Another good quarter

3 Likes

Superb performance by the company! Amazing execution and consistent scale up. Good to see further expansions being planned.

Ayush

Disc: Invested in family and client acs

31 Likes

I have recently come across RACL.

Can someone please elaborate on who their competitors are in Taiwan, China & Vietnam?

For everyone’s benefit:

There is a typo in mentioned email id.

correct address is: investor@raclgeartech.com

‘r’ is missing in gear in company letter.

4 Likes

RACL Q3 Concall notes. Another good call.

-

Current factory details (Gajraula : 95% revenues from here) – Total 4 sub-plants

a. Chetak – Domestic, 3W, trucks etc – precision and cleanliness req lower (Oldest plant)

b. Tejas – Export 2W plant

c. FG storage

d. Forging plant – 50% forging is done in-house, rest through suppliers (2014)

e. Ojas – 2021 Plant

f. Shakti - New plant (Nov 2022)

g. Vacant plot about 1/3rd existing built up area size for future expansions -

Timeline of the company

a. 2004 – First exports order from Kubota Tractors Japan (1st Indian co exporting gears to Japan)

b. 2005 – Tier 2 supplier to BRP Rotax (First indirect European order)

c. 2008 – Single source for Vespa from Day 1 in India; USD 1 Cr revenue

d. 2009 – First direct transmission assembly order from BMW Husqvarna

e. 2010 – Orders from KTM and BMW started

f. 2011-13 – Invested USD 5mn for inhouse forging plants, advanced robotics, power honing technology (precision machining)

g. 2014 – KTM order for complete subassembly of 690cc gearbox

h. 2015 – Name change to RACL Geartech (New target market : luxury segment)

i. 2016 – Stops all aftermarkets business; fully OEM

j. 2017 – Exports becomes > 50% of top-line, overall sales was USD 20mn

k. 2019 – Full owned subsidiary in Germany

l. 2021 – Company enters PV segment thanks to ZF, invested EUR 4 mn for Ojas plant -

Product portfolio

a. Steering and axle shafts – supplies to ZF – helps in having a better turning radius for 4W

b. Axle shaft – Truck part, goes to Europe

c. Balancer shafts – ATVs and multi cylinder engine motorcycles (KTM Duke)

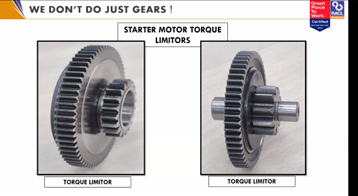

d. Starter motor torque limiters

e. Park lock wheels – for locking the wheels in park mode (Supplied to an EV customer in Europe)

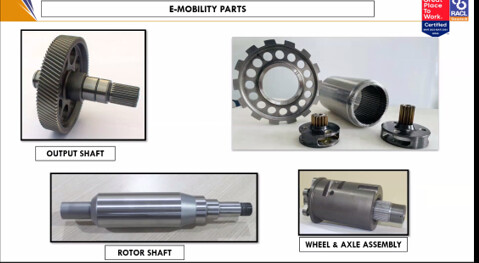

f. E-mobility shafts

g. Foot rests -

Numbers and future

a. 470Cr guidance for FY24 (confirmed orders) and 365Cr for FY23

b. Shakti Plant will be operational mostly for post FY24 revenues

c. ZF sourcing 300mn USD from India right now and their target is to source 3bn USD from India by 2030 (RACL has a very strong relationship with ZF)

d. The journey from 500-1000Cr will be partly driven by the current projects which are still in infancy stage. They are also exploring opportunities in aerospace and defence industries for planning the next leg of growth.

Some photos of the product portfolio and RFQ to production process:

24 Likes

Q3 concall notes:

- Picture of gajrola factory spread across 26 acre of plant (95% of revenue from here).

- Residential complex for key employees: 80 families.

- 100 cr of sales. 72% Exports. 28% domestic.

- New capacity additions running at 70% capacity utilization

- First co to export gears to Japanese OEM

- Started gear honing technology which improved our margins & value addition.

- Got 1st order from KTM for assembled gear shaft (shaft, gears, bearing) put straightway into engine housing. Top of line, duke 690. Got contract in 2014.

- 1st electric car: Mahindra Reva : E20 had RACL gears. When mahindra overtook they started producing their own gears.

- Product portfolio: Complex critical safety components & assemblies

- Gear has application in chassis, engine,

- Foot rest (for an indian 2w), steering tube (central pivot on which bike head is mounted), rad flanch (break mounting part), steering shafts (ZF, Revolutionary product.), axle shafts (truck part going to europe). These components will go to EVs also. Balancer shafts, Balancer shaft assembly (going to engine, duke 990 motorcycle for KTM; very complex requirement; Weight balancing, angle of weights)

- Parking lock wear (for EV car),

- E-mobility parts: output shaft, rotor shaft, wheel & axle assembly :

- Operator packages the part where it is manufactured.

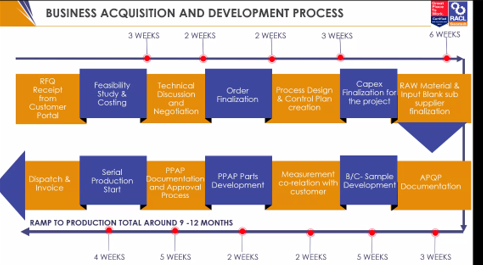

- Competitive advantages: Business RFQ: RFQ to actual sample submission, product generation, high lead time for equipment deployment,

- 800 different part numbers

- Guidance for FY24: 470 cr. 43% from 2w. Cars : 9% of revenue in FY24. EV: 4% (based on confirmed orders).

- Guidance of 365 cr for Fy23 (105 cr for Q4)

- Building a new plant : Shakti plant. 470 cr majorly from ojas plant. Low contribution from Shakti plant. Primarily being built for beyond FY24. Put solar power plant on our ojas plants. 5% of electricity from rooftop solar. In next 5 years, ~50% of electricity will be from non-fossil fiel based sources.

- We have barren land on the left side. We produce wheat also.

- Customer who strategizes their business plan. We take that forward. ZF has very ambitious plan to source components from india. ZF sources 300M$ right now from india. 2030: 3B$ source from india. (10x in 7-8 years). We were 1st co in india who gave fully finished parts for passenger vehicles for europe for ZF. New flood of RFQ with us. Just in 3 years ago we started & the business is growing well. All our customers have ambitious plans.

- For capex we are spending 25% from reserves.

- Seasonality: Different products have different seasonalities (on road & offroad vehicles). It balances out.

- Working on beyond 500cr milestone: Existing business projects are in infancy stage. Volumes will ramp up by Fy26/27. That will grow revenue beyond FY26/27.

- Niche & luxury british motorcycle manufacturer was sitting in our factory some time ago.

- Roadmap very soon on 500 to 1000 cr roadmap.

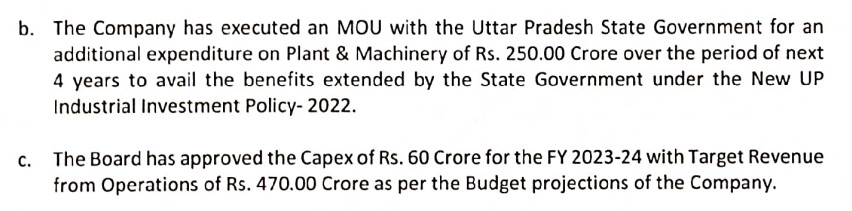

- 250 cr capex over 4 years, then over Next 12 years , 20% of the capex (50 cr) will be given as subsidy (4cr / year).

- Many times need to invest up front to produce 1st part.

- Dont see margins Q to Q.

- Debt is comfortable. Customers compensate even if some orders fall through. For next 2 years at least no change in strategy of capital structure.

Disc: Invested, biased.

32 Likes

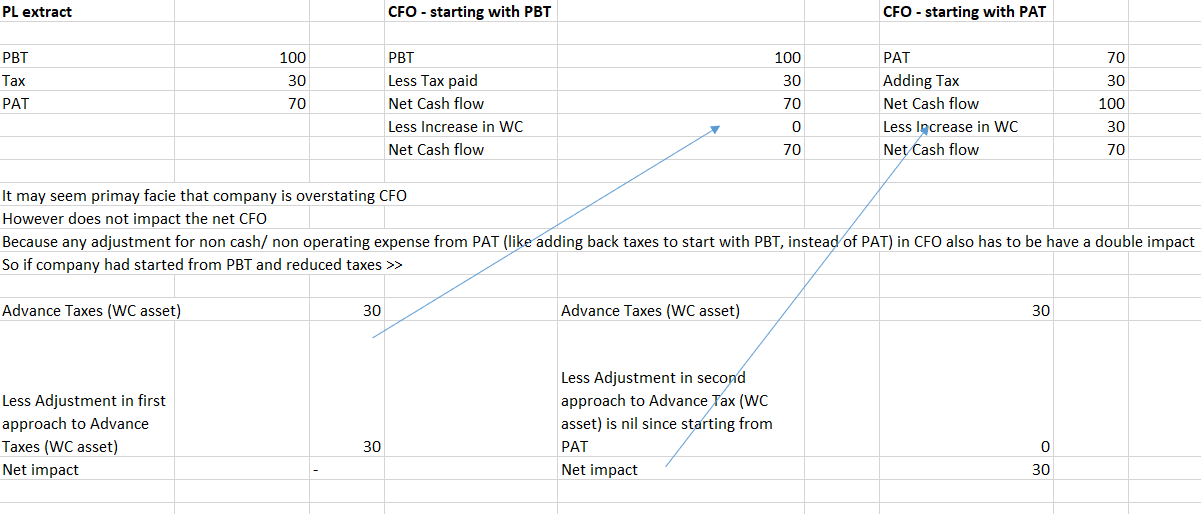

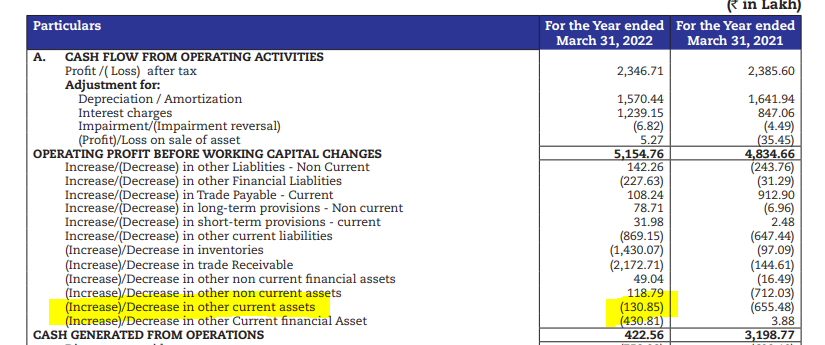

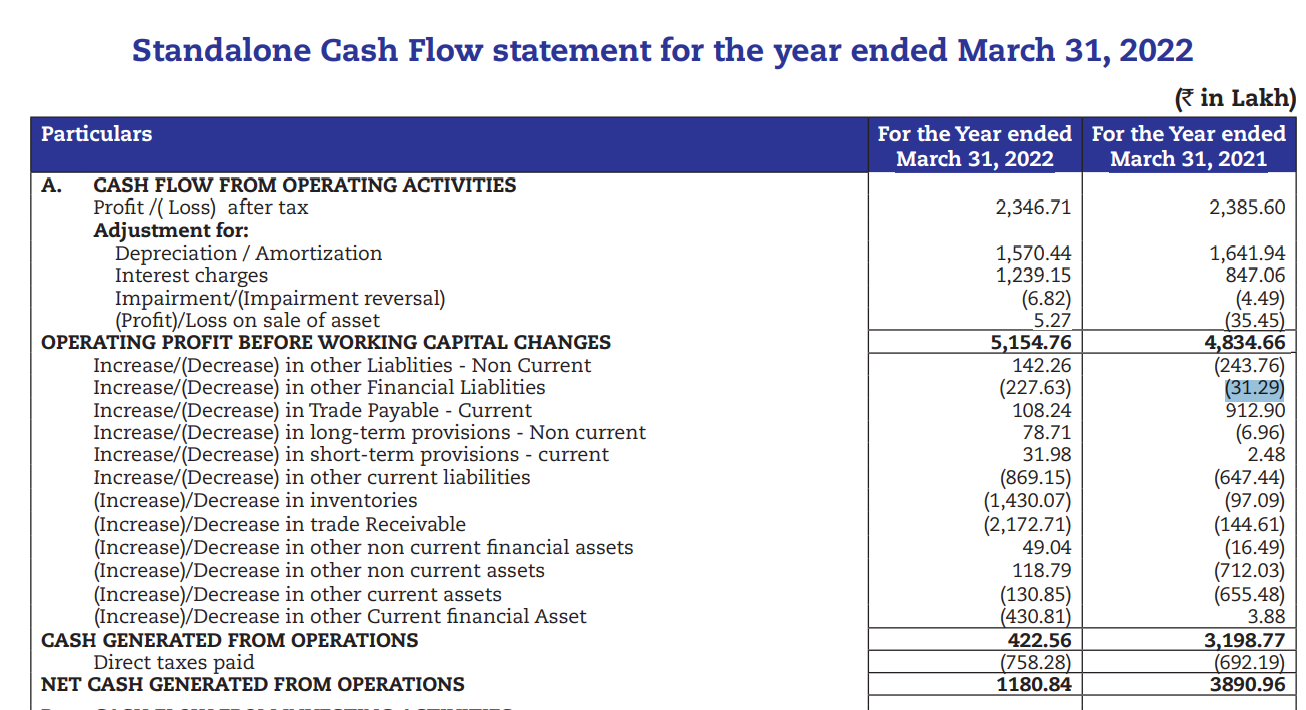

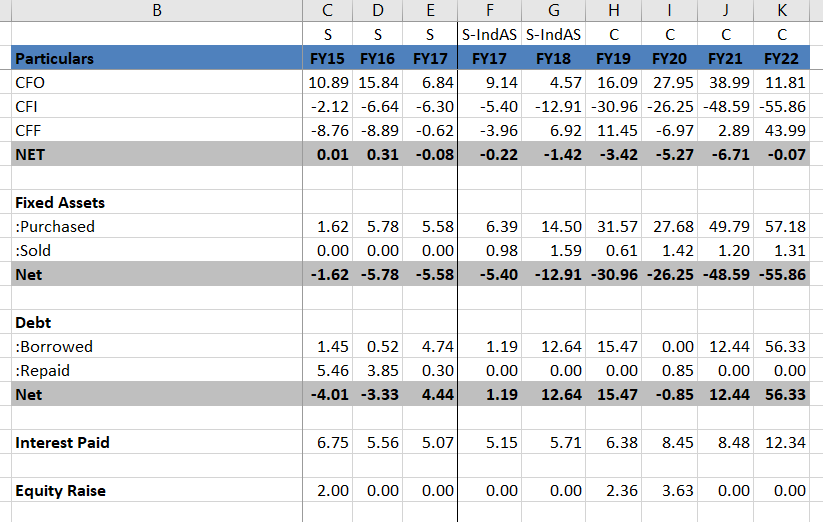

Amidst all the great things happening in the business, this old question of unconventional OCF calculation has been bugging me and a few others like @komal.

Management was asked on the concall yesterday about their existing practice of starting with PAT and adding taxes to arrive at OCF. Apparently many people have been reaching out to them with this query and they said on the call that they will relook at this practice and change over to the conventional method that starts with PBT and subtracts taxes.

I do think the OCF since 2019 was being overstated by the amount of taxes paid (Stated OCFs were about 20% higher than they should have been). This change in treatment roughly coincides with the appointment of Gianender & Associates as their statutory auditors, so the change in methodology could have been the auditor’s suggestion. The auditor’s term gets over in FY23.

Anybody with more detailed knowledge of IND-AS 7 who thinks RACL’s current practice may be acceptable? My cursory reading of IND-AS 7 did not suggest so, plus I have never seen another company calculate OCFs like this.

6 Likes

This is more a presentation thing in my view - should not impact net CFO - either overstating or understating. I have tried to explain below - otherwise the Cash Flow wont tally at all

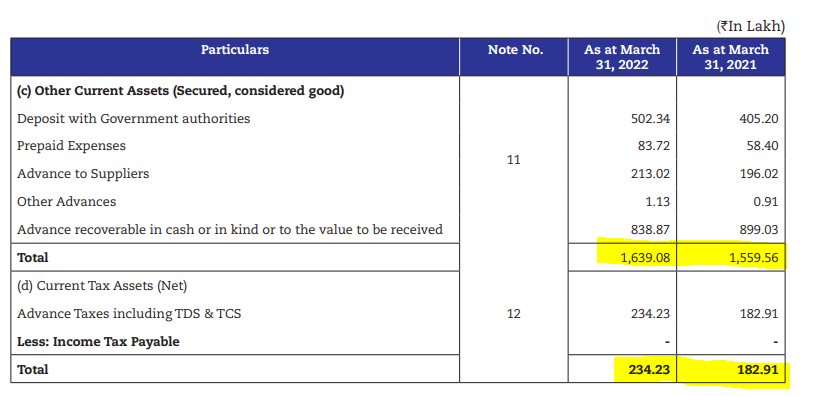

Its represented clubbed in other current taxes. At standalone level = (1639.08-1559.56+232.23-182.91) ~ 130

Disclosure : Not invested, + I may be wrong - although a chartered accountant, I am not a IND AS or tax expert

5 Likes

The company is actually adjusting for tax provision under the current financial liabilities within the working capital changes head of the cashflow statement and thus is adding the amount back.

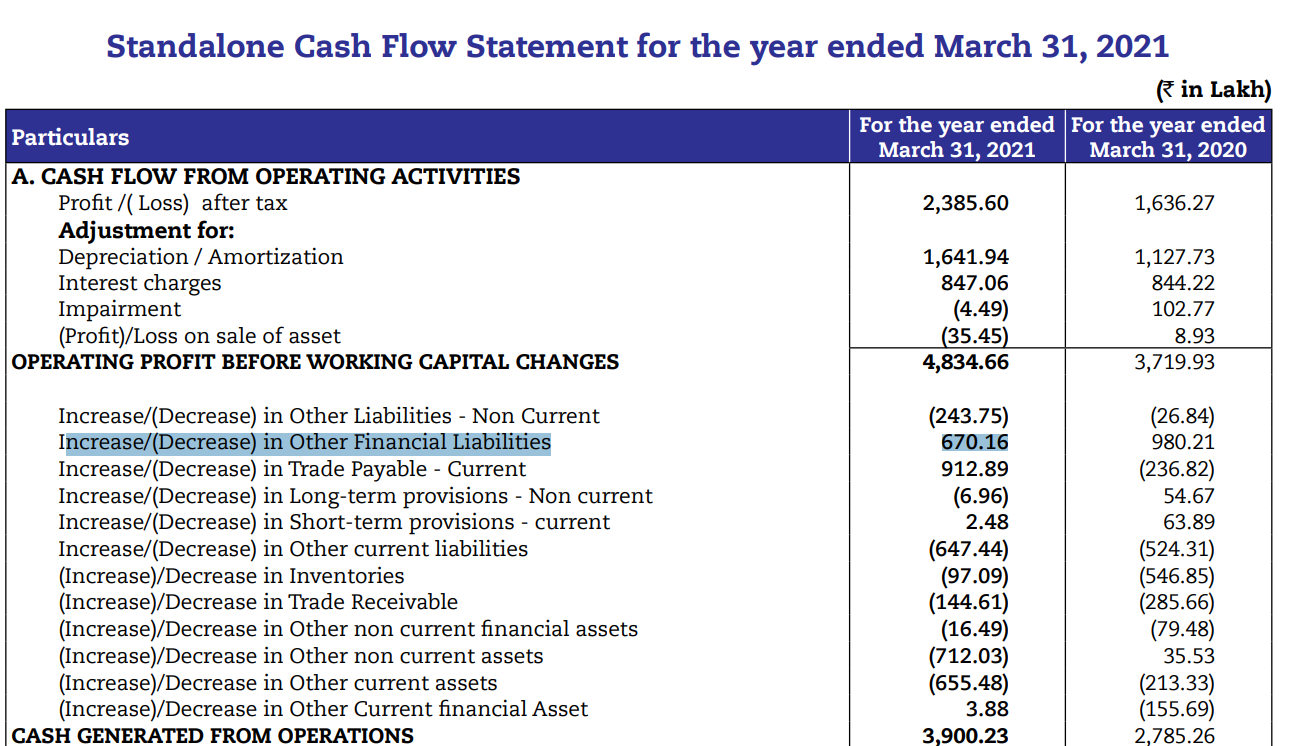

See FY21 cashflow statement in FY22 Annual Report and then in FY21 Annual Report.

So FY22 and FY21 cashflows as per FY22 annual report is correct. Before that for all periods, not very sure, but it seems like cashflows were inflated by tax amount.

Correct cashflows as per my understanding & working-

2 Likes

Link for investor ppt and concall recording

Which other companies might benefit from this ? Any other existing suppliers of ZF in listed space ?

5 Likes

As discussed in the Q3 concall, I asked RACL to clarify the OCF accounting issue via email. I received a reply from the company yesterday. Reproducing the text of my email below. Based on this reply and the couple of posts above, I am considering the matter closed for now.

Hello Prabh,

Good morning. This is Nirvana reaching out as discussed to get a clarification on the method used for OCF calculation for RACL Geartech. Please find my original email below which highlights the difference in treatment of taxes in FY18 and FY19 and in general the unconventional practice of calculating OCF by starting with PAT and then adding taxes.

I request you to provide the following clarifications so that the matter stands resolved and understood

- Till FY17 RACL used to calculate OCF via the conventional method - starting with PBT and subtracting taxes paid. Why was this practice changed starting in FY18?

It was our auditor’s opinion as per their understanding to changes to the IND AS7

- In my opinion, the present method used to calculate OCF for the company may be overstating the OCF by the amount of taxes paid because the calculation starts from PAT and then again adds back taxes, which in my opinion amounts to pre tax cash flows, not post tax cash flows. Please clarify this and correct my understanding if wrong.

I don’t think anything is being overstated. Its a way of presentation. If you start with PBT then you subtracting taxes, if you are starting with PAT you are adding taxes, end impact is same.

- In the call Mr. Singh mentioned it would be a good idea to go back to the conventional method of calculating OCF starting from PBT. Can we expect the FY23 annual report to present OCF using the conventional method?

Yes, we are going to start cash flow from PBT from FY23 onwards

20 Likes

Transcript for Mar 23 is available now

Concall Transcript

For instance, PBT = 100, Tax = 30, PAT = 70. Then, if we start with PBT and subtract tax then CFO = 100 - 30 = 70. But if we start with PAT and add tax then CFO = 70 + 30 = 100. Not the same.

What am I missing? Thanks.