Shri Jagdamba Polymers Limited

BACKGROUND

A technical textile solutions company with humble beginnings manufacturing plastic products like HDPE/PP Fabrics & Woven Bags at Dholka (rural Ahmedabad) in 1985. Today the company employs 1700 employees and its yearly production is approx. 20,500 MTs of finished polymer based products.It’s mainly an exports company with very little domestic business.

MAIN PRODUCTS/SEGMENTS

The company is engaged in the business of technical textile, geotextile, and other allied products like manufacturing of PP/HDPE woven and non-woven fabrics and bags. Its products comprise PP Woven bags, fabric, box bag, ground cover, and lumber cover, mainly in the woven polypropylene market.

During FY2021 AGM, the management confirmed that it manufactures a building product for the US housing market in the form of Synthetic Roofing Underlayment.

If one carefully looks at the cover pages of the company’s past annual reports, for the first time in the FY2021 annual report, the management showed pictures of a house under construction with roofing underlayment and house wrap as their main products. In earlier years the company has always been showing silt fence, geotextile, and agri textile application pictures.

Below is the screenshot the latest AR cover page:

MAIN MARKETS/CUSTOMERS

SJPL is mainly an exporting company.

Almost 85% of the revenue contribution comes from the exports market.

The company doesn’t give any further breakdown of their sales.

As per our industry scuttlebutt, US is the biggest market for SJPL’s building product i.e. Synthetic Roofing Underlayment which it serves primarily through Epilay Inc and Edge Tech Partners LLC, and few much smaller players.

CURRENT MARKET/INDUSTRY TRENDS/SCUTTLEBUTT FINDINGS

Through scuttlebutt work we have confirmed that the roofing underlayment industry is going through a shift from Organic Felt (waterproofing tarp, saturated bitumen felt, asphalt felt) to Synthetic Underlayment. This migration started happening from about the 2011-12 period. Currently about 40% of the industry roofing contractors are still using the asphalt based traditional underlayment. And this shift is happening at a faster rate post COVID which is very positive for players like SJPL.

Two big problems with legacy underlayment products were 1) it was too heavy for roofers to carry to the roof 2) it was slippery as roofers laid the underlayment felt and walked on top of it to nail it down and prepare for adding the next layer on top of it. These are the two issues that were being addressed by the synthetic underlayment product for the roofing industry.

US Synthetic Underlayment market size is expected to be in the range of $1B to $1.5B. There are mainly two kinds of players in the Synthetic Underlayment roofing industry. 1) Branded full package (warranty) solution providers 2) Discretionary roofing solution providers who try to give the best solution at least possible cost, with or without warranty. Full package sellers are big branded players like GAF, Owen’s Corning, Dupont who give full warranty for all the layers of roof as a package. Generally there are 3-4 layers of roofing that goes into the making of a roof. Hence they command premium pricing. And most of them get their underlayment manufactured from India/China. Discretionary players sell only one layer in the form of synthetic underlayment.

Top 5 players command ~50% of the market and 45-50 players comprise the rest of the market. As mentioned before GAF, Owen’s Corning, Dupont are the biggest players dominating the market under full roofing package and full warranty business model.

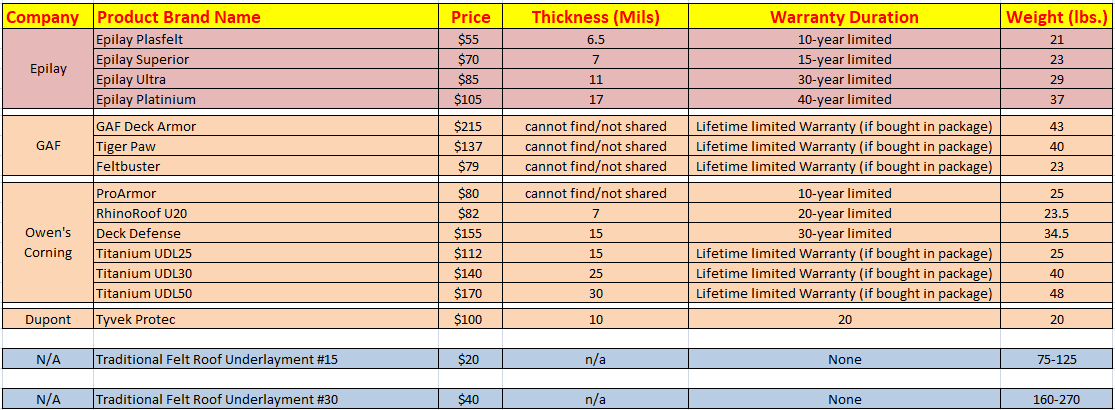

Below table gives product specification and pricing comparison of underlayment players:

Roofing contractors compare products mainly by price and thickness; more the thickness better the protection.

GAF, Owen’s Corning (OC) and Dupont are well established players serving the US roofing industry for decades. OC is a public company while GAF most probably is a private business. GAF’s main business model is to sell underlayments as part of a full roofing package with full warranty, hence premium pricing. GAF & OC’s lifetime warranty products are not directly comparable with Epilay’s products due to different business models but we can get an idea of how big the price difference is for similar underlayment with warranty being the main differentiation.

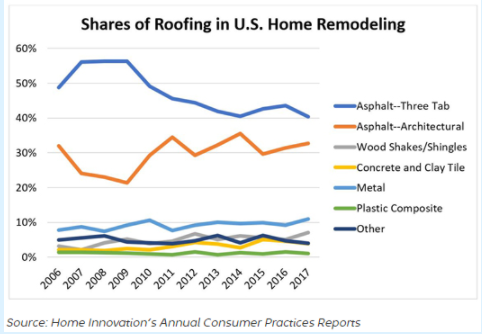

Asphalt Roofs Dominate US Home Roofing

Source: Home Innovation Roofing Market Trends

Asphalt shingles are used in more than 80 percent of home roofing and re-roofing projects in the United States. Regardless of the type of roof, underlayment will always be needed. But this is just to give an idea of roofing type breakdown.

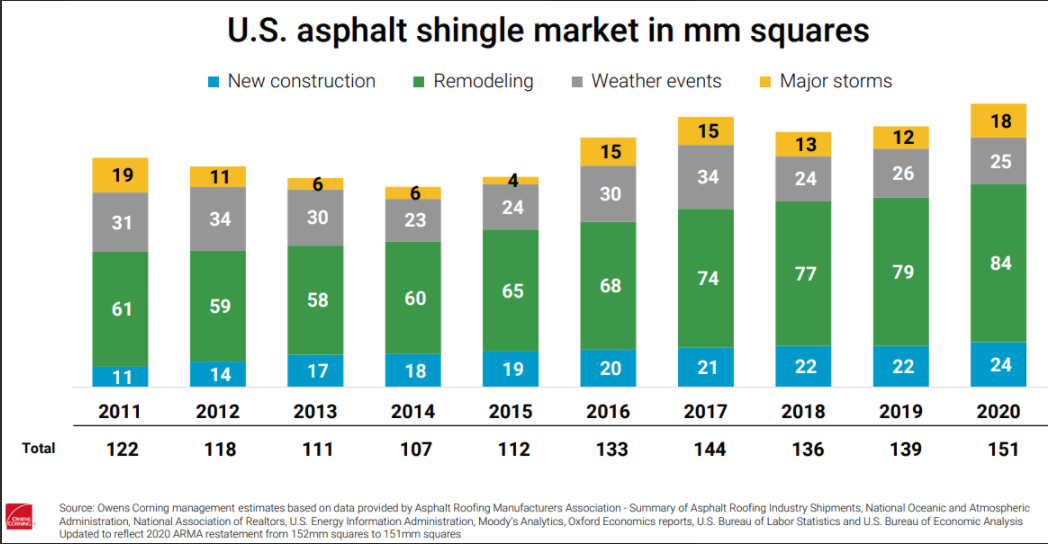

Source: Owens Corning Q3 Presentation (slide #27)

New construction demand annually has been around 15% of total asphalt shingle demand. Major portion of roofing demand comes from remodelling, weather events and storms. Most of the remodelling demand is likely non-cyclical. This slide indirectly confirms an industry expert’s assertion that the replacement market is the main market, and not new construction.

Miami-Dade County Data

The Miami-Dade County Product Control Approval System allows new and innovative ideas to be developed into practical, lasting and safe products. This approval process is recognized at both the national and international level. Product Control’s approval designation — Notice of Acceptance or NOA — has been recognized and accepted in Hawaii, Japan, South America, Guam and the Caribbean. The Product Control Approval System establishes a protocol to evaluate the standards of products used in construction in Miami Dade County. Miami-Dade County, with its inclusion in the High Velocity Hurricane Zone (HVHZ) has the most stringent code requirements of the Florida Building Code.

Source: Miami Dade Country Construction Materials standards

Roofing Underlayment sellers in the US need Miami Dade County NOA to be able to sell their products in the state of Florida and also in the US. There are about 36 sellers referenced in their website database who have their synthetic underlayment approved with Miami Dade County. Their products are manufactured mainly in China, India, and some in Canada.

Big companies like Dupont, Owen’s Corning, and others get their big brand underlayment products manufactured in India. Owen’s Corning in Silvassa and Dupont in Dadra. Ahmedabad/Dholka seems to be a big hub for the Polypropylene and Flexible Intermediate Bulk Container (FIBC) market. There seems to be other manufacturers in the Dholka area apart from SJPL like Veer Plastics Private Limited. [Scope for further scuttlebutt in India].

Roofing contractors are the final decision makers as to what underlayment goes into as part of the final installation of a roof depending on end customer warranty choices. Roofing contractors buy their underlayments from the distributors who ultimately stock up the products of various brands.

BULLISH VIEWPOINTS

-

FY2018 has been an important pivotal year for SJPL because it’s business performance has improved considerably since then. Prior to FY-2018 it’s EBITDA margin was in the range of 10%-12% which increased to 16%. Since then it’s EBITDA margins have increased above 20% for TTM ending September 2021. It’s sales have more than doubled in the last four years.

-

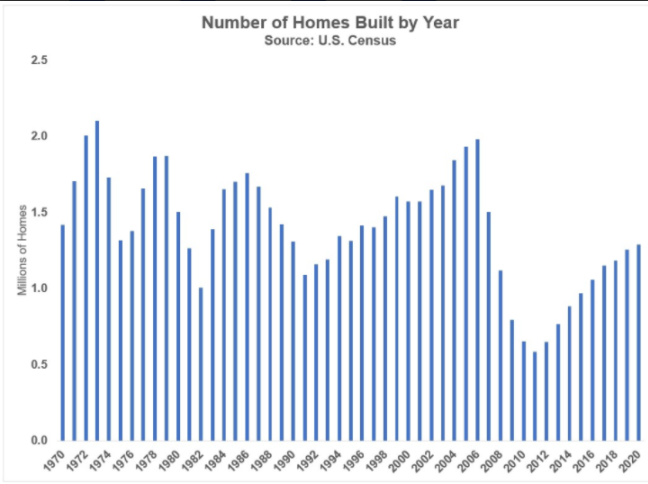

Current U.S. Housing Cycle has been going through a strong growth uptrend since 2010. About 500,000 homes were built in 2011 which has increased to about 1.3mn in 2020. Recovery since the 2008 crisis has been very smooth and consistent. Overall US construction spending has also followed a similar trajectory for both residential and non-residential segments.

Source: Construction Spending US Census Bureau

-

US construction spending has been growing at about 4.8% CAGR in last 3 years. SJPL started selling Synthetic Roofing Underlayment from FY2018 and since then their sales are growing at about 13% CAGR. SJPL doesn’t share breakdown of their sales, however, we strongly believe that their Synthetic Underlayment segment sales is growing faster than the industry which is contributing to growth in market share.

-

Industry going through migration from asphalt based underlayment to synthetic underlayment. About 40% of the roofing contractors are still using asphalt based underlayment which is shifting to synthetic at a very fast rate, especially post covid.

-

While lot of players can and do manufacture roofing underlayment products competitively, selling in developed markets like US is tough, and totally dependent on local distribution strength/branding. Manufacturer - Distributor relationships seem deeply entrenched with very little incentive for distributors to switch vendors. SJPL’s biggest customer in the US, Epilay is growing at a fast rate and penetrating well in the US roofing market. It has a strong distribution network and sales team. It attends all major roofing exhibitions in the US, and carries out aggressive marketing campaigns and promotions for brand awareness.

-

Given roofing contractors are the final decision makers for what type of underlayment goes into the roofing installation - their main concern is to provide best quality at cheapest possible cost to end-customers who’s main interest is in the length of warranty they get for their roof. As seen from above pricing comparison table - Epilay provides warranty on all of its products at half the price, as compared to the full package solution brands. There’s incentive for more roofing contractors to shift towards offerings like Epilay’s which will in turn benefit SJPL.

-

SJPL has been a consistent performer from a business standpoint. Very impressive Sales & Profit growth over last 5 and 10 years.

Source: Screener.in -

Management has guided for a 370-380Cr topline for FY2022 and decision on further CAPEX in FY22-23. SJPL did sales of 239 Cr in FY21.

-

Since bulk of the demand is replacement driven, new construction cycles have minimal impact on the overall demand.

-

Customer-driven value migration to higher-end building construction products is a distinct possibility

BEARISH VIEWPOINTS

-

SJPL’s current capacity may provide growth for next 1-2 years. Beyond that SJPL growth visibility is clouded as the management has not provided any timeline for new capacity expansion plans, as yet.

-

SJPL promoters have another unlisted entity Shakti Polyweave Pvt Ltd (SPPL) in a similar line of business with same product lines.

-

Unlisted entity has 1.5x the capacity as compared to the public entity. Future capex could possibly get diverted to private entity, at the expense of SJPL.

- SJPL - 20,500 MTPA

- SPPL - 32,000 MTPA

-

Typically low barriers to entry with high competition and no bargaining powers with the distributors and end customers. However, difficult to envisage main long-term customer Epilay, switching vendors.

-

There is very little product differentiation between the players in the industry. Everyone is making almost the same type of underlayment but packaged differently and wrapped with different warranties. It’s a commodity-plus business. However, the lowest cost producers/sellers can win market share which seems to be the case with SJPL and its customers in the last few years.

INTERESTING VIEWPOINTS

[TBD]

BARRIERS TO ENTRY

-

Barriers to entry for manufacturing the underlayment are low. Anyone with decent pockets can come in and set-up the manufacturing facility for synthetic underlayments. SJPL expanded its capacity from 12,000 MTPA to 20,500 MTPA in 2020-2021 at a cost of Rs. 46 Cr. SPPL recently expanded its capacity from 22,000 MTPA to 32,000 MTPA at a cost of Rs. 68.10 Cr.

-

Although someone with decent pockets can come in and set-up a manufacturing facility, but getting the right combination of a synthetic underlayment product and nailing down the final product can take upwards of 2-3 years. To quickly get the right product combination, it’s imperative to have people with deep polymer and polypropylene expertise.

-

Being able to manufacture required product isn’t enough to get one past the goalpost in developed markets. Barriers to selling the product in the US is very high. Having a recognised brand which has a wide distribution network in the US takes time, money, and consistent investment in market development. SJPL’s biggest customer in the US has got a strong brand and good sales & marketing team for pushing their products.

-

Synthetic underlayment products need to be approved at County and State level in many of the states of the US. Getting such approvals is a lengthy and cumbersome process as it can possibly take about 1-2 years.

BUSINESS MODEL

Business model of SJPL is very straightforward. To be the least cost producer of the synthetic underlayment and other products that it makes and enable its customers in the US to be least cost sellers for them to compete with the large brands who provide full roofing package solutions.

VALUATION MODEL

On a TTM basis, SJPL is available at ~14.5x PE given current market cap of Rs. 818 Cr.

If SJPL were to deliver a topline of 360-370cr for FY22 with current margins sustaining, it could possibly deliver a bottom line of around 65 Cr. This gives us a forward PE of 12.6x.

CORPORATE GOVERNANCE SCAN

Promoters having a private entity which runs a similar line of business is the biggest red flag for this story. Since SJPL has grown at a very consistent pace in the recent past, it gives some comfort that the management might continue to invest in both SJPL and unlisted SPPL, without prejudice to either.

RED FLAGS/FORENSIC SCAN

[TBD]

DISCLOSURE(s)

Amit Rupani: Invested