So far the RACL Europe story seems to be firm in the face of inflation and gas shortages. Consistent with what Management has guided. Need to monitor this for a couple more Qs.

Core competency: Gear cutting, laser welding and cutting which differentiates them from peers. Very good with concurrent R&D. Work with customers in design phase to see how it can be scaled to manufacturing

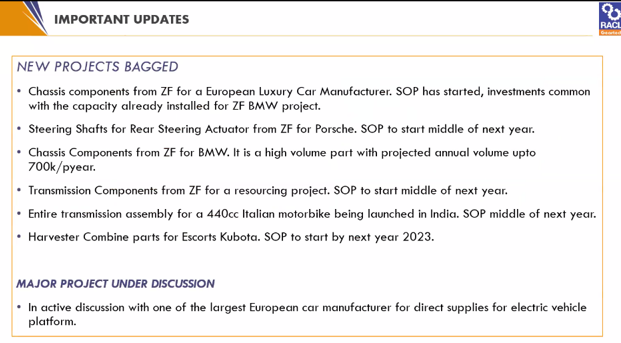

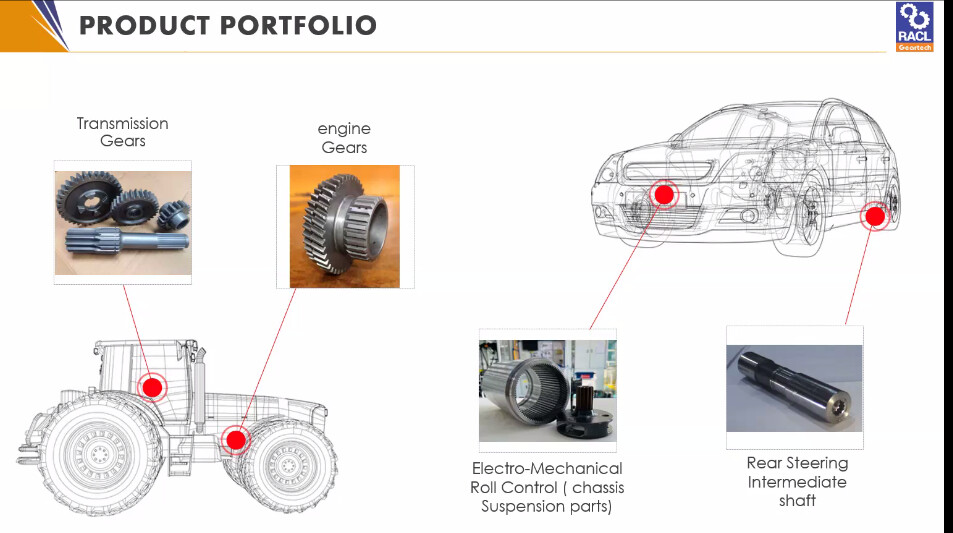

ZF car parts: Electro mechanical roll control, rear steering. Have introduced a new technology

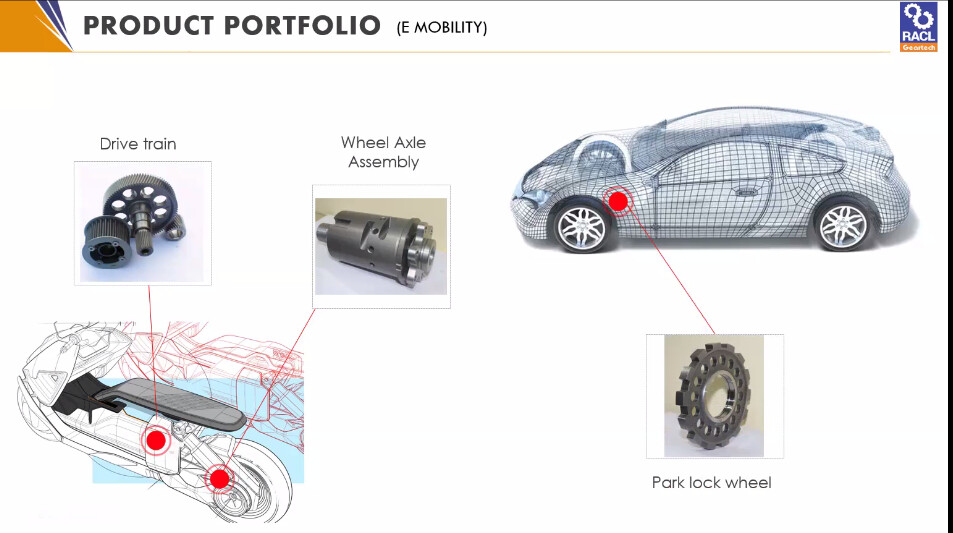

E-mobility (recently started commercial production)

Centrally air controlled plant, clean room with no dust accumulation on machines|

European market grew for RACL (ZF started in June)

Put up capacity with 3 year growth in mind for newer customers which was fully booked by the customers. These capacities are already operating at 70% utilization. Overall, operating at 75% utilization

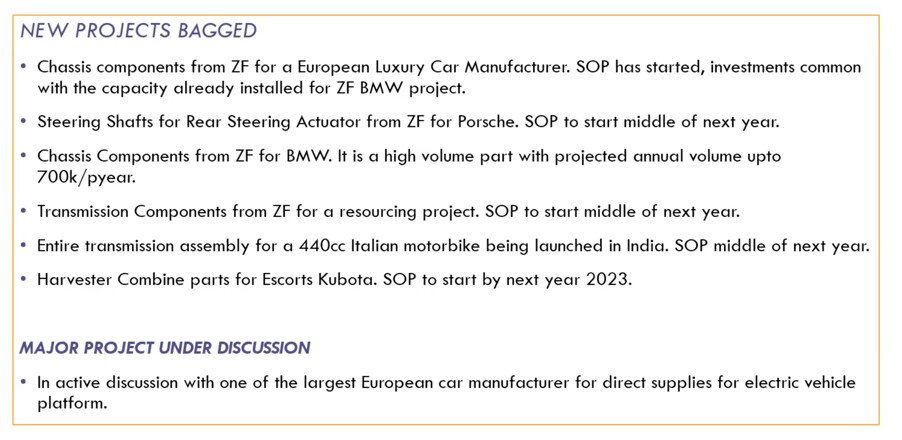

New project with ZF (not modeled before). This was earlier being manufactured by ZF

ZF is confident that steering shafts using actuator for rear steering will be widely adopted beyond Porsche. If that happens, RACL’s parts will flow into them

Bagged one more order from ZF for BMW for one part (high volume: 700K units per year)

Domestic launch of a new 440 cc Italian bike: RACL is the exclusive supplier to them

Have surplus land and are putting up another plant. Building will be finished by March/April 2023

Revenue recognition policy: Recognized once its handed over to logistics partner in Delhi. Work on FOB

One major project under discussion which can be a game changing (luxury car manufacturer through ZF for an electric vehicle, high volume product)

Higher inventory: Large number of SKUs as parts are small in volume but high in realizations

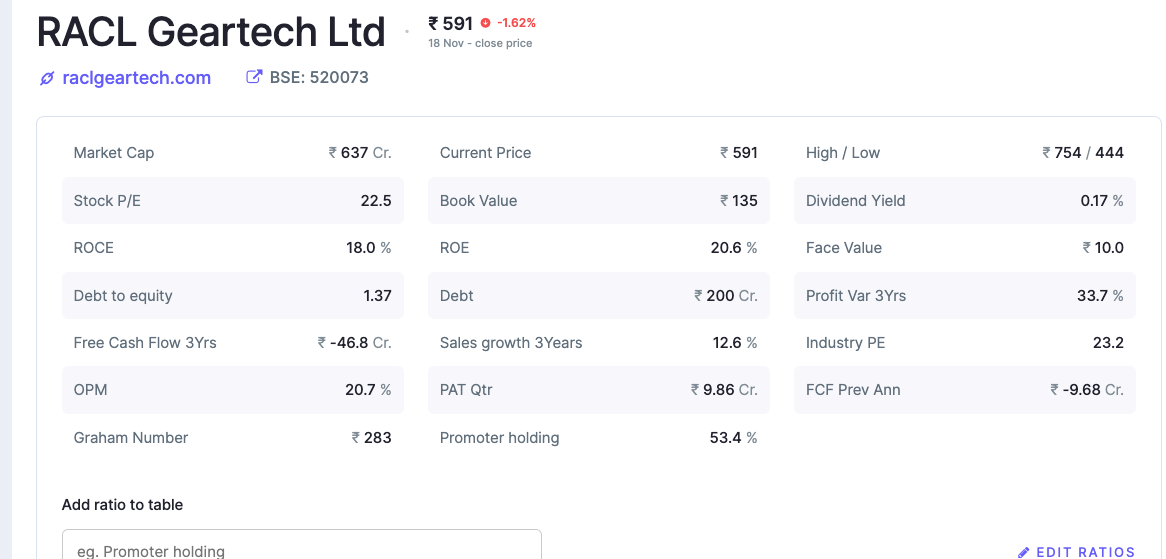

Debt equity is around 1x, still below peak allowable of 1.5x

Optimum utilization is around 2x fixed asset turns

Geographical Segmental shifts: North America: no new projects, Asia Pacific: should increase a bit due to newer projects and same for Europe

Most raw materials (95%) are procured domestically

Don’t have enough bandwidth to scale up industrial customers

Disclosure: Invested (position size here, no transactions in last-30 days)

Wonderful call from RACL Geartech. They shared a lot of new info this time. I wasn’t able to capture everything but got some snapshots which I am sharing below

They have shared a host of new projects/programs that they have bagged in FY23. Lots of new projects via ZF and also a couple with Kubota and an Italian bike manufacturer which is launching in India

Their new partnerships are going very well, especially the one with ZF. ZF had initially contracted with them for 1 program for supplies to 1 OEM. Now, impressed with RACL’s capabilities, they have given RACL another program with a new OEM. As a result their most recently established plant is running at 70% capacity now as against expected 50%

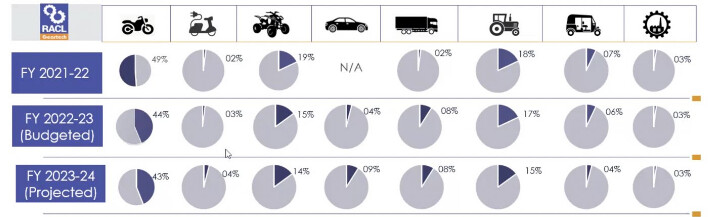

They have got a nice foothold into the pas-car market via ZF, so much so that they are projecting 4W as % of revenue to increase to 9% in FY24 from the existing 1%.

They are setting up another plant to cater to new orders/programs - I think this is related to ZF but I will have to look at the transcript to confirm

Capex is going to be expedited as a result of new orders

Management was questioned a lot about debt reduction but they remained steadfast that debt was at sustainable levels. Their POV on debt:

All-in interest cost is only 4.1% so interest burden is very low (This includes both LT and WC debt, but I am a little stumped by how low the number is. Not all of this is Euro debt, some of this is INR debt)

While they take on more debt, they are also retiring old debt, so as per them net debt won’t rise fast

They incur debt only when a confirmed program/order is in hand, so there is much less risk of debt driven capacities not being utilized

They may have something to announce wrt a partnership with an Indian 2W EV OEM in the next quarter if everything goes well

When questioned on expansion into industrial gears segment, Management said while there is a lot of scope there and RACL already has prestigious customers like GE in the segment, they are unlikely to be expanding in that segment due to bandwidth issues. Their bandwidth is completely choked with auto related orders and programs (Very bullish for Auto, but is there scope to capitalize in parallel on the industrial segment by bringing in a vertical head or a strategy head?)

Overall, Management appeared to be very much in control of the business and quite bullish about its prospects. The business seems to have very promising prospects in the medium to long term.

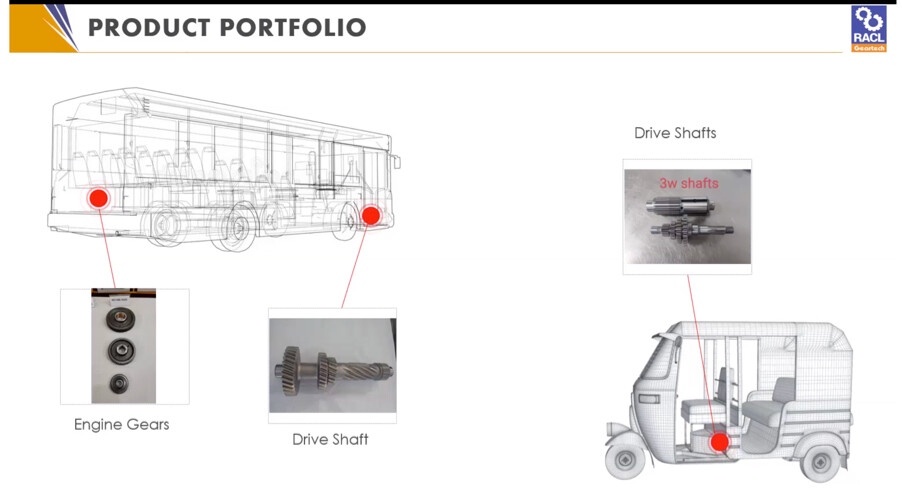

Some more snapshots from the presentation about their products (Couldn’t get all, sorry)

I think this has been an eye opening call even for investors who have been invested for long; on multiple fronts. Rather than give a blow by blow account of the concall, let me summarize some new things I learned about the co in this concall.

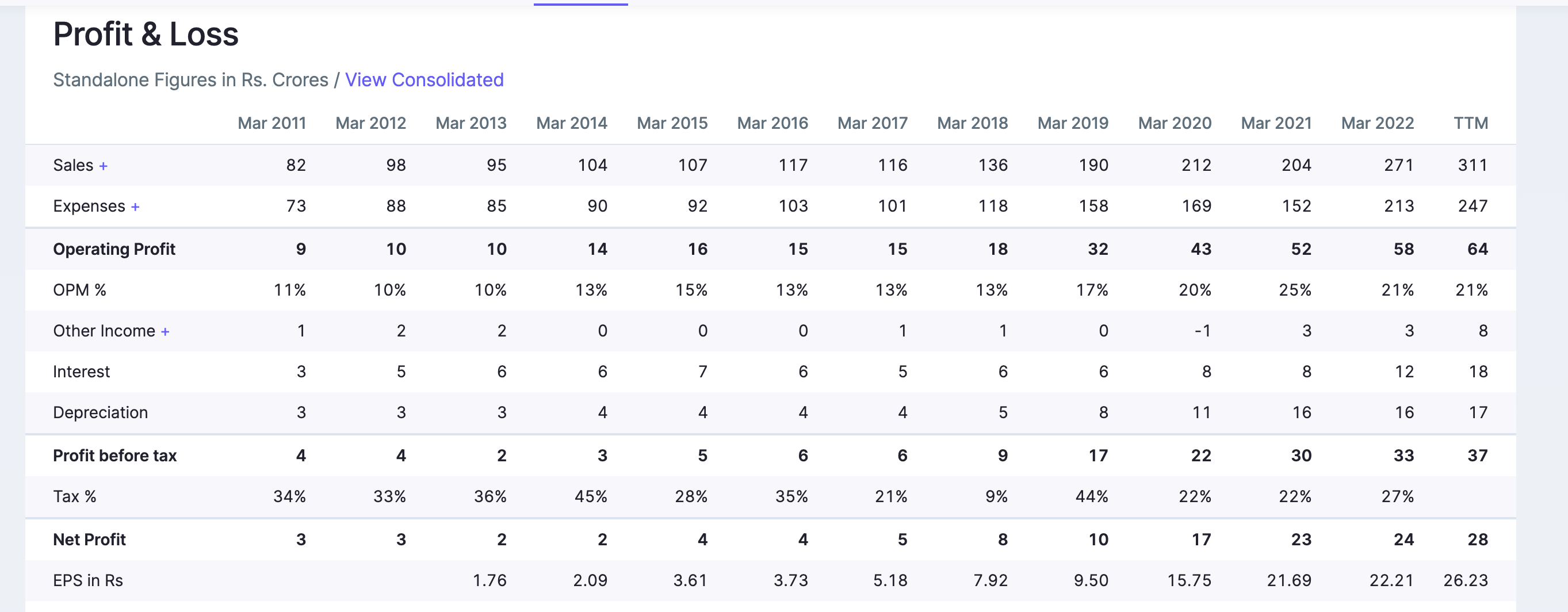

[Margins]: One might wonder why RACL has 20-25% OPM & 70% GPM when most auto ancs have 10-12% OPM & maybe 40-50% GPM. There are a few diff reasons we understood in this concall for this outcome. Firstly, RACL being in a niche space, some customers do production once a month, some only produce once a year. Many European OEMs do 70% production in 4-5 months then do 30% prodution in rest of year. But RACL cannot work that way, can it? Because it needs to run its plants at some constant utilization levels in order for it to make economic sense. Thus, they overproduce during lean periods of european production (my guess is winters) & underproduce during summers (eating up from inventories). But this is the business model of the co. Due to the seasonal & small volume/niche nature, the competition in this space is also far far lower which is precisely what enables RACL to command premium prices & margins for each part. The inventory & margins need to seen in conjunction. CMD says that the they are more than compensated in this biz model. Is it better to be in mass market low margin lean inventory supply chain or high margin high inventory niche supply chain? I think the cross-cycle ROCEs speak for themselves.

[Growth]: Recession, demand destruction, Europe energy crisis. What is going on? I think of key learnings for me personally over last 2 years has been the intangible value associated with a co belonging to 1 supply chain versus another. Let me explain. Imagine 1 co makes gears that go into mass market cheapest cars. In such entry segments, demand destruction is very much imminent every few years leading to cyclicality. This can be seen in india with the entry 2w markets, the global auto markets. GM, Ford. The end user’s ability to pay is tightly linked to labor market conditions, inflation, wage hikes, interest rates. Because it’s a P&L purchase. Most discretionary purchases for lower & middle class are P&L purchases (Funded by P&L of the end user). Now contrast this with a gear maker who is a part of a luxury or high end auto supply chain. Porche, BMW, KTM & the likes. Person buying porche typically does not take an auto loan with 5 year EMI to buy it. These are typically bought by people who do balance sheet purchases. This strength of the value chain & purchasing power of end consumer is under appreciated here imo. This actually shows up in larger orders, more orders, ZF bringing in bmw, porche , a large high volume ev OEM (my guess is Volkswagen based on the indicated figures). The capacity created in 2021 is already running at 70% utilization in November. If racl manages to grow well next 2 years while global auto industry suffers it wil further strengthen investors confidence in their end consumers buying power. It was also very interesting to hear about higher asset turnover on account of better utilisation for profit side assets (like a cleaning machine etc which don’t add topline but add profitability). China+1 Europe+1. Zf, GE running after racl : you make the gears. We make it more expensive. You’ll make it cheaper. Very interesting. Could Europe energy crisis end up being a blessing in disguise for racl ? Is this what it means for a co to be anti -fragile ? The European energy crisis might lead to European manufacturers shifting more production to india & racl, leading to anti fragility at least with respect to 1 specific risk.

Investors way of thinking vs owners way of thinking: as investors we always have some picture of an ideal company and we want every company to conform to that ideal. One such thing is on debt to equity ratio. Debt to ebitda ratio and so forth. Of course if racl continues to grow at 25% or more they will have to take on debt since their roe cannot support that level of growth intrinsically. I think investors should be open to evaluate each company on its own merits. And be able to take a co specific call. In this case given the above two points , given that RACL only does a capex once they have revenue visibility. I think one should be very excited about the capex. The world is full of ever evolving subjective factors. Risks like zf or ktm facing 30% annual degrowth. Such risks need to be adjusted in our position sizing depending on our subjective assessment of these risks. @msandip has been doing some of this but some of us need to chip in & do a better job tracking racl clients & their growth prospects. Racl is definitely grabbing wallet share. But we also need end market growth in order to have sustainable growth beyond immediate 5-7 years.

On whole i think this concall has been eye opening. I am tempted to increase allocation despite this already being a 10% position (I’m not a big fan of excessive concentration because often we over estimate our ability to understand & predict companies futures)

Disclaimer: invested, biased. Do your own due diligence

I had invested in RACL in April of 2020 at an average price of 60. It ended up becoming my first ten bagger in a year. I sold out when the price crossed 700 and I realized that the promoters would have no choice but to pile on debt to grow further. However as I’ve tracked the company from the sidelines it has become markedly less attractive from an accounting perspective than it was in 2019.

Few red flags:

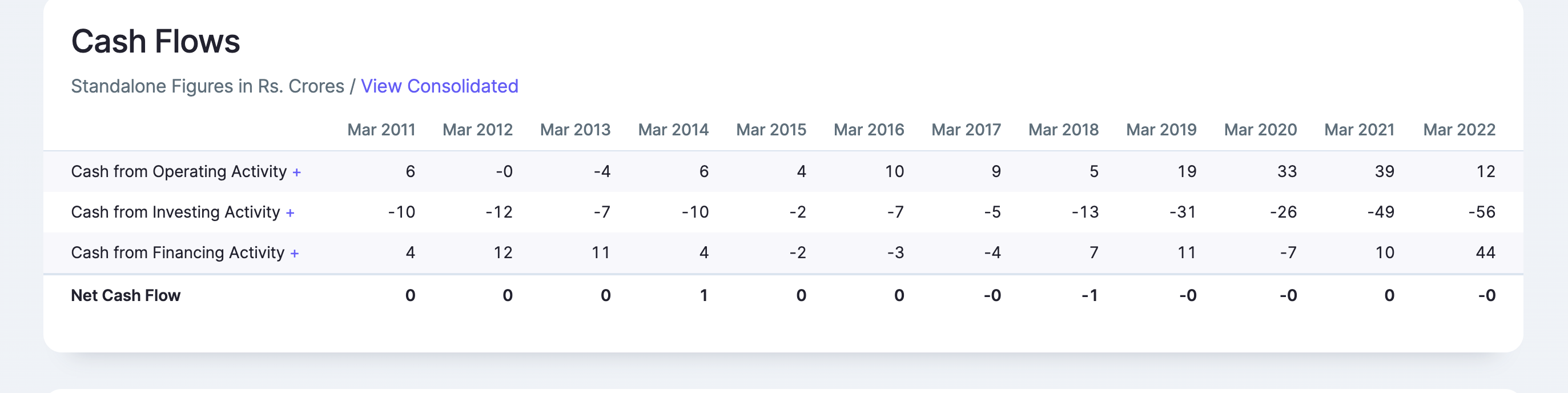

Cash generation was never an issue for RACL until FY21. Profits were consistently being converted to cash.

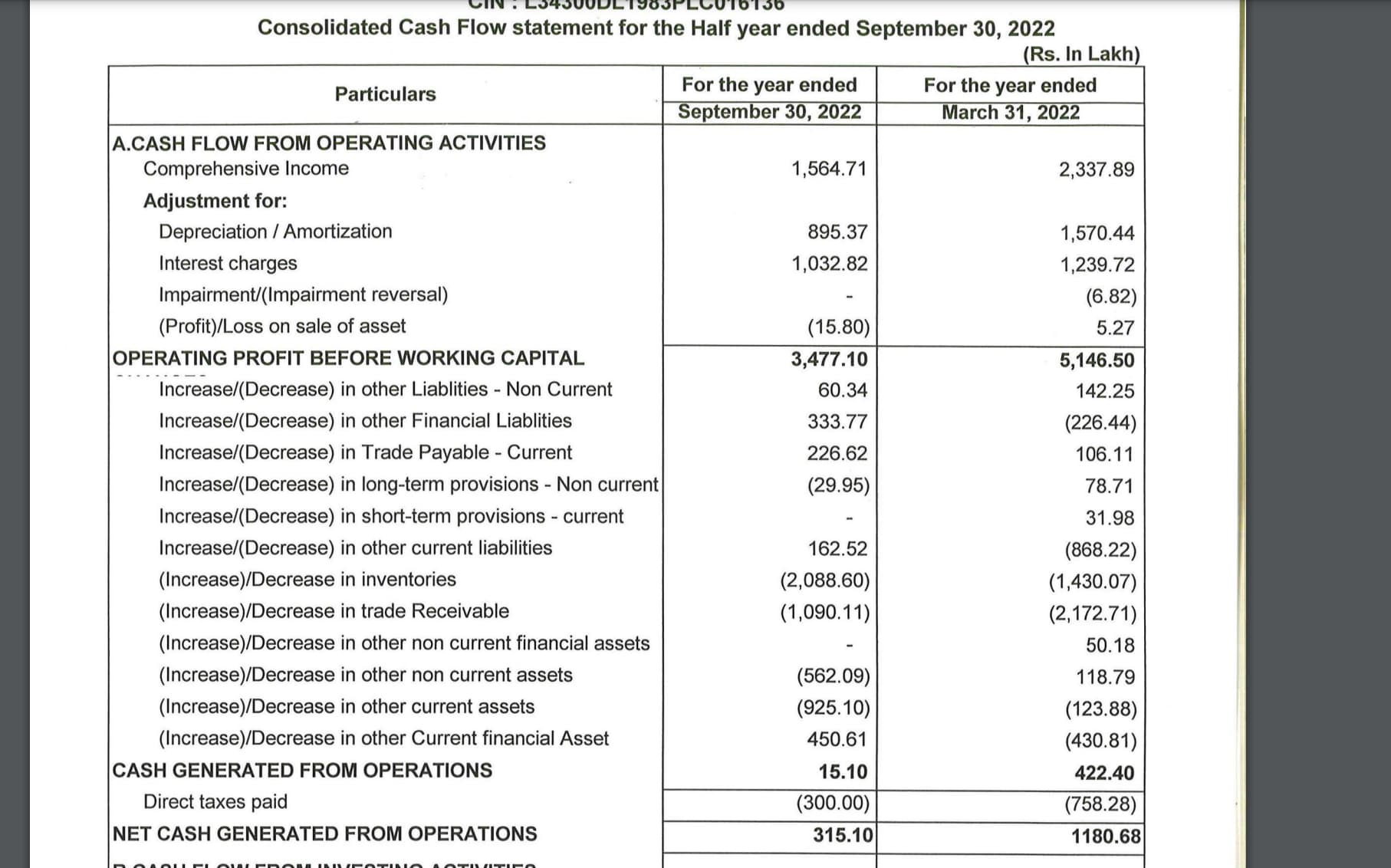

That dropped off a cliff in FY22 and has been even worse in H1FY23. Its so bad now that they are unable to fund even interest payments from operating cash flows - they have need to draw down additional borrowing for that.

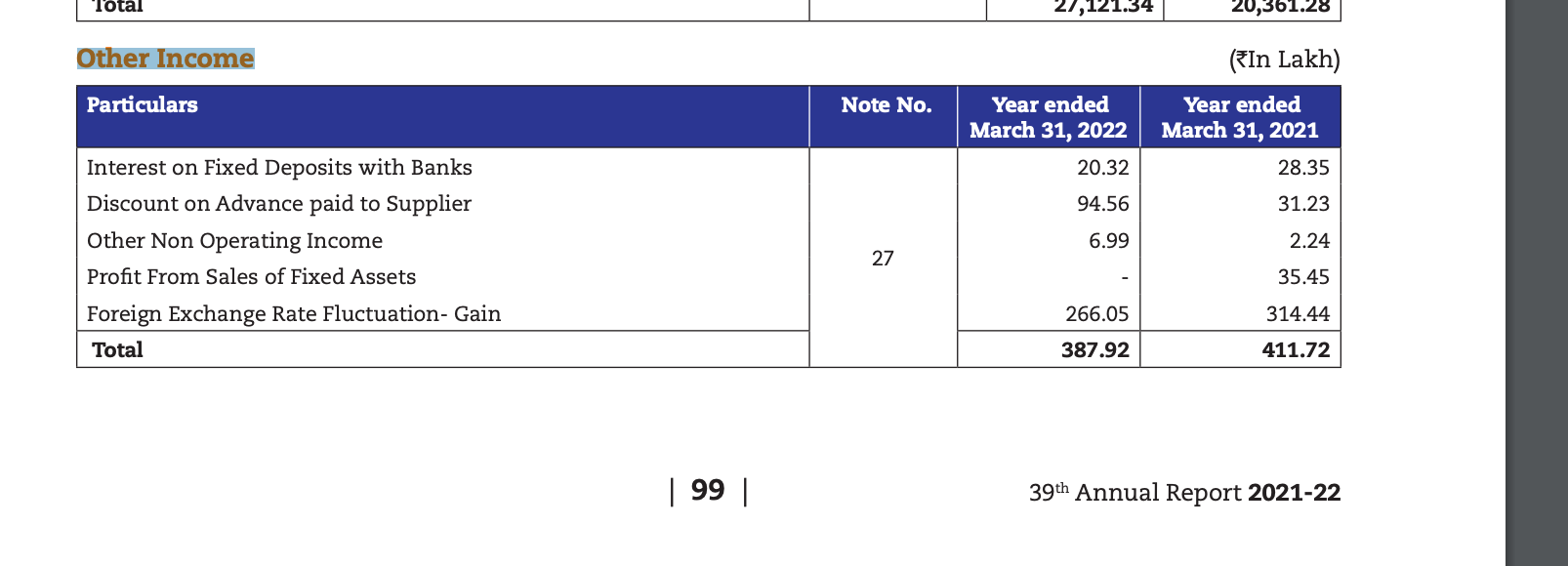

Other income shot up from nothing in FY20 to INR 8cr in the trailing 12 months which is > 20% of PBT. This income is largely gains on holding foreign exchange.

RACL seems to have become an astute forex trader. Made increasing gains in last 3 years consistently while EURINR has fluctuated wildly.

Depreciation policy is odd. Depreciation wildly fluctuates on a quarterly basis with depreciation in the March quarter being nearly 2x of other quarters.

Naturally with such cash flow deterioration and aggressive capex, debt has exploded to INR 200 cr. This debt is not cheap (last q interest cost was 5 cr which would imply annualized interest cost of 10%) and is likely to rise when long term borrowings need to be rolled over.

The only two parameters that RACL has improved on in the last 18 months are accounting profits and investor communication.

Debt has always been a concern for RACL Geartech considering their high receivable and inventory days. But I think Mr. Singh has explained why the business fundamentals require such high inventory and receivable days amply in the calls. Also if you take a look at debtor days and inventory days below, there is no material change from 2018 to 2022. For TTM, inventory days are 175 and receivable days are 103. Inventories are actually much lower at the moment than the historical trend.

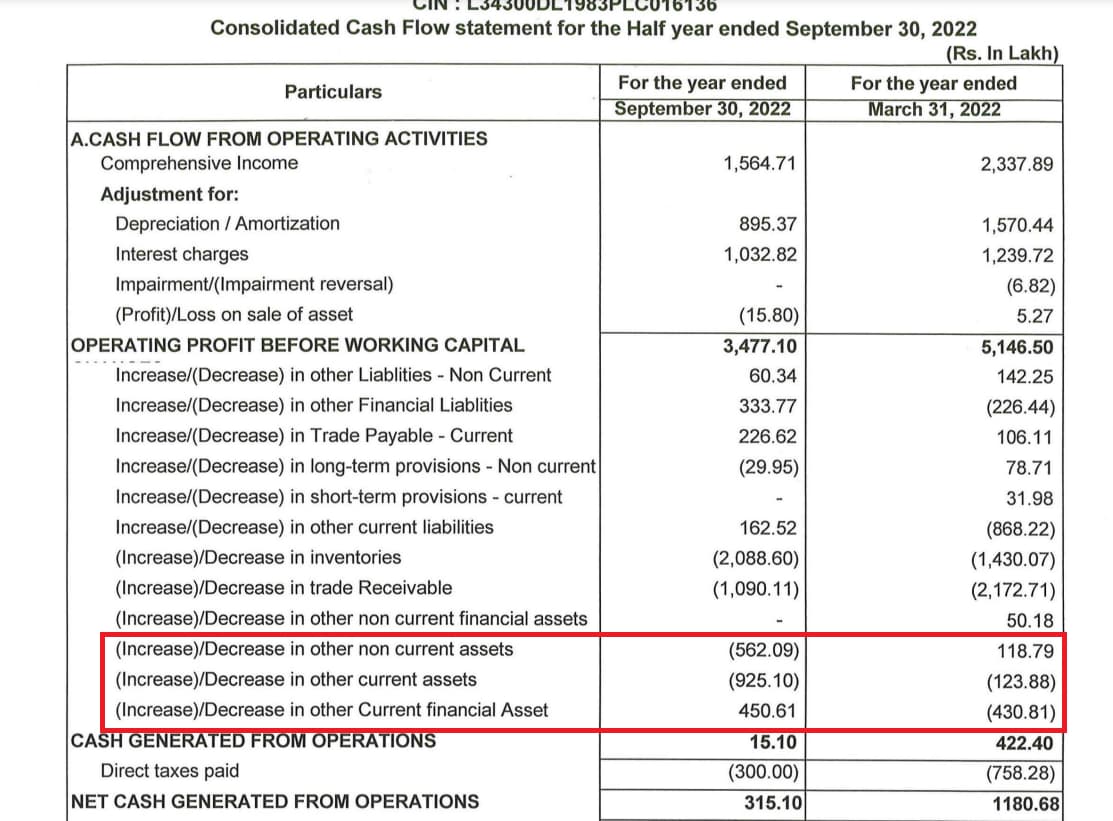

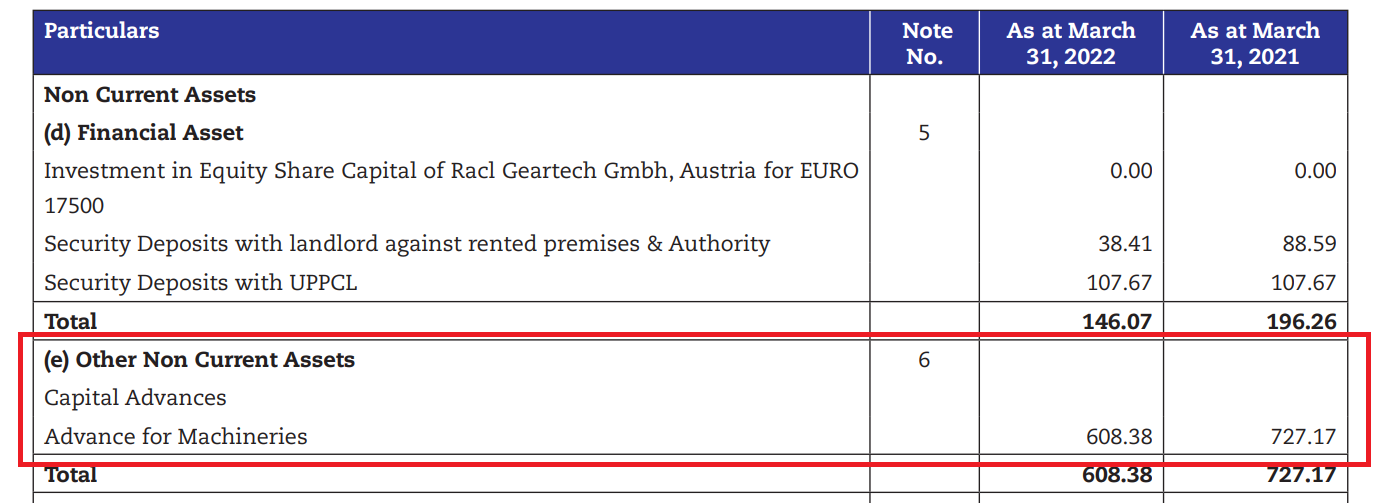

If you check what these items are from ARFY22, you will realize these pertain to advances for machineries, prepaid expenses and advances to suppliers. So these mostly relate to advance cash outflows meant for putting up the new capacities required. Therefore, I wouldn’t be too concerned about quality of cash flows at this point. I expect cash flows to revert to the mean when the new capacities stabilize.

On the whole though, the high debt burden is probably the only thing that rankles a little for investors. I am hoping they will be able to retire more debt once their domestic business share picks up. The domestic business would have a much shorter cash conversion cycle and would boost their OCF.

I also did not understand Mr. Singh’s comment on the call regarding 4% net/net interest rates as I mentioned in my notes above. Interest rates are clearly @ around 10% as evidenced by ~20Cr interest costs on ~200Cr loans. If anybody understood what he meant by that, please let us know.

Hi,

As per my understanding of the business and the products. RACL has a 2% presence in the EV space and expect to go to 4%. More details in the post by Nirvana. Now if you ask what are the transmission components in an EV.

2W - A EV 2W will have a motor with a 1:1 gear ratio. Now these are similar components to your say first gear of an ICE 2W. I do not see any new shift in transmission technology in the gearing space in the near future.

4W/LTV: here you have a couple more things such as a electronic parking lock and the general transmission gears ( which is also a 1:1 gearing ratio). However some companies like Lexus are playing around with it. But frankly I am yet to notice any big improvement.