Having written my views yesterday after the analysis of q4 numbers and the press release note’s tone, I would want to add a few points after watching VV’s media interactions:

I have never in the last 2 years hear him sound so cautious about the outlook(though it may be just near tearm/short term). On a particular question about asset quality, he classified retail into two buckets- Prime bucket(Home loans, LAP and Business loans) where he said GNPAs may rise 100-150 bps if Covid 2.0 persists and other bucket, which is a matter of concern was unsecured perosonal credit, consumer durables, rural where in stress may be much more.

Honestly,no one knows how long Covid 2.0 will last and will India have Covid 3.0. These uncertainties do add an element of risk on credit quality.

If you read the last 2 annual reports, they have always talked about how fantastic a ‘capital first’ lending model with cost of funds of a bank can be in terms of growth, perpetuity and resilience(he always talks about how the loan book sailed through disruptions like demonetisation, gst, rera etc and we have to give it to him on all those fronts). Even before raising funds via QIP he explicitly mentioned funding for toilets, cattle and the unbanked in general. Now suddenly after Covid 2.0 and the recent fund raise, the focus seems to have moved to safer assets with lower yields and better quality. I would want this shift in stance to be temporary rather than structural because I do genuinely believe that IDFC has unique capabilites there.

3.If this shift in stance is more structural and longer term then we would have to go back to our models and revise our NIMs estimates lower.

So if you see VV’s media interactions in the last 6-8 months, he had always maintained that he could offer 6-7% on SA accounts because they were lending upwards to 15-16% and that they have very unique capabilities(moat) of giving millions of loans with ticket sizes of Rs 10000 or lower. This unique capability made the bank a leader in its segment.

Now suddenly because of Covid shocks ,VV wants to compete with the HDFCs and Kotaks of the world in the prime retail market by reducing rates. My forecast is:

1.It will be not be easy to compete with the top tier banks in their game of the prime retail market.

2. Sudden reduction in CASA from 7% in Jan to 4% in May can lead to some good chunk moving out.

3. Reduction in Savings rates and change in stance of lending to prime retail may be more temporary in nature and the extra NIMS earned this year could be used for Covid 2.0 provisions.

I would want that once Covid is gone, IDFC sticks to its earlier proposition of a unique high yield algorithmic lending capability along with low cost of funds rather than compete with the top tier banks who have a much more lower C/I, larger branch networks and deeper entrenched relationships with customers.

The bank has always said that while they have focus areas, they will diversify and be a broad based bank. Hence the still substantial corporate book which they intend to keep, while focusing on retail. Similarly within retail, it makes sense to diversify the book into quality as well, particularly as the size grows.

The only difference seems to be that currently they are focusing on the quality bucket alone rather than quality as well as high yield. I’m quite happy with the scenario because it does look like there will be significant retail stress over the next 2 quarters. Plenty of time to focus on the yield when this black swan event passes. An all guns blazing approach in retail right now would be irresponsible, imo.

NIM is already at industry highs, the income from expansion has only been deferred. Meanwhile, the bank is ensuring that the income grows from the size of the book, while maintaining top class margins and asset quality.

The concerns with the bank are with the industry and the economy as a whole. Of course covid has an economic cost as well, but nothing has changed for the bank, aside from the strong progress in the transformation.

Strategy is to get into “prime segments of all businesses including the prime home loans” - ppt slide 35

Bank already has acquired customer depositing money large amount into saving accounts to get higher interest rates. Bank would want to target these customers for additional products such as credit cards. Customer acquisition is very expensive and valuable.

Indian regulatory changes making switching providers easier and seamless with changes such as number portability, standardized insurance policies, external linked lending rates etc.

Given this backdrop, prime home loan is a great way to make prime customer sticky with a bank for 10-15 years. IDFCFB non-interest income has been smaller compared to more established banks. Prime customers can be sold additional products such as car loan, personal loan, credit cards, MF, insurance, forex etc. Bank has already has tie-up with CRED since they have acquired prime customers via a loss making business. CRED valuation might be irrational but it also indicates attractive and validation of this line of business.

Since home loans at floating 6.9% could be a teaser but it can move higher in inflationary environment. Credit demand in subdued in India for last few years. With every bank/NBFC going after retail customers there is competitive pressure for high yield lending as well.

I am sure there are software package providers and consultants offering solutions for algorithmic underwriting using cashflow/non-conventional analysis. This capability might not be a differentiator in medium to longer term.

There is one more point of concern which I have.

Management had given a target NIM of 5.5% 2 years back. Till last quarter, management used to include net interest income from loans via banking correspondents after deducting servicing fee. When they declared this quarter numbers, they included gross interest income and subtracted the BC fees at an opex level. So NIMs obviously got bumped up.

The annual cost of BC comes to around 480-500 Crs. If you subtract it from the NII, the NIM(as per old calculations when guidance was given) works out to 4.68%.

Hopefully, VV clarifies about this that new NIM guidance would 0.5% higher because of the change in accounting.

P.S: IDFC First Bank still remains my largest portfolio holding(very high concentration, upwards of 40%). Booked some profits at 65 levels. Believe that if someone has to invest in the listed banks it has to be IDFC or Kotak.

In general, the IDFC management team is on track building a good & reliable bank. But I don’t think right now the bank (the stock price is Rs 56) is trading discount price based on Q4 result, management’s outlook and COVID situation in India.

Regardless of whether one is extremely bullish on the bank or very worried about their future it would help all investors, and potential investors to understand the bank better if they did conference calls.

I started the Twitter hashtag #WhenIDFCFBankConCalls with the goal of reaching out to the bank and enabling them to hear out their investors.

Please consider tweeting at the the bank with this hashtag and letting them know that as investors we would love for them to start doing concalls. It’s an almost 4.5B$ company now and imo it is high time that they start doing conference calls and answering some investor questions.

Very interesting interview and some key incremental insights i could not find in such a straightforward way in other Q4 interviews:

(Covid Wave 2): Expects April and May to be affected, but after two or three months, things will come back. 2nd wave is giving mixed signals. On one hand, it looks like a hard one to deal with. On the other hand, it is not a national lockdown. Sectors such as manufacturing and exports are still moving.

(Savings rate @ 5%): Customers want safety, plus our savings rates are still very competitive. Plus we have a great brand, institutional feel and customer service, so we think our deposits will continue to grow.

(Incremental asset side): Earlier, our growth came from SME and consumer financing. Now, our incremental growth is coming from home loans. Last year, our home loans grew by 37% and asset quality is great. (Sahil’s note: I have also highlighted this shift in loan book composition in many earlier posts. This has been a secular trend, not a one off. But it has been accelerated due to covid IMO).

(Why the move away from unsecured lending?): Unsecured lending will also continue to grow, but we will carefully watch the economic environment for that. Want to participate in secured financing where peace of mind is high because asset quality is good. Also, home loan is a long journey with a customer. (Sahil’s notes: interpreting last part as large opportunities for cross-selling of other financial products like credit cards, insurance, mf, other loans to prime customers).

(Guidance on asset quality): Pre-covid we were at 2.6% GNPA. Given current underwriting standards & trends, we are heading towards gross of 2%, net NPA of 1% and provisions of 2% on a sustainable basis. We are modelling our risk parameters for this and can meet this guidance, post the Covid second wave provisioning. (Sahil’s note: the 2% provisioning is including for NPAs as well as rest of the loan book).

Overall thoughts: It looks like bank is doing some serious thinking about the composition of their loan book. Now that they have a brand and have managed to capture customer headspace, they are utilizing the stickiness of CASA (some would argue it is not, I would argue it is to some extent. When they reduced SA rate, i simply created FDs out of my SA, did not run to open new bank account) to guide them through slightly lower CASA growth at the cost of being able to lend to much more prime segments of the market at lower rates but more importantly much better credit quality. Home loans are indeed an interesting gateway product since they are sticky, large duration, large sized, and thus provide a gateway for bank to cross sell multiple other products to these customers over decades. The fact that bank wants to be cognizant of economic environment and not mindlessly keep giving out unsecured loans also shows thoughtfulness on the part of the bank. They are not shying away from unsecured loans, only being conservative. In banking business a conservative banker is a good banker. I would rather go with a banker who wants to calibrate and deliberate before giving unsecured loans. Bank has also raised lending standards (higher LTV, higher credit score, higher minimum balance requirements, lower loans to first time creditors) since covid hit, all of which points to thoughtful lending. The interview has served to increase my confidence in the investment thesis. At the same time, following remain key monitorables which can break the investment thesis for me:

Asset quality and credit costs of 2% GNPA and 2% provisions are reasonable. Let us see if bank can meet these medium term post covid.

As asset side grows, the operating costs should grow much slower and get amortized over a larger base. This should lead to reduction in Cost to income ratio and thus profitability for the “retail” segment under which header all the opex for branch opening goes.

the CA part of CASA is still quite low (10%) compared to peers (40-50%) as i had shown in previous posts. This is an important source of 0% funds for the bank and If i could ask just 1 question to the bank: it would be their strategy for growing the CA of CASA.

Disc: largest position in PF and so I am heavily biased. This or any of my posts are not investment advice.

IDFC has announced a prime lending rate of 6.9% but that’s just the headline rate and only very few customers will qualify for that; the average rate of the book will be much higher. So for example, HDFC’s prime lending rate is 6.75% but the individual loan book yield is far higher.

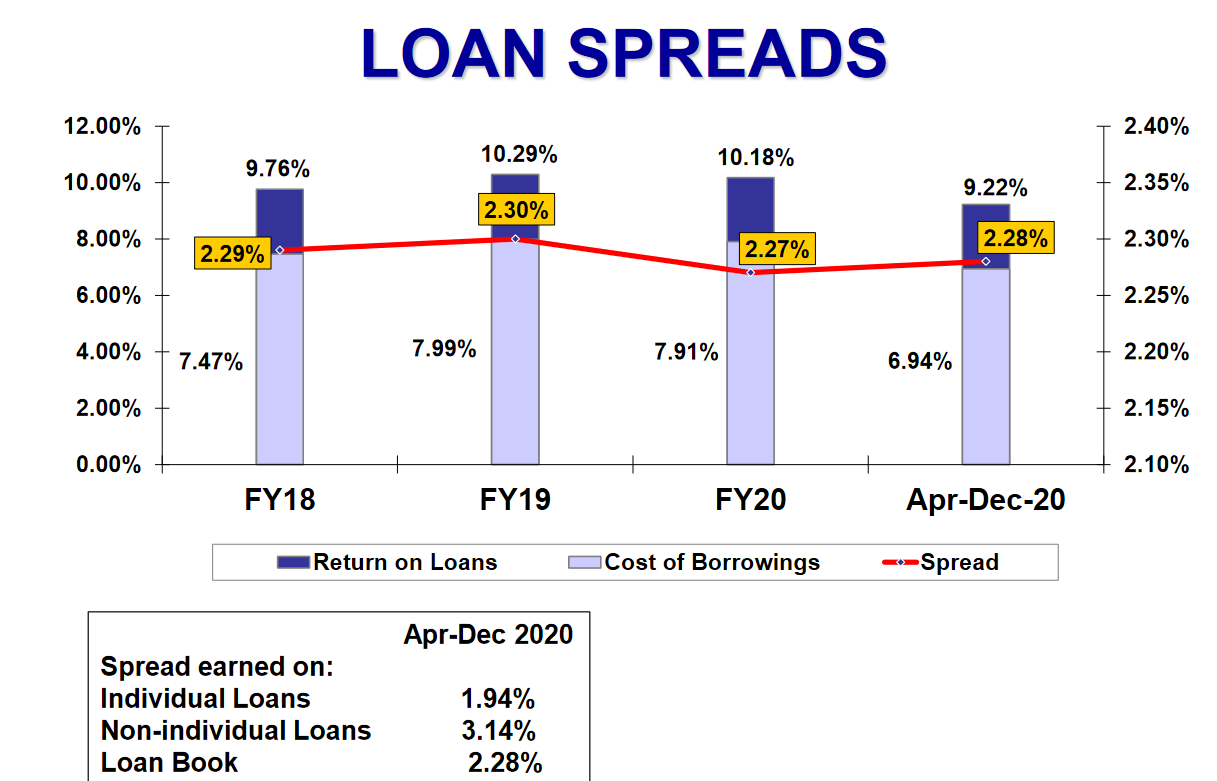

Their loan spreads for individual loans is around 2%; which means their average yield is around 9% for the entire book with a CoF of around 7%. With an incremental CoF between 4-5% IDFCB can get a NIM of around 4-4.5% easily even by targeting the same HDFC customer.

Also of note is the difference in the cost of funds between HDFC and IDFC going forward; IDFC might be at par with other banks but now has a huge advantage over NBFC’s like HDFC/Bajaj. The home loan market is massive and banks are going to capture the best customers from NBFC’s with their CoF advantage.

To put things into context, SBI’s aggregate cost of funds are ~4.4%. It currently not possible for IDFC First bank (which is offering higher interest rates on savings account) to lower its cost of funds to SBI’s level. IDFC First’s incremental COF from NHB was 5.5%, they can raise CP money at low rates but that cannot be used to build a housing finance book. No financial institution in India can make NIMs of 4%+ by lending to the prime segment (with gross yields of 8-8.5%).

There are two ways companies make money in housing finance:

Increasing gross yields by doing higher LAP, project finance and control credit costs (this is a graveyard for a number of HFCs)

Decreasing cost to income and do prime lending. HDFC, with its cost to income at 8% (lowest in India), has been successful in executing this. Canfin is another who have managed to lower C/I to 12% levels. Every other company operates at 18-20% levels.

If you read my post I am talking about IDFC competing with NBFC’s like HDFC/Bajaj and not SBI. HDFC has a 20% market share in housing loans and even someone like Bajaj has a 40,000cr odd housing book of which a large % is mortgages. There is a big enough pie for all the banks with low CoF.

Our discussion above was limited to NIM’s as it was about what sort of NIM’s IDFC could potentially make.

If your incremental CoF is 4-5% and you are lending at 8-9%, then your incremental NIM’s are 4-5%.Most of HDFC’s higher yielding loans are classified under non individual loans where the yields are higher.

This is not an apples to apples comparison. If you are looking at incremental cost of funds for IDFC, you should also be looking at incremental cost of funds for HDFC Ltd. When i checked a few months back their NCDs were trading at 5-5.3% and FDs are also yielding similar. So I think incremental COFs for both are similar, plud IDFC has a much higher C/I compared to HDFC; which means impossible for it to lend to a prime borrower profitably. However, if the bank is able to cross-sell that same customer multiple products, it might make sense. Uday Kotak in his Q4 concall also mentioned that they are looking at home loans strategically; since it is an important touchpoint to acquire the customer relationship.

I have been emailing the bank for past 5 months, requesting them to hold conference calls.

Had also tried this.

Finally, something seems to be happening. The bank recently replied to me with the following:

In the spirit of collaborative investing, I seek suggestions from the members of this forum. Please take some time, and request you to come up with suggestions on what questions to ask the bank in response to their email. I will of course also utilize this time and come up with my own set of questions. I cannot guarantee that every question posted on this forum will make it to the list of final questions but would try to incorporate all concerns/questions/angles after ensuring deduplication, up-leveling and ensuring that we are able to focus more on the strategic direction of the bank.

PS1: Request everyone to read all previous questions to make deduplication work easier for me. It is not worth our time to post the same question repeatedly.

PS2: I would be quite disappointed if no one ends up posting questions.

Split up of the cost to income ratio. Its close to 80% now, would help to understand how much of that is because of new branches. How is the ratio for like new branches vs old branches. How long do they foresee a high cost to income ratio and has the assumption changed because of covid ?

Would help to include write offs, write backs to the presentation maybe ?

Estimate on any upcoming restructuring ?

Why has the narrative suddenly changed from unsecured lending to prime housing loans. Also how do we plan to compete with banks having lower cost of funds ?

Breakup of NPA’s by different segments ?

Why the change to include origination fee to NIM’s from this quarter ?

Are they going to revise any of the previously mentioned 5 year targets if so which ones and why ?

Newbie here, feel free to ignore any of the questions if you find them irrelevant

I think Vaidyanation answered the first question he said they got low cost borrowings from NHB at 5.5% so they took it and it shows up as borrowing on the BS so nothing to worry about i guess

Thanks, I saw that too. Question is whether there’s a change in strategy on liabilities too, given reduction in savings interest rates, etc. Bank’s Credit/Deposit ratio continues to be quite high compared to peers. If market borrowings continue, C-D ratio will continue to remain elevated.