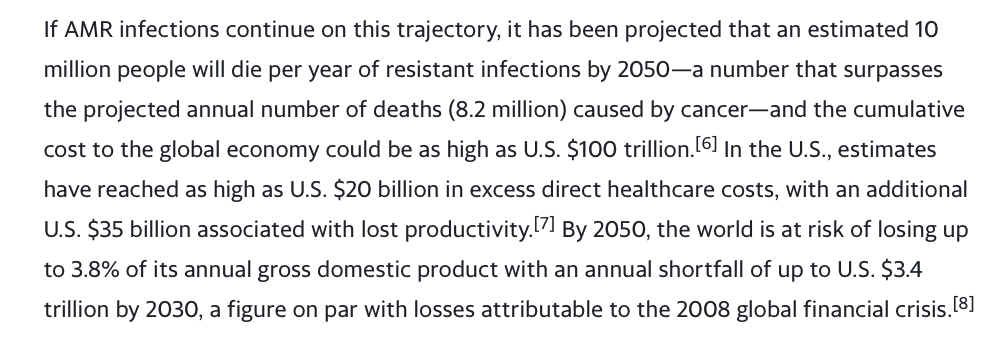

This bit is from Venatorx failing to get FEP-TAN approval this month (more on this later) which again speaks of a similar 10 million number by 2050.

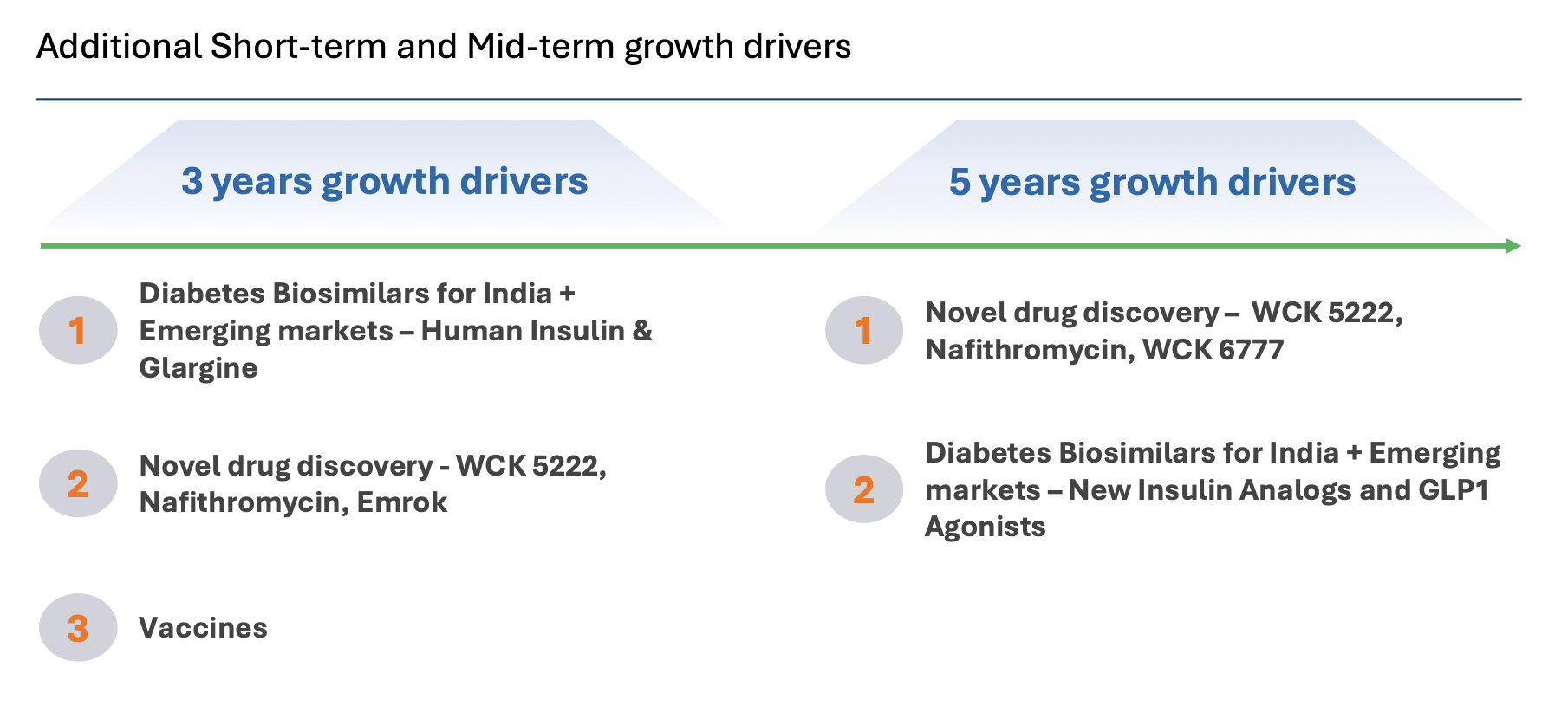

Antibiotic pipeline is more or less dry so a company like Wockhardt which has kept its R&D going becomes all the more valuable, over and above the value of the 6 NCEs it has developed. (Consider gestation in decades and experienced talent with 315 scientists and 55 PhDs)

It looks like growth will come from insulin glargine launches in emerging markets and also from vaccines business (need more clarity here though on what these 150 million doses are for and what Wockhardt can expect to make from it - the longevity and profit-sharing is enticing but hard to figure out what it will generate) and from US business restructuring, alongside growth in Emrok/Emrok-O and Nafithromycin launches in India and other Emerging markets in the next 3 years - outside of WCK 5222.

Also good to see long-term vision in GLP-1 analogs - but this could be a rather crowded space by the time semaglutide goes off-patent.

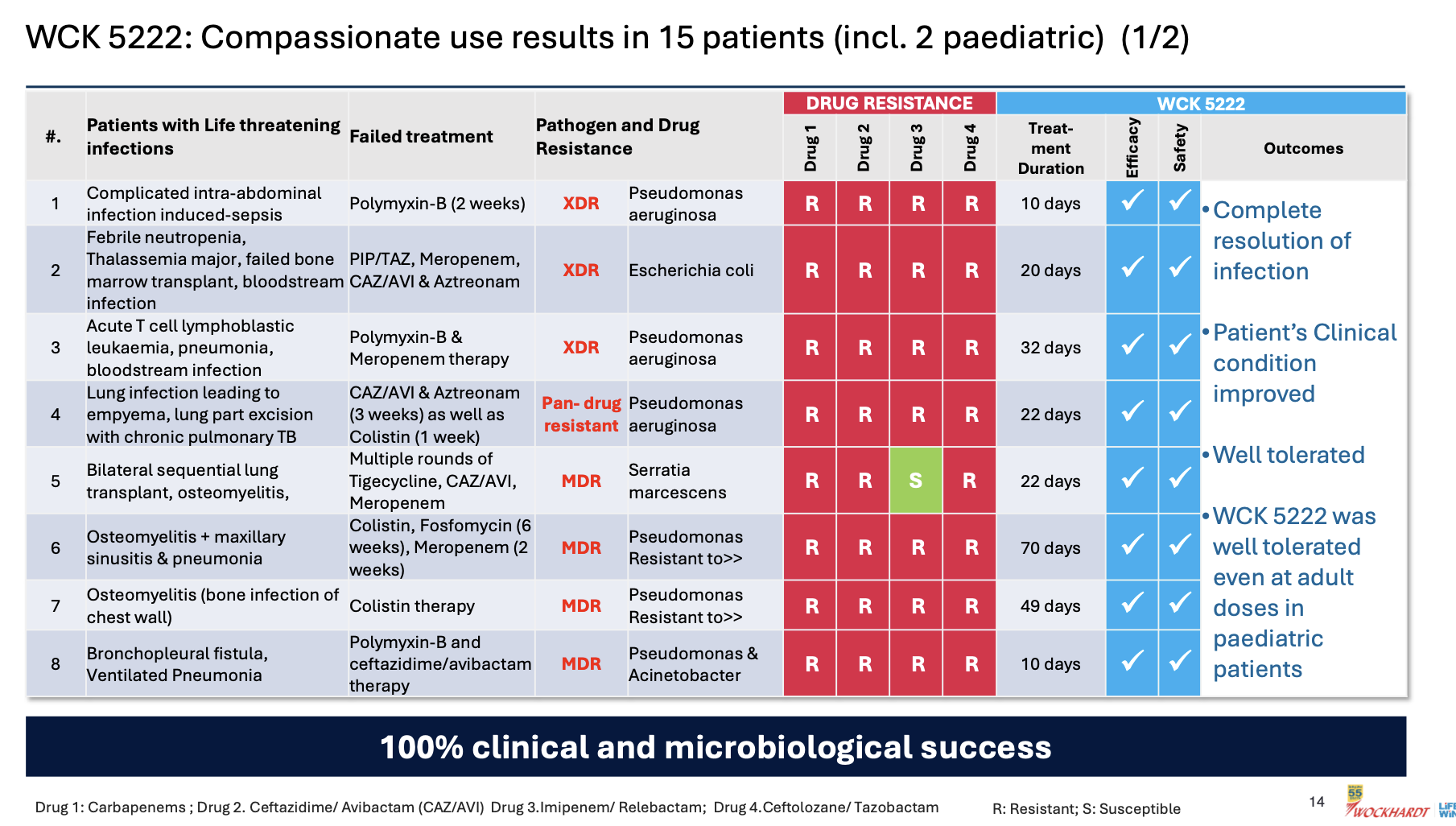

Coming back to WCK 5222, the company has disclosed the compassionate use results in great detail

Few things of note

- Pediatric use was well tolerated even at adult doses - so safety of the drug is becoming better established

- 100% clinical and microbiological success confirming efficacy

- CRPA is where WCK 5222 seems to shine (11/15 cases)

- Avg. use of drug could be around 4 weeks (though sample size is small, it appears varied so could be a general indicator)

- Colistin and Polymyxin are present in most ineffective treatment - wondering if these could be replaced with WCK 5222 right off the bat. While Meropenem is expected to fail in these, it is also good to see CAZ/AVI or CAZ/AVI + AZT resistant strains being susceptible to WCK 5222

(Please take above interpretations with pinch of salt - I am going by my half-baked knowledge)

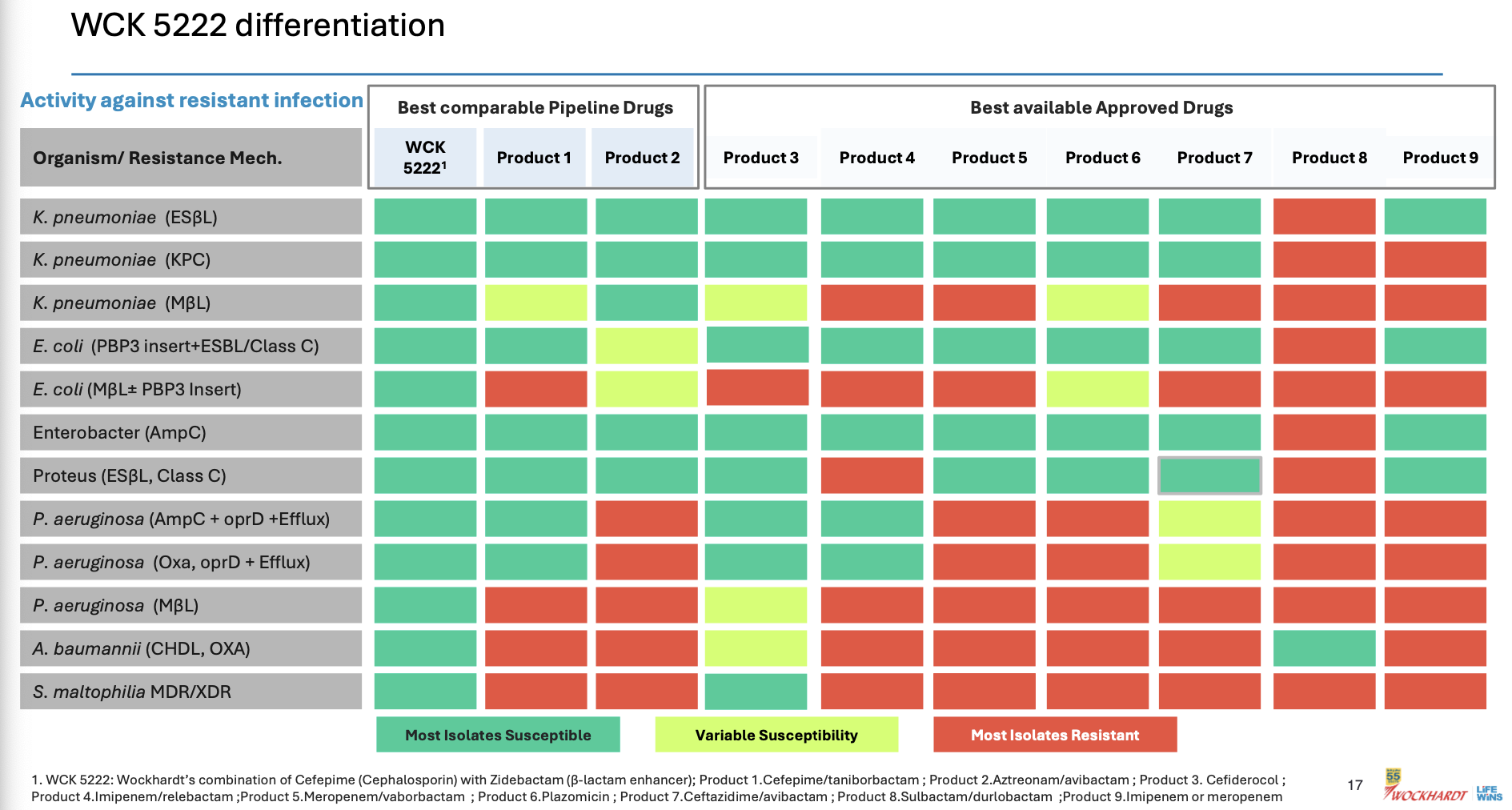

This is the clincher for me

This was the point of our post based on our research from various papers. Here it is laid out clear for even a layman to understand.

The actual products are mentioned in fine-print at the bottom of the slide. I see WCK 5222 being better than CAZ-AVI, FEP-TAN, CFD, AZT+AVI which are the main comparable treatment against lot of the resistant strains - especially the MBL-producing PA and E. coli. With FEP-TAN too falling out (probably due to Treatment Emergent Adverse Effects being higher than Meropenem), value of WCK 5222 once approved should be substantial.

Before I close, the same yahoo finance piece mentioned MBL prevalence increasing the US

MBL-producing pseudomonas is where WCK 5222 has very good edge over the others. This increase in prevalence in the west again increase market value of WCK 5222 once approved

Overall things seem to be going in the right direction. Hope the company can raise the funds required to take the phase-3 to completion and not botch it up somewhere

Disc: Invested