A friend of mine who is also shareholder attended their AGM in July and asked Sanjiv Bajaj about the possibility of demerger, to which he replied “we are not in the business of closing businesses”. So looks like they might continue with the current structure. It is still a hold if you are positive about Bajaj Finance and any rationalization of dividend distribution tax will add to the upside.

Is anyone still following this stock?

Well, I calculated the valuations and discount again at CMP and think it can be a value buy at these levels with good margins of safety.

Edit - It ran up by 20% in a couple of days after this post. (Valuepickr power? ![]() )

)

Discl - Added around ₹2500 odd levels in last couple of days.

7 Likes

The current discount b\w holdings and investment value and mkt cap is 71%. For those who’ve been holding this from long time, what is the avg. annual discount to investments value that this stock trades at.

Also, if anyone attending this year’s AGM, are there any plans of promoters to dissolve to co. now?

The co’s holding discount should narrow now based on 2 below developments : -

-

The promoter holding coming entirely under the gambit of Bajaj Holdings. With ownership control tightened I blv the promoters will have a clear strategic call on managing the investments.

-

Owing to change in DDT policies, holding cos. are better off paying more dividends now. This might be the case here as well, the co. may start throwing out more dividends pay-out and this combined with the appreciation of underlying investments might make a trigger to narrow the Holdco. discount.

Disc : - Not invested yet. Trying to get more clarity on above points. I’m interested however because it seems to be the cheapest way to play on Bajaj Finance and Finserv businesses.

1 Like

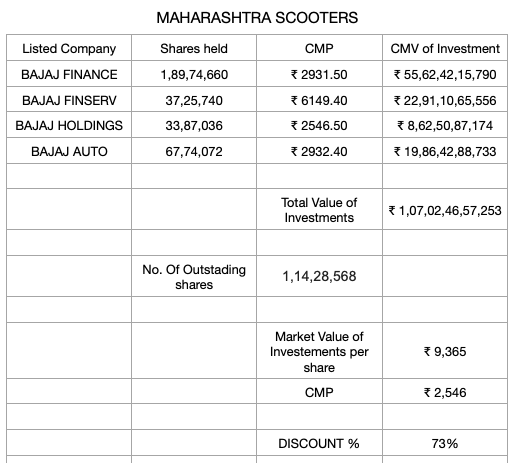

Hello all, this is my first post on Maharashtra Scooters Ltd (MSL), I got interested in this company after a simple search using the “Net Cash” formula advocated by Peter Lynch in his book. I was extremely surprised when I saw the value of investments which is = “Cash And Cash Equivalents” in the Bajaj group shares: Bajaj Finance, Bajaj Auto, Bajaj Holdings & Investments, Bajaj Finserv in the Balance sheet (BS)

The valuepickr forum ignited my interest and made me investigate it further after seeing that something like this is already been discovered and discussed and started following this counter, I remember @shardhr asking about the avg discount to investment value it trades at, so I thought let’s try to calculate it.

I got to work and started digging up the numbers from the Annual reports of MSL from the BS readily available on Tijori FInance.

Since AR13, the investments under Non-Current Investments: Fully Paid Equity Shares: Quoted: have not changed.

The core holdings in Bajaj Finance, Bajaj Finserv, Bajaj Auto and Bajaj Holdings and Investments have stayed the same. However, in AR14, the company sold it’s investments in Bajaj Hindusthan (So I have safely ignored that in my calculations, which had no material value to it) and only taken the core holdings into consideration which had substantial value.

One more thing, In AR17, Baj Finance announced a split of Rs 10 to Rs 2 and also announced a 1:1 bonus, therefore, the number of shares in the AR17 of MSL shows 18974660 in the later ARs instead of 1897466 (1897466 shares were visible in the AR13-16) (it does not affect the calculation just a point that I wanted to share before I start explaining.)

Since the Investments from AR13 till AR20 have remained the same as the core holdings, I got the daily closing price of all the investments in the BS using Google finance in Google sheets.

Then I multiplied the number of shares of that investment with the price that security closed that day, and did this with all the other investments.

I got the aggregate Value of the investment for that specific day, Since the number of shares of MSL have remained constant and haven’t changed, I divided the aggregate value with the number of equity shares. I got the Net Value per MSL share

That is how the investment value or “Net Value Per share” was calculated, I then took the price of MSL for that specific day and used this formula:

MSL PRICE / MSL INVESTMENT VALUE

This gave me the percentage value for which the investments in the BS of MSL were trading at.

For example, if I got 0.42 or 42% this indicated I was paying Rs 42 for Rs 100 Investments in the Balance Sheet.

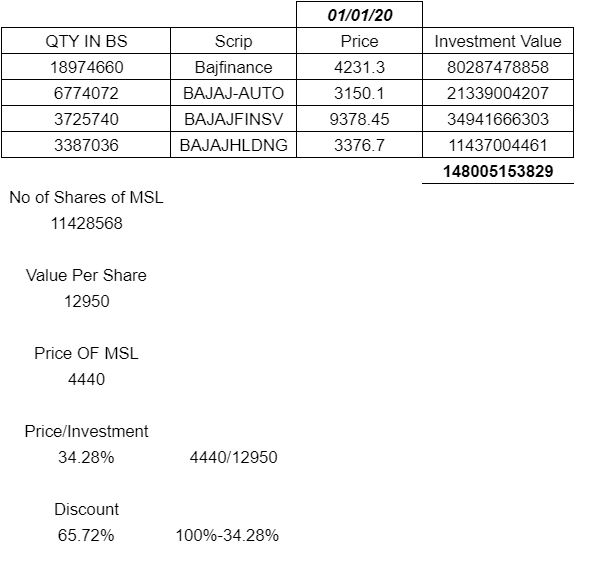

I am also attaching a sample calculation to explain it better:

This calculation has been done for 01/01/20.

Above calculation implies that on 01/01/20 the Price/Investment value was 34.28% and this discount was 65.72% which is simple 100%-34.28%.

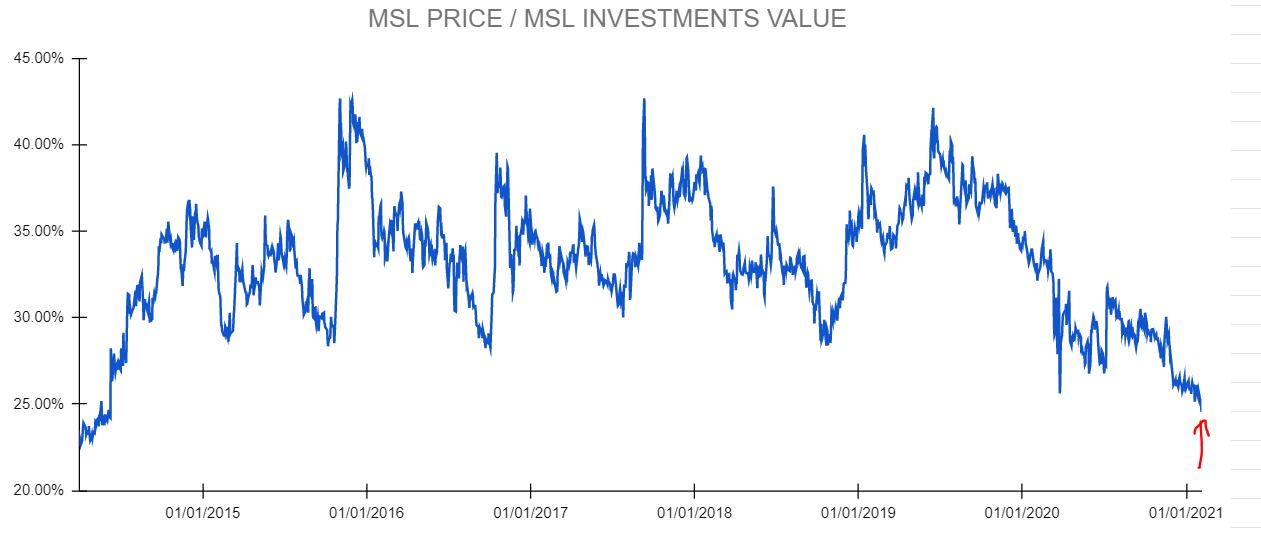

I did this calculation for the last 7 years since AR13 till AR20 daily using historic data

Date: 01/04/14 to 17/03/21

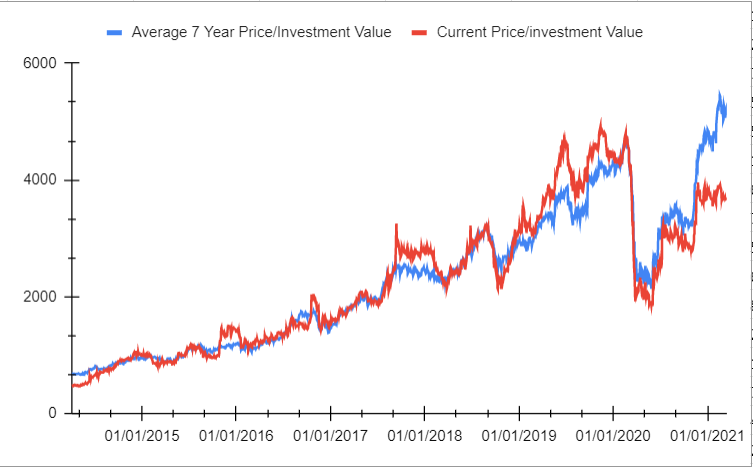

I have attached a graph to have a look at the historic price/investment value it is traded at.

Max Value: 42.68%

Min Value: 22.59%

Average: 32.97%

SD: 3.86%

Currently, the price/investment value is at 23.37% (17/03/21) which is extremely low according to the historic data:

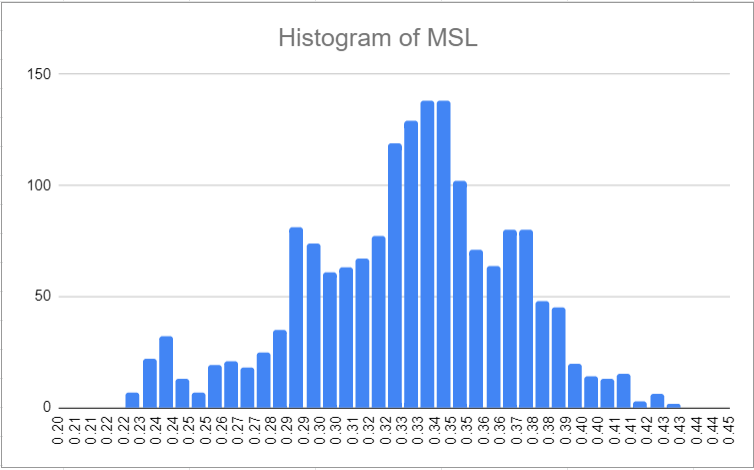

Using a histogram and considering it to be a Normal Distribution, it has only been lower than this 0.6383% of the times and 99.3617% more than this, which indicates a really low probability of this value decreasing.

(Kindly note the data is not a normal distribution in reality, but it has been considered one to simplify our calculation and analysis)

Histogram:

I am also attaching a graph if we were to assume the long-run average to be 32.97% multiplied value per share(this is not 100% correct but this could help us analyse the situation a little better) and comparing it with the actual price/investment value multiplied with the value per share.

Conclusion:

Answering the common query what is the overall discount to this stock

the answer is 100% - 32.97%= 67.03%

Avg DIscount: 67.03%

Current discount 17/03/21 76.63%

Avg Price/investment Value: 32.97%

Current Price/investment Value: 23.37%

If we were to assume the current price/investment value to move to the 7 Year daily average this implies the current price of MSL to be 4994 which is currently trading at 3540, which is a 41% return!!!

Risks:

- if the value of the underlying assets falls dramatically and there is no fall in the MSL share, this will increase the price/investment value, which will hurt our position.

- This is just based on my observation and I might have missed some key variable while making this observation, it is also possible that I could have made some error which could prove fatal if one were to take this as investment advice, it is NOT investment advice just an interesting thing I noticed and which I wanted to share with all the VP members.

Few more things:

1.The average keeps changing daily along with the SD and the probabilities as and when the new data is updated in the google sheet, I will post the table again very soon if there is some major movement in the price/investment value.

That marks the end of this post. I am eagerly waiting for the input of the other VP members.

One last question is this really an opportunity for us to go forward and take a position in MSL or is the market hinting towards correction in the core holdings of MSL (which will increase the price/investment value and contract the discount that is currently available)

What do you think?

Disclosure: Invested.

12 Likes

@Shivansh_Bansal :- Nice write-up.

Supplemental to ur above understanding will be Moerus grp’s latest letter which I shared on other thread : -

This contains a very insightful discussion on investing in holding companies by Amit Wadhwaney. Please check out.

Whr things get interesting in Bajaj’s case is that thr are essentially 3 holding cos. structure : -

- Bajaj Finserv

- Bajaj Holdings & Investments

- Maharashtra Scooters

All 3 trade at discount to thr Fair value and with majority control the fair value realisation lies in thr hands. Wat is needed to be analysed is in which case thr are triggers for narrowing up the discount to Fair value and how sooner or later - e.g - Bajaj Finserv is a spawner for finance businesses so I dont think that structure is going to collapse in near term.

I primarily chose Maharashtra Scooters (and that was more than a yr ago) because : -

(a) The discount here was widest and it still is

(b) The majority shareholding came under Bajaj’s mgmt after settlement with WMDC. So, either the Bajaj mgmt collapses this structure or continues - It will surely be better managed

(c) With Maharashtra Scooters, one gets exposure to Bajaj Auto. Now this is completely personal choice as in if u want to avoid exposure to Auto sector than one can go for Bajaj Finserv. Also if one wants more diversified exposure to equities than one shd go for Bajaj Holdings

Thoughts??

Disclosure : - Invested

2 Likes

@Shivansh_Bansal Very insightful post!

Coming to the question: “is this really an opportunity for us to go forward and take a position in MSL or is the market hinting towards correction in the core holdings of MSL (which will increase the price/investment value and contract the discount that is currently available” - I have a couple of points:

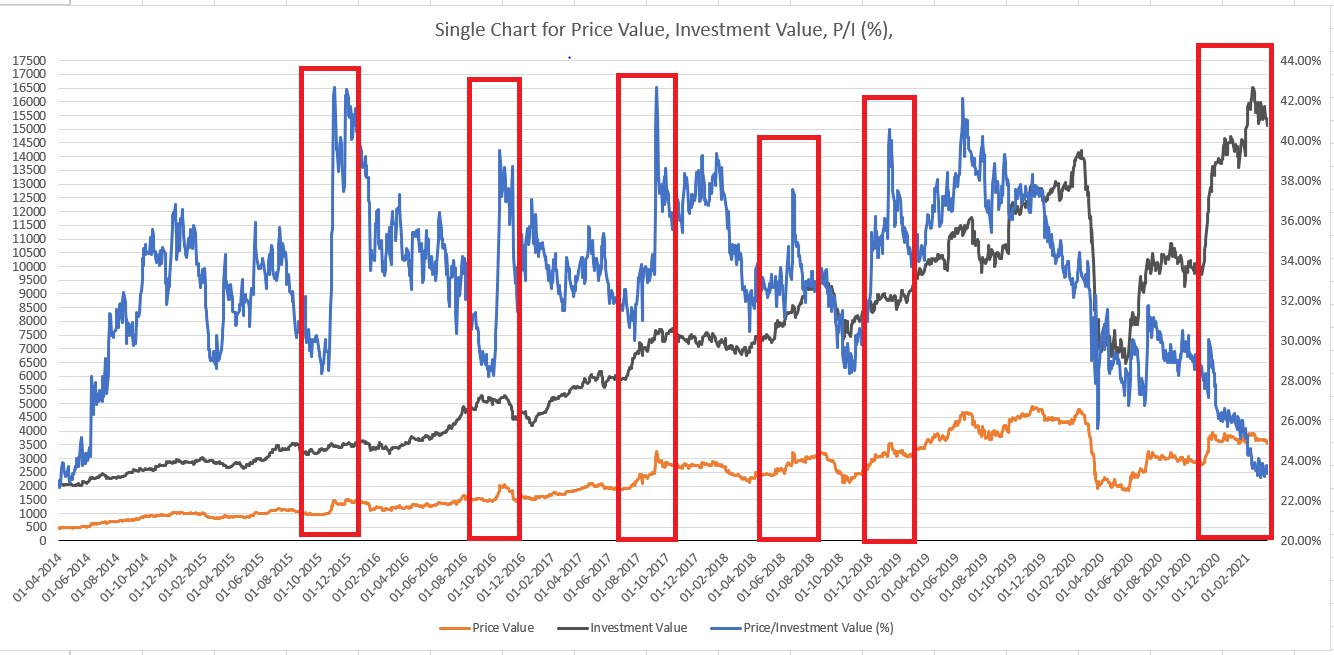

- From the “MSL PRICE/MSL INVESTMENT VALUE” ratio trend we can see that it has mean reverted 5-6 times in last 5-6 years (ratio increases after dipping below ~30%). If you have the data readily available, can you please put MSL PRICE, MSL INVESTMENT VALUE and the ratio MSL PRICE/MSL INVESTMENT VALUE in a single line chart? This will let us see if the mean reversion in past instances has happened due to MSL PRICE increase or decrease in MSL INVESTMENT VALUE.

- I think there is also a structural change in the composition of the MSL INVESTMENT VALUE - this is increasingly driven by Bajaj Finance/Finserv in the period you have taken. So, we need to consider that this might be a structural change in the discount rate.

Disclosure: Not invested

Let us look at 1 year and 5 year returns from MSL vs the underlying companies it holds as investments.

| Returns | 1 year | 5 year |

|---|---|---|

| Maha Scooters | 26.8% | 2.8 times |

| Bajaj Finance | 79.2% | 8.3 times |

| Bajaj Finserv | 52.5% | 5.8 times |

| Bajaj Auto | 64.9% | 1.6 times |

| Bajaj Holdings | 35.9% | 2.4 times |

The numbers tell their own story and what the market thinks about holding company.

With the benefit of hindsight, let us look at this. On a 5-year basis, Rs 100 invested in MSL would have grown to Rs 275. However if Rs 100 was split equally in the four investee companies, the investment would have grown to Rs 452.

With MSL, one really needs to hold till the “trigger event” for narrowing of discount happens which can take many many years! The question is - how much patience do you have?

5 Likes

Chasing indian holdco discounts, especially those run by promoter entities is a tricky game to play. The majority stakeholder doesn’t have any incentive to pay the minorities a price in excess of the current market price, irrespective of its intrinsic value. In the case of Maharashtra Scooters, it is even more complex since the holdco has a very small market cap and Bajaj can keep ignoring it / squeeze the minorities at throwaway prices by making one of their private promoter entities take over the minority shareholding. The same was incurred by WMDC, a MH Gov holding, who got paid way less than its intrinsic value. Hence in my view, I don’t see the discount closing down by a huge margin (apart from minor monthly fluctuations).

I am much more comfortable owning Bajaj holdings given the size of the co, and it’s existential purpose. Amit Wadhwaney from Moerus too has invested in the later than the former.

Disclosure: Not owning either, this is not an advice, please do your own due diligence

1 Like

Gaurav,

The point you are referring about lower price given to WMDC is technically not comparable because there was already an agreement with WMDC for their stake sale to which promoters had done written agreement . ( details of the case argument)

secondly how can minorities be squeezed by private promoter entities .Request you to kindly elaborate. Any previous similar cases ??

I can see names of Ramdevji and Motilalji in top shareholders list , i dont think bajaj group will loose their credibility .

What I meant by a minority squeeze was something like this:

Scenario 1- Bajaj intends to buy-back the shares in Maharashtra Scooters, Bajaj sees no incentive in paying above the current discounted market price. Shareholders either accept and sell @ discount or the buy back doesn’t go through.

Scenario 2- Bajaj doesn’t care about a small co. like Maharashtra Scooters, let’s it languish for the foreseeable future. The discount keeps getting wider with no activity from the management.

The only triggers will probably be when someone intends to merge/acquire a controlling stake in Bajaj entities and thereby offers to buy-back Maharashtra Scooters at a higher price than that which is currently being quoted. I doubt Bajaj will be selling any of their entities unless they face some severe financial distress.

Regarding Ramdeo, his stake is quite small and major entities like PPFAS were also holding shares in the co. but their patience ran out and they reinvested the proceeds in Bajaj Holdings.

But I can be wrong, and your views can differ from mine.

1 Like

Hi all,

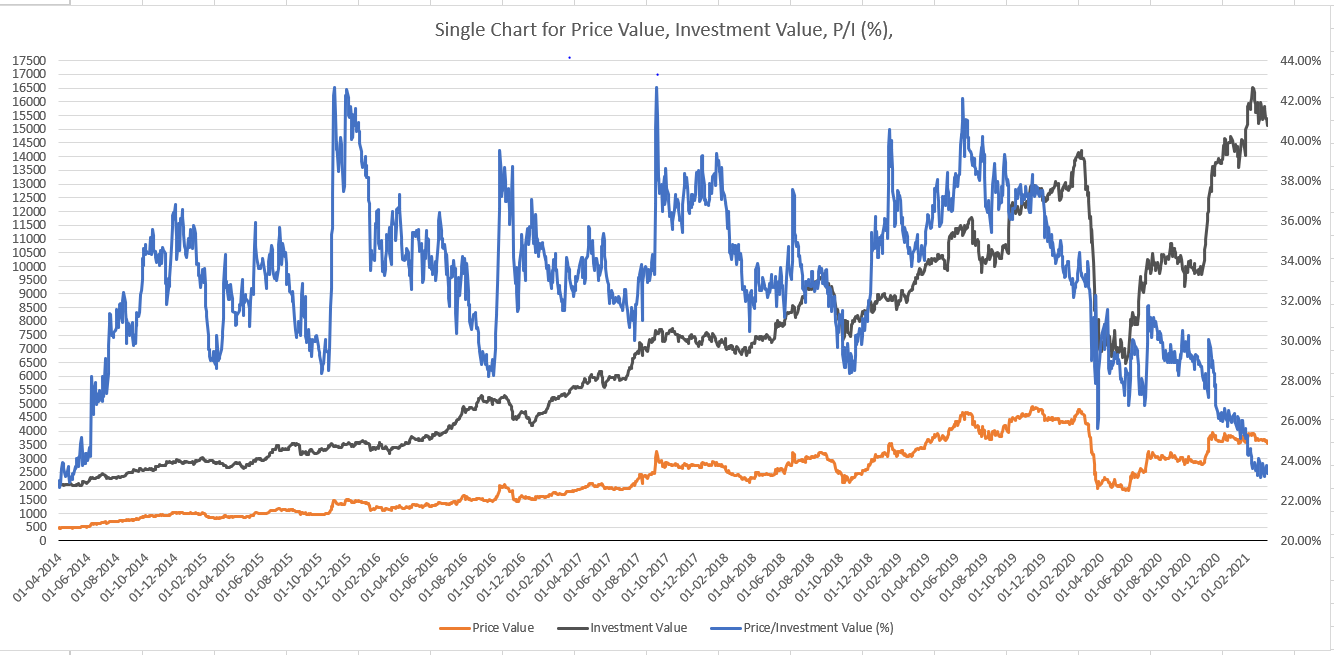

I have constructed the graph which @anirband87 asked for, I think this graph can actually help us understand things better and actually reveal if the change in P/I value (Price/Investment value)

(which is nothing but 1 - Discount %) is due to this factor or because of the change in investment value held by MSL.

This is the graph, which I have constructed using the data available to me.

1. Orange line: Price Value (The closing price of that day for MSL)

2.Black Line: Investment Value (Core holdings of Bajaj group with MSL calculated using the closing price can also be called the ‘Book Value’ or “Net Value Per Share”)

3.Blueline: P/I value (%) (Price/Investment value %, which I had presented in the previous post)

On looking at this graph the first time, It was extremely overwhelming but on closer observation, I noticed something.

I noticed several spikes in the MSL graph (on a closing price basis) during several periods specially when the P/I Value touched 27%/28%, this spike might look small at a first glance and one might think that it doesn’t really mean anything substantial but all those awkward spikes indicate a return of 20/30% at least and one can actually observe this easily.

Talking about the orange line, MSL price on closing basis

1st spike: Takes place near 01/12/15 when the “Net value per share” was increasing steadily but the Price of MSL (price value) was decreasing rapidly which brought down the P/I to 28% odd levels, and after touching that zone it spiked significantly.

MSL went from 900 levels to 1400 levels

2nd Spike: Takes place near 01/12/16 when the “Net value per share” was increasing steadily but the Price of MSL (price value) was decreasing rapidly which brought down the P/I to 28% odd levels, and after touching that zone it spiked significantly.

MSL went from 1500 levels to 2000 levels

3rd Spike: Takes place near 01/10/17 when the “Net value per share” was increasing steadily but the Price of MSL (price value) was increasing at a slower pace which brought down the P/I to 30% levels this time and after touching that zone it spiked to lower 40% levels.

MSL went from 2400 levels to 3050 levels

4th and 5th spike: These spikes were absolutely meaningful but the fourth spike never reached attractive levels for a person to take positions, the 5th spike actually tested the patience of the investor, it had touched a good level back in 1/12/18 but took almost 6 months to reach a good level for us to offload our position.

My Observations:

The common thing in all these spikes was the gradual decrease in the P/I level, with a steady increase in the investments but the price of MSL decreasing/growing at a slower pace than compared with the Investment value.

but…

This time MSL has actually retested the 7 year level and the P/I Value (%) is now at 24% levels and has been significantly decreasing for the last one year since the infamous crash back in 2020. The P/I value decreasing, Investment value shooting up rapidly and Price value of MSL decreasing or growing slowly does match with what we have observed in the past, but the past barely resembles the future…

Is this scrip actually testing the patience of the investors and will soon be rewarding them with handsome returns or the discount will continue to be at such high levels only?

Where are we really headed?

Let me know ![]()

Disclosure: Invested.

8 Likes

Hi Shivansh, This is amazing work…thanks.

As a holder of mah scooters for over a decade now i always wanted to

construct something like this but found it daunting.

1 Like

Gaurav_Sheregar,

Can you kindly share the stake (the exact quantity of shares) PPFAS held prior to disinvesting it in favour of Bajaj Holdings? I am not able to understand why they preferred Bajaj Holdings over Maharashtra Scooters. What makes you think ‘their patience ran out’ ? Have you anywhere come across such a statement made by them? In what ways do you think investing in Bajaj Holdings requires less patience?

Disclosure: Invested

Hi Sudhakar, I talked to PPFAS just after they did it as I was curious too. They said they were growing AUM and had a liquidity concern. That was the only character for the switch. Liquidity of MahSco compared to Bajaj Holdings. …

Hey Sudhakar,

I am not sure why PPFAS sold and diverted their stake to Bajaj holdings, one can never be sure of the exact reasons unless one works in the investment team of PPFAS. So yes, it is my presumption that they felt they will be able to generate superior returns in the later. But that is not of much concern to me as PPFAS can be wrong too, so one should not take that at face value.

I have highlighted my concerns in the above points of why Maharashtra Scooters can take a long long time (maybe never) to see its discounts narrow down/disappear. If you feel otherwise then probably we can discuss your narrative

Regards,

GS

Ppfas sold & converted to Bajaj Holdings as they wanted to reduce exposure to Bajaj Finance, as they felt it was overvalued then. I guess Bajaj Holdings is relatively leaner on Bajaj Finance.

IMO, the triggers for this undervaluation gap to close will be a cigar-butt’s reversion to mean.

The charts and 5-yr performance data shared above are clear contrarian indicators of that. Not saying that it’ll outperform the underlying cos. but the risk is better covered here in case any of the underlying cos underperforms. Also 2 more factors to consider : -

(a) With consolidation of promoter holding under Bajaj grp, they might diversify some funds into other debt\equity investments making this a small-version Bajaj Holdings. They have no plans of closing out as confirmed in the last AGM.

(b) With dividend payout policy becoming favorable frm last yr, relatively better payout is expected. This driver vl also make valuation attractive on dividend yield basis.

Disclosure : - Invested

@Shivansh_Bansal Kudos to you for your efforts and research as it had provided valuable insight.

I just came across company called Hindustan housing company - only listed in BSE, almost no trading happening in this counter and promoted by Bajaj group.

CMP is 35 INR and book value is around 9000.

There is one more example ELCID Investment though not bajaj group. It had investment in Asian paints and same - no trade happening as price is around 15 and book value is 4 lacs and All trade happens in grey market around 85k.

Would wonder if there is any possibility that same could happen with Maharashtra scooter?

Thanks!

4 Likes

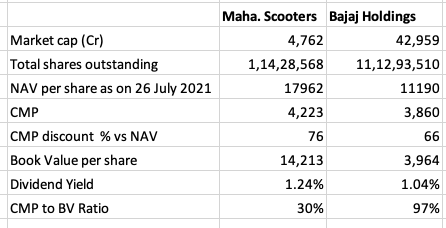

Here is a rough comparison between Maharashtra scooters vs Bajaj Holdings.

I used trendlyne site data for value of holdings.

If you had to choose between the two on pure value basis, Maharashtra Scooters looks better as it has higher discount (so has to catchup to Bajaj Holdings discount) and gives better dividends.

I don’t understand why Maharashtra scooters book value is so high though compared to Bajaj Holdings, if both companies are just investment holding vehicles…