Can Valuepickr’s guide me on the negatives about this company?? Views would be greatly appreciated. I see huge potential in the company coupled with excellent management

Regards

Ramakrishna

Can Valuepickr’s guide me on the negatives about this company?? Views would be greatly appreciated. I see huge potential in the company coupled with excellent management

Regards

Ramakrishna

There is already a thread on this company. Please post your question there. Also follow the guidelines for starting a new thread on valuepickr where a new thread can not be created like above without value contents.

http://www.valuepickr.com/forum/not-so-hidden-gems/218071271#145641055

Sorry the thread is bajaj finance and not bajaj finserve. But still if you have to ask a question then post in the q&a section and not by starting a new thread. Request admin to inform all the members to strictly follow the guidelines. Self discipline is the first thing everyone need to follow to maintain the quality of discussion here.

Hi Manish,

I thought i posted in company Q&A section. Since i saw individual company threads in that section thats why created a thread for it. Can you guide me to the section you are referring to??

Thanks

**

**

Admin,

Can we have a thread where the questions regarding any company can be thrown at the experts who can reply in the same thread? This will prevent too many threads being created. Also we can request the seniors/experts to regularly visit that thread and answer the queries because it is very difficult for them to visit each and every thread.

in this case of bajaj finserv , i think we can continue with this thread.

Ramakrishna - you can post the details, you can present your case like what are the potentials / positives for the company.

why do you think finserv will do well.

a comparison with competitors etc.

Hi Manish,

If the administrator agrees to this thread i will put in my thoughts here.

Regards

Hi Manish,

If here.

Regards

**I think you can go ahead with your thoughts on this thread as there is no other specific place to put the same. **

Thanks Manish. Find below my thoughts.

Good management track record- Bajaj group

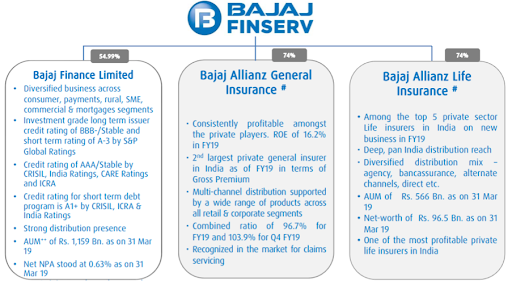

Bajaj Finserv was formed in April 2007 as a result of its demerger from Bajaj Auto Limited to act as a pure play financial services business. The process of demerger was completed in Feb 2008.It holds Bajaj Finance (from July 2010, it is a subsidiary)****, has insurance business, getting into wealth management business including mutual fund business. Read somewhere that its insurance business is 2nd most profitable in the industry.

Financials (Source: moneycontrol and screener.in):

Return on assets: 2.36%

RoE: over 30% over last 3 years

RoCE: 20.79%

EPS: 130 up from 47.6 in 2010

PE: less than 6

Book value: 352 up from 181 in 2010

Price to book value: 2.2

Revenues have grown from 985 to 3904 crores from 2010

Reserves up from 2553 to 5000 crores from 2010

**

**

Update from Sharekhan after Q3 results:

During Q3FY2013 Bajaj FinServ reported a consolidated net profit of Rs248.7 crore (up 46.2% year on year [YoY]) led by a strong growth in the lending business (Bajaj Finance) and the general insurance business. The income from the operations showed a robust growth of 35.7% YoY to Rs1,119.8 crore, leading to a strong 41.8% year-on-year (Y-o-Y) growth in the operating profit.

Life insuranceâearnings growth steady, premium growth slips though

The life insurance business reported a combined profit of Rs331 crore in Q3FY2013 (policy holdersâ surplus of Rs231 crore) showing a growth of 17.0% on a Y-o-Y basis. However, the gross written premium (GWP) declined by 9.9% YoY with the renewal premiums declining by 17.8% YoY. The assets under management (AUM) declined by 0.9% on a quarter-on-quarter (Q-o-Q) basis to Rs40,249 crore.

General insuranceâstrong growth in profitability

The general insurance business reported a profit of Rs91 crore in Q3FY2013 as against a profit of Rs60 crore in Q3FY2012. The gross premiums increased by 22.6% YoY during the quarter while the combined ratio stood at 98.7% (including motor pool losses). As required by the Insurance Regulatory and Development Authority (IRDA), the company provided Rs53 crore (Rs42 crore in Q3FY2012) for motor pool. The profit growth was strong despite a rise in the claims ratio (60.5% vs 58.1% in Q3FY2012).

Bajaj Financeâstrong growth continues

Bajaj Finance showed a strong growth in profit (up 33.4% YoY to Rs160 crore) in Q3FY2013. The growth in the profit was driven by a strong uptick in the net interest income (NII), which grew by 27.4% YoY to Rs504 crore. The deployments of the company grew by 11.9% YoY to Rs5,200 crore during the quarter while its AUMs expanded by 9.6% quarter on quarter (QoQ) to Rs16,844 crore.

Valuations

Bajaj FinServ has delivered steady numbers for the third quarter of FY2013 on the back of a strong growth by Bajaj Finance and the general insurance business. Though the life insurance business remains profitable, but the adverse environment and regulatory prescriptions could affect the premium growth, which, in turn, could affect the future profits.

We believe the increase in the foreign direct investment (FDI) limit to 49% by the government will be sentimentally negative for the company as the company has given an option to its joint venture partner to raise its stake at a pre-agreed price till 2016. However, the company can take shelter under ambiguity in the Reserve Bank of India (RBI)âs circular (transfer of shares to a foreign entity at a fair value). While the profit growth remains steady, the stock has appreciated significantly, leaving little room for upside. We upgrade our recommendation to Hold and maintain price target of Rs892.

Hi Manish,

If

** here.

Regards

I **

Ramakrishna,

You should have started the thread with these details. We are trying to avoid the threads without any homework by merely putting some questions and the whole analysis is put by others.While here you have already done sufficient work to start a new thread. Keep it up.

Thanks Manish, will be more careful in the future.

Regards

others.While

My question, as per your ananlysis above - why not invest in bajaj finance, as it is mentioned in the report that finserv performed well due to bajaj finance n general ins business. in life ins business there is very stiff competition.

Bajaj finserv will be a good investment if we have reasons to believe that the life ins business can grow at a steady rate.

Disc : i am invested in bajaj finance n hence biased towards same.

Hi Manish,

Not looked at Bajaj Finance so cannot comment on it. There are regulatoryuncertaintiesas far as life insurance is concerned which according to me are short term in nature (reduction in commission for ULIPs,etcwhich i think is good for consumers like us) and which has affected its insurance business for last couple of yrs . As i mentioned earlier i am betting on finserv because of huge opportunity in life insurance business (Insurance coverage is in single digits for the country i think) and the fact that it is more profitable compared to its peers.

**

Find below link to their recent investor presentation:

http://www.bajajfinserv.in/images/pdf/inv/BajajFinservInvestorPresentation-March-International.pdf

Hi Manish,

Not regulatoryuncertaintiesas ** ULIPs,etcwhich **** us) ** peers.

My question, as per your ananlysis above - why not invest in bajaj finance, as it is mentioned in the report that finserv performed well due to bajaj finance n general ins business. in life ins business there is very stiff competition.

Bajaj finserv will be a good investment if we have reasons to believe that the life ins business can grow at a steady rate.

Disc : i am invested in bajaj finance n hence biased towards same.

**

Bajaj Finserv Ltd has announced the following results for the year ended March 31, 2013:

The Audited results for the Year ended March 31, 2013

The Company has posted a net profit after tax of Rs. 508.40 million for the year ended March 31, 2013 as compared to Rs. 765.70 million for the year ended March 31, 2012. Total Income has increased from Rs. 1441.80 million for the year ended March 31, 2012 to Rs. 1522.50 million for the year ended March 31, 2013.

The Consolidated Results are as follows:

The Audited consolidated results for the Year ended March 31, 2013

The Group has posted a net profit after taxes, Minority Interest and share of Profit / (Loss) of Associates of Rs. 15736.40 million for the year ended March 31, 2013 as compared to Rs. 13377.70 million for the year ended March 31, 2012. Total Income has increased from Rs. 39047.80 million for the year ended March 31, 2012 to Rs. 50748.90 million for the year ended March 31, 2013.

Bajaj FinServ**

**Recommendation: Hold

Price target: Rs826

Current market price: Rs755

Price target revised to Rs826

Result highlights

During Q4FY2013, Bajaj FinServ reported a consolidated net profit of Rs812.9 crore (up 3.6% year on year [YoY]) led by a strong growth in the lending business (Bajaj Finance) and the general insurance business. The total income (including transfer from policy holder’s account in life insurance) grew by 15.2% YoY to Rs2,018.1 crore, though the higher interest expense and tax outgo resulted in sluggish earnings growth.

**Life insurance-earnings decline YoY as premium growth contracts

**The combined profit of the life insurance business declined by 10.3% YoY to Rs1,022 crore in Q4FY2013 as the gross written premium (GWP) declined by 5.9% YoY. The decline in the GWP was on account of a 13.8% drop in the renewal premium. The assets under management (AUM) declined by 3.6% YoY (5.6% sequentially) to Rs38,003 crore.

**General insurance-strong growth in profitability

**The general insurance business reported a profit of Rs62 crore in Q4FY2013 as against a loss of Rs39 crore in Q4FY2012. The gross premiums increased by 25.5% YoY during the quarter while the combined ratio stood at 105.2% (including motor pool losses). As required by the Insurance Regulatory and Development Authority (IRDA), the company provided Rs59 crore (Rs138 crore in Q4FY2012) for motor pool. The profit growth was strong despite a rise in the claims ratio (69.7% vs 67.6% in Q4FY2012).

**Bajaj Finance-strong growth continues

**Bajaj Finance showed a strong growth in profit (up 51.3% YoY to Rs164 crore) in Q4FY2013. The growth in the profit was driven by a strong uptick in the net interest income (NII) and other income. The deployments of the company grew by 21.6% YoY to Rs5,106 crore during the quarter while its AUMs expanded by 33.6% YoY to Rs17,515 crore.

**Valuation

**Bajaj FinServ earnings showed a marginal growth on YoY basis due to a year-on-year (Y-o-Y) decline in the life insurance earnings, though the other two segments (ie lending and general insurance) continued to report a strong growth. Going ahead, the growth in the insurance segment will remain subdued due to a change in the regulations and company’s focus on rationalising the cost structure. We have reduced our growth assumptions for the life insurance business, resulting in a reduction in our sum-of-the-parts (SOTP) based price target to Rs826. We maintain our Hold rating on the stock.

Source: Sharekhan

A very dumb question from a beginner. At what point is a parent/holding company more attractive than a subsidiary ?

Bajaj Finance is trading near Rs 7000 while Bajaj Fin Serv is trading near Rs 1850. since Bajaj Fin Serv is holding 57% of Bajaj Finance shouldn’t the parent be worth atleast 57% of subsidiary ? or framed it the other way, isn’t it cheaper to own 57 shares of Bajaj Fin Serv by buying 100 shares of Bajaj Finance ?

ok, ignore above comment. After a bit of analysis it seems my assumptions were wrong.

lets assume there are

1000 shares in parent

100 shares in child

100 parent = 57 child is not logical

actually parent has only 57% of child

so 1000 parent has only 57 child

so 1 parent has 57/ 1000 shares of child

i.e . only .057

5,38,72,190 - total shares in BF (Bajaj Finance)

15,90,91,745 - total shares in BFS (Bajaj Finance services)

3,08,56,613 - total shares owned by BFS in BF

1 share of BFS = 3,08,56,613/ 15,90,91,745 shares in BF

1 BFS = .1939 of BF

100 BFS = 19.39 shares of BF

If one see that the Consolidated Profit of the Bajaj Finserv. Bajaj Finance has played Very big role here ( 40% of the Total profit ).

I am surprised to see Bajaj Finance hasn’t moved up.

Is there some other news ?