Wonderful call from RACL Geartech. They shared a lot of new info this time. I wasn’t able to capture everything but got some snapshots which I am sharing below

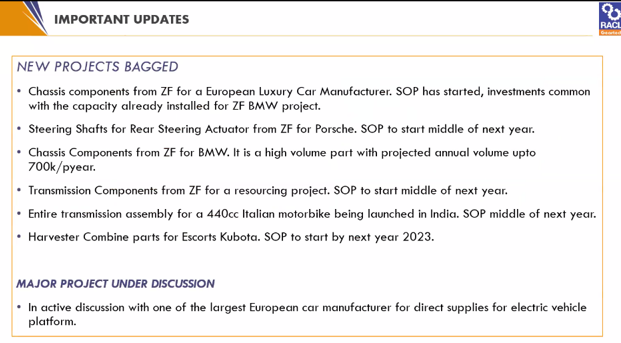

- They have shared a host of new projects/programs that they have bagged in FY23. Lots of new projects via ZF and also a couple with Kubota and an Italian bike manufacturer which is launching in India

- Their new partnerships are going very well, especially the one with ZF. ZF had initially contracted with them for 1 program for supplies to 1 OEM. Now, impressed with RACL’s capabilities, they have given RACL another program with a new OEM. As a result their most recently established plant is running at 70% capacity now as against expected 50%

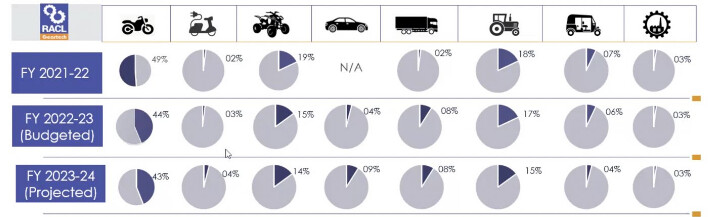

They have got a nice foothold into the pas-car market via ZF, so much so that they are projecting 4W as % of revenue to increase to 9% in FY24 from the existing 1%.

-

They are setting up another plant to cater to new orders/programs - I think this is related to ZF but I will have to look at the transcript to confirm

-

Capex is going to be expedited as a result of new orders

-

Management was questioned a lot about debt reduction but they remained steadfast that debt was at sustainable levels. Their POV on debt:

-

All-in interest cost is only 4.1% so interest burden is very low (This includes both LT and WC debt, but I am a little stumped by how low the number is. Not all of this is Euro debt, some of this is INR debt)

-

While they take on more debt, they are also retiring old debt, so as per them net debt won’t rise fast

-

They incur debt only when a confirmed program/order is in hand, so there is much less risk of debt driven capacities not being utilized

-

They may have something to announce wrt a partnership with an Indian 2W EV OEM in the next quarter if everything goes well

-

When questioned on expansion into industrial gears segment, Management said while there is a lot of scope there and RACL already has prestigious customers like GE in the segment, they are unlikely to be expanding in that segment due to bandwidth issues. Their bandwidth is completely choked with auto related orders and programs (Very bullish for Auto, but is there scope to capitalize in parallel on the industrial segment by bringing in a vertical head or a strategy head?)

Overall, Management appeared to be very much in control of the business and quite bullish about its prospects. The business seems to have very promising prospects in the medium to long term.

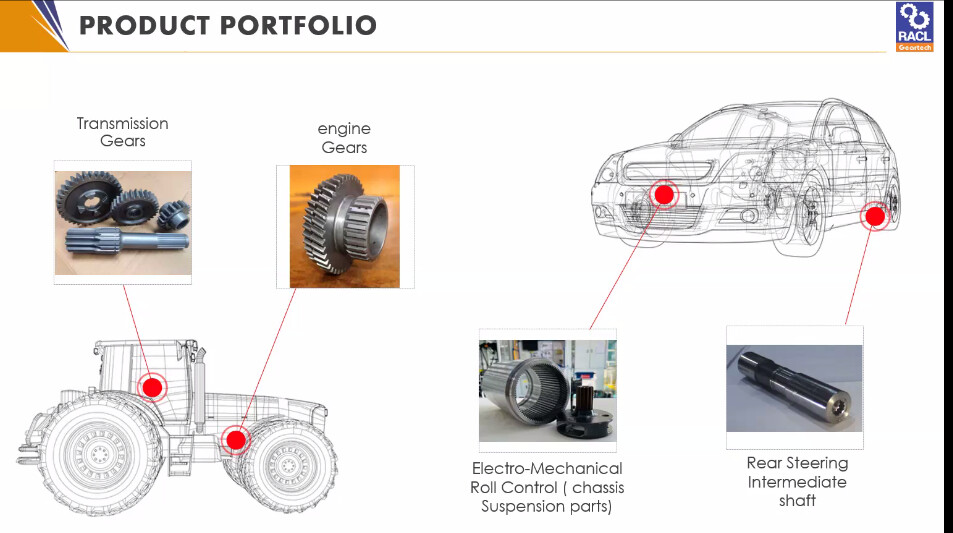

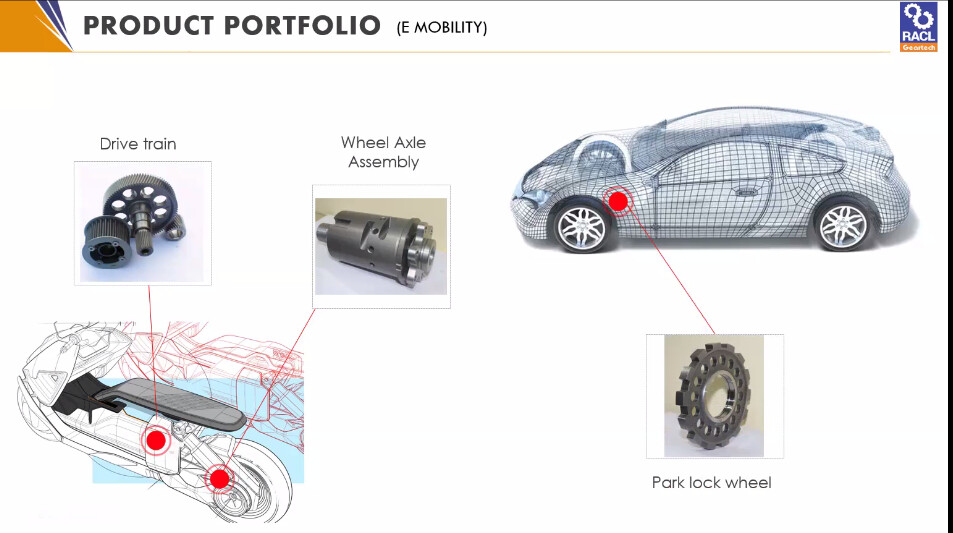

Some more snapshots from the presentation about their products (Couldn’t get all, sorry)

Disc: Invested.