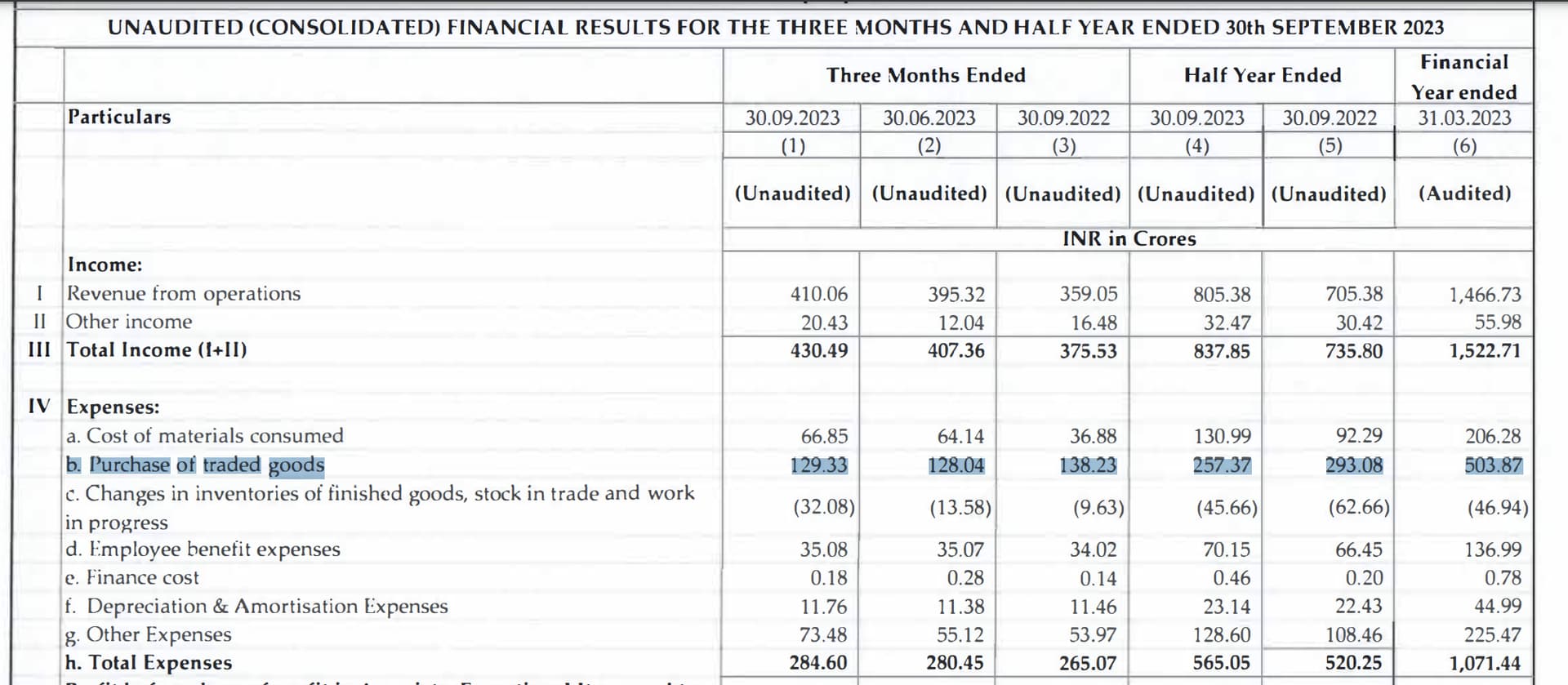

Another good quarter from the co, sales grew by 14% and EPS by 25%. They are in heavy investment mode, which will continue for the next few quarters. Concall notes below.

FY24Q2

- Large reduction in purchase of traded goods leading to better gross margins. However, guides for lower gross margins going forward

- Profit share for Caplin Steriles: 30% with 70% coming from product supplies. Made 12.5 cr. EBITDA in H1 as they are expensing out all R&D and filing expenses. Core business has same margins as standalone (if R&D/filing expenses are removed)

- LATAM revenue breakup: Wholesalers 55%, Direct to Retail 25%, Institutional 20%

- Mexico expansion: want to replicate LATAM model where they sell via smaller distributors. Meaningful scaleup will require atleast 2 years and 100 products

- Tied up with third party manufacturers (2 Indian + 1 Chinese) for supplying penicillin and cephalosporin range of products in Mexico

- Plan to launch 15 own-label products in US in next 1 year

- Niche products in USA: filed 3 Ready-To-Use Bag products, filing Suspension Injectables, Emulsion Injectables, Emulsion Ophthalmic and Plastic Vial injections

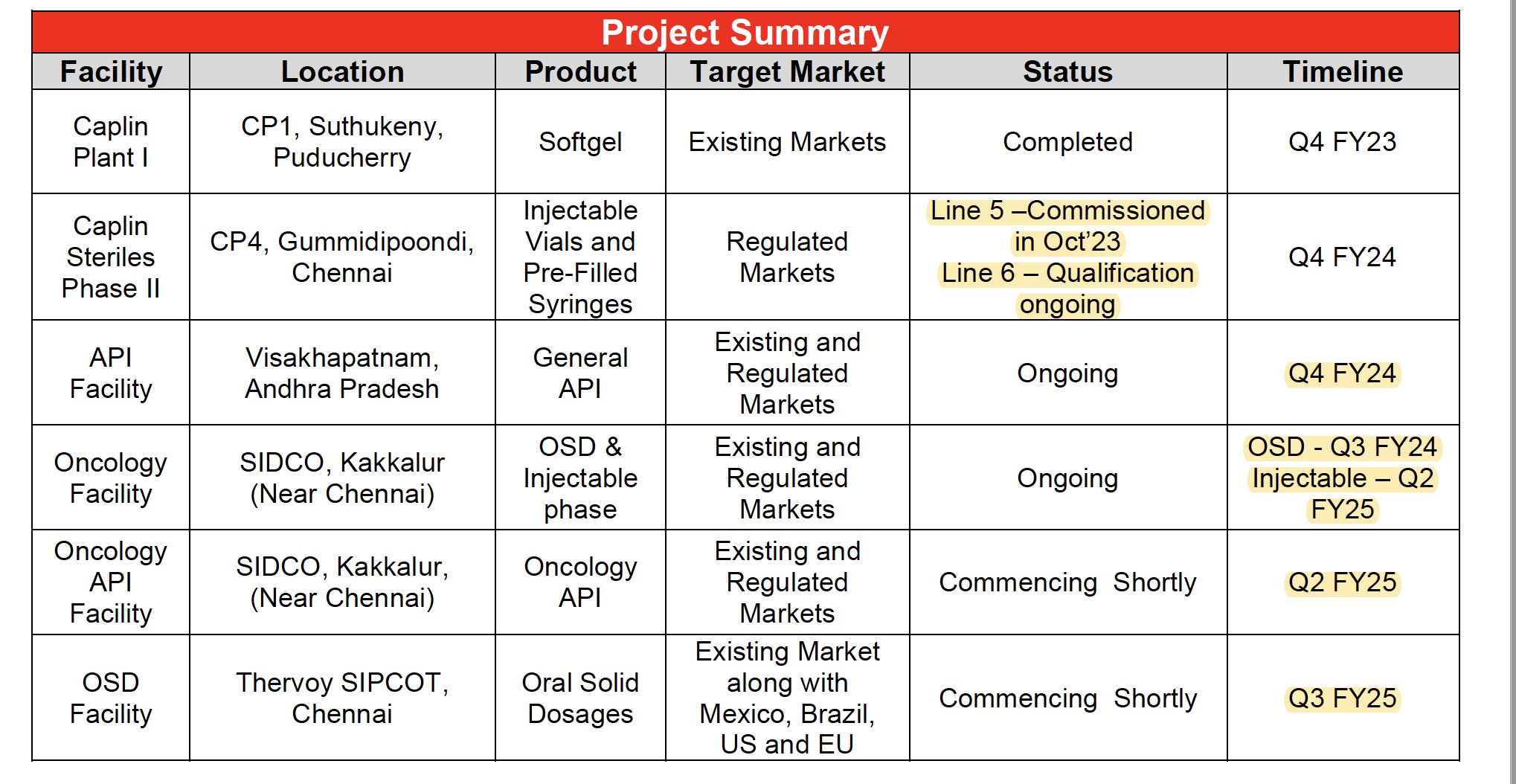

- Injectable facility will cater to non-US market as well, filing completed for multiple products

- Planned capex: 600-650 cr. (more than half has already been spent)

- High speed vial filling line commercialized (will be replacing other line as the new Bosch line is 2-2.5x faster)

Disclosure: Invested (position size here, no transactions in last-30 days)