Cred has launched a new product which offers each cred user (for now this might be restricted) access to instant credit line with flexible terms for drawing the loan (withdraw as much as you want) and flexible emi options. The interest rate applicable for me was 17%. The credit limit was around 3,75,000 rupees. As one can expect, the reason I am posting this on this thread is that idfc first bank is the banking partner.

I think this is a brilliant move because specially for ui/ux cred is 1000x better than any banking website and app. This would also give idfc first bank access to a very select high credit quality client base leading to low credit costs. All analysis can be front loaded. The bank is truly a leader when it comes to partnering for fintech innovation.

What does everyone over here think of the valuation of IDFC First w.r.t peers? I see that peers are averaging at around 5 times book value but IDFC is currently trading at around 2.3x. I think the market has not factored in the trajectory of what IDFC-F and VV are trying to achieve. I think in spite of the run up from 18 rupees in Mar 20 lows to current 58 rupees or so, I still it’s still reasonably valued.

I have taken my 1st chunk of position at average cost of 58… And I want to add much more to make it my largest holding. Based on some of own study and going through the thread here, I am getting more convinced by the day. @sahil_vi 's post from 3-4 weeks ago is a solid insight. I’m going to now read the QIP document as well

Morning context has reported in March-2021 that they have disbursed 1000cr in past 5-6 months.

They are charging 1.5% on processing fee & no penalty on prepayment.

They have disclosed last year that credit lines are being extended upto 5lak rs.

One risk is that, this credit line might be used by many to pay off their credit card rollover debt. I.e.a bit high risk customer but, the spreads are decent.

Cred allows people with high CIBIL scores only. These are educated, money savvy people.

Why would such clients pay 17% for a personal loan when same can be got for 10-12% via banks?

TBH, it’s alarming, surprising to see how many people use credit card as a debt instrument. Very few people actually use credit card for their benefit.

One thing credit cards may offer (not just IDFC’s) or even Cred’s offering is that they don’t have EMI payments. One can let the interest run for sometime until it is repaid (only dread the thought of such compounding on the expense sdie). PLs need EMI. I know it doesn’t make sense for us investors here but looking at how HUGE credit card liabilities are in the world and the exorbitant interest earned by banks on them, people still chase it.

This could be one reason, just thinking out loud. Anyone else got anything better?

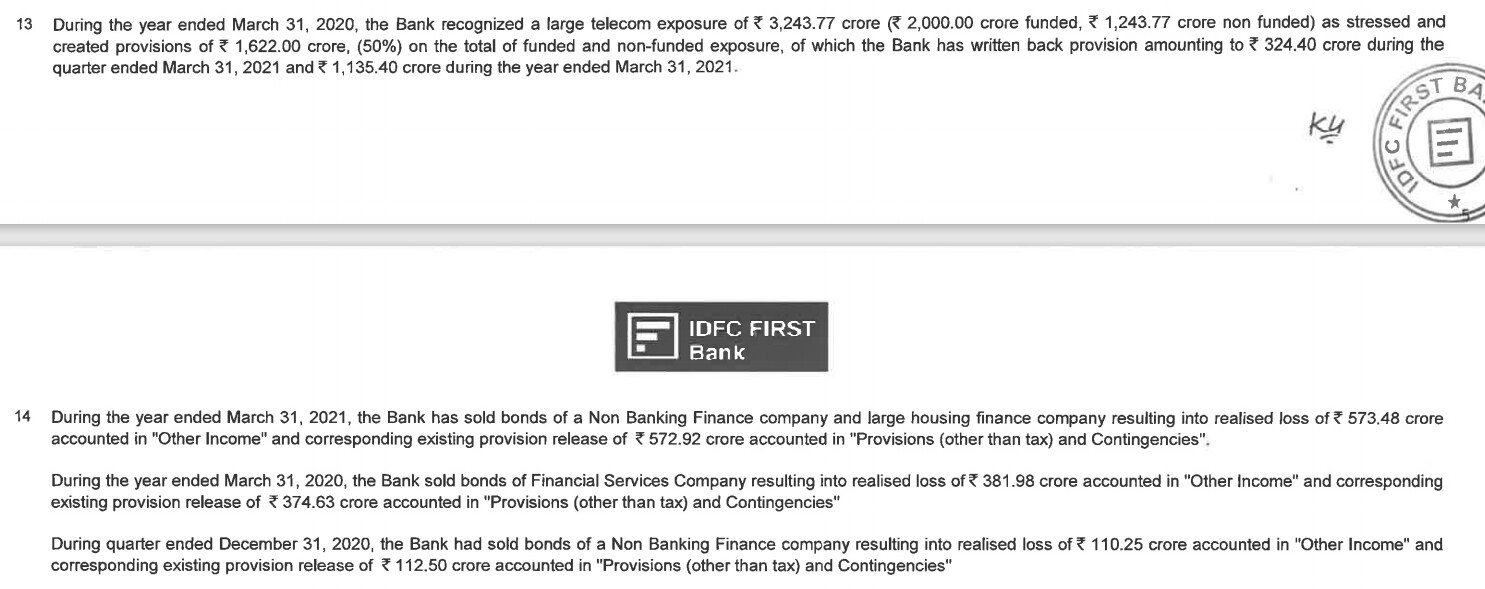

@gurjota your point makes sense in general. But, when we get into detail credcash adds very unique value for some customers.

1.Preclosure charges:

Every PL comes with a foreclosure charges- which ranges from 4%- 6%. For credcash this is 0.

Fund utilisation period:

Most banks will not allow the pre closure within 1 year. - when you look at this in EMI perspective, it doesn’t make sense to foreclose after 1 year since major chunk paid in year 1 consists of interest & arbitrage between closure charges & incremental EMI interest is not much.

For credcash you can prepay anytime and reset your credit limit.

First time borrowers:

Usually salaried new to credit folks will not have pre-approved offers since they won’t have any running loans.

credcash- will be the only source for them to take a quick credit line.

I too have a pre approved offer from ICICI at 10.5% yet, I had to use credcash@15.5% for a short term need due to above reasons.

Maybe 1000cr disbursement in 5-6 months validates the market requirment for such product.

Totally agree. These loans are more in lines of an Overdraft facility for individuals. Use as you go. This is one of the hottest selling product for Bajaj Finance and Cred has simply adopted it and will use their wide distribution. And this is despite the fact that the facility has higher interest rate than Personal Loan. Personal Loans are extremely rigid in their structure related to tenure, prepayment, monthly payments etc. I also had the choice of going for a Personal Loan but I preferred the OD by Bajaj Finance.

Although one caveat for IDFC First Bank - Currently they are the partners with CRED but CRED may already have moved or is in active talks with other larger banks as their banking partners.

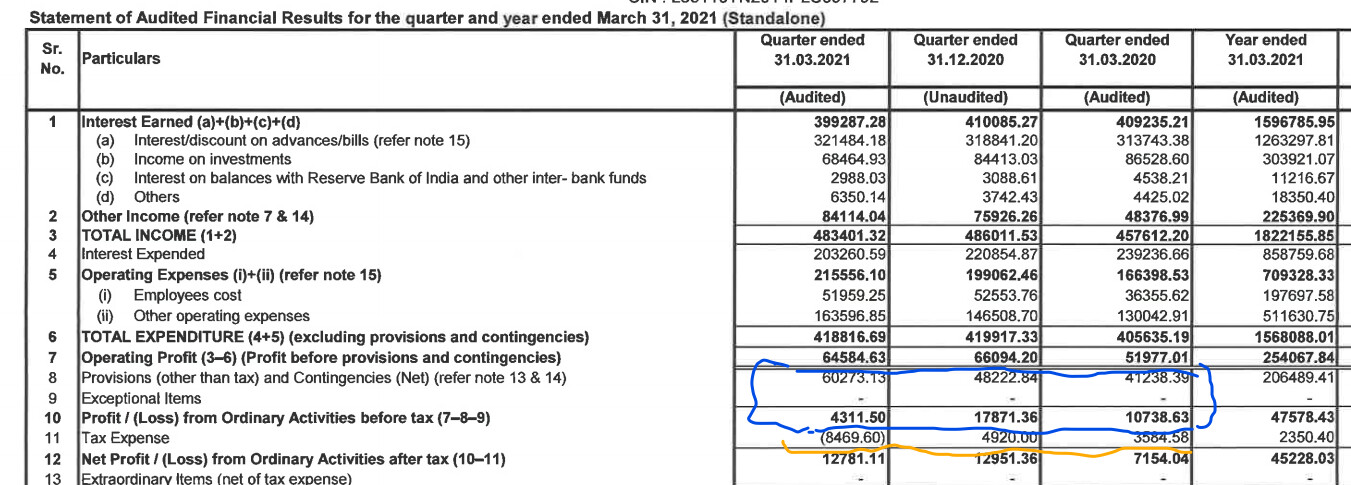

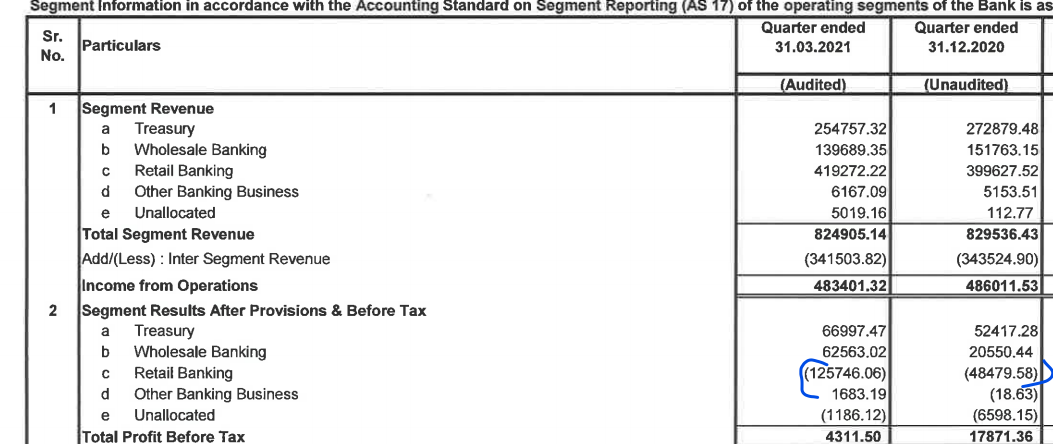

Provisions has increased from 482 crores to 602 crores, close to 22% (highlighted in blue) … i believe these are fresh provisions due to retail loans which is what worries me,

The other provisions that they had made earlier are being removed and in couple of cases added back to “Other income” as mentioned in point #14 , wondering how could they do that ,someone please help me

They have written back-removed provisions for the Idea loan

They have removed provisions for DHFL and added to other income

Just a wild guess, They are reducing the tax on the profit by showing provisions on which they don’t have to pay taxes, atleast for now…

2,they are cleaning their books big time, results after 1 or 2 quarters should be bumper

But the impact of provisions is not felt bcos they are writing back the tax paid which is 84 crores… hence the net profit is brought back to the q3 levels

Hmm smarty pants?? not soo… looks like they have incurred losses on the retail loan front too and now they are caught pants down

IDFC FB was known for erratic results in the past. Even VV told in a TV interview, quote “Jo hai who bol diya”.

But for last few quarters, we see efforts to match the numbers.

Am thinking how to take this, is management loosing it’s innocence or getting shrewd ?

In general banks have a secular growth story in a country like India. Key monitorables for investors are the soft aspects of the bank. For example, if we carefully observe IDFCF bank, the risk on balance sheet has been completely transformed and reduced in last few years. Earlier MSME and MFI were huge part of the balance sheet. Now, mortgage and consumer loans are a much larger part.

See this part of this post.

In addition everything they have said this quarter wrt how they have increased lending standards, more loans to 700+ credit score, less loans to first time lendees,

cred tie up (see post quoted below), are all steps towards reducing the risks.

One has to understand the transformation of the balance sheet to see where the puck is moving. NPA numbers trend has to be understood. Not just this Q and next Q.

I have been tracking and been invested for more than a year. Conviction and research was also there for more than a year. Since Dec-19. My only regret is I should have loaded up more in Mar-20. Did that too, for many months my average buying price was 23-25 rupees. But second round of large loading up I could only do in 50s. Should have loaded up lot more in 30s. So if there are many gap downs and stock price tumbles next week because GNPA did not improve as much as investors were expecting this Q, that would be a buying opportunity for a long term investor for me.

Coming to Rafi’s questions:

I don’t understand how provisioning can worry anyone. Banks got covid shock which only revealed itself in 1 Q due to moratorium. Provisions have to be created slowly, over time. More provisioning is good. It reduces the NNPA number and cleans up the balance sheet. The gap between 4% and 2% is the provision. The 2% NNPA will move to 1% as they provision more and more every quarter.

Banks have very broad leeway when it comes to the P&L statement. The Bank P&L statements are quite useless IMO. Profits are only an accounting item. How bank treats standard assets is up to the understanding of the bank. When they took 50% provision proactively for VI, did investors cry about it? They did. Now that VI looks much more set to not go under, is still a current account and hopefully their bonds are trading at a higher market value (haven’t verified this), bank is reducing that provision slowly (and also adding larger covid provisions). I see absolutely nothing wrong with that. In fact all the VI provisions have been repurposed for covid provisions which is very healthy IMO.

This has always been the case. I have explained in detail in the SIP document post what is happening in the retail segment.

Please read this part carefully.

In summary, I think if someone were to ask me top 3 most important things to track in a bank, they would be:

management

management

management

Numbers are only a way to judge whether management is walking the talk and hence secondary in the case of banks. If someone were to put a gun to my head and force me to track numbers, I would track the NPAs, the NIMs and the Cost to Income Ratio. The trends in all 3 are positive IMO and hence this remains an investment for me.

Disc: largest position in PF and so I am heavily biased. This or any of my posts are not investment advice.

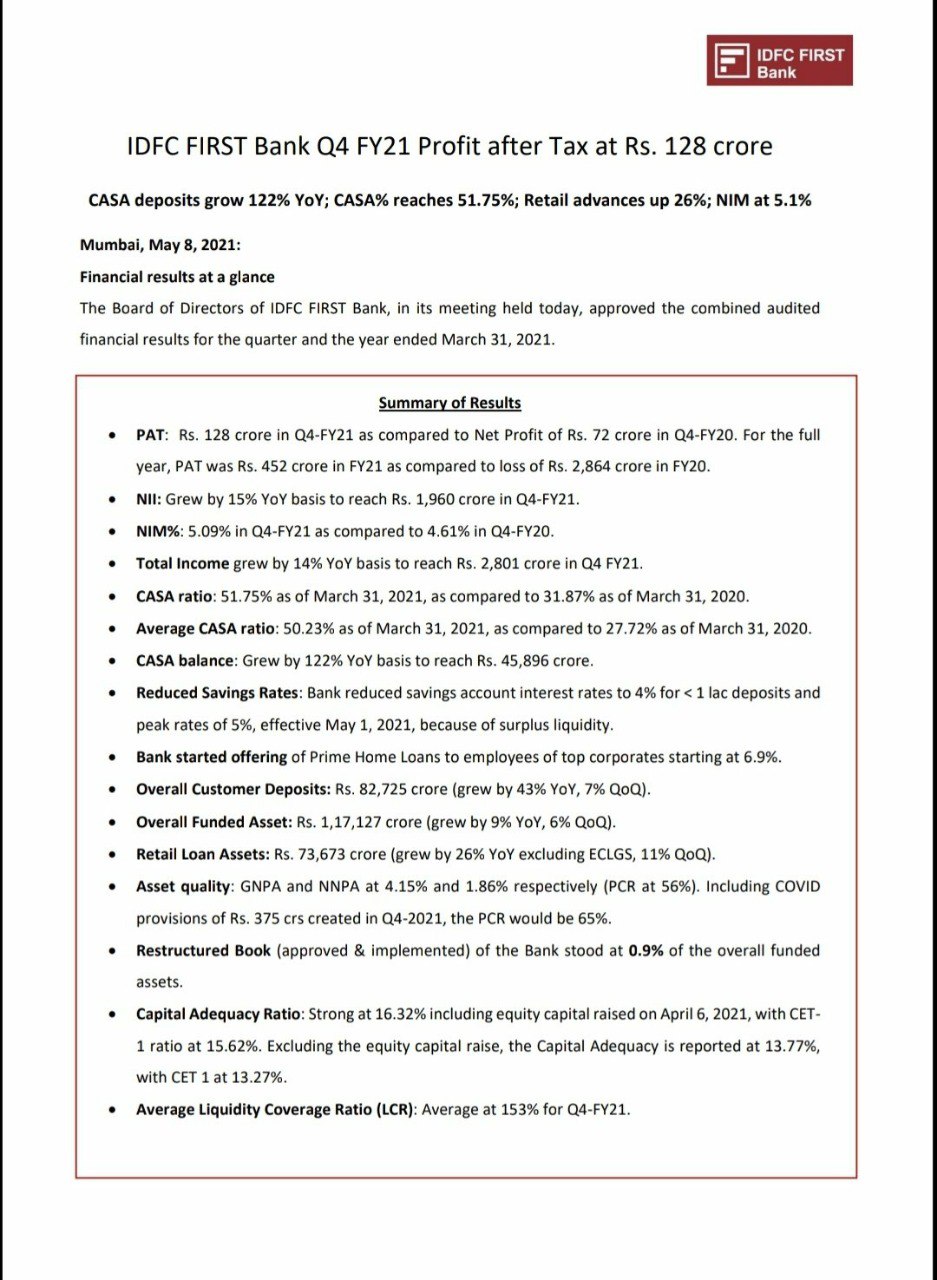

Last Quarter (December 2020) they mentioned 2165 crores as Additional COVID-19 Provisioning and this quarter they mentioned 375 Crores as Additional COVID-19 Provisioning.

Does That mean they are carrying 2540 crores as COVID-19 provisioning?

If not then what happened to the 2165 they provided in earlier quarters??

As per December Reporting ----- “During the quarter and nine months ended December 31, 2020, the Bank has made an additional COVID-19 related provision amounting to t 390 crores and t 2165 crore respectively. The COVID-19 related

provisions held by the Bank are in excess of the prescribed RBI norms”

While I continue to understand IDFC First better through reading and research (including reading on this forum / channel), I came across that Cloverdell Investments had pledged their entire stake in Q3/Q4 2019 to raise money for their PE Fund. They own 9.99% of the stock in the company. However, I find no mention of this anywhere in the annual report of IDFC First etc. Was this pledge released or what?

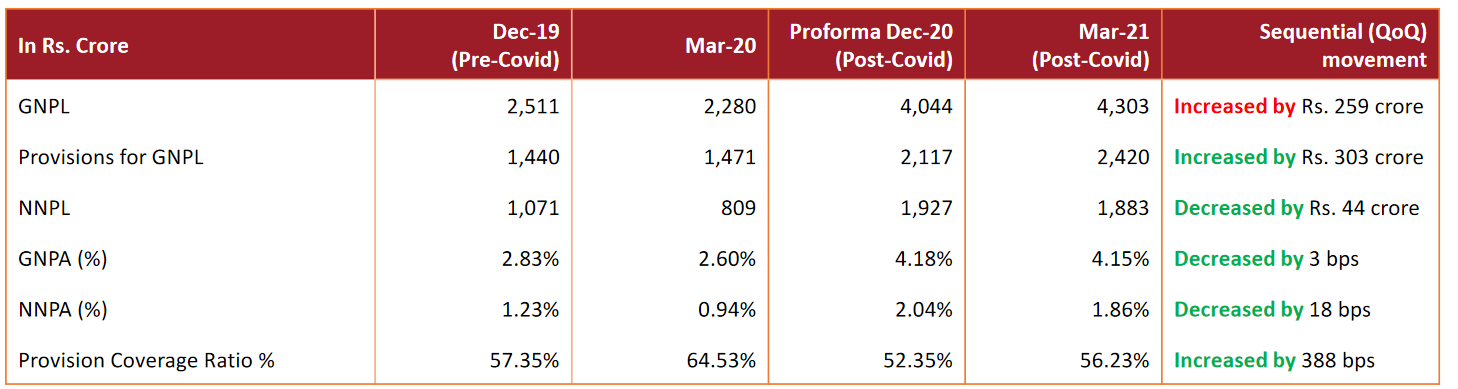

The additional provisioning was included in the Proforma NNPA figure.

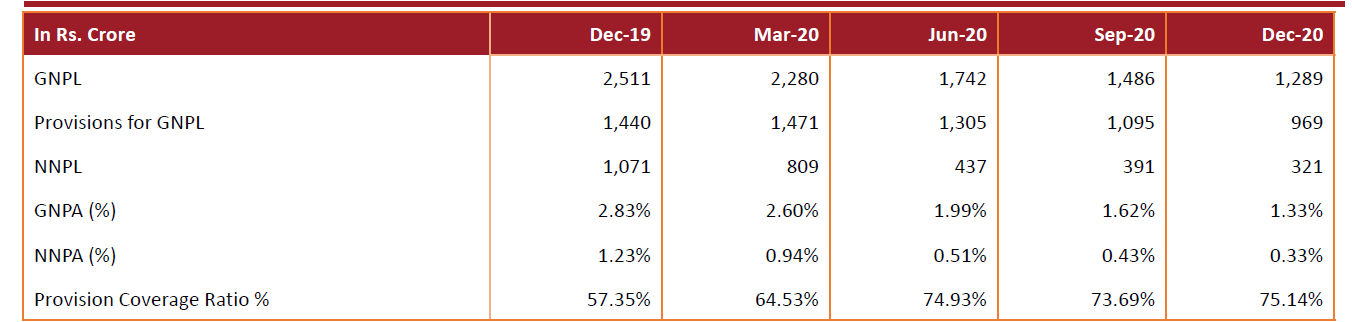

So in Dec, 2020 GNPA was 1.33% and NNPA was 0.33% while Proforma GNPA was 4.18% and NNPA was 2.04%. So the Covid related provisioning is captured in the Proforma NNPA figures. Its a bit confusing but see below:

The provisions for GNPL were 969cr in Dec 2020 and these went upto 2420cr in March 2021; this is where the aditional Covid provisioning has been utilized (same as other banks), the difference between this utilized amount (2420-969) and the 2165cr are probably due to writeoffs as the bank was unable to do any writeoffs till March 2021 due to the Supreme Court order.

Going forward into FY22 the bank is now carrrying Rs 375cr as additional provisions which can be used for any additional stress from the second wave.

IDFC First bank’s USP was to provide high-yielding loans to underbanked customers and at the same time keeping the NPAs under check but this step will have an effect on the yields of the bank (no doubt it will reduce the risk) and will put it in direct competition with HDFC and other big private banks.

Also, COVID had an impact on these high-yielding loans as also seen in the case of Bandhan bank, and with the second wave of COVID pain can last for few more quarters. Every quarter it seems that provisioning is behind and there will be no further significant bad loans but every time it gets extended, this time for retail loans which is the core business of the bank.

Results are a bit disappointing no doubt. It will take some time before the impact of second-wave settles down and operating leverage kicks in, at least for 2-3 more quarters in my opinion.

(Disc: 13% holding of my portfolio)

I feel the management wants to grow the retail book per their guidance, irrespective of the current covid situation. And that means that they will continue to grow branches to total 800-900 by 2024-25 per their stated strategy and continue to source loans through DSAs and that means elevated Op Expenses for at least 24 months. The Cost-to-Income ratio actually deteriorated this quarter from already elevated levels to above 80%. The bank is in investment phase, but it might have been prudent for management to slow down on the investment, get CI and profitability under control and then grow.

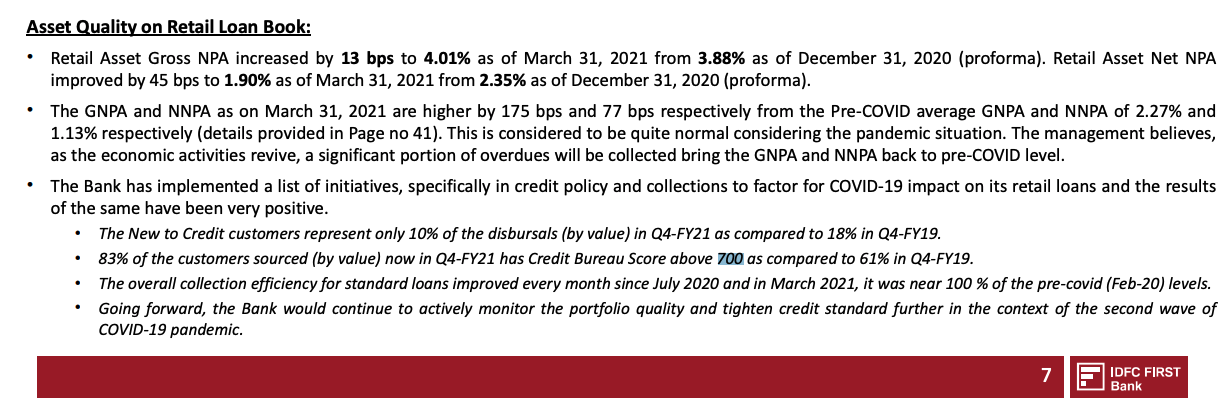

Also one last point is that the Net NPA is the figure that’s most important as that is the post provisioning NPA. In Dec 2019 (pre covid) the NNPA figure was 1.23% which has gone upto 1.86% in March 2021. This is a rise of roughly 60bps after what has probably the toughest year the Company will ever face. If one adjusts the 375cr of carry forward provisioning then the NNPA is actually closer to 1.55% which is a rise of just 30bps. So barring any huge surprises from the second wave the bank is actually quite decently positioned going into FY22. Also of particular note is that the restructured book actually stayed below 1% despite the December guidance of it going upto 2%.

So basically they have used up all the provisioning they did in last 3 quarters and also used Voda-Idea provisioning they made earlier. Ex of that they might have posted a loss this year too.

Please see the results release, roughly 500cr of the Vodafone provisions remain. Secondly if Vodafone’s financial position has improved then it makes perfect sense to reduce the provisioning. Infact I fully expect them to write back the remaining 500cr or use it for Covid as the Vodafone bonds that they own don’t have a very long duration and are likely to be paid back in full.