One fundamental question – looking at the percentages, they seem to be at cost. Shouldn’t one track the portfolio at Mark To Market, rather than at cost? This gives a misleading picture and may lead to incorrect decisions I feel.

3 Likes

The FMCG and agri divisions are growing well, their tobacco business is a free cash generator, valuations are reasonable. Also, they have a very very long track record of being profitable and dividend paying while growing at higher than nominal GDP rates. The diverse business profile provides a lot of downside comfort making ITC more than a one trick pony. My expected IRR is 30%+, that’s why the high allocations. Lets see how future unfolds.

Of course valuations! In the past, I have made money on both HDFC AMC and Nippon Life despite Nippon being a bit inferior in terms of business performance (which was reflected in valuation differential). My expected IRR from HDFC AMC for a 4% allocation is much lower (~19%) than from an Aditya Birla (~26%). That’s why 4% allocation for both.

Its not at cost, it MTM. The model portfolio is supposed to be a guide as I allocate fresh capital on a continuous basis. I let most portfolio positions vary by ±2% from target weights. Recently, I have started the practise of only adding to positions whose weights have fallen but not trimming positions whose weights have increased slightly (mostly to reduce churn and reduce transaction costs and taxes).

12 Likes

Hi was going through ur portfolio and setup and all details are beautifully explained.

Can you please guide in hw to find the forward price and hence deduce the total returns . I am new to investing and learning phase and trying to understand more on value buy, growth buy and fundamental analysis

Hi Harsh! What’s your rationale behind choosing Ashiana Housing than someone like Ahluwalia Contracts which has a more Diversified and large Book order, better financial strength and more reasonable valuations?

Hi Harsh

Did you come across EKC, which is a focused play on cylinders? Time Techno is kind of diversified product basket that has cylinders in it.

If you come across such scenarios how you break down your thesis and decide which one to choose ?

I am more curious to understand your approach.

Many Thanks

1 Like

I have explained my thought process for a few companies, you can look at them. Also, I would not call this system perfect, these are back of hand calculations and guesses. Below are some examples of my speculation for a few growth companies.

About value buys, the post below summarizes my thoughts.

Both are part of different industries, Ahluwalia is an EPC player and Ashiana is a pure residential developer. The underlying business models are completely different.

I haven’t done much work on EKC. A quick look at their balance sheet shows that they have rapidly deleveraged in the past few years. I don’t have anything meaningful to contribute here.

Over the past few months, I have been working on the domestic agri value chain and will share my understanding in the next post. This hopefully will also clarify my thought process about such opportunities.

1 Like

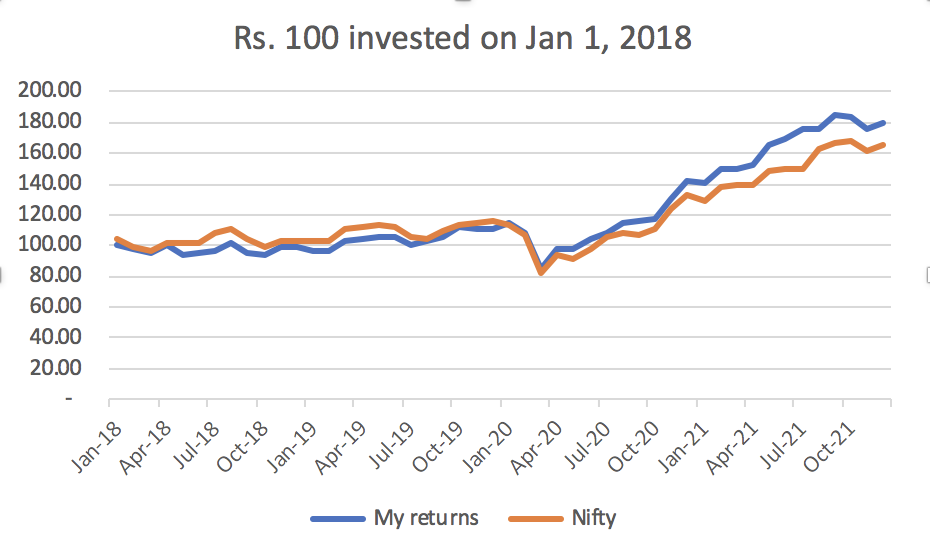

Its now been close to 4 years since I have maintained my investing records, the performance according to calendar years is shown below.

| Calendar year | My returns | Nifty returns | 100 invested in Harsh folio | 100 invested in Nifty |

|---|---|---|---|---|

| 2018 | -0.63% | 3.15% | 99.36629809 | 103.1512625 |

| 2019 | 11.83% | 12.01% | 111.1261021 | 115.5428994 |

| 2020 | 27.18% | 14.89% | 141.3329775 | 132.7468312 |

| 2021 | 27.30% | 24.12% | 179.9159566 | 164.7644355 |

A more granular performance (on monthly returns is shown below).

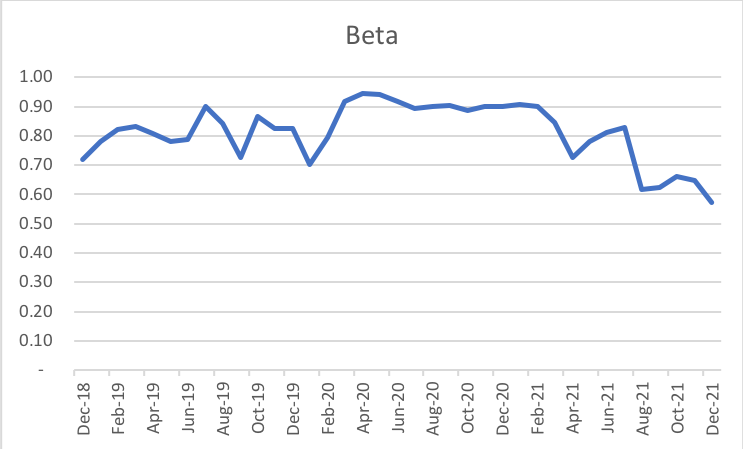

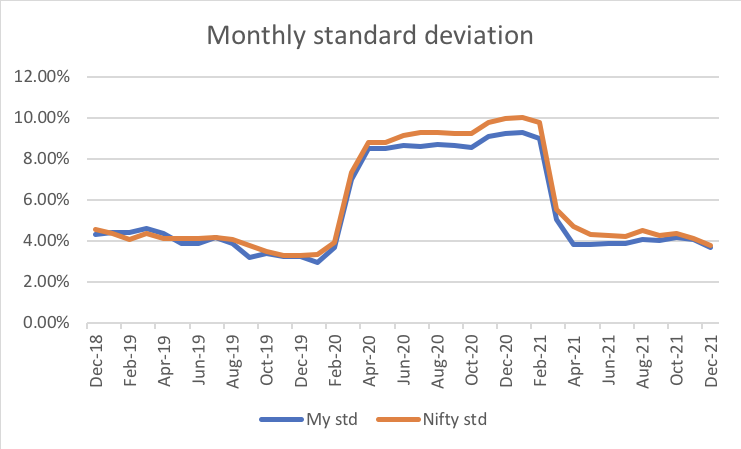

I have managed to outperform nifty over this period, with CY20 being the year with maximum outperformance and CY18 being the year with maximum underperformance. I also track other features of my portfolio. My portfolio beta has decreased over time (computed on monthly data with 1-year lookback).

This is mainly because of increasing divergence of my returns with Nifty returns as a result of more bottom-up stock picking. This is clearly shown in the standard deviation chart which has not shown any significant divergence. It has always been slightly lower than Nifty consistently.

One feature that stands out in the above chart is how volatility regime changed in CY20 and is now back to normal. In changing regimes, there are lots of stock specific opportunities (so called stock picker market). This was also the time when my portfolio performance diverged the most against Nifty. We are now back to the normal volatility regime.

Over a long term period of time, I want higher returns with lower volatility and this has been achieved thus far. Lets see how things happen going forward. Wish everyone a very happy new year and loads of success in life.

48 Likes

Thanks for sharing. May I know how you keep track of your returns?

1 Like

Hi Harsh, any write-up on Aegis?

")

5 Likes

As of today, I have created 2% position in Shri Jagdamba Polymer. The key rationale is beautifully captured in the thread below. With 360 cr. in FY22 revenues, PAT should be somewhere around 55 cr. (adjusting for foreign currency fluctuations) making it kind of fairly valued (~15 P/E). They are growing very well without any dilution and I want to see how this story plays out. The key risk is that of information availability. Cash levels have come down to 5%. Updated portfolio is below.

Core compounder (60%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 8.00% |

| Housing Development Finance Corporation Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Manappuram Finance Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| Aegis Logistics Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Aditya Birla Sun Life AMC Ltd | 4.00% |

| HDFC Bank Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| Control Print Limited | 2.00% |

| Shri Jagdamba Poly | 2.00% |

Cyclical (16%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 4.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| SWARAJ ENGINES LTD. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

Slow grower (6%)

| Companies | Weightage |

|---|---|

| Cochin Shipyard Ltd. | 4.00% |

| Power Grid Corporation of India Ltd. | 2.00% |

Turnaround (6%)

| Companies | Weightage |

|---|---|

| CARE Ratings Ltd. | 4.00% |

| Lupin Ltd. | 2.00% |

Deep value (7%)

| Companies | Weightage |

|---|---|

| SJVN Ltd. | 1.00% |

| ATUL AUTO LTD. | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Time Technoplast Ltd. | 1.00% |

| RACL Geartech Ltd | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

8 Likes

@Rafi_Syed: I am summarizing my understanding of the agri value chain, mainly focusing on agrichemical companies dealing with insecticides, fungicides, herbicides, and plant growth regulators. I am not including seeds or tractor companies.

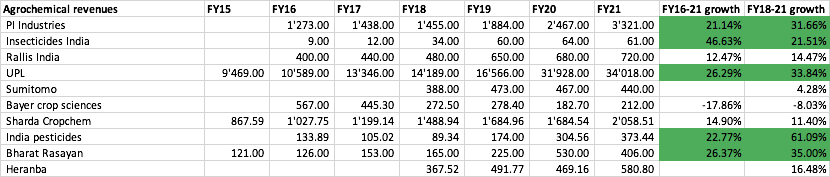

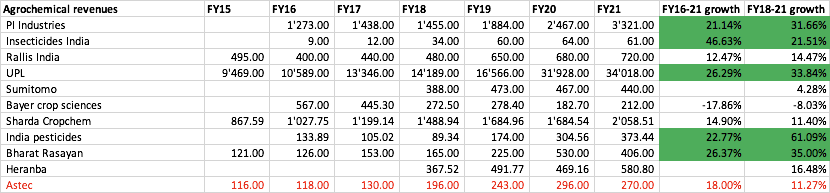

1. Domestic marketing companies: Traditionally, Indian agrichem companies would forge partnership with innovator MNCs (mostly Japanese, American and European) to launch exclusive products, whereby active ingredients (AIs) were procured from the MNCs. In this so called in-licensing arrangement, Indian companies would pay royalty on sales, in addition to buying AIs from the MNCs. A number of Indian players adopted this strategy (Rallis, Insecticides India, Dhanuka, etc.). This strategy is asset light in nature as formulation mostly involves mixing of different ingredients in a given proportion (making fixed asset turns of 8-10x). However, the downside of this strategy is that its not scalable beyond a given point (around 1’300-1’400 cr. of domestic sales). Here is domestic agchem revenues of large agchem players.

Its very clear that all Indian companies (PI, Dhanuka, Insecticides, Rallis) have struggled to scale beyond 1’300-1’400 cr of domestic sales. MNCs who have a larger product offering due to their global R&D along with better brand recall (I am considering UPL as a MNC here) have been successful in going beyond 2000 cr. Bayer numbers look very high because it includes Monsanto’s seeds business, for UPL ~10% contribution would be seeds (so domestic agchem would be ~4000 cr.).

Once a large domestic scale is reached, companies face usual vagaries of monsoon, government policy, etc. making sales growth in-line with nominal GDP growth. However, this business is super capital efficient as shown in the return ratios of companies like Dhanuka (30%+ ROCEs leading to high dividend payouts and buybacks).

2. Exporters of AIs: In the last few years, this space has garnered a lot of attention due to shift of market share from China to India. A large number of companies have been doing well here. There are largely two business models that exist here, i) Export of generic off-patent AIs and (ii) Export of patented AIs by collaborating with MNCs. In the second category of patented exports, PI is the only successful player with some others like Bharat Rasayan and Astec Life trying to crack this business model. This line of business is very sticky and high margin in nature. Below is agchem exports of major Indian companies.

Generic or patented, exports have grown for everyone. Even MNCs such as Sumitomo have started using India as their base to manufacture AIs. Fastest growth players (20%+ sales growth) are Bharat Rasayan, India Pesticides, PI Industries, UPL (through acquisitions), Insecticides India (although on a small base). If we only consider off-patent AI exports, most players have scaled to 400-600 cr. kind of annual sales. PI with its unique business model has scaled beyond 3’300 cr. and is in a very different league.

In this business model, capex is of utmost importance making it capital heavy unlike domestic formulators who only need to setup a strong marketing engine.

3. Global marketing companies: Global agchem marketing companies build a portfolio of finished formulation of agrichemicals by registering in different countries, and sell them as per demand from the respective countries. Two such listed companies are UPL and Sharda Cropchem, who derive a significant proportion of revenues through outsourced manufacturing. Sharda Cropchem has a unique business model, where they do not manufacture AIs or formulations but procure it from different suppliers and supply it as per demand from various markets. Sharda has grown sales at ~18%+ rates over the past decade. In this business model, money is spent in registering products which is both time consuming and expensive (3-30 cr. per product depending on the geography). Once a company has a large portfolio of registered molecules, their job is to procure from manufacturers according to demand schedule and manage working capital. So capex is in form of molecule registration (and not machinery management) and working capital management is important to generate reasonable cashflow (to fund further registration). This business has very good economics (20%+ ROCE). To showcase how scalable a marketing business can be, revenue per employee for Sharda is ~13.69 cr. in FY21 (vs 0.42 cr. for HCL Tech and 0.32 cr. for TCS).

Here’s the summary of the three business models

Domestic marketing: High return ratios + asset light + strong working capital management + limited growth (beyond 1’300-1’400 cr.)

AI export: Asset heavy + Product concentration risk + strong growth with a large market (PI has scaled to 3’300 cr.+) → return ratios is a function of product profile

Export marketing: High return ratios + very high registration costs + strong working capital management + strong growth with very large runway (UPL has scaled to 34’000 cr.+)

Now lets see how market is currently valuing these business models.

Domestic focused companies: Market values MNCs much higher than Indian players. Sumitomo, Bayer trade at 25x+ EV/EBITDA and 5+ EV/sales (basically at branded FMCG kind of valuations). The remaining (Rallis, Insecticides, Dhanuka) trade at 1-2.5x EV/sales or 10-20x EV/EBITDA.

AI exporters: These are currently in market fancy and trade at 5x+ EV/sales or 20x+ EV/EBITDA. Also, these companies as a group (PI Ind, Bharat rasayan, Astec Life, India pesticides) have shown higher growth rates than domestic focused companies (so premium valuation is for a reason). In this lot, the cheapest companies are Meghmani Organics and Heranba and that has to do with corporate governance doubts in the minds of market participants.

Global marketing: Both UPL and Sharda Cropchem trade at very modest multiples (9x EV/EBITDA for UPL and 5.5x EV/EBITDA for Sharda). Similar to generic pharma, market is currently not assign a high multiple for formulation exporters. I find this to be the most opportunistic space because both UPL and Sharda are growing at high rates (15%+ sales growth) and are not in fancy (UPL probably because of governance doubts and Sharda because of their different business model which involves intangibles and is clearly not understood by the market).

My approach

Clearly the most exciting space (in terms of growth) is that of exports. In AI exports, I like PI’s business model the most. However due to high valuations, I have reduced my allocations over time (from 6% in 2018 to 2% currently). Bharat Rasayan is also at an interesting juncture, if they are able to crack the MNC business (like PI did) their valuation might expand. In terms of new listings (India Pesticides, Heranba), I find India Pesticides as more interesting. However, in the paucity of a public market track record, I will prefer Bharat Rasayan (as both are trading at similar valuations).

My bigger bet is on Sharda Cropchem which is growing at very high rates and have built in operating leverage (in terms of higher possible sales per molecule). Also, their margins are at decadal low levels, so a revival in margins will have disproportionate impact on earnings (and they are cheap even at current margin earnings). So Sharda can benefit from margin expansion + multiple re-rating, that’s why my higher allocation.

This is a very rough mental model that I have built, I will be very happy to discuss more specifics and dive into more granular discussion.

60 Likes

I would love to hear your views about Astec Lifesciences which is also in the field of herbicides/fungicide and at an interesting juncture as founding promoter will be leaving by March end giving complete control to majority shareholder Godrej (who are bringing in professional managment - ex Navin Fluorine guy).

As Sharda cropchem and other asset light players get affected by petroleum prices, we need.to watch it. If recent jump in crude prices and subsequent cooling indicates players like sharda cropchem are going.to be in fancy. Threat of hike in US interest rate should keep crude prices in check.

Disc: No holidings, used to track Sharda Crop

1 Like

Astec Lifesciences has delivered lower sales growth compared to its peers. Given their business model, I consider their peers as Insecticides India, India Pesticides, Bharat Rasayan and Heranba. Also, their margins have been quite volatile which might be because of their limited process expertise (mainly an expert in triazole chemistry leading to product specific risk) and raw material procurement from China. I like Bharat Rasayan more than Astec.

Also, Astec is mostly a fungicide company, and only now getting into herbicides (which is the largest segment globally). About Godrej being promoter, its both a good and a bad thing. It gives them access to cheaper capital (in terms of ICDs) but also brings in a different kind of corporate culture than a hungry entreprenuer driver company.

7 Likes

Hey Harsh, Do you see a revision on the projections based on the spectacular turn around Sharda have posted during Q3.

Growth has been very strong in the last 4-5 quarters, and is way higher than my own expectations. This calls for revision of estimates, I revisit most of my estimates at the end of a fiscal year. So I will do the detailed calculations at the end of FY22.

At the current growth trajectory, Sharda should end FY22 with sales of ~3600 cr. and management is guiding for 20% volume growth beyond that. This would imply they are trading ~1.25x EV/sales (on FY22 sales) which is still one of the cheapest (after Insecticides India). My thesis is built on strong sales growth + possible margin expansion. If current quarter gross margins of 33-34% are sustainable, it would imply PAT margins of 12%+ which means they are trading at 11x P/E on FY22 numbers. This is quite cheap for a business growing sales at 20% levels. I am happy to hold it as long as growth continues.

4 Likes

@harsh.beria93 - how do you see Q3 results for Eris. Added here

1 Like

You summarized it perfectly, nothing exciting nor dull! They are growing at faster rates than IPM, Q4 has a large number of product launches which can boost growth in the coming quarters. Its a cashflow and margin focused management, and is a better alternative to MNC pharma who are also cashflow and margin focused (but don’t have same growth ambitions).

9 Likes