We need to differentiate between cells and battery packs. While some OEMs may keep battery packs in-house, very few OEMs go backward to make their own cells. The value proposition of Amara/Exide is that they will manufacture cells at scale. Battery packs are anyway very low value addition.

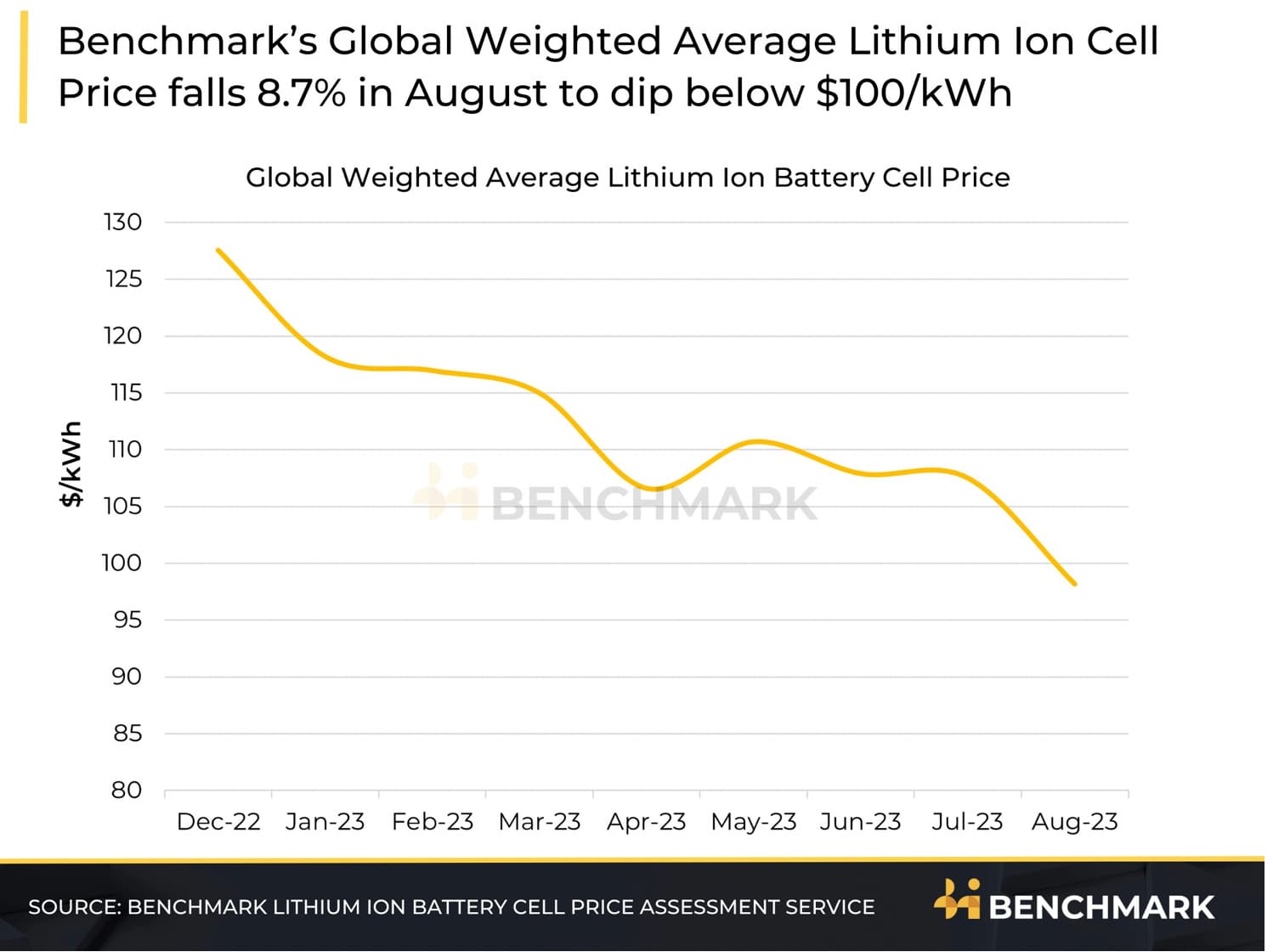

The larger risk for cos like Amara/Exide is that they may not be the lowest cost manufacturers of cells, as the Chinese have already built economies of scale. At a cell price of $100/GWh and 2GWh capacity, Amara expects fixed asset turns of 1.4-1.5x and gross margins of 25-30%. If for some reason, cell prices come down (as have been coming down in recent months), the entire value proposition goes for a toss.

They are not putting up any investments for this, as manufacturing will be outsourced. They are simply leveraging their existing dealer network to try and grow sales. This is akin to FMCG cos introducing new products at minimal costs, if it works out they can manufacture in-house at some point, if not it was atleast worth a try.

They will be manufacturing cells, which can then go into battery packs for EVs/storage centers/telecom tower/etc. Amara is anyway the leader in storage batteries used in telecom sector with a 60% market share.

Shouldn’t have any impact, Johnson control divested their battery division to private equity and haven’t been investing much in lithium ion batteries. It doesn’t have any impact on Amara’s business.

Related party issues used to a pain point in 2012-15, but of late Amara has been trying to rectify these. All these mergers are being done at very reasonable valuations (7x EV/EBITDA for Mangal, 6.5x for Amara Power systems). Also, the way its been done allows promoters to increase their shareholding in the co., which is quite low.

Disclosure: Invested in Amara (position size here, bought shares in last-30 days)