My comment on sourcing was on A2 - if it’s something uncommon it would be complex to source as there is competition out there which drives up price or may be we need to create new capacity for it - which requires more capital. As discussed in the article shared above , it seems more of a branding strategy thus I would be happy if this company focuses on value adds where its strength lies.

1 Like

Q1 FY20 Results look average. Sales growth was not much compared yoy and sales were lower compared qoq. Good to see operating margins recovering as compared to Q4. Company also acquired a new brand “Proliva” from Nutrisattva Foods Pvt. Ltd., good to see company getting aggressive in Health and Nutrition segment.

- Gross Margins decreased from 29.64% to 26.40% yoy (29.33% in Q4). Gross margins were lower due to increase in milk prices which were partially passed on in this quarter and remaining will be passed on in next quarter.

- Employee cost increased by 30% yoy.

- Operating margins decreased from 11% to 9.5% yoy (7% in Q4). Margins were lower in Q4 due to increased share of SMP segment. SMP is back to 13% in Q1FY20 as guided by the management in concall last qtr.

- Other expenses were low as compared to Q4FY19, they were higher in Q4 due to some one time expenses.

Regards

Harshit Goel

5 Likes

Can you please share the source of this news? Can’t find it in the attached document or Google. Came to know that the co-founder Shirish Upadhyay of Nutrisattva is the former VP of Parag Milk.

2 Likes

Approved acquisition of “Proliva” not acquired. My bad.

1 Like

Thank you.

Proliva has lots of SKUs in Amazon, just like avvatar. But I hope they will create different value proposition to avoid cannibalization.

IMHO Parag is overdoing in the number of brand & product launches, brand expansions etc. I hope they can afford that. I would be more happy if they spend more energy on increasing brand awareness and distribution reach.

1 Like

Acquisition of Nutrisattva (proliva), looks like a related party transaction.

Founders of Nutrisattva are current & past board members of Parag Milk Foods.

BM VYAS - current board of director in Parag

Ravi Khimani, Shirish Upadhyay - Ex Senior VP of Parag

3 Likes

Any knows why this stock is going down day by day?

Edited Transcript of earnings conference call of Q1FY2020

https://finance.yahoo.com/news/edited-transcript-paragmilk-nse-earnings-195206286.html

Motilal Oswal Report

1 Like

I think the market is pissed off by the recent reshuffling of the top management.

I would say Parag has a better (in terms of experience) CEO now than before. As they have required number of products, what they need is distribution network which Mr. Venkat can help them build.

Coming to price correction it can be because of govt planning for import from AUS & NZ, high raw material prices or PLEDGED shares, no one knows, or there is something that market knows and we are not aware of because the price correction is huge (30% in a month) for above mentioned reasons.

I would personally wait for clarity before buying the dip.

Disclosure : Invested

3 Likes

Heard Q1 Concall and was extremely disappointed. No direct answers! Seemed like mgmt was beating around the bush.

Few turn-offs for me…

-

They said Vector Consulting experiment has been extremely successful and they have completed that experimenr for Mumbai, but when asked to share some data for the same, they sort of backed out saying they will share it "may be in next 2-3 months’. Why? At least share some insights. Just saying it has been successfully in every concall when asked from last 4 qtrs without backing it up with any numbers whatsoever cannot be trusted.

-

Why acquire another milk additive brand - Nutrisattva" when Parag already got a large product portfolio in the same segment with its own brand Avvatar? They proposed to buy this new brand having around 2 cr sales at 80 lacs. But what is the need? No satisfactory explanations given!

-

Why not share revenue numbers or at least give investors some hint about the progress they have made on Avvatar over last 2 years, especially when they were so gung ho about it few qtrs back and launched it with so much fanfare last year? Categorical denial when asked about revenue breakdown can be a policy, but saying that they will share details when something ‘meaningful’ happens (10 cities) is very odd and goes against their own repeatef comments in all concalls that Avvatar is “showing great promise”. I didn’t like this. Things must be backed with numbers especially when the new category is well past the launch date (almost 2 years). It’s okay to say it is making losses or it is not up to the mark till date or they are trying something. But, saying it is doing very well repeatedly, but not backing up with even a trace of numbers is a big turn off. Probably hiding something?

-

Operating Cash Flow explanation was all but convincing! It appeared that the person asking that question was prematurely dropped-off from the call when he tried grilling on the issue. His question was relevant and the answer wasn’t clear. They mentioned something in the last concall and then changed those numbers during this concall. Could be a serious red flag if i understood it correctly.

-

When asked about working capital days, they have always maintained…“it is similar to last qtr”. Well, why not give a specific and direct answer? Though, when grilled with back of hand cash flow and working capital calculation, numbers didn’t add up for working capital days. And the person asking couldn’t continue due to concall rule of asking just 2 questions at a time. It was actually one question, which was followed by an unvlear answer. So he was trying to dig deeper.

-

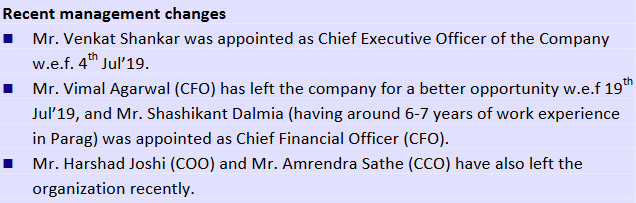

Recent management changes also give an uneasy feeling, especially when they were so upbeat about the talent they managed to bring in order to portray good management feel and FMCG status! Few of those guys joined only a few qtrs back with so much fanfare, with lengthy introductions in concall. Many of them leaving within 2-3 qtrs? Odd?

-

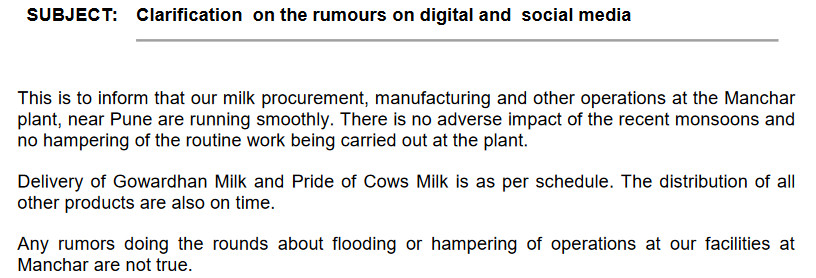

Lifting milk to Singapore and the explanation offered for the same when asked why not target other Indian metros left me stumped. I understand that Pride of Cow is their flagship brand which helps promote Paeag’s overall image rather than contributing to the revenues meaningfully, but at the same time i believe they need to put in their energies in something worthwhile (80:20), which would really count. Lifting milk to Singapore is an eye grabber for sure, but doesn’t help company’s cause. Then, when grilled on the overall plan for this farm fresh milk, they said they want to expand it to 40 cities (currently 2-3 cities). When asked how much revenue they are targeting out of this venture, answer was doubling the current revenue. Well, going from 3 cities to 40, and revenue just doubles. These answers were very incoherent and vague!

-

Constant addition of new brands and products like gulab jamuns and sweets, mishti dahi, top up and what not. Well, it seems they just want to remain in news with useless product launches. No follow-ups whatsoever on the revenue from those products and categories. Then, few qtrs later, they would term those products as experiments.

-

No doubt these guys managed to create two good brands and certainly have a mind-share when it comes to gowardhan ghee and go cheese. But, their persistence for being in limelight and begging investors to give FMCG valuation has always been troubling.

-

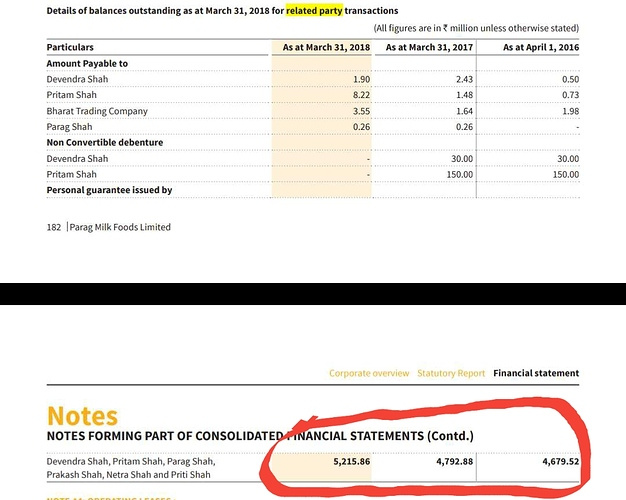

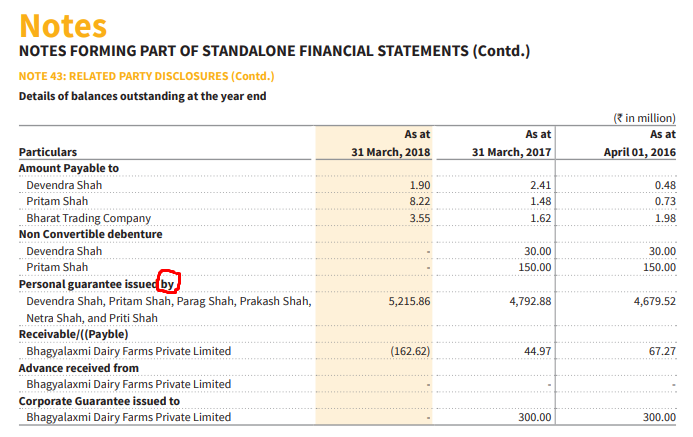

In related party transactions, there is one entry (guarantees to Shah family from the company) which always troubled me (close to 450 cr) and has been increasing every year. I am not sure about the same so i tried asking Vimal Agarwal (ex-CFO) about the same through email but didn’t get any satisfactory answer. He was willing to help me understand it on phone but for some reason i was not able to connect.

Disclaimer: Formed 3% of my pf. Sold at loss, when it breached its previous lows (close to 195-200). I kept holding it despite knowing some of these red flags merely in hope that the brands are real with good shelfspace and their network is good and expanding, about which the scuttlebutt confirmed. Reaized there are better companies with much better corporate governance, where I can sit peacefully despite draw-downs.

40 Likes

some sanity to the thread based your reply…have been tracking it for a while and there are signs which leave one wanting more clarity…airlifting of milk, distribution in NCR, why launch ads when you dont have distribution to back it up…pride of cow/bottle design/celebrity involvement…noise around Avtaar…inviting moneycontrol guys to visit your farm…and yes finally they getting fmcg valuations

1 Like

4 Likes

Could you please point out the schedule and page number where I can find this figure. Thanks.

Note from last year - "This amount is rising every year and is currently 521cr! Loans are just 290 cr with plants and inventories as collateral. Then why is this amount shown as pending to the promoters and is rising every year from last 5 years? I spoke with cfo whose answer wasn’t convincing. He said “this entry would never be realized”, which i take as “until the company defaults!”

But then the amount if shown due to promoters is like a back door and must be shown as contingent liability or must reflect at some other place, not just RPT?. Also i am not sure why would personal guarantees increase when the debt is decreasing."

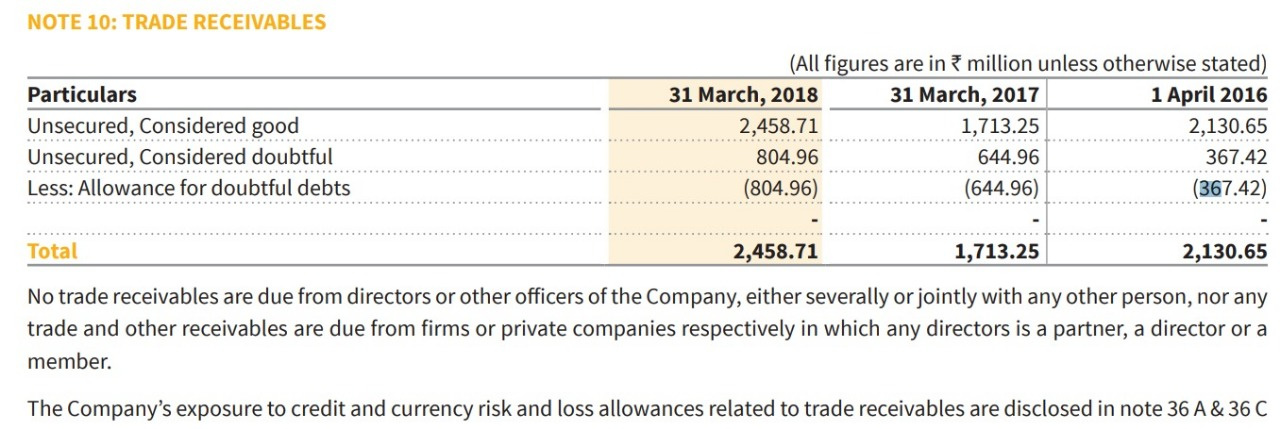

- Another concern on receivables from one of my old note on Parag…

Look at these ballooning bad receivables. Although they have made provisions/allowances for the same which reflects in all three financial statements, this is an area of concern. Why so many defaults especially post IPO. This is gross so figure might look daunting, but look it in light of additional 16 cr bad receivables in FY18 on rev base ~2000.

I am not an expert as far as financials are concerned. Enlighten if anybody got clarification.

13 Likes

I too feel the same and agree to every point you have raised. In my experience, Parag has been trying to do too many things. Due to this the company has been buried in debt and even the cash cow of the company will not be able to get the company to recover.

2 Likes

These are personal guarantees issues by promoters for loans issues by banks to parag, but what is unclear is …why amount is rising every year despite reduction in debt.

agree with @sushildarveshi that this are the personal guarantee issued by promoters… and the reason that this is increasing could be because, they might have pledged shares… and as the price of the share falls, they have to pay MTM… I am not an expert on this but just wanted to share the possible reason…

I didn’t get your point… could you please elaborate…