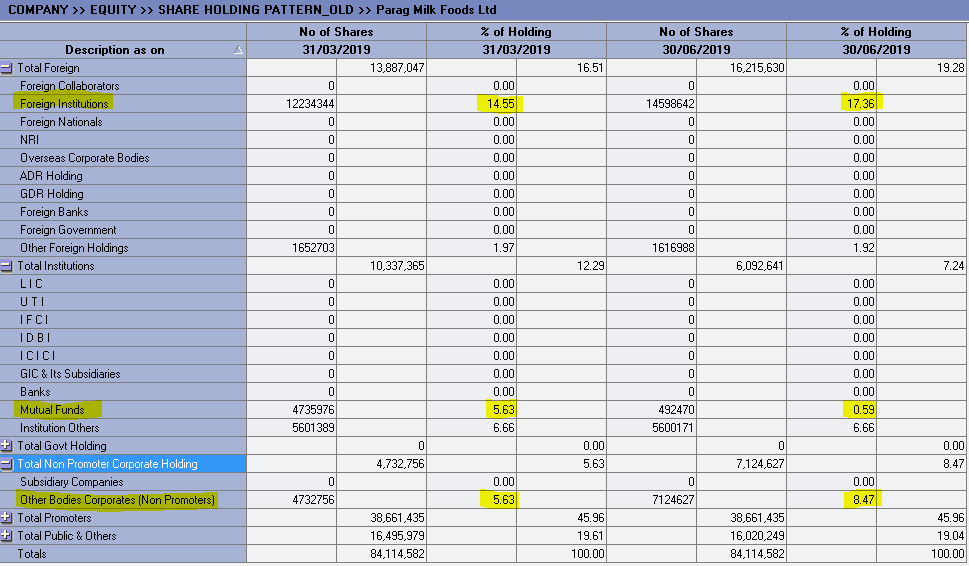

FIIs buying and DIIs selling… and still it is falling… strange… also, other bodies corporate is includes the stitching depository APG Emerging markets equity pool… does anyone any idea about this fund? I don’t understand why FII’s are buying this stock where they are overall net seller and stock is still cracking…

Parag milk share price fallen to Rs.142… Couldn’t understand what happened to the stock so that it has fallen from 320+ to 142… in 2018 it has traded above 350 levels… and now… to 142… why? Just because they are going to miss their EBITDA margin target by 1 or 2% this year? or management churn? Anyways they have brought in a quality management on board from brands like brittania and Amul… so… unable to understand the reason behind this fall?

I feel the fall in the price will only justified if their books are cooked and reality is something else…

Was this the model they adapted with vector consulting? If yes why is not mentioned in the presentation, as it talks about phase I completed in Mumbai ?

Has anyone emailed the company and asked about the guarantee from company to promoters or is it vice versa and why is it increasing and any idea on pledge as well, they have again pledged a good quantity? @harshitgoel@Mridul

Initial results for Mumbai via Vector Consultants show 1) ordering of unique SKU has increased 60%, 2) total lines of sales have doubled, 3) repeat orders have gone up 130%, 4) active outlets have doubled, and 5) moving production, supply chain and inventory at the depot level on a replenishment basis has increased fill rates to 96% from 80%. In our view, cost of adding telecallers and schemes given to retailers will be ~0.4% of sales (which is not total cost of TOC) while increased sales due to range-building and higher throughput per store has added ~4-10% incrementally. The project will breakeven in 4-5 months in Mumbai (total time: 18 months)

I think that is due to collateral as price drop sharply in one month. (Dis : invested avg price : 232). Not planning exit at this level will wait for 2 more quarters how things will work out.

The growth is limited for a company as the item is perceivable in nature . however the terapacks enhanced the life even now the self life is increased up to one year WHY you can’t find VERKA ( famous in Punjab ) in neighbouring state AMUL is only Exception .another cooperative which is expanding wings is DElhi’s MOTHER DAIRY … products includes Organic vegetables if you recall old vegetable DHARA ( one of the first mover in refined oil space ) is now part of Mother Dairy .

business is based on uncontrollable Variables : first is types and different varieties of cattles … RAMU KI Gai Ka DUDH …> sold as AMUL DUDH PITA HAI INDIA

Logistics & Skin in game : Logistics plays very important role Low cost refrigeration is used in chillers such as ammonia based . The specialised cold chain storages are required at the warehouses .but the product margin are so thin

Cows milk is also gaining popularity ( even the DONKEY"S MILK IS in trend TOO DEAR to buy 5000 / liter )

The Natures acts are gods acts but can severely affect the profitability of the industry drought effect of last year and delayed monsoons, feed availability was severely constrained leading to stress at farmer level.

The only portion which i like is the skimmed milk but there are global competition if one talk about export . i don’t find a single baby milk formula company sourcing Milk powder from India ( please correct me if i am wrong )

disc: Invested in past for very short span of time and then exited

Hi, the bank loans here likely being working capital limits, utilizations can vary from the sanctioned amounts . Personal guarantees will be for the total sanction and reflect as such - even for term loans the guarantee will not reflect the amounts repaid. We can see in MCA data that the total charges on the Company exceed 500 cr. Also, the increase is about 30 cr, which is reflected in the new charge ceded to Bank of Bahrain and modification of Union Bank’s charge.

Wrote a mail to the company few days back with my queries. Got a call from Investor Relation Team. Following are the notes from the conversation

How has been the response from the Northern Indian Market after the commencement of Sonipat Facility?

The response has been good. NCR region is dominant by Buffalo Milk category. Only Mother Dairy is supplying Cow Milk. Our products have been well accepted by the market. Can do around Rs. 110-120 cr sale from this plant in FY20.

Response from Pride of Cows category is also good from Delhi Market. Our product is of better quality than the local competition.

On Cheese:

23% of our sales is from Cheese.

50% B2C and 50% B2B in cheese we are doing.

35% market share in cheese that they talk about is in B2C category.

Avvatar Brand: Launched 4-5 new variants. Currently doing 3-3.5% of total sales in Health and Nutrition segment (this segment mainly includes Avvatar sales). Aim to take it to 6-7% of sales in FY21.

Floods in Maharashtra: No big impact on us. Our vale added products have high shelf life and liquid milk is not that much share so impact on us has not been much. Farmers in the flooded region affected badly. Procurement price of milk is higher by 15-20% (Rs. 2-3 per litre) as compared to march quarter. For a week may be the prices were higher but not much impact on working on quarterly basis.

Pledge of shares: Recent pledge increase was due to correction in share price. Pledge is not for the loan of company. Pledge is for loan taken by promoters in personal capacity.

If they just focus on their B2C Whey Protein venture, build the brand, raise awareness etc. growth will automatically come. Whey protein is a by-product of cheese-making, and they are already one of the top Cheese-maker in India. They don’t need to build additional capacity as of now.

While ingredients are right and product is right, I was disappointed by the huge variation in their results. Not sure about promoter quality also. I think in FMCG and dairy, there are much many better bets, now with recent correction in some FMCG names, they are even better placed. I had huge expectation from Parag, had entered as it was cheap compared to other FMCG, but it ended up getting cheaper and cheaper. With all value added products that they keep talking about, why are they not even able to increase their profits at 10% consistently also is a big question mark to me…

I invested in Parag because it has the proper ingredients, and given their success in Cheese I thought they could perhaps capable of doing the same with Whey protein too. But they seem to be more keen on entering in more categories (even me-too ones like sweets), releasing more variants of a category, acquiring a brand of similar category with loads of SKUs… than a company of its size is capable of affording. Also, they are doing some Rosy things (airlifting premium milk to Singapore) to probably catch eyeballs possibly in an attempt to achieve ‘FMCG like valuation’ sooner than later.

I exited when the stock hit stoploss near 180. I still believe not much is lost, other than market trust which may take longer to regain. They still have the distribution, the procurement chain, own farm, brands everything. If they take some lesson from the beating of market price, then they will probably focus in near future on things where they probably have the higher probability/right of winning. They should look at their own history, own recipe which brought them success with Cheese, other than doing flamboyance in order to get rich valuation.

Except Gowardhan, haven’t heard any of their brands despite staying in Mumbai and being a frequent shopper. I use whey, never heard of Avvatar (name funny though) till now. Feel, they should expand their distribution and brand. Why don’t they tie up with some renowned celebrity. I see management launching the products themselves everywhere displaying fat bellies.

)

)