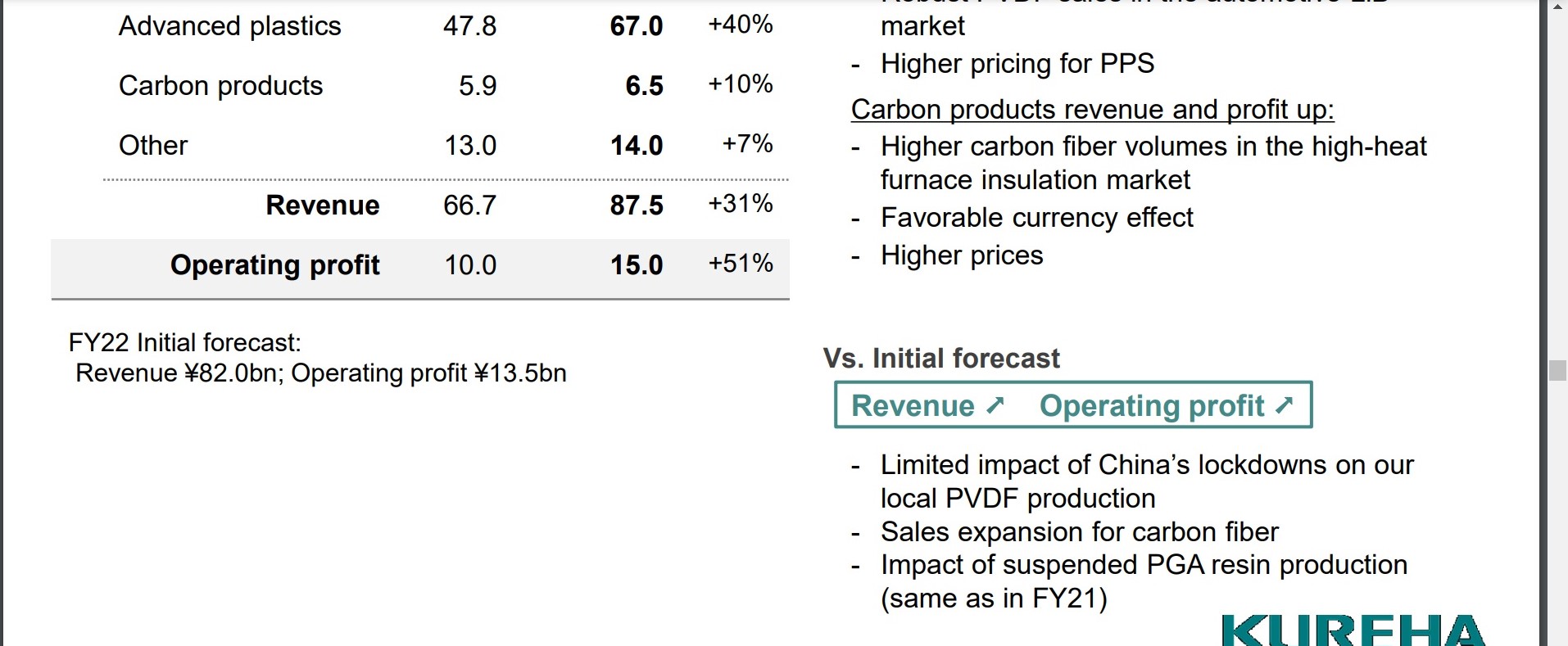

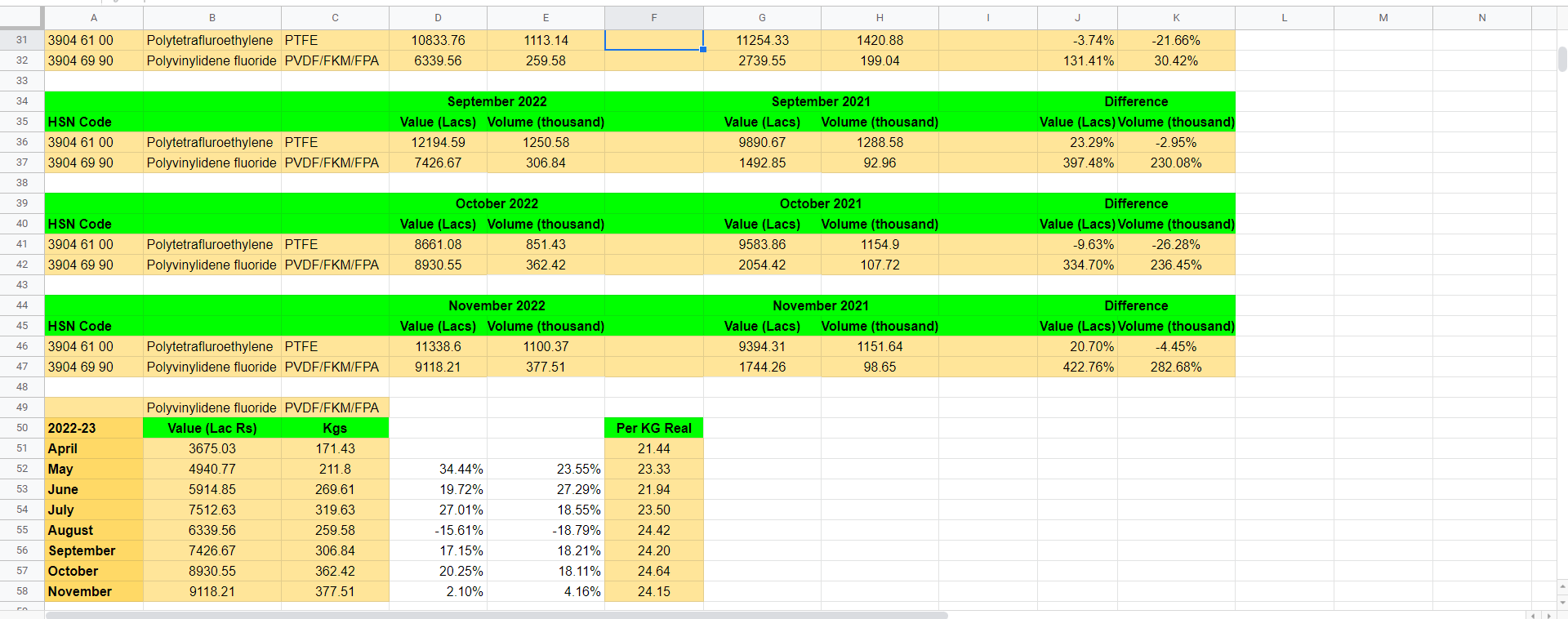

Selected excerpts from WSJ Article on 3M PFAS Liability claims (among others like earplugs)

Liability claims related to chemicals called perfluoroalkyl and polyfluoroalkyl substances, or PFAS, are still growing for 3M. Commonly called “forever chemicals” because they take a long time to break down in the environment, the chemicals have highly durable compounds that can resist heat and repel water, grease and stains.

About 20 years ago, 3M quit making two varieties of PFAS chemicals that are often linked to health concerns. Before 3M discontinued production of the two chemicals, it sold them to other companies for use in their products, potentially exposing 3M to litigation and cleanup expenses incurred by other companies, analysts have said.

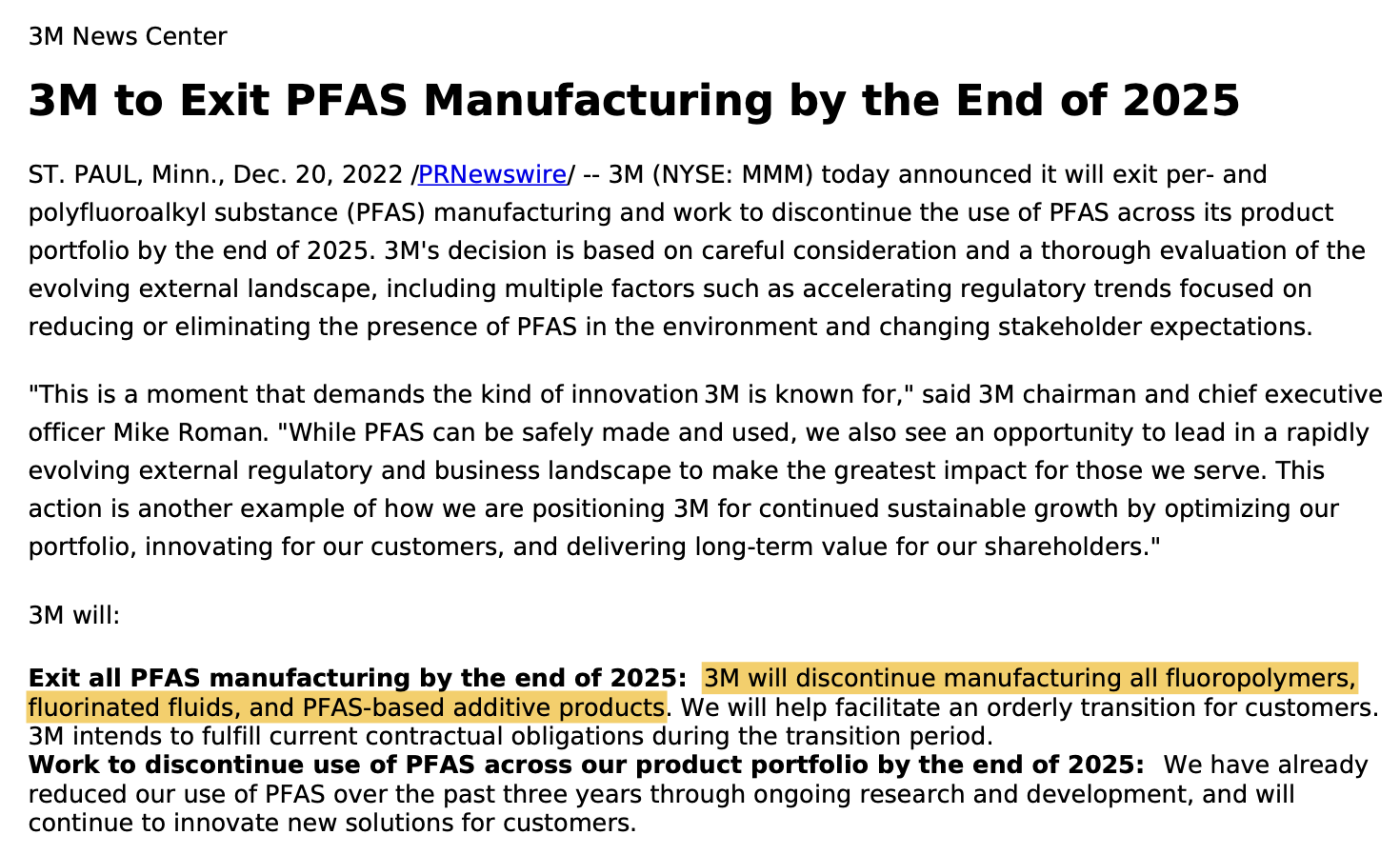

While the company continued to make other varieties of PFAS chemicals that 3M has said are safe, the company said Dec. 20 that it would wind down its production of those chemicals by the end of 2025, citing increasing regulation and customers’ interest in alternatives.

3M estimated its current annual sales of PFAS chemicals at about $1.3 billion, or about 4% of total sales, according to analyst estimates. Nigel Coe, an analyst for Wolfe Research, said exiting the business would be relatively immaterial for 3M, but is a “reminder of long-tail PFAS remediation and compensation risks.”

Related reading:

Stricter federal guidelines on ‘forever chemicals’

More on PFAS liabilities here and here (mostly relate though to PFOA and PFOS discontinued in 2000 by 3M and 2015 by Dupont

3M’s liability from PFAS litigation could reach nearly $30 billion by the end of the decade, according to Capstone. The group estimates that more than half of that could be paid to cover claims over firefighting foam.

DuPont has an agreement to share PFAS liability costs with Chemours Co. and Corteva Inc., two companies spun off from DuPont’s predecessor businesses during the past decade. The agreement is set to last until 2040 or up to $4 billion.

PFAS Legal Liability Exposures - What Manufacturers need to know

There are currently three tiers of manufacturers that experience PFAS risk.

The first tier includes those who actually fabricate PFAS chemicals. These manufacturers face the highest level of exposure to legal liability risks.

Since 2005, DuPont has been a named defendant in over 6,100 lawsuits related to PFAS; some estimates show 3M’s PFAS liabilities could reach as high as $30 billion, this Bloomberg PFAS lawsuits report details.

The second tier of manufactures with exposure to PFAS liabilities includes companies that used PFAS chemicals to treat the products they produce, typically for water-, stain- or fireproofing.

The third tier encompasses companies that have supply chain exposures. These companies are likely assembling products out of components that have been treated with PFAS but don’t use the chemicals themselves.

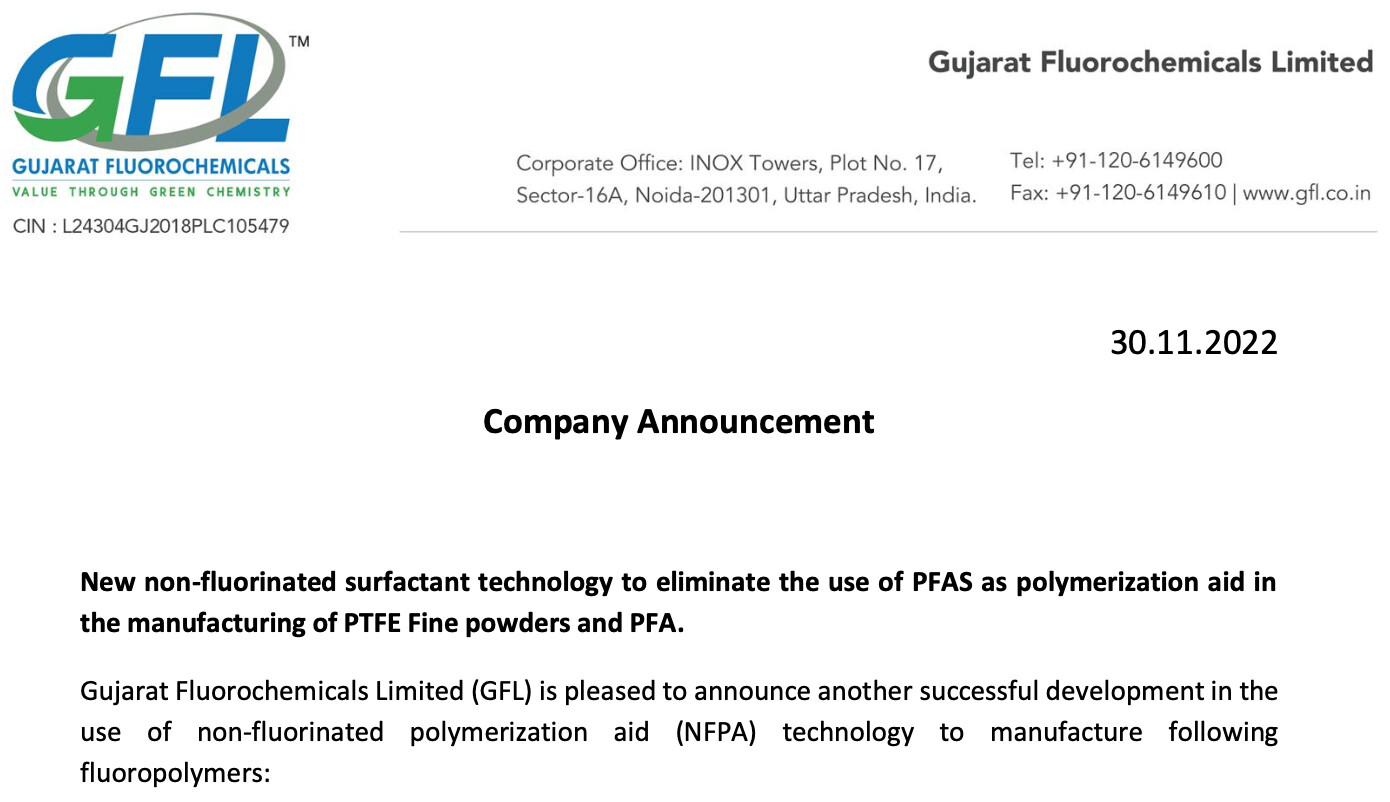

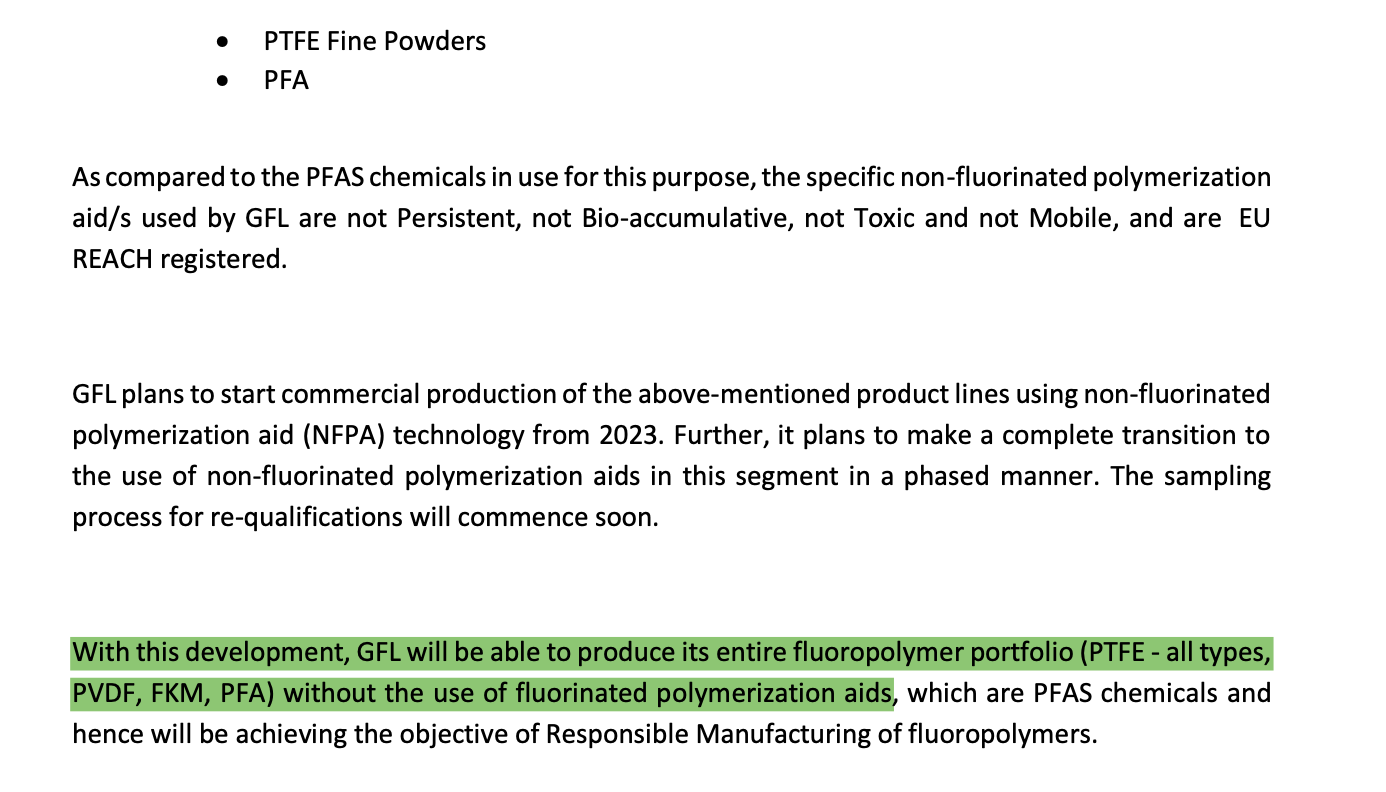

Summary: Prima Facie, looks like most litigation are to do with legacy discontinued use of PFOS and PFOA class of PFAS products, and other products using PFAS chemicals (flourinated ploymerization aids). GFL consistent course of action of announcements since early 2022 of having developed completely new processes (PFAS free) by now for its entire Fluoropolymer portfolio (PTFE all types, PVDF, FKM, PFA) as summarised nicely by @spatel above, shows commendable strategic intent and ability to deliver on critical business/technology/legal challenges, without taking foot-off-the-pedal?