Glad that this discussion is getting momentum and everyone is diving really deep to understand blind spots.

@sammy11 - Vinay - Much appreciate your detailed work on adding right perspective to the provision/write-off points.

@Karan - Just awesome for someone who is new to VP. Good work dear.!!!

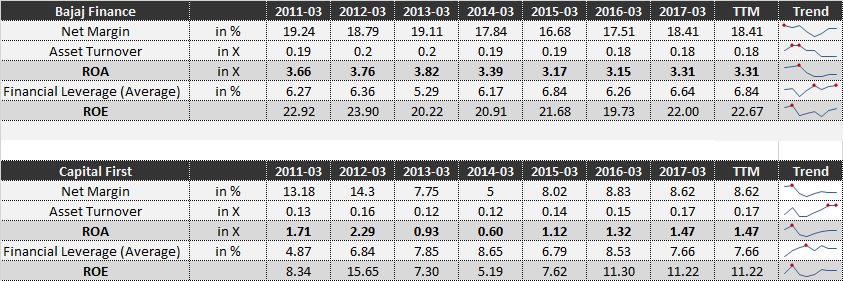

In the initial post I stopped at ROA calc and did not shared the ROE working since for lending entity ROA is considered to be better metric. Here is the upended working summary:

Basis my previous post and again with your data points, by now we agree that the Net Margin % is culprit here for both ROA and ROE numbers. Further agree that ‘other expenses’ differs significantly ~13% between the two and that’s the edge for one over other. However, I would prefer to do little bit of digging before ascribing that this 13% difference is primarily driven by the write-off/provisioning.

.[quote=“Karan, post:135, topic:239”]

This was shocking to me as why other expenses difference is 13%. Digging deep, it came down to two factors.

1- First factor is the provisions and write-offs

[/quote]

To do justice to this counterpoint, I am trying to use data points extensively from AR2017 for both Capital First and Bajaj Fin. Please bear me if its appears to be number heavy:

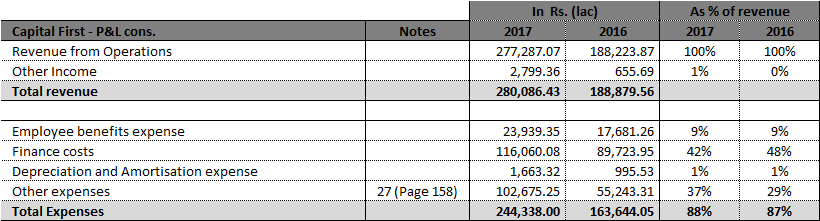

- Capital First consolidated P&L (page 133, AR 2017):

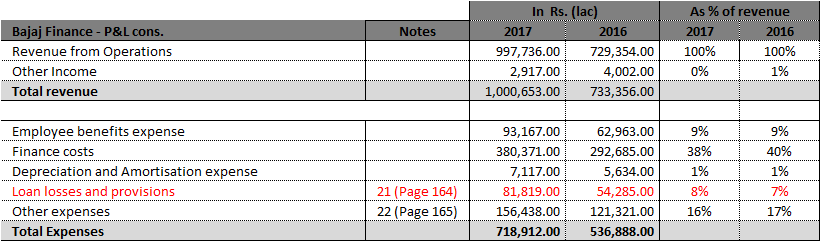

- Bajaj Finance Consolidated P&L (Page 145 of AR2017):

As you may have noticed, CapFir has provisions/write-off reported within the '‘other expenses’ while Bajaj Fin has ‘other expenses’ 17% and ‘Loan Loss & provisioning’ of 7%. Therefore, we need to go further level down and scrutinize through the ‘Notes to statement’ to see actual gaps.

- Calc from Capital First Notes #27, Page 158:

- Calc from Bajaj Finance Notes #21 and #22 (page 164 and 165 respectively):

Please note that I am taking the liberty to include ‘Recovery Cost’ from other expenditure and considering those on the lines of write-off/provision etc. Two reasons, a) amount is significantly high ~317 Cr. or ~3% of revenue, b) thinking practical, recovery cost and write-off will have same implication to the business - which is, x rs less recovered against outstanding. (Accounting/regulatory experts please chime-in if I am getting wrong on the practical implication part).

Though not full parity, however now we have somewhat pare-able data. We can study, analyze and drive conclusions.

-

CapitalFirst’s Provision and Write-off at 16.34%, 12.56% and 7.38% of revenue for 2017, 2016 and 2015 receptively. Consistently higher provision/write-off.

-

Bajaj Finance Provision and Write-off at 11.39%, 12.90% and 10.94% of revenue for 2017, 2016 and 2015 receptively. Just stable.

-

Till last year, CapF had comparatively lower numbers under provision etc.

-

Please take a close look, no numbers reported under ‘Bad debt written-off’ for 2017 for Bajaj Finance though this was significant 5.20% and 3.39% of revenue for 2016 and 2015 respectively. Personally, I hold Bajaj Finance very high on so many aspects (and this keeps increasing as I dive more), however, not easy to envision a landing entity having absolute zero write-off. (not suggesting any red flag, just by that though).

-

Not with certainty, however, is this higher write-off by CapF to do anything to do with 120 days DPD transition in FY2017. If true, can be a lead indicator on what to expect since NBFCs need to move to 90 days DPD by 2018.

-

Further, we can expect higher provision for standard Assets as per the RBI Notification 2014-15/299. will Impact both Bajaj Fiance and CapF in FY18 as well though first is NBFC - D (deposit accepting) while later is NBFC - ND - SI.

-

Other key point that Karan delved upon was about Amortization cost for CapF

Very surprising to see approx 8.55% of total revenue going into amortization expenses. As per page 141 of AR, origination cost + expenses are supposed to be amortized equally over loan tenure.

In conclusion, provision/write-off are one of the key watchable in this entire story. Currently also high but not scary high (comparatively speaking). It may has to do with aggressive growth pursued or may have to do with the shift that company is going through on business model. Personally for me, more than the growth, the bet is on transition to retail loan where IRR is better and ticket size is small. That being said, NPA is one of the BIGGEST RISK for any landing entity.

Some documentations for easy reference:

CapF 2017 AR:CFL_AR-2017.pdf (2.2 MB)

Bajaj Fin 2017 AR: Bajaj Financel-annual-report-2017-for-web-indi.pdf (2.2 MB)

Bajaj Finance 2016 AR: bajaj-finance-29th-annual-report - 2015-16.pdf (2.5 MB)

@Karan, @sammy11 and others - Hope we continue the momentum and track it closely on a quarterly basis to see the trajectory.

Regards,

Tarun

Disc: Invested no transaction in last 6 months.