Introduction:

Bajaj Auto is an automobile manufacture which most of us have heard since decades. The company is into manufacturing motorcycles. Listing down the company’s brands segment-by-segment.

- Entry: CT100, Platina

- Commuter: Discover, V

- Sports: Pulsar, Avenger

- Super-Sports: Pulsar, KTM, Dominar

What’s interesting in recent times?

The company seems very concerned about its current market share of motorcycles and wants to call itself a major automobile manufacturer aiming for market share of about 25%. The revenue growth was spectacular in FY19 with Bajaj’s market share improving by about 3% to 18.7%. Going by number of units, domestic sales increased by 29% and exports increased by 25% in FY19. This is the first time ever where their total sales hit 5 million units and international sales hit 2 million units.

Though they have seen reasonable growth in the Sports segment too, most of growth has come in the entry segment. Hence, the actual Revenue from Operations growth is lower than pure volume growth at 18.3% and PAT growth is at 16.7%.

Apart from that, promoters are buying shares in the market on regular intervals through Bajaj Holdings. Their shareholding increased from 49.3% in FY18 to 51.18% in FY19. Some KMPs of the company also bought some shares through market in FY20. Hopefully, there is some increased optimism within the company.

One can also appreciate that the stock price of the company held still while other Auto companies have seen rampant correction in their stock prices.

Market / Company Data:

Look at the segments data and Bajaj’s performance in those segments below.

| Segment | Market Share of Segment | Market Share of Bajaj in Segment (FY19) | Market Share of Bajaj in Segment (FY18) |

|---|---|---|---|

| Entry | 26% | 35.40% | 29% |

| Mid-segment | 51% | Poor | Poor |

| Sports | 16% | 44.10% | 39.00% |

| Super-sports | 7% | 7.50% | DNA |

| 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | ||

|---|---|---|---|---|---|---|---|---|

| Bajaj Motorcycle sales | 4236873 | 3369334 | 3219932 | 3358252 | 3292084 | 3422403 | 3757105 | |

| KTM India Sales | 50705 | 46321 | 34970 | 30362 | 22627 | 11050 | 7399 |

| Production capacity (in lakhs) | ||||||

|---|---|---|---|---|---|---|

| 2019 | 2018 | 2017 | 2016 | 2015 | ||

| Waluj | 24 | 24 | 24 | 24 | 24 | |

| Chakan | 12 | 12 | 12 | 12 | 12 | |

| Pantnagar | 18 | 18 | 18 | 18 | 18 | |

| Total two wheelers | 54 | 54 | 54 | 54 | 54 | |

| Waluj | 9.3 | 8.4 | 6.6 | 6.6 | 6.6 | |

| Total CVs | 9.3 | 8.4 | 6.6 | 6.6 | 6.6 |

Production of 3W is fungible with production of Qute. Management plans to expand CV capacity to 1 million this year.

Entry Segment:

CT100 is 36% of domestic volumes for Bajaj and is sold at negative margins. The aim is to convert these sales to Platina which has single digit margins. The company slashed the price of CT100 aggressively in order to attain market share. KMP is justifying this pricing game saying that it is just 14% of the turnover.

Platina 110 is at the higher end of entry segment. The price of CT100 was actually slashed at around Q1FY19 and by the end of Q4FY19, the company managed to achieve higher growth in Platina and also slightly increased the price of CT100, but still at negative margins. One needs to validate if this kind of growth is sustainable for longer period of time.

Default risk of loans taken for entry segment bikes are higher.

Though we sell at poor margins in this category, our Exports, Sports & 3W categories give us 20% margins.

Commuter Segment:

As one can see from above tables, the company’s performance is poor in the commuter segment which is about 50% of the motorcycles market. Respected Chairman, Rahul Bajaj, has said that they will fight like never before in this segment to gain market share.

The Discover model has been performing poorly in this segment. The Company has launched 125cc model Pulsar to tackle this segment later. We can expect the company to launch more models in this segment.

In one of Conf Calls, KMP has mentioned that the commuter Segment market share has been decreasing over time. He says the customers are increasingly wanting to own Sports / Performance motorcycles. And the Entry-level motorcycles will continue to see the growth as cycle owners in the country want to upgrade to riding bikes. FYI, commuter segment contracted by 12% in volumes FY19.

Sports / Performance Segment:

Pulsar is a very strong brand for the company in this segment. Bajaj commands 44.1% market share among all Sports motorcycles sold in the country. They have recently launched Neon version in Pulsar brand and they are receiving good traction driven by their aesthetic appeal.

However, Pulsar Neon is priced cheaper compared to other Pulsar bikes of the same horsepower and analysts expressed their concern of whether there is some down-trading which is happening. KMP is justifying the move saying that they are targeting lower purchasing power customers using the Neon models. Another justification is that they will see up-trading from 125cc players due to this move. I think this was the growth driver for the company in Sports segment, but one needs to assess if this can continue for a longer period of time.

Avenger brand is more or less stagnant at volumes of 8000 / month. KMP doesn’t look hopeful on increasing the volumes of this brand. They have done some re-modelling and re-launching but doubt if it will do much for the company, especially when competing with brands at the likes of Royal Enfield. So one shouldn’t expect much from this brand.

Super-Sports Segment:

The Company’s products like Pulsar RS200 and Dominar 400 have gained decent traction. KTM has won special attention among urban consumers.

Bajaj Auto doesn’t directly own the KTM brand but through a subsidiary. It has invested a total of 1219 crores and holds approximately 48% stake in KTM AG of Austria (not just Indian subsidiary). KTM is the fastest growing motorcycle in the world. KTM sells about 212,000 bikes across the globe, with India being the largest market at about 50,000 bikes per year. About 100,000 KTM bikes are manufactured in Bajaj’s Chakan plant. They recently launched Duke 125cc bike and say that it has beaten all of their expectations.

The company is going to partner with Triumph to build and market products of ~350cc products. 350cc is above the horsepower of a typical product from Bajaj and is below the horsepower of a typical product from Triumph.

Exports:

Africa = 50%

South Asia to Middle East = 20%

Latin America = 15%

ASEAN = 15%

As one can see, Africa is the geography which is driving exports for Bajaj. Management expects further growth in exports through Africa. The brand which is very successful here is Boxer. African motorcycle market is mainly a Taxi market and Boxer seems to be doing well here. Other competitors in Africa are mainly Chinese and Japanese.

The company has excellent market share in lots of African countries. For example, it has 68% market share in largest African motorcycle market, Nigeria. Having said that, Africa is not just a Nigeria story. We have 95% share in Uganda, 42% share in Crimea, 60-65% share in Ethiopia. All these markets put together are as big as Nigeria.

One part of Africa which is not very explored is Francophone part of West Africa (West of Nigeria). There was an issue of trademark in these countries. The company got it resolved 18 months ago but in the meantime competition entrenched a lot here. So can take some time to get growth from here.

Speaking of Latin America and ASEAN, most of the exports here are Pulsars. These markets are now fairly penetrated. Further, worth noting that over 85% of the company’s sales come from 21 countries where Bajaj Auto is either No. 1 or No. 2.

Three-Wheelers:

Bajaj commands extra-ordinary market share in 3W market. They are already super strong in the passenger market. Have recently launched product in Goods Carrier market and it has been seeing tremendous growth. Look at below table for numbers.

Bajaj is also strong in 3W exports as can be see in the numbers. Egypt is a large component of 3W exports. Govt is licensing the three-wheelers in the country and putting a lot of administrative work creating a bottleneck in the industry. However, this is temporary and expected to get resolved by end of 2020. It is good for Bajaj in the long term as the industry gets more organized.

Among 3W Exports,

Africa = 35%

South Asia to Middle East = 50%

Latin America = 10%

ASEAN = 10%

| 2019 | 2018 | 2017 | 2016 | ||

|---|---|---|---|---|---|

| Bajaj three wheeler sales | 777603 | 635852 | 444462 | 534995 | |

| Bajaj three wheeler market share | 61.30% | 62.50% | 56.70% | 56.80% | |

| Passenger carriers (3W) market | 1133908 | 894234 | 671034 | 842588 | |

| Bajaj passenger carriers sales | 745254 | 612590 | 431022 | 533670 | |

| Bajaj passenger carriers share | 65.70% | 68.50% | 64.20% | 63.30% | |

| Goods carriers (3W) market | 134792 | 122466 | 112518 | 99945 | |

| Bajaj goods carriers sales | 32349 | 23262 | 13440 | 1325 | |

| Bajaj goods carriers share | 24% | 19% | 11.90% | 1.30% | |

| Bajaj commercial vehicles exports | 378777 | 266215 | 191236 | 280000 |

EVs:

Bajaj is launching EVs through a brand called “Urbanite”. Not much details are available about this right now. They plan to extend this brand to 3W after launching it for 2W.

The Company also plans to setup a separate distribution network for Urbanite instead of re-using the existing distribution network.

Questions / Concerns / Risks:

- Over the past few years, when the growth was mainly in Scooters and when motorcycles industry was flat, why didn’t the company consider manufacturing scooters? The company just grew by 25% in a period fo five years, from FY13 to FY18.

- RE60 which was hyped so well, just seems to be a dumb product. Poor sales and looks like a poor product as well. Though I tried reading about it, I didn’t understand what market they were trying to address. Maybe we can give it an excuse that it is still new to the market

- Is company really expanding its customer base by introducing cheaper categories in Pulsar or diluting its brand in the process? Again, one needs to question if this is a sustainable way to keep growing for the company?

- Slashing prices of CT100 aggressively for the market share. One should justify if this is really worth it as CT100 sells at negative margins? One should track if the company can convert these to Platina 110 and if they convert so, will growth falter again for the company?

- Though this can vary from person to person, I didn’t like the KMP’s answers during the Conf Call. I felt there is a lot of beating around the bush.

- One needs to observe how the company will act when the EV evolution starts to get some kickers / tailwinds.

Financials / Valuation:

You can get the detailed numbers from Screener. Putting down some numbers for starters.

ROCE => 30%+

ROE => 20%+

EBITDA Margins => ~20%

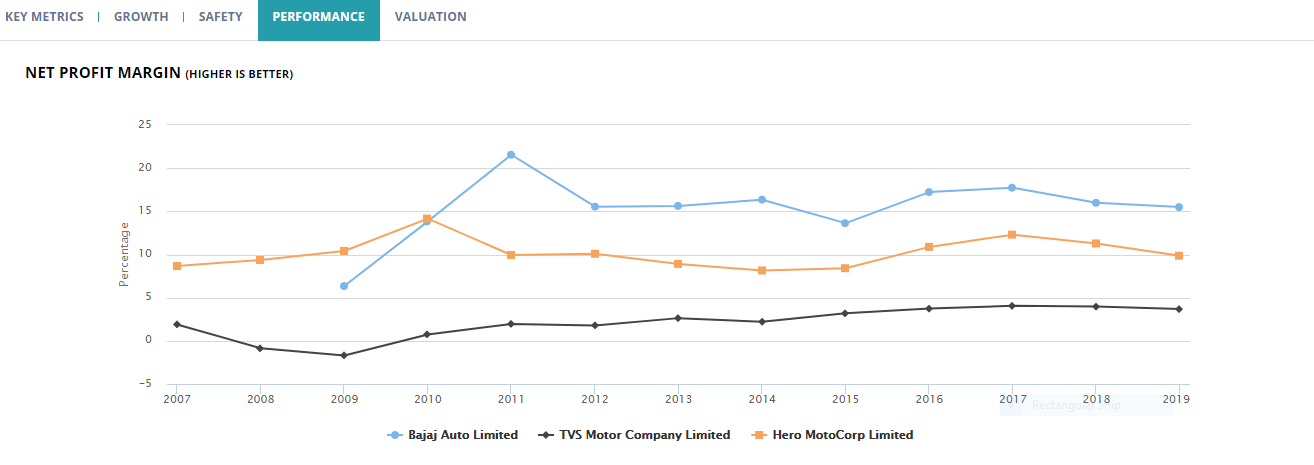

PAT Margins => ~15%

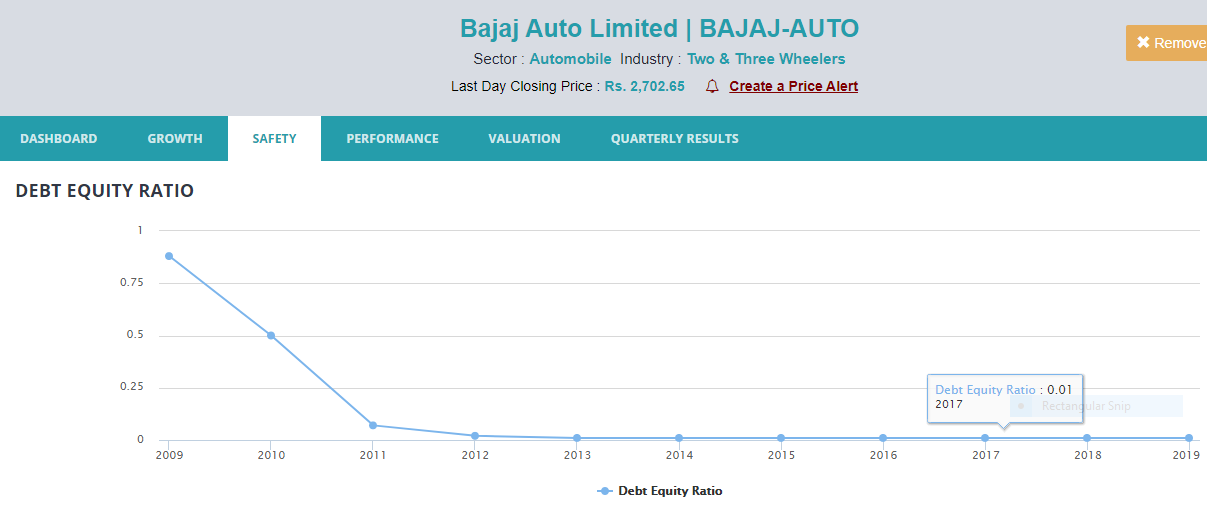

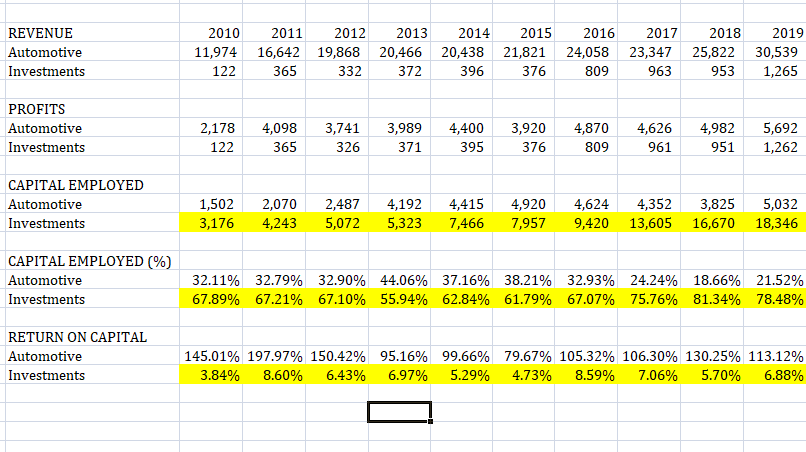

Zero debt + Loads of liquid balance sheet at around 18000 crores of financial investments => They accumulated a lot of cash since no growth over past few years and no capex was needed

Revenue at 31800 crores and PAT at 4900 crores in FY19.

Company is trading at Market Cap of 85000 crores with a P/E of 17-18. Hero, which is competitor, is also trading at a similar P/E of 17-18

Disclosure:

No holdings. Learning about the automotive industry. Please do your own due diligence. All the above content is public information and doesn’t belong to any private entity. Above post is not to be interpreted as a buy / sell recommendation.