I haven’t seen any lending co maintain such high spreads and yet have so low credit costs, so I don’t know an appropriate benchmark. That being said, a 6x PB maybe appropriate if they maintain these return metrics on incremental loans.

Largely unchanged, I like the fact they have become more open with investors and are judiciously investing in lithium ion batteries, while maintaining leadership in lead acid. However, their free cash generation will be lower for the foreseeable future. With these two caveats, I am happy holding and adding at current valuations.

I want to get an opinion on the Affordable Housing Industry.

Many of the Small Finance Banks have started growing their affordable housing loans, given that they have low cost of funds how do you think Aptus or Aawas can compete with them ?

Personally I think its the New to Credit Consumers and the Low Opex Costs that play a very important role in growth for Aptus. Are there any other advantages that you think Aptus has over the SFB’s venturing into this space?

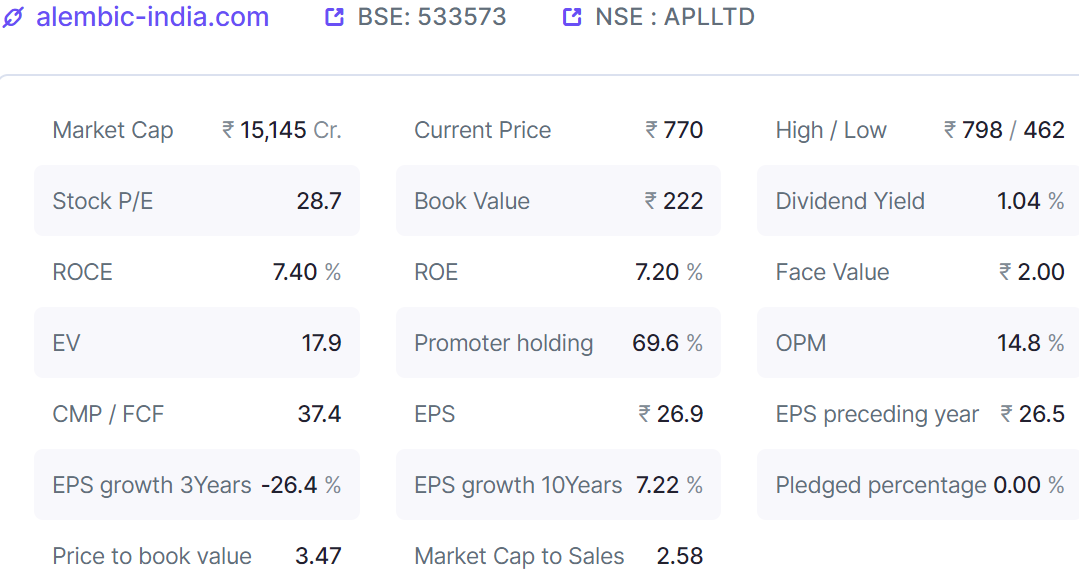

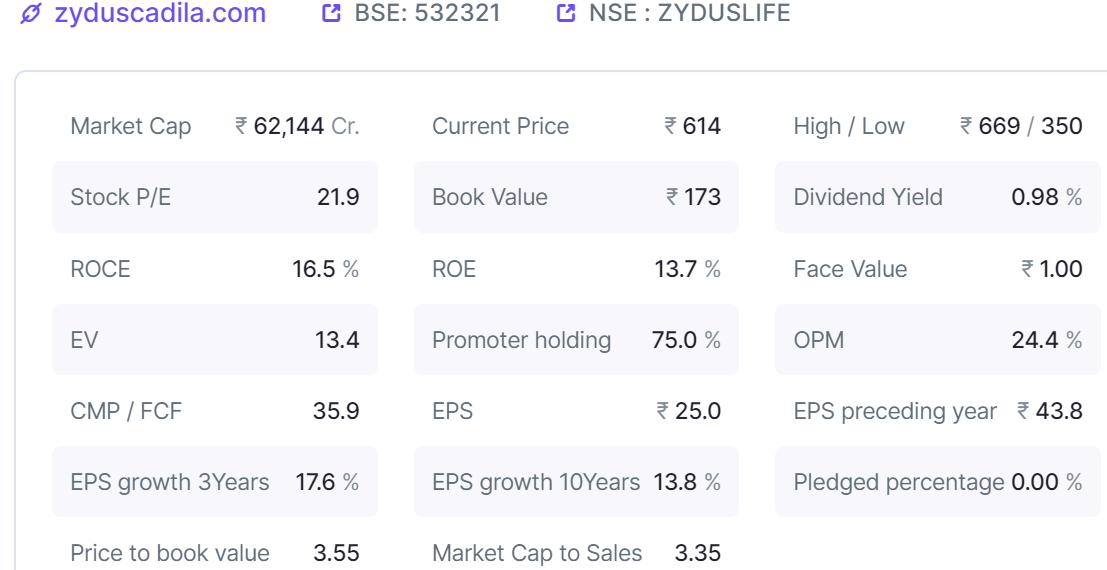

Hi Harsh, Why Alembic Pharma and not Zydus Lifesciences? Specially given that the promotor of Alembic Pharma does not seem to have the highest standards… Over 10Yrs EPS growth has been higher for Zydus, its OPM and ROCE are both higher. Promotor stake is also higher… Valuation wise also Zydus is not that expensive given its higher profitability ratios… Market cap to Sales of 3.35 over Alembic Pharma’s 2.58; and if one compares EV/EBIDTA its lower for Zydus at 13.4 over Alembic’s 17.9

Do you anticipate Alembic to do much better from now on? I frankly have not studied their launch pipelines which I agree may have a much bigger impact in the medium term; but still for a long term investor the above ratios should be more important or am I missing something…

Zydus Iife sciences mainly caters to OTC segment. Main thing here is volume growth which seems to be missing for last 4-5 years as a result stock price also hasn’t performed. Lately promoter has bought large number of shares from market, so need to track.

Sold 2% position in Transpek. Company is facing some headwinds in their end markets along with price compression in their end products. What I particularly dislike is their delayed capex plans despite them running at fully capacity for sometime. I am looking to buy Ultramarine as an alternate, as they are doing modular expansion and have similar business profile.

Sold remainder 2% position in Chamanlal Setia. Despite 20% drop in volumes, they were able to report higher profits due to smart raw material procurement done in October. Basmati cos are currently doing very well due to decadal high basmati prices, and I want to take money out as I dont know how long the basmati cycle will last.

HDFC merger into HDFC bank takes 4% HDFC position out of portfolio and replaces it with a 4% position in HDFC bank. I will likely scaleup HDFC bank to 8% at some point in the future

Reduced position size in Sharda Cropchem from 4% to 2%. Global agchem companies are facing higher pressure compared to domestic cos and I want to tactically allocate more to domestic facing cos (see #5)

Added 2% allocation in Dharmaj Crop Guard as they have been doing exceedingly well, having grown sales at 30-40% CAGR in past few years. As their technical plant come onstream this quarter, their margins will get a boost. I am expecting 20-25% sales growth with some margin expansion over the next few years, resulting in high EPS growth. Current valuations are not very demanding

Increased position size in SGRL - PP from 1% to 2%. SGRL annual report was a delight to read and management is very confident about future growth. This is a company which can likely trade at very high valuations as they have a very differentiated business model, as seen in high margins and ROCEs

Increased position size in Geekay wires from 1% to 2%. Despite a 4-5x jump in prices since I initiated the position, valuations haven’t increased significantly as earnings have just exploded. In their annual report, they mentioned about their order book being full and them doubling capacity in nails. Recently, I came to know that Geekay is one of the only 2 Indian companies who are approved to sell pneumatic nails in the US. Also, the anti-dumping investigation came out in their favor, which gives further fillip to their business. On trailing basis, they are only trading at 10x earnings

Added 2% position size in Worth Peripherals in deep value basket. This is a business currently not doing well, but I like their execution since their IPO in 2017. They are cheaply valued, and I hope to sell at 2x PB in the next couple of years. I feel its a low downside opportunity, where downside is capped at Rs. 90-100. Given the spectacular success I have witnessed in deep value strategy, I will now be initiating new positions at atleast 2% position size

Added 2% position in Godrej Agrovet and 1% in KSE Ltd. Thesis in both is of mean reversion. Both companies are into feed manufacturing and their margins were adversely impacted in last couple of years. As a result, both are trading at cyclical lows in terms of EV/sales. Margins have started recovering since last quarter. The additional kicker in KSE can come from a potential of Godrej acquiring them, as they already own some stake in the co and are in the same business line

Reduced position size in Aditya Birla AMC from 4% to 2%. A number of their equity schemes have been doing badly of late. In terms of strategy, Aditya Birla schemes are exactly reverse of HDFC AMC, where Aditya Birla focuses on high return metrics often combined with obnoxious valuations, whereas HDFC is much more value focused. Value has made an amazing comeback in the past year and I am looking to buy more of HDFC AMC.

Added 2% position in Mayur Uniquoters. Growth in exports is back for Mayur, and its likely that they grow sales at 15% for the next few years, which along with margin uptick can result in 20%+ EPS growth. If that happens, it can be a doubler.

My current thoughts on a few portfolio companies:

I want to reduce position sizes in Ajanta Pharma and Gufic Biosciences as pharma companies have done exceedingly well in past few months (this basket is up 37% YTD for me) and I want to reduce allocation to companies which are trading at higher end of their valuation bands. I think Ajanta is the most differentiated midcap pharma co, however they have been topping out at 6-6.5x sales, with current valuations being ~6x sales. Gufic is also trading at higher end of their valuation band.

I want to increase Aegis’ position back to 4%. Over time, clarity has emerged about the sustainability of LPG as a good alternate to LNG in industrial applications. I was earlier confused if this replacement was due to one time arbitrage in pricing between the two fuels, whereas the management was confident of this sustaining for atleast 2-3 years. Its turning out that management were spot on (as reflected in much higher LPG imports into India vs LNG). Aegis has a very very differentiated management.

I want to increase position size in Kaveri seeds to 4%, finally their growth has started kicking in due to their focus on rice and other vegetable seeds. Additionally, they are doing exceedingly well in export market. Its uncommon to get a market leader with high return metrics at such low valuations (10x earnings) in Indian markets.

I want to increase position size in Manappuram to 4%, as growth is coming back and they are trading at very cheap multiples.

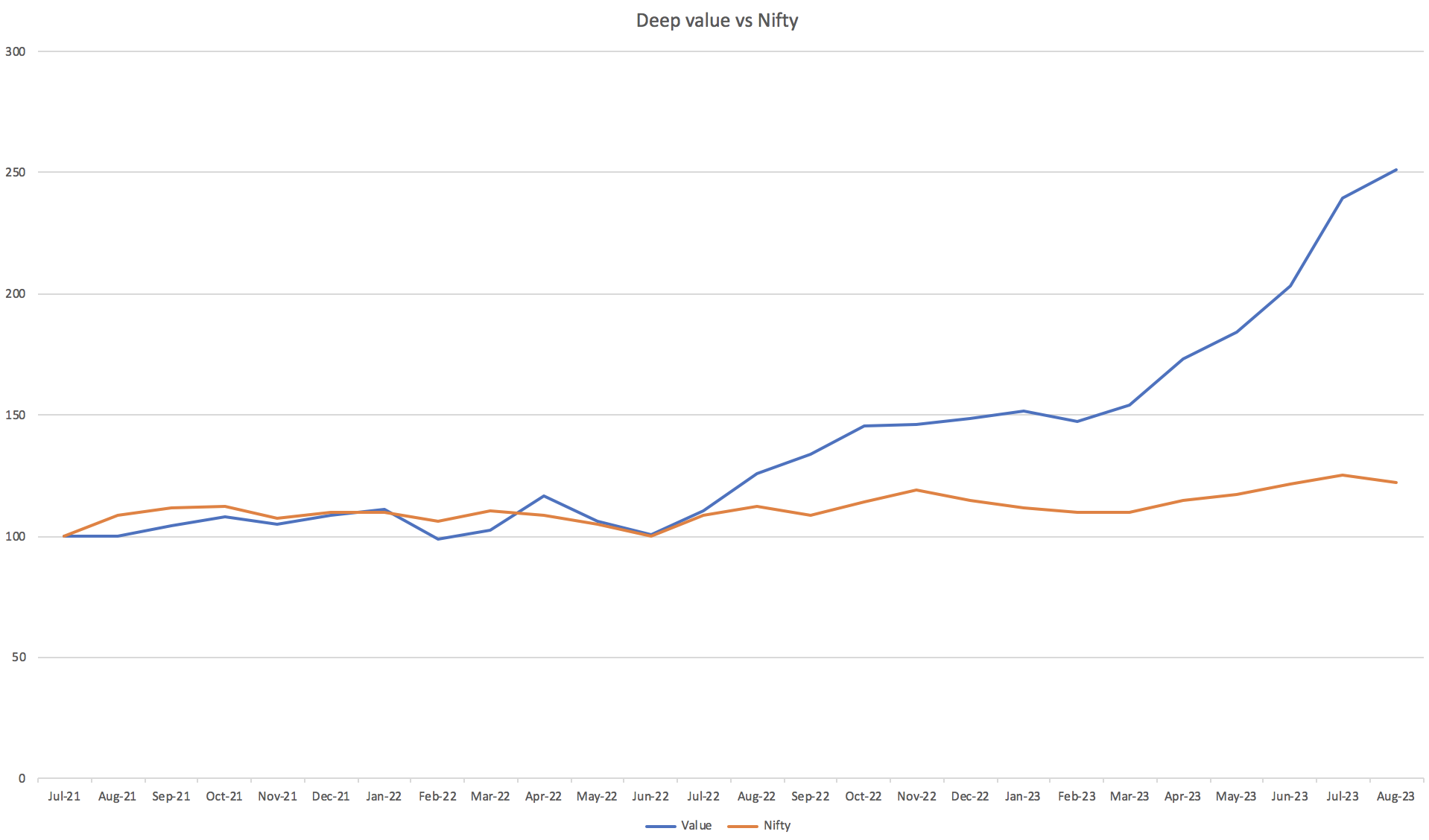

I keep sharing my time weighted returns annually on this thread, you can see returns until 2022 below.

In 2023 until August, portfolio is roughly up by 32%, so you can compute overall returns. What I dont share on this thread is capital weighted return. Since peak of January 2018 until August 2023, capital weighted returns (net of dividends and transactions costs) has been ~27%. But this number fluctuates wildly depending on market performance.

I think runway for anything related to loans is very long in India as credit growth is a multiplier of nominal GDP growth. I expect housing finance industry to keep growing at 14-15%, affordable housing at 18-20% and differentiated affordable housing companies (likes of Aptus) can potentially grow at 25-30% for a long period of time. More than growth, I am focused on credit underwriting quality and cost structure for NBFCs. In both terms, I find Aptus to be higher quality (high NIMs, low credit costs, very low operating costs, secured loans).

Yes, I am invested and continue to remain bullish on the company. For now, I haven’t thought of an exit plan. To be honest, I think Propequity can easily trade at 1000 cr. market cap, given the kind of valuations market gives to loss making platform businesses.

Alembic Pharma has actually done exceedingly well if you zoom out a bit and look at their growth profile since 2011. The mistake they made was allocating too much capital at cycle top, and then facing FDA issues. However, the FDA issues have now been resolved and they are being more measured about capital allocation now.

Zydus is currently doing very well due to revlimid opportunity, and their successful forey in injectables and transdermal patches. However, over a longer period of time, Zydus’ growth rate has been lower than Alembic as Zydus has a very high base. Going forward, I feel Alembic will make a strong comeback. My personal philosophy is one shouldn’t get overbullish during good times and overnegative in bad times, as neither last.

You are mistaking Zydus wellness with Zydus Life. Both are different businesses, owned by the same group.

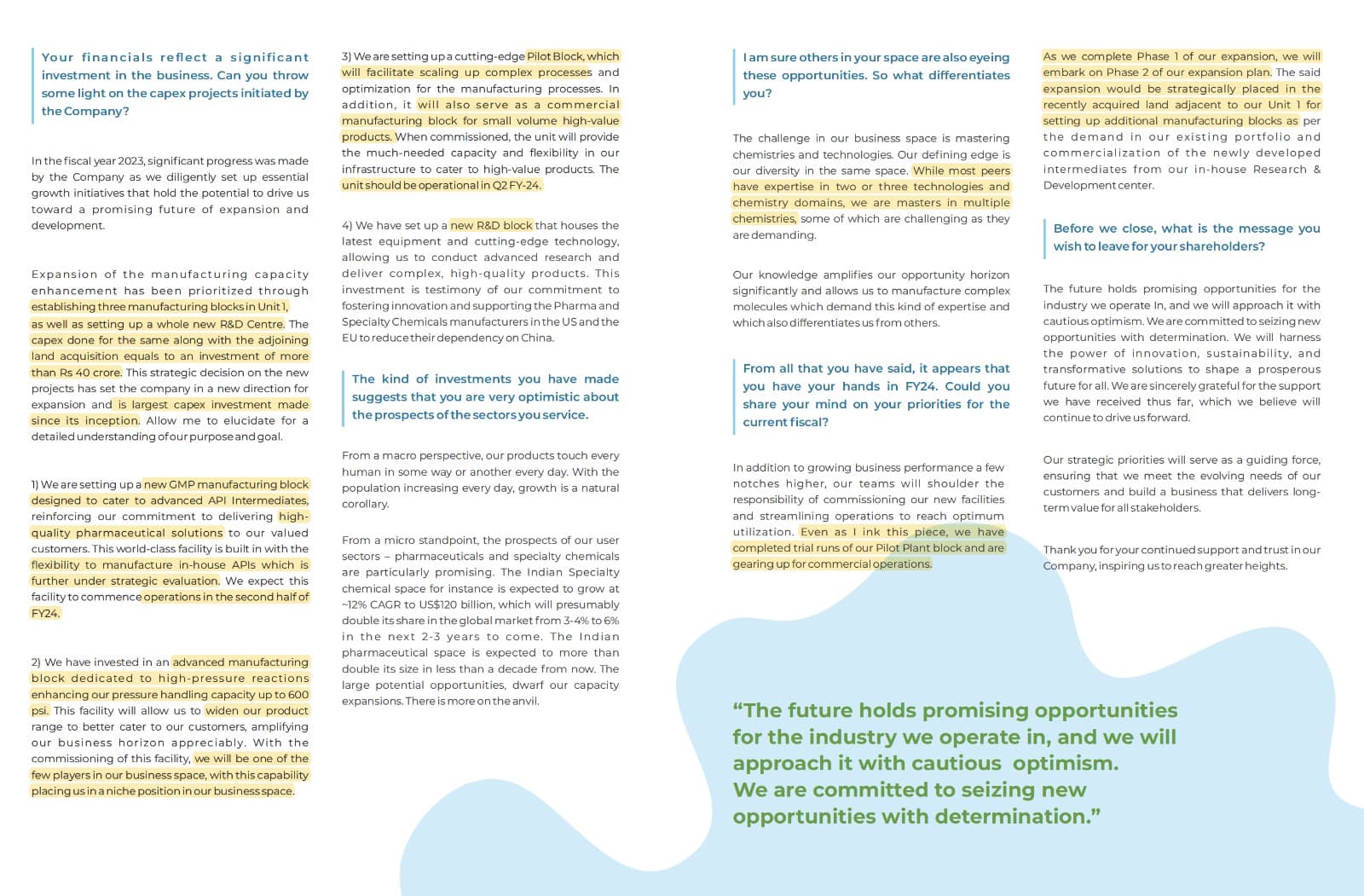

Dharmaj am holding since IPO due to their growth prospects and gone through the painful period of holding it. Have you been able to attain today’s AGM? I was late to it, towards closure part of it. They guide high EBIT of 400-500 bips but not sure as I heard last part of QA.

Hi Harsh, What would be the criteria for you again buy Chamanlal setia in future? Will u go with Price to Book metrics coupled with favourable business environment only? Are you OK with Chamanlal touching say 1000 in next one or 2 years with favourable conditions? Technical like crossing all time high make any impact in thinking? Because more gains happen when business is in bullish mode coupled with market in bullish mode.

Thanks

Yes, company also emailed me answers to my detailed questionaire as there were questions that couldnt take up during the AGM. I was impressed to see how detailed the answers were.

Congratulations for growing business in such a tough environment, with minimal loss of margins. I have the following questions

In domestic branded crop business, companies report sales return item which is generally 10-20% of sales. I do not find this line item in the annual report. Instead, I see discounts given as a line item in two different places (other expenses, revenue from operations).Discount given: 2.14 + 6.14 cr. ~ 8.28 cr.(vs 1.7 + 5.82 ~ 7.52 cr. in FY22). Is this in relation to our branded B2C business? And what is the sales return we booked in FY23 and FY22?

We normally do not accept sales return except in the case of damaged or leakage due to mishandling. In case there is sales return we show sales as net of sales return. 2.14 cr. is discount received on procurements, 6.14 cr. is the discount given. Sales return was around 1.3% of sales in FY23 and 1.4% in FY22

Despite such a tough macro environment, how are we able to grow our domestic branded and institutional business so well? What are we doing differently vs peers?

A key differentiating factor for Dharmaj in the last 8 years of our operations has been our absolute focus on demand generation and farmer engagement activity. This is a proactive function that runs through the entire organization. Further, this is supported by constantly refreshing our product portfolio to keep in line with the trends of the industry, not only we launch new products each year, but we are also able to generate sales out of them – as is reflected in our Product Innovation Index disclosed in the AR & Investor Decks. We have also significantly increase our sales and marketing team, which has nearly doubled from 109 people in FY22 to 186 in FY23 and ~220 in Q1FY24.

Given that we are a late entrant in domestic market, have we managed to finish our product portfolio of generic molecules? Or are there still gaps within our product portfolio?

Being a generic formulator we have covered almost all type of generic molecules for all kind of crops. At present we have around 160 generic molecules in our product portfolio. We will be able to cover some of the identified gaps as we increase the scale of operations, our Active Ingredients expansion will also aid in this aspect.

In our institutional segment, we talk about serving small formulators as a strategy. What % of our institutional business comes from small formulators vs larger companies?

80-85% to small formulators , rest from large formulators

A lot of innovation happens in domestic business via differentiated 9(3) filings. Do we have any 9(3) molecule in our portfolio and in our pipeline? Have we inlicensed molecules from Japanese and European MNCs?

Don’t have any 9(3) filing or pipeline currently , no collaboration with Japanese/European innovators yet. We certainly have ambition for collaborating with foreign players, as we scale our operations, commission active ingredients plant, and mark our presence across the entire agrochemicals value chain; but that is a couple of years ahead of us.

Foreign innovator normally looks at production facilities, product portfolio, market reach, network of an Indian domestic company to partner with. Dharmaj is having world class facilities, experienced team, upcoming backward integration plant, we are introducing new products every year, have captured almost half of the country in B2C business and whole India in B2B business. In nutshell we are meeting all the required criteria to partner with Foreign Innovator.

We talk very bullishly about public and animal health vertical. Can you talk more about this segment, its potential and our market positioning? Who are our large competitors in this segment?

Public health is a growing segment and current market size in India is 1300-1400 cr. out of which 45% is used in Private and 55% by Government and Public institutions like Hospitals, Railways, Military, CWC Godown (Grain Storage), Plywood Industries (for termite protection) etc.

There are 20 active players with cos like Bayer, Syngenta, UPL, Heranba, Sumitomo, Arbuda, Kilpest, etc. commanding good position. Dharmaj is a new entrant starting business in 2021 and currently has 14 products . As it is a high margin segment , we are targeting to scale up the business in this segment and building a team to capture a portion of the Indian market by building our own sales channels.

What is our growth outlook for FY24? We talk about maintaining 25%+ sales growth for the foreseeable future, which is much higher than any of our peers. How will we manage to achieve this?

We have mentioned earlier that our presence currently is in Central, North and Western India with some portion of North East India. Last year we have marked our entry into 6 new sates, where sales potential is significant, and we have only scratched the surface. For us currently still entire South India market is untapped in branded business, and we are confident to penetrate Southern market in coming year. In export also we have ready customers who are waiting for our technical plant to start commercial production, further we have a decent product registration pipeline that should open new markets for us in the coming years. Public Health is another division where we can foresee lot of potential and hence, we have deployed a fresh team having experience in similar segment. All of these factors put together give us the confidence of doubling our topline every 3 years (or as you said 25%+ growth).

Board should consider paying dividend, given that we raised a lot of money during IPO and our core business generates good amount of cash. Even a small 5% payout shows management intent of sharing wealth with minority shareholders

Will declare dividends once capex gets completed in Q3FY24. They believe in paying dividends out of internal accruals over IPO money which was raised for a different objective.

We should also do an investor meet every 6 months to be better updated with company activities

Yes we have already planned half yearly investor call instead of quarterly to keep our investors updated on companies activities.

Other points

Manage inventory on a month-to-month business and according to crop cycle

10% of inventory comes back at year end

Focus a lot on marketing via social media for demand generation

Expect technical plant to run at full utilization in FY27 (3 years from commercialization)

Due to sluggish performance post November of FY’23 our EBITDA margins remains at 9% which normally in the range of 10% to 11%. If we compare with normal EBITDA percentage the improvement will be around 300 to 400 basis points. We are expecting our Technical plant scale up and runs at optimum level by FY 27 i.e. 3 full years of commercial operations, since in FY24 the plant will only be available for one quarter. However, yes the margins will improve from 2% to 3% in first 2 years in our existing business and it will improve up to 400 to 500 basis point from current level once it reached at full capacity utilization. Further we expect much better margins in our standalone Technical sales to 3rd party, which will further aid overall margins.

I can buy around book value. If it reaches share price of 1000 in near term, I will be depressed!

In the agrochemical sector, could you please explain why you preferred Dharmraj over BestAgrolife? High inventory, receivables, and a Debt to Equity ratio greater than 1 seem to be issues in BestAgro. However, it is available at half the valuation of Dharmraj. Similar to Dharmraj, BestAgro also doesn’t have much exposure to the international market. Additionally, according to management guidance, BestAgro is expected to achieve a 30% sales growth and improve its CFO in the second half of this financial year.

Hi Harsh, thanks for the update, I bought this seeing promoters background and AR and after Q1 results, hopefully they will conduct a concall after Q2. Thank you once again.

Hii Harsh, first of all thank you for sharing your insights and mindset, I wanna know your views about concentrated portfolio because yours is opposite one and did you felt that you miss return on whole portfolio due to low allocation to that one particular company which given magnificent return.

Hi I was researching this company found the valuation is very cheap wrt what the growth can be in coming years. But need to be very sure of their growth.

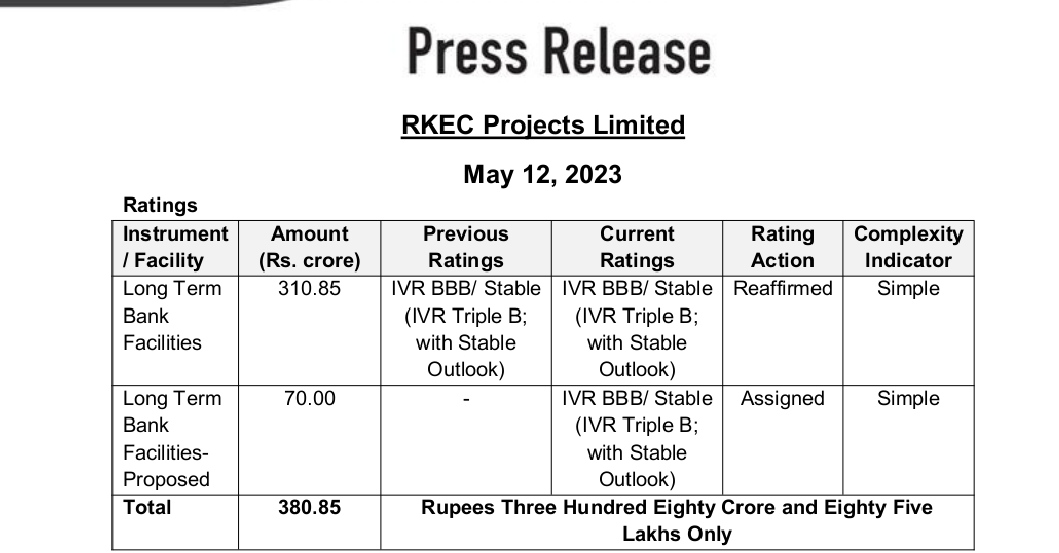

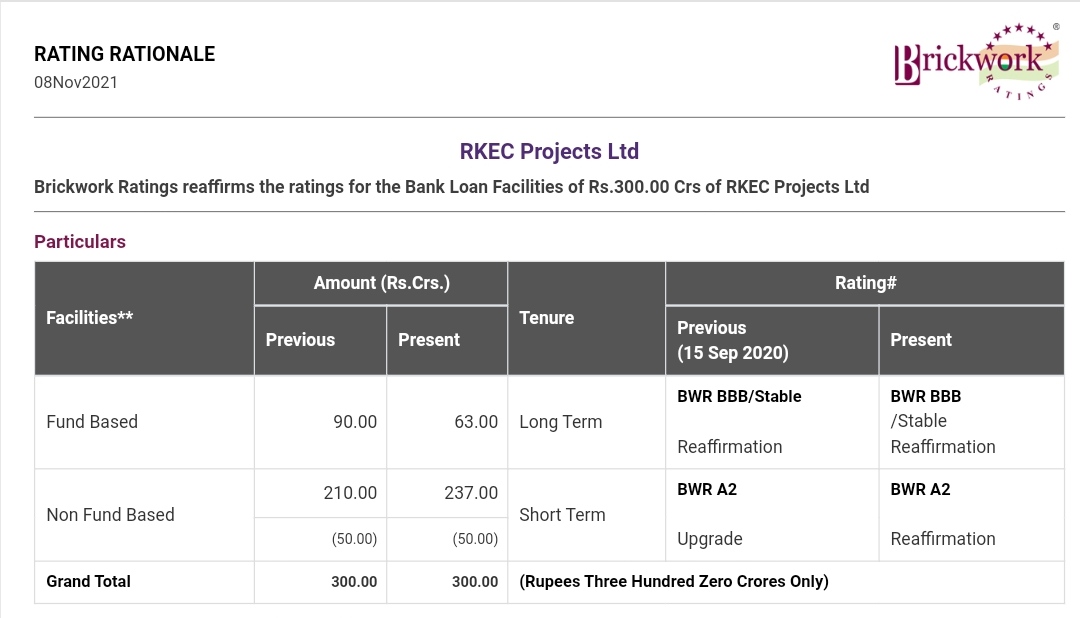

What I think js it’s not the orderbook that limits their topline Growth but the working capital availability which in turn is dictated by how much the banks are agreeing to provide. On this front this issue seems to have improved from the credit rating reports of 2021 and latest one where it says earlier they could get 300 cr loan now it’s 380 cr…so this should help the growrh.

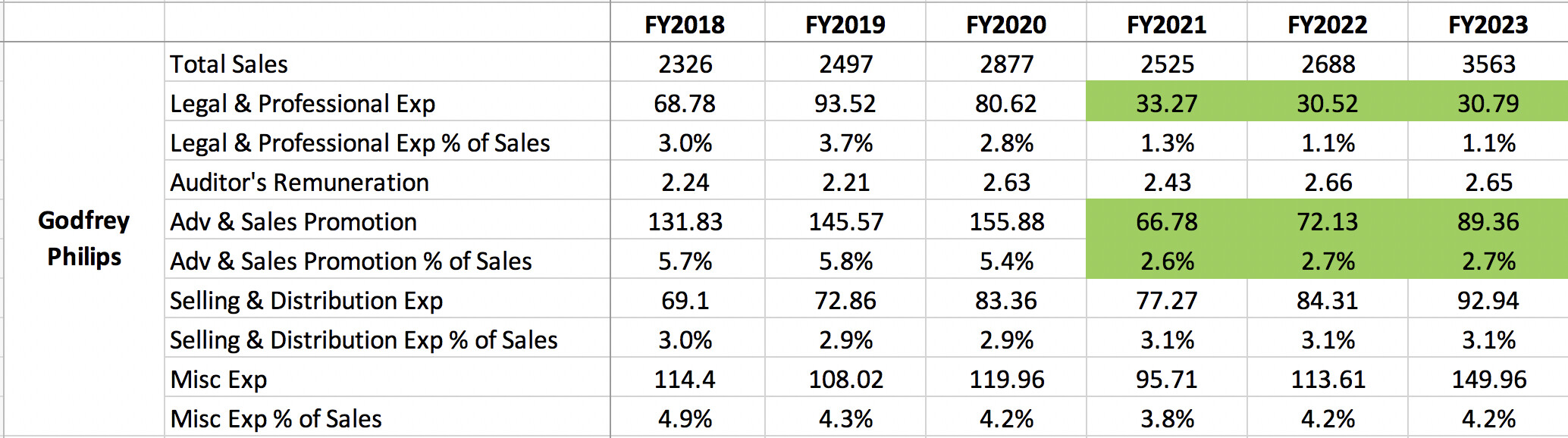

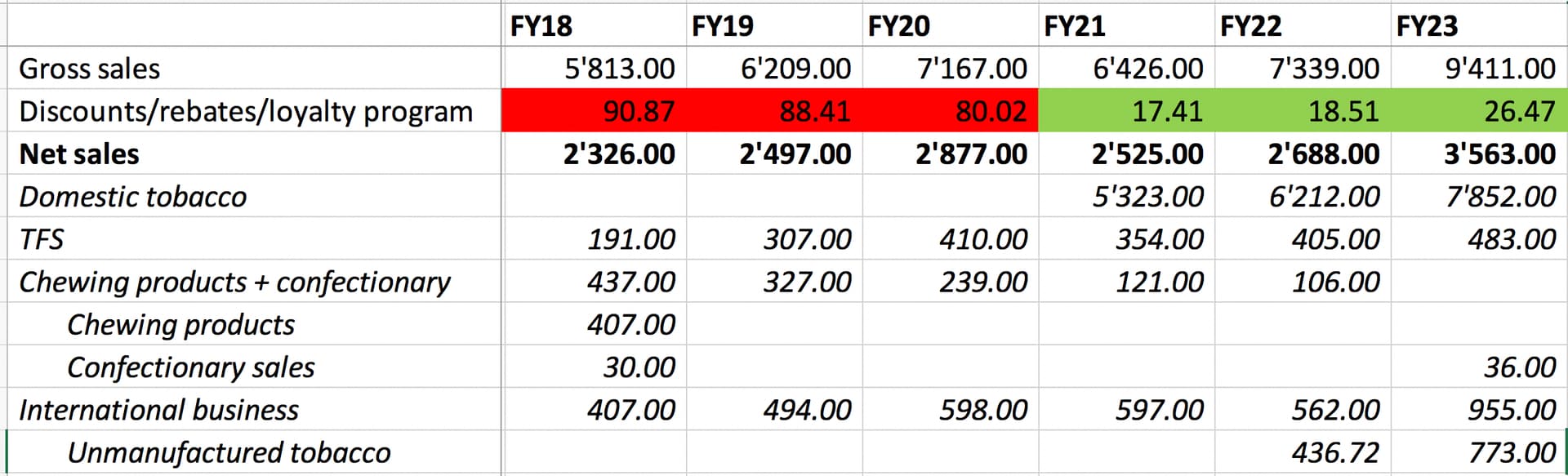

I have allocated 4% to buy Godfrey Phillips by allocating remaining 2% cash and reduced position in ITC to 2% (from 4% earlier). When I had exited Godfrey earlier in March 2023, this was the note I had shared.

Since then, Godfrey has continued reporting fantastic numbers with margins and growth being maintained. In last quarter, they reported their highest ever quarterly profits of 250+ cr. and looks set to report 1000 cr.+ profits in FY24. Just to give some context, they had 260 cr. annual profits in FY19, so there has been a 4x scalability in profits since 2019.

This large jump in profits has come on the back of reduced legal and advertising costs. Whats even more impressive is they have managed to grow despite reducing discounts/rebates. Generally, this is very uncommon for a FMCG co.

International business continues to be their growth driver with them benefitting from realignment of Russian supply chain. At their AGM, they mentioned that global tobacco cos like Phillip Morris are now buying more raw tobacco from Indian cos after the Russia Ukraine war. At 11’000 cr. market cap and a potential 1000 cr. PAT, I find them to be a very reasonable bet in this heated market. Cash comes down to zero. Updated folio is below

Core compounder (42%)

Companies

Weightage

NESCO Ltd.

4.00%

Eris Lifesciences Ltd.

4.00%

Ajanta Pharmaceuticals Ltd.

4.00%

HDFC Bank Ltd.

4.00%

HDFC Asset Management Company Ltd

4.00%

Gufic Biosciences

4.00%

Godfrey Phillips

4.00%

I T C Ltd.

2.00%

Aegis Logistics Ltd.

2.00%

PI Industries Ltd.

2.00%

LINCOLN PHARMACEUTICALS LTD.

2.00%

Caplin Point Laboratories Ltd.

2.00%

P.E. Analytics Ltd

2.00%

Aptus Value Housing Finance India Ltd.

2.00%

Cyclical (47%)

Companies

Weightage

Kolte-Patil Developers Ltd.

4.00%

Avanti Feeds Ltd.

4.00%

Alembic Pharmaceuticals Ltd.

4.00%

Amara Raja Batteries Ltd.

4.00%

Sharda Cropchem Ltd.

2.00%

Stylam Industries Limited

2.00%

Ashiana Housing Ltd.

2.00%

Ashok Leyland Ltd.

2.00%

Kaveri Seed Company Ltd.

2.00%

Sundaram Finance Ltd.

2.00%

Time Technoplast Ltd.

2.00%

RACL Geartech Ltd

2.00%

Manappuram Finance Ltd.

2.00%

ANUH PHARMA LTD.

2.00%

Shree Ganesh Remedies Ltd - PP

2.00%

Aditya Birla Sun Life AMC Ltd

2.00%

Dharmaj Crop Guard Ltd

2.00%

MAYUR UNIQUOTERS LTD.

2.00%

Godrej Agrovet Ltd.

2.00%

KSE LTD.

1.00%

Turnaround (2%)

Companies

Weightage

Punjab Chem. & Corp

2.00%

Deep value (9%)

Companies

Weightage

Geekay Wires

2.00%

Jagran Prakashan Ltd.

1.00%

D.B.Corp Ltd.

1.00%

Shemaroo Entertainment Ltd.

1.00%

Modison Metals

1.00%

RKEC Projects

1.00%

Worth Peripherals Ltd

2.00%

I have been very concerned about the state of Best Agro’s balance sheet and cashflow generation. Not only do they have large debt, but they also don’t generate any cashflows. P&L and balance sheet paints completely different pictures. On the other hand, Dharmaj has managed to grow while maintaining very strong control on their working capital. Also, I find their promoters very grounded and focused at their jobs.

Please search this thread to know my thoughts on diversification. I will not repeat the same thing over and over again.

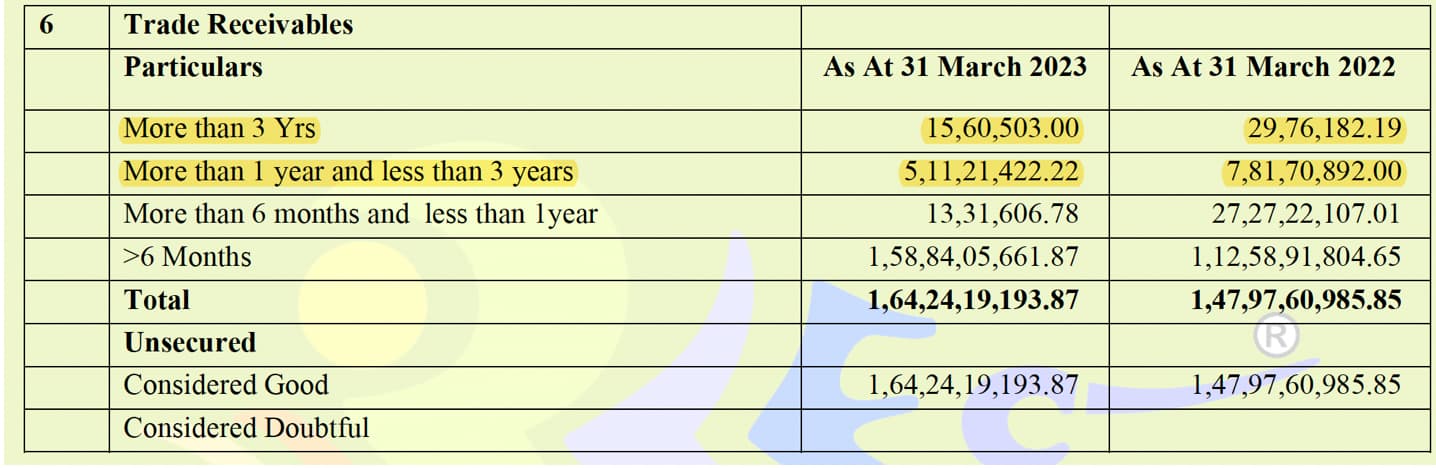

Ageing of receivables do not show anything very alarming (~3% older than 1 year).

If you carefully read their annual report, you will see that they paid 3.4 cr. interest on statutory dues which suggests they delayed these which might be due to liquidity constraints. Recently, I noticed in their EPFO filings that they have cleared large amounts of EPFO payments, and have become regular in their statutory deposits. This suggests that their liquidity situation is improving. In FY23, they also generated very good cashflows.

Additionally, they won a few arbitration orders which will further help them fund their projects. Their outstanding order book in March 2023 was around 1050 cr. which gives good visibility on revenues. Lets see how they are able to scale, current market cap of 170 cr. is quite small and captures a lot of risk.

Thank you so much for your posts, I look forward to them.

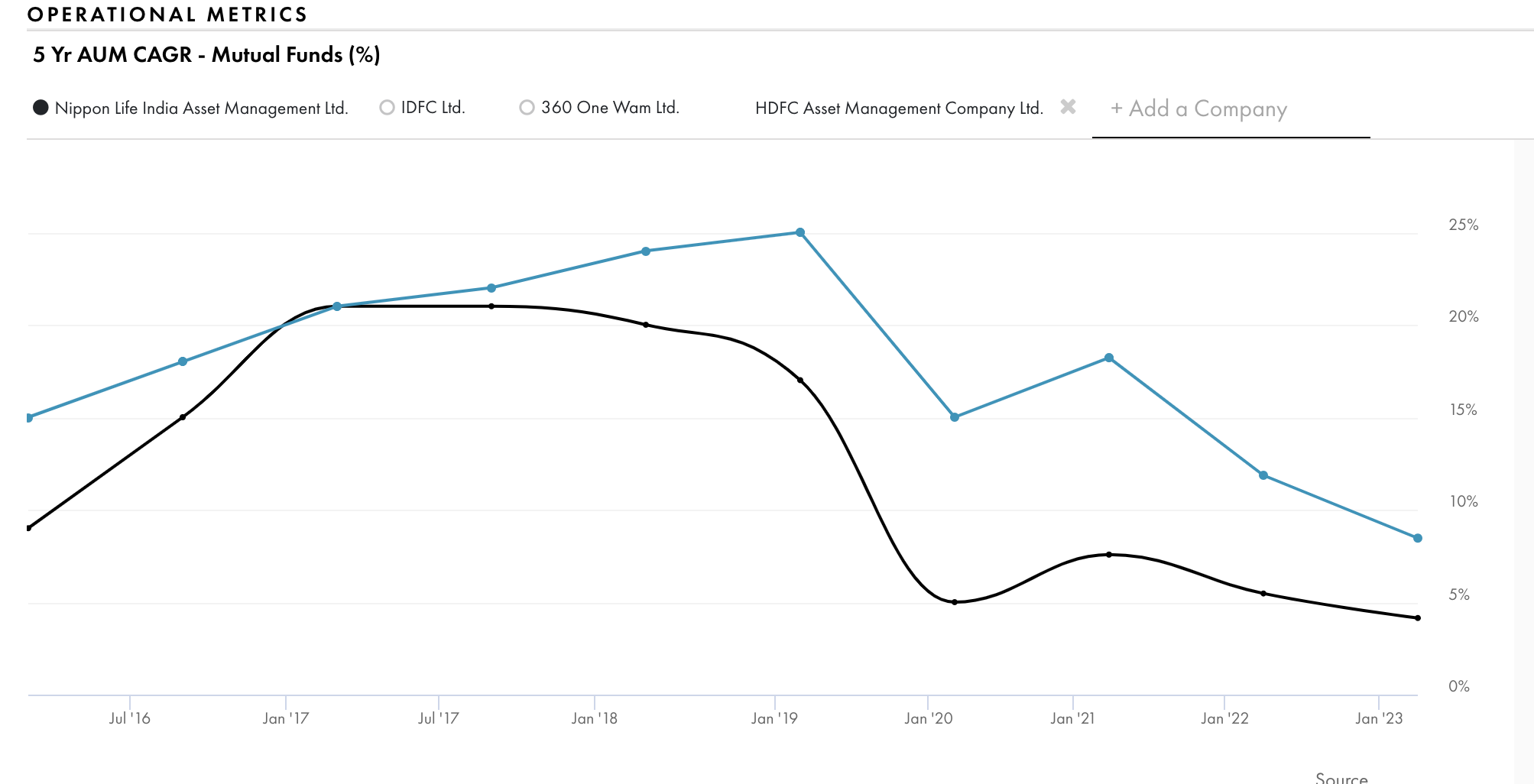

I am following AMC’s from quite some time.I am holding both Nippon and HDFC AMC.

I like Nippon more for the following reason.

1.Clear Leader in ETF products as of now, If we see US markets, three players control 90% of market (More liquidity brings more customers).

2.20-30% cheaper than HDFC and distributing entire PAT as dividend.

3.Performance of funds across various categories is among best across time frames.

4.SIP market share improved from 6.5% (June 22) to 8.3% (June 23), this will lead to market share improvement in coming quarters.

5.Equity AUM improving as % of total AUM (This is true for HDFC as well…They are leaders here).

Comparison of recent AUM data on closing basis.

1.Total AUM up for both by 66K CR in last 8 months (Nippon up by 23% while HDFC up by 14%).

2.Equity AUM up for both by 37K CR in last 8 months (Far higher growth for Nippon).

I agree that NAM looks like a good opportunity, given their MNC background which generally fetches higher valuation in Indian markets and strong recovery in investment performance. The broader investing style of NAM is value investing which is very similar to HDFC, and both have seen exceptional recovery in performances in past few quarters.

This being said, I feel bank backed MFs have a structural advantage over non-bank backed MFs (superior network). This is clearly visible in growth over longer periods of time. Until March 2023, HDFC AMC always had higher AUM growth.

Even from March 2023 to June 2023, HDFC AMC witnessed higher growth (@15% from 449bn to 516bn) vs NAM’s growth of 12% (from 295 to 329bn).

ETFs are very low yield commoditized businesses and most ETF money is driven by one large customer (EPFO). If we see a shift to ETFs over a long period of time in India, the entire industry profit pool will evaporate. Just as an example, I am also invested in a German asset manager who are leaders in ETF and passive products. This co trades at very low valuations. I try to buy them when their enterprise value becomes negative (meaning business becomes free) or their absolute dividend yield approaches 10%. I am worried if ETF trend picks up in India, consequence might be catastrophic for AMC businesses.

Hi Harsh RKEC projects has AGM on 27th I’m attending. Is there any specific questions you want me to ask?

I’ll ask about what growth they are expecting this year and in next years, is there any limiting factor to hinder growth like they talked about in last concall, how is the present liquidity condition compared to 2 years back, what is the ebitda margin they are expecting.