I was going through Annual report 2017 of Capital first and found out an interesting piece. I have compared the RoE for both-Capital First and Bajaj Finance and underlying reasons for that.

And, I have some serious concerns with Capital First.

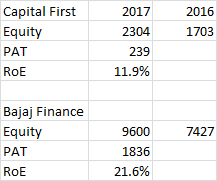

RoE computation-

Two reasons for high RoE can be high yields or high capital gearing. Then, I computed these figures for both the companies for 2017-

But, for both the points, Capital first fairs equally with Bajaj Finance. So, the problem of low RoE is not related to these two points. Then, there must be some problem with the cost structure. Either, Capital First cost of borrowing is very high or there are very high provisions/write-offs.

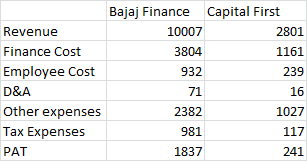

I went to the consolidated 2017 financials and they are as below-

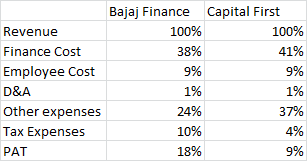

Re-basing everything to revenue-

This was shocking to me as why other expenses difference is 13%. Digging deep, it came down to two factors.

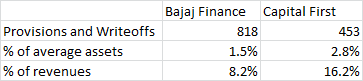

1- First factor is the provisions and write-offs

Capital First has written off approx 403 crore of assets and that is approx 2.5% of their average assets. This is inspite of them claiming that they have very stable asset quality. I think they write-off the loans to under-report NPA’s. This is one very serious observation I have found.

Again, They have Amortised loan origination cost that is approx 237cr and is 8.5% of the revenue. I have no clue what it is about. Can anyone help me with that?

I don’t think RoE will improve much if this condition persists where they have to write off such amount of loans.

I am new to valuepickr and looking for comments and feedback.