Have compiled some numbers for Capf:

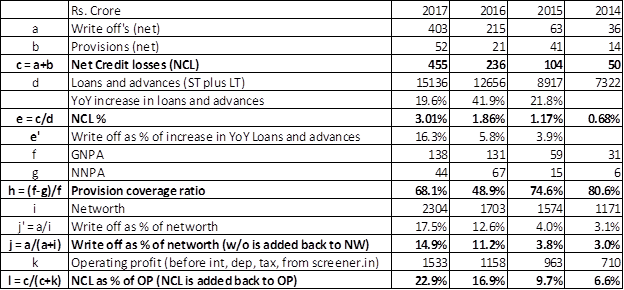

While the mathematics of the formulae are not exact, my focus was on the trend of NCL, PCR and writeoff %, which are all indicating downward trends.

Frankly, the NCL is not shockingly bad in absolute sense (3% NCL as % of loans and 23% as % of OP before NCL, is fine, for the segment the company caters to), particularly when the company is growing at 40% plus. Just in case growth slows down (say, if high base effect kicks in), then the percentages will start looking increasingly worse. However if Bajaj Fin is growing at 40% inspite of being 3-4x the size, my guess is that growth for Capital first may not slow down given the runway.

Coming to the write-off’s in 2017, unless there is some element of one-off in FY17 (maybe due to demonetisation perhaps?), and if the purge has been done in 2017, then the trend may reverse going forward.

Above table gives NCL relative to the increase in loans and advances for 4 half-year periods. Imagine a tap running from top, and a hole in the bucket. The increase in loans is water being added to the bucket. the NCL is the leakage in the bucket. Higher the leakage, faster the tap has to run so that the bucket continues to remain full.

Loan growth in HY-Sep16 was just 6% which inflates the NCL to 26.4% (not sure why the loan growth was so low). During demonetisation, the NCLs have increased during Q3 and Q4. It is possible that the management has actually been prudent and taken some accelerated write-off’s? And if indeed the management has been conservative, there could be write-backs as well. However at this juncture, this is just my conjecture.

In this period the loan book grew 12.8%. In FY16 and earlier, the figures were not so bad.

In my view, if one trusts the management, one can hold on and see how the numbers pan out over the next 2 Qs, which could indicate if FY17 was one off. Just that one needs to keep in mind that the stock is currently quoting at 3.5x book (excluding 340cr of capital raised recently; including which pb is about 3x) and 30x trailing pe, and whether there is adequate margin of safety to absorb further shocks.

Discl invested from slightly lower levels. Sold a little today to lighten the holding. Will keep reviewing.