Yes, they have 487 crores voda provisioning left.

Please share the residual duration for the Voda Bonds if you have the data.

But still the fact remains that if the 811 + 324 crores that is 1135 crores were not written back they would have posted a loss for the year.

Just goes to show that the inherit retail franchise is not as strong as it is claimed to be and have created a negative book value by itself.

Retail stress is camouflaged by previous years losses that they showed.

2 Likes

.

Reducing interest rates on saving accounts and FD twice in a short span of time , Trying to move towards safe segaments like prime home loans instead of their usual stated USP ‘high-yielding loans to underbanked’ and opening almost no new branches from last few months…most of us are seeing these steps as positive but can all these be signs of underlying stress…???

9 Likes

I have been a huge admirer of how this bank has transformed from being predominantly wholesale to a retail one, both in terms of assets and liabilities within a period of 2 years.

Mr V Vaidyanathan has done a fabulous job at it and deserves full credit. He has also been quite unlucky that since the merger while he was busy crafting a bank of his dreams, termites like DHFL, Reliance Capital,Cox & Kings, Sical Logistics,Vodafone ate into very precious capital that was needed for a start-up bank like IDFC.

Inspite of all this, he kept the boat moving positively with a CET-1 of ~14% thinking that he will raise capital 2-3 years down the line at good valuations.

Then COVID happened and everything went haywire. The bank raised 2000 crores at below book valuations, his own stock got sold at Rs 20/share and Covid provisions skyrocketed in Q1,Q2 and Q3.

Although Covid and other previously mentioned termites did drill a huge hole in the balance sheet, the moniterables looked quite promising in terms of CASA, Retail growth, Margins and Management commentary.

However, Q4 results yesterday have shaken somebit of my confidence because of the following points:

-

Additional Provisions of Rs 375 crores for Covid. If this is for future Covid wave 2 then understandable, however if it is for poor repayment behaviour observed in Q4 then it raises questions.

-

There is a change in management commentary with respect to the model of business they want to follow. From a ‘high yielding loans’ rhetoric, it seems to have mellowed down to ‘prime retail loans’ with more focus on customers with high credit scores and shy away from ‘New to Credit’ customers. This sure can have an impact on Retail yields which we need to factor in.

-

The sudden reduction in interest rates on savings accounts which would improve NII could also indicate further provisioning for stress but could backfire with CASA coming down. I personally know a lot of people keeping huge CASA balances(upwards of 15 lacs) who are very unhappy. With digital mobility, I think customer stickiness which VV keeps on talking about may not be that sticky anymore.Need to monitor.

-

This sudden reduction in interest rates could also be attributed to new investors(via QIP) presurring on profitability numbers.

-

The QoQ growth in core fee income seems to be poor at 3%. Either Q3 fee income was window-dressed for the impending QIP or there seems to be a slowdown. Old banks like HDFC,Kotak can sail through a low loan growth environment but a new bank like IDFC with high C/I will have to struggle if Covid wave 2 persists longer.

In conclusion, the cart that VV is pulling seems to be getting heavier and the heavier it gets the slower he will be able to pull it. He has given it his best but external factors have taken a toll for now.

15 Likes

See there is no doubt that the retail book has been impacted by Covid but that is true of all retail focused lenders. The important question is has the impact on IDFCB been more or less than competition and what has been their relative performance? Feel free to add to the below but this is how IDFCB has done vs Bajaj, ICICI and Bandhan, three retail focused lenders-

Credit Cost (Provisions+Writeoffs)

IDFCB- ~2% and 3% if I include the Vodafone provisions transferred; P&L impact is roughly 2%

Bandhan- 5%

Bajaj- Roughly 4%-4.5%

ICICI- 2.2%

NNPA

IDFCB- 1.8%

Bandhan- 3.5%

Bajaj- 0.75%

ICICI- 1.14%

Additional Provisions that can be used for Covid

IDFCB- 375cr+500cr Vodafone or 875cr or roughly 0.8% of advances

Bandhan- 388cr or roughly 0.4% of advances

Bajaj- 840cr or roughly 0.55% of advances

ICICI- 7475 or roughly 1.1% of advances

Bajaj has aggressively written off bad loans which is why the credit costs are so high and NNPA’s much lower. Based on the above IDFCB seems to have come out of the last year in decent shape and well placed going into next year and no worse off when compared with competitors. Also keep in mind the relative valuations and that IDFCB is by far the cheapest of the lot; so its not a case like Bandhan where the valuations are totally out of sync with relative performance. Cost/Income continues to be high vs competition but we should start to see a substantial impact from the the cut in SA/Deposit rates that has been done in Q4FY21 and Q1FY22. With a CASA balance of 45,000cr a 2% cut in rates alone adds 900cr per year to NII which is like 13-15% of FY21 NII.

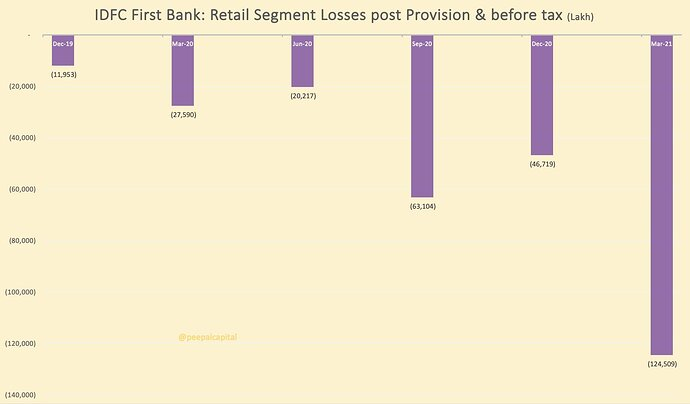

Somebody had posted this pic-

Would have been helpful to add context to this chart as all new branch opening costs are captured in the retail segment, thats why there is a consistent PBT loss. In this time period branches have gone up from 420 odd to 600.

12 Likes

Tried to model IDFC First future growth in a sheet based on guidance given by VV till date.

Guidance summary by VV:

- 13-15% ROE , In one interview he mentions 18% ROE in long run.

- 1.5% ROA

- 25% AUM Growth rate for many years.

In the Below sheet one can configure:

- ROE across different periods

- Fund Raising Amount & Valuation.

- Dividend Payout Ratio as % of PAT

- AUM Growth Rate

- Max gearing [In place of CAR]

- Total Funded assets as % of total assets.

Note:

- In the long run raise in EPS & Book value will directly correlate with stock price performace.

- Have used only 10 year projections, once can expand them to more years but, make sure to add some stress periods for every 7years.

- Growth on larger numbers might be less that what it is today so, go slow on the AUM growth in longer tenures.

- Some Banks in Mature markets are making 10-15% ROEs & 1-1.5% ROA’s in long run, so it is a fair assumption to have those factored for now. [These ROEs are driven by Fee income pools rather than only spreads]

- Bank growth depends on Liability gathering ability[Deposits+Borrowings] rather than Assets [Loans] so, one needs to have their own assumptions on how much IDFC First can attract from the market for factoring in the AUM Growth.

IDFCF Value_Manikya.xlsx (20.3 KB)

3 Likes

While I am yet to go through the latest numbers in detail and understand them well, a few things are very apparent from the results and commentary -

COVID will make a dent to most lending businesses and IDFC First Bank won’t be any different. What is more important is that the management continues to stay transparent and the state the ground reality as it is rather than sugarcoat the message.

Branch expansion continues as planned and management is not playing it safe here. Building a high performing branch banking sales team is not easy and takes years, it is very difficult to make operating profit on newly opened branches in urban centers. Getting into the details of the existing customer base, getting the RM’s to build relationship with them and to sweat the customer base through product sales is much easier said than done in today’s competitive urban retail banking landscape. Walk into any HDFC/ICICI Bank branch and witness the 8:30 AM huddle, it is brutal work.

Anyone running a bank will want to build liabilities first before starting to lend to them. If New to Credit accounted for a good chunk of the incremental lending, I would see it as a negative. Ideally you first get the customer on board, get them to park their savings/deposits with you, then explore lending opportunities once you have understood them well. This is pretty much the basic principle of building a retail asset book without taking on too much risk, going out and lending to new customers is easy to do but can backfire spectacularly. VV has seen this cycle play out in ICICI Bank, he’s too smart to make the same mistake twice.

Numbers getting better in banking depends as much on the operating environment as it does on management skill. When NPA’s rise, they rise across the banking system. Managing risk well and laying out a healthy growth path is where management skill becomes important, culture will decide whether the bank becomes a pan India player or remains strong only in a few areas. That is another element which needs to be evaluated carefully. Unless the hiring functions can scale and incentivize people well, it is not easy to become a pan India banking player.

Based on channel checks the bank is at the forefront of the fintech landscape which can be seen both as a positive and a negative. Using fintech engines and new age models to get customers on board is good, but using the new age models (who don’t understand credit/underwriting well enough yet) to start lending aggressively can be a recipe for disaster.

Waiting and watching here over the past few quarters, bank is doing some interesting things for sure. The risk in the business has been cut down by more than half over the past 15-18 months in my assessment.

Disclosure: I have a position here, the only lending business I own as of date

19 Likes

@hcpl2000 - That isn’t the point right? You pledge shares when you take a loan (which Cloverdell did to raise funds to pay the partners in the firm?). So effectively their pledge is dependent on Cloverdell’s ability to repay, nothing to do with the quality of IDFC themselves. If they couldn’t repay, the lender will simply sell those shares in open market or sth. They own 10% stake.

While I agree this is not eminent risk as Cloverdell seems fairly managed and that the such transactions was supposed to be “normal”, it is just very surprising to me there is NO mention of this whatsoever. I am not sure how pledge of shares (even if outside the business) done by a 10% stake holder doesn’t count for a “material” event that requires disclosures.

No cause of worry. Cloverdell ( read Warbug Pincus ) is a major !

Also it was an erstwhile promoter of Capital First…but a NON PROMOTER of IDFC First . So it does not require any disclosure…and no mention is required. All is par for the course…

4 Likes

But why is this unexpected; as CASA rates come down this was bound to happen right? NIM’s in Q4FY21 were already 5.09% (5.24% if adjusted for interest on interest reversal). The management has guided for NIM’s between 5-5.5% as per their 5 year plan; so that target has already been achieved and this is before factoring in the 2-3% of cut in CASA/Deposit rates announced in the las few months. If they continue their existing strategy NIM’s can potentially go up to 6.5%-7% over the next few years. Rather than doing that they are maintaining their existing NIM target and just offering cheaper loans to a more prime customer.

4 Likes

I don’t like the fact that the management seems to be window dressing the results to show stable QoQ and YoY profits. Covid Wave -2 might have a significant impact on asset quality. Exited my holdings today.

This is a rare management (Mr. VV) who believes in complete transparency. Their presentation is over 70 pages. They even give client wise exposure details, if required.

This is a turnaround story. Give them some time. If you look past 2 yrs, results are palpable.

2 Likes

I’m not able to find cost of fund, plz help if you can find.

@sahil_vi

If they start lending at such a low interest rates, NIM will eventually go down, So entire thesis will go wrong.

Is it good idea to improve asset quality by compromising profit margin?

We know VV for his success in Capital first for lending to underbanked at high interest & still keeping asset quality under check.

My entire thesis is based on expansion of NIM going forward ![]()

What are your views ?

Cost of fund is reducing since CASA is raising and saving rates have been slashed to 4-5%.

Lockdowns hurts the under-banked section most. This can be inferred from the fact that most of the under-banked don’t have the ability to work from home. No point extending loans to them if their ability to pay back has taken a hit. Hence, IDFC First is pivoting and targeting more stable high end home loans.

Until the economic effects of wave 2 lockdown resides it would be best advised for the bank to focus on high quality customers.

5 Likes

Correct. I see this as management adjusting to the new reality. Given excess surplus bank has, it is better to lend to prime corp employees at 6.9% rather than keeping funds with RBI. When economic situation improves, I expect bank to pivot again to their strategy of lending to underbanked/self-employed segments for higher yields.

4 Likes

Why not pay up high cost liability instead ?

I agree with this view. In view of the pandemic and its disproportionate effect on the poor segment of the working force, it is prudent to ease the gas pedal for the so called unbanked for a few months till the affected sectors of economy limp back. Extend credit only to those with the ability to pay back. VV will definitely come back to this sector, once the pandemic settles down. This is his area of specialisation and he achieved success in Capital first through this strategy. His main aim of getting hold of a banking licence was to lower his borrowing cost while maintaining the lending rate.

I had invested strongly in Capital First after the merger plan announcement, and again added substantially in March, April 2020 as it was a god send opportunity.

Thorough and threadbare analysis is good and essential for all of us but it should not lead to panic. The basic story of the company remains intact. In fact it is getting better.

2 Likes

In the interview, it seems that IDFC First bank considers write-offs as a line item below provisions, i.e. first they provide money according to ECL norms and subsequently write-off a given amount. This is normal industry practice.

However if we look back in time at capital first’s book, their approach was not the same. Capital first used to write-off and show it in their other expenses item, subsequently NPA numbers looked better but the underlying ROAs were impacted as other expenses as a % of revenues was high (for details, I have attached the series of posts below). I was looking at IDFC First’s other expenses item and it seems this number hasn’t grown so much, so probably there is a change in this strategy. Am I correct in my interpretation? This would signify gross NPAs correctly represent stressed asset pools.

5 Likes

This is in Hindi, in this VV is also talking about Credit loss.

plus also look at his body langauge when he talks about “provisioning policy” ![]()

2 Likes

I think the prime home loan portfolio is being misread.

Due to reduction of Cost of funds, it just opened up another area to lend which was not possible earlier. It is only natural they diversify when they have that opportunity. Especially in the current situation when lending is tough with no cash flows for businesses.

The impact on idfc first of covid second wave will be high considering their liability profile being retail. just look at recent RBI measures. Most of it is targeted towards retail loans. That speaks of how asset quality will be in the coming months for banks in general. Idfc is not an exception.

They just have to wade through this wave. In terms of coming out from 1st wave, they did hold well, especially the restructured loan data (pg 10 of 91) and also 1.5% increase in npa due to covid (considering their target segment)

It’s definitely an unknown territory for every lender for this quarter. But well capitalized banks should get through these tough times.

8 Likes