I fail to understand why Bajaj Investment Holding Co. which owns ~30% of bajaj Auto and ~40% of Bajaj Finserv is selling for only ~8500 crore. Instead if someone independently purchases ~30% of bajaj Auto and ~40% of Bajaj Finserv, he will have to shell out ~21000 crore. Apart from these two mammoth ownership, Bajaj Investment Holding also owns several other investments on its B/sheet and the company is debt free.

Can anyone explain the rational behind this mediocre valuation?

Its a holding company,holding cos. never trade at market value of its assets. The reasoning is that it’ll never be liquidated. Market does react positively when holdings are liquidated but then again,there are questions like will the cash be given back to shareholders or in what will it be re-invested!

All companies should be valued on the basis of their expected cash flows. It is very unlikely that Bajaj Holdings will sell any shares of either Bajaj Auto or Bajaj Finserv in the near future. So its valuation has to be based only on the basis of the dividends it receives from these entities rather than the market value of those holdings.

It is pretty weird. While I understand why me as a minority shareholder cannot fix this discrepancy, I do fail to understand why Bajaj holdings’ management does not sell stocks of Auto/Finserv to buy back its own equity. That’s a risk free way for it to add shareholder value. Certainly Warren Buffet does it himself whenever he gets a chance. In fact he is ready to buy at 130% of book value, if the opportunity presents itself.

I also checked the promoter holdings are no where near 75%. What am I missing here?

The holding co is a part of the management’s strategy to maintain control on the group cos. Selling significant quantity of shares of Bajaj Auto/Finserv can affect their shareholding pattern in those cos.

While I understand that holding cos. should not be traded at market value of its assets because of overheads involved due to its structure…what is the right discount that should be given to such cos.? What is a right price to buy and sell?

Should it be valued on the dividends that it receives from underlying cos? Well…what if underlying co. is a grower and doesn’t pay dividends? These dividends also may not be passed to the investor of holding co. as it may involve double taxation. Then, why you see some individuals holding good part of some holding cos. as minority shareholders? What is in it for minority shareholder? And if it’s a part of the strategy to maintain control, why is it listed entity in the first place?

I’m invested in few holding cos and want to figure out buying/selling points. Any thoughts on this?

I am trying to understand holding companies, can someone suggest a good write up. I am looking at understanding how to evaluate their fair value and advantages.

I have Bajaj holding for 2 years now and it has given steady return.

Hello friends,

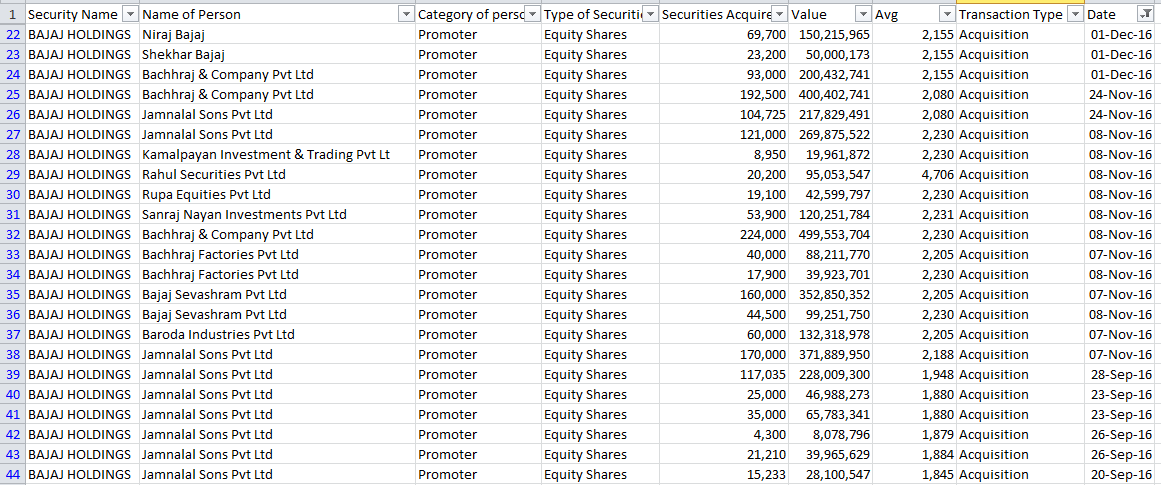

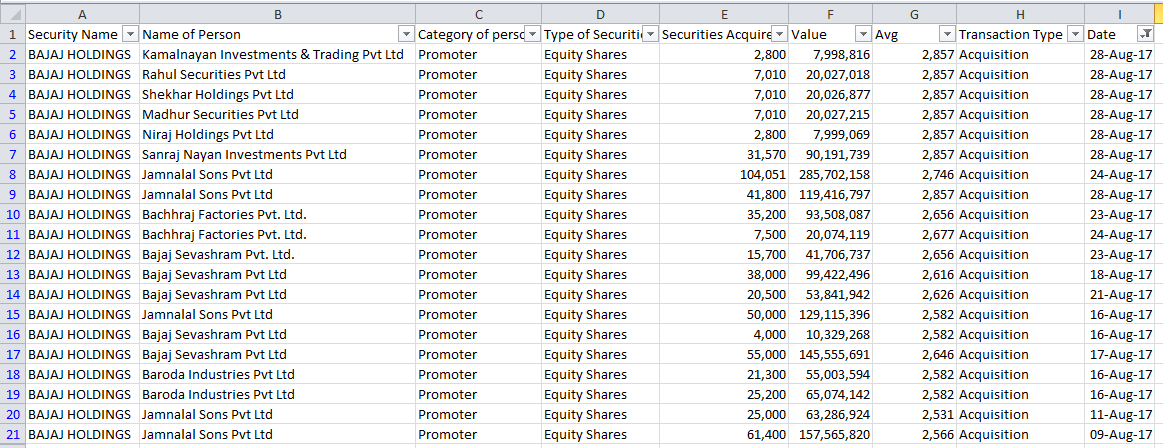

I am watching this stock for last 6 months and I have noticed that promoter is continuously buying shares from open market. So, I am not able to interpret that whether as an investor it is a good thing for me and bad. I have invested a small amount in this stock just for tracking purpose.

Promoter Buying is a good thing and shows conviction. It might mean that the promoter thinks the market price is reasonable or cheap. But we cant say that for sure.

Holding companies have one dominant objective and that is to safeguard the promoters’ grip over the underlying companies. They are not investment vehicles also.Main income is dividend income.

So book value and intrinsic value of the holding company has little meaning for the investor. The potential cash flow is possible but not probable,since it will remain unrealised,because the underlying shares will never be sold.

and @visanty,

promoter buying of holding company shares is a good thing only on paper, since it is only another way of tightening the control of the promoters’ over the underlying companies.

AND @nikhilmoryani,

you are right that even when shares are liquidated, the minority shareholders seldom benefit,since there is no pass through to the minority shareholders.

As to why such limited purpose holding companies are listed,perhaps that is to provide a legal way to retain and increase control of the promoters,at the cost of the minority shareholders,while also raising relatively cheaper-cost funds for doing so.

Can someone knowledgeable on valuation of holding companies give some wisdom or point to any place where we can understand this? The huge discount doesn’t make sense

I agree to your point that holding companies are not best investments but still they seem to do well like Tata investment and even Bajaj holdings…plus dividend is also good. Why do they do well at all if minority shareholders pay all cost , who buys them apart from promoters then and why? Just trying to understand thought process of non promoter buyers…

Hi,

Pls note in the above article that the abolition of dividend distribution tax “may” have a positive impact on holding companies.

Disc: Invested.

Thanks,

Anto