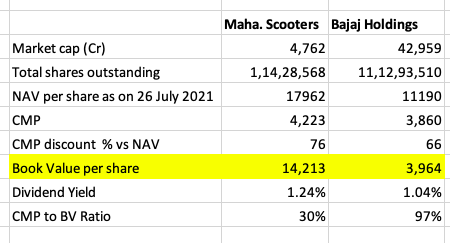

You should only rely upon exchange notices for such calculations. Took me just 5 min to do it. BHIL’s P/B is roughly 30% as of today’s value. Just to highlight that your calc is way off the mark. So pls be very careful for your own sake. And here’s the sheet I referred to.

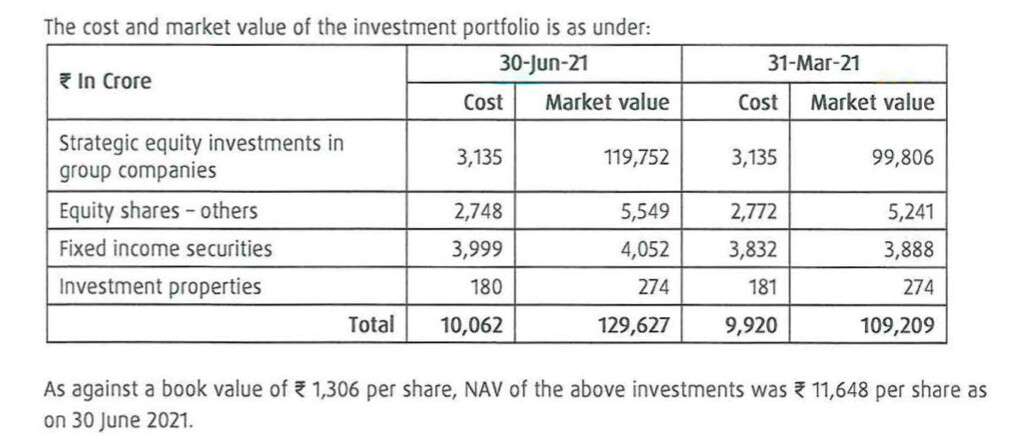

the book value here is even lower at 1306 (vs 3964 in trendlyne and also screener .in).

market value based on NAV (which I refer to as “per share value”… I will correct it as “NAV per share” and edit order of rows for better understanding) is Rs 11648 here while the data from trendlyne was Rs 11190 but thats due to diff dates (Bse report is 30 June, and trending I took 26 July). This part - the discount of CMP to the current NAV - there is no doubt.

But you said P/B is just 30%… are you saying your Book Value = NAV value?

my confusion is highlighted row… why Maha scooters BV is so high vs BH…

Sorry…I meant p/nav.

BV in these holding companies has little relevance just like in case of an fmcg.

I never looked at MSL but my guess is that BV is higher due to maybe a higher acquisition price at which it acquired the assets. But again bv has little relevance here.

As an aside, it is better to invest in underlying companies (if listed) than the holding companies. Holding companies are created for many reasons…mostly to protect promoters’ own interests. From whatever I hv seen, in the long run, a holding company gives a far lower return compared to its underlying assets/companies. However, in the short run, the nav fluctuates, though rarely in a wide band, but could be wide enough to entice us as investors and make us feel we are getting a good bargain….but that good bargain would still lead to a far lower return, if the actual value is being created by the underlying asset/company whose value will grow far more than the holding company.

On the other hand, an investor could justify investing in holding companies saying that - I am ok with a lower return as long as I have a higher protection in bad times as then the holding company price will fall less than the underlying company.

As Dividend Tax is abolished and holding company can transfer dividend without double taxation. This cascading effect will increase the cash inflow of Holding company. And if they choose to pass the dividend then discount is bound to narrow, because of this I see opportunity in this area for next 2-3 years.

Does anyone know why the dividends are not being paid out in full? Ideally the dividends from the investments should be passed through as the new tax laws would allow them to be exempted from income tax but the dividend yield is hardly 1.5% currently.

In the last half year they made a PAT of 136 CR, if they paid it as a dividend there should have been a dividend yield of 2.9% for the half year.

I’m not an expert in reading balance sheets but i see Purchase of investments of 124 cr in the cash flow and divident of 54 cr

I went through the share holding patterns of the held companies bajaj auto, finance and holdings and there is no change in the number of shares maharastra scooters owns.

I went throught the last two annual reports and it looks like they are investing a majority of the money into NCD’s of bajaj finance and other debt instruments.

In this case i don’t think an investment in Maharastra scooters makes much sense, the dividends are being used to buy low yielding fixed income assets that are going to be taxed. It looks like the promoters have some plan for this, they may possible using this company like an emergency fund.

In theory there is a lot of value but if even the cash flows are being hijacked i dont see what the point is in investing in it.

Also a few listed/ unlisted ones which i have not done indepth studies of currently. But will try to update the spreadsheet soon or if any fellow boarder can help with that.

So with layers of discounting - bajaj hoilding itself holds around 50% of Maharashtra scooters the value of the underlying assets is deeper than it looks on the surface…

Thankyou for providing this sheet. It’s been a while since you made this sheet. Can you please update it for the benefit of all to evaluate the holding co. discount?