2500 Cr investment in FY23 and FY24 - More granular Capex details here from Indian Chemical News

There is perhaps more “Opportunity” in the constantly evolving Supply/Demand situation for a nimble player like Gujarat Fluorochem (?), provided we can strive to understand the Industry/BusinessCanvas better!

Selected Excerpts. Not sure these have been shared publicly before (?)

Cyclicality concerns (in 1-2 years) in some Key GFL products like LiPF6 and PVDF are valid. Equally there are big opportunities in LiFSI, HFPs and Refrigerants (?).

One direction we could work on understanding/establishing *Changes" global supply/demand scenarios for Gujarat Fluorochem Product Pipeline.

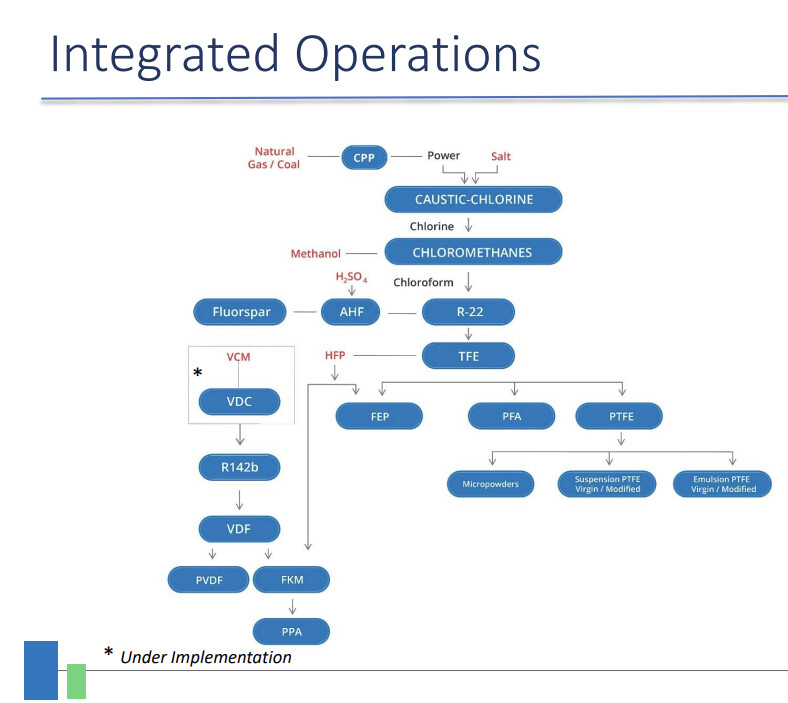

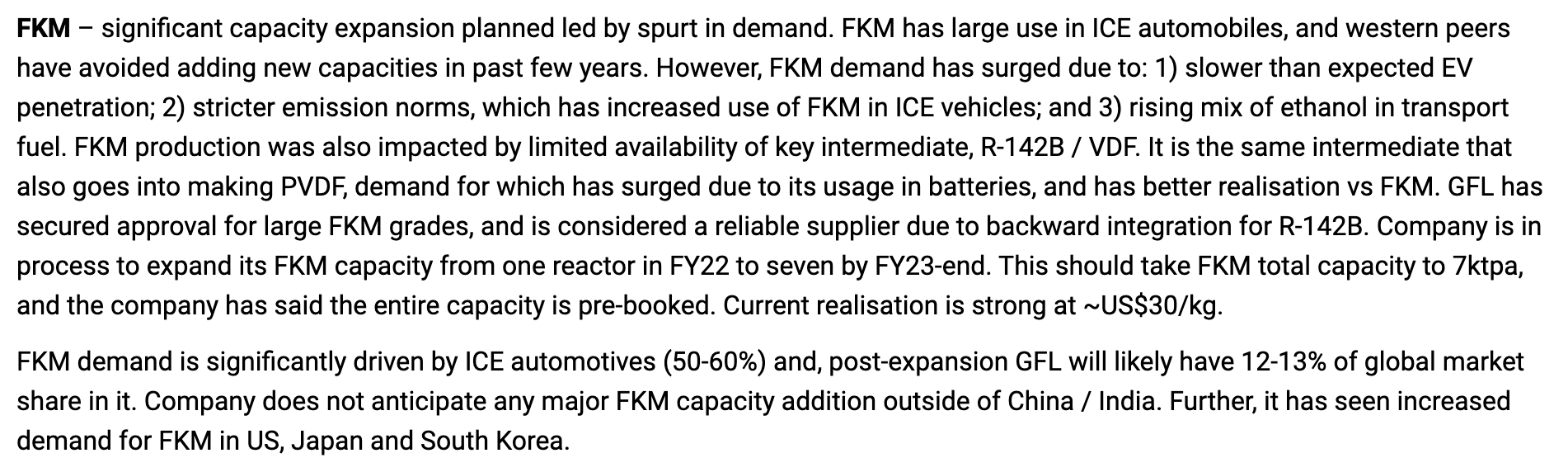

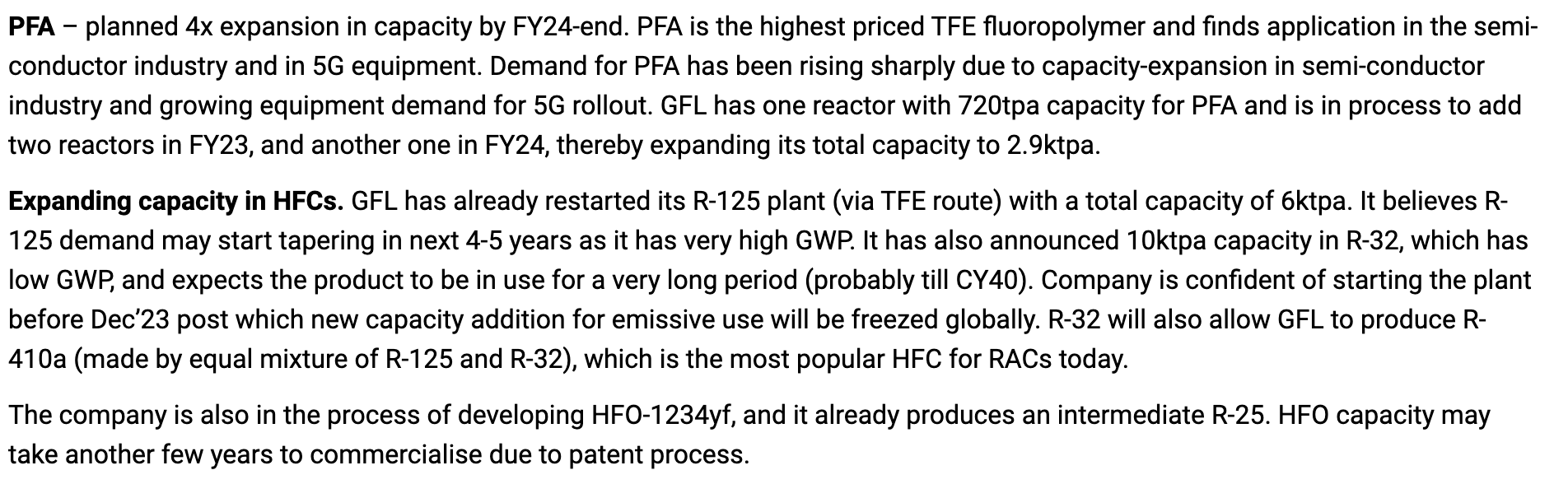

- R-22 >> HFP >>High performance FP route products including FKM, FEP, PFA, HFE, PFPE, R127

- LiPF6 supply glut expected in 2 years vs LiFSI ramp up

- Industrial PVDF glut in 2 years vs battery grade PVDF

- Domestic Supply cornering vs Exports (especially new FPs, battery chemicals)

- China+1 Competitive Position for US and EU markets, Non-China

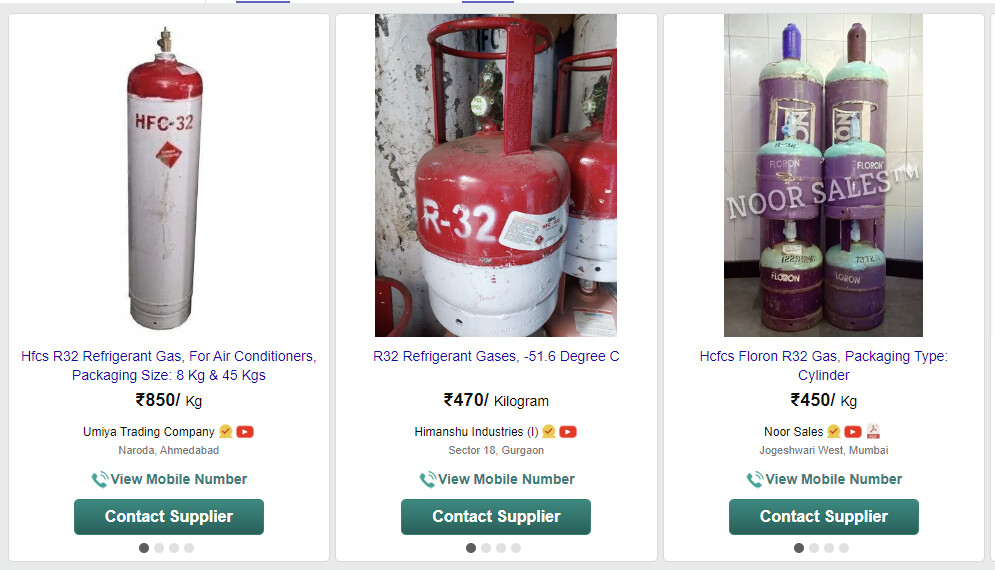

- Refrigerants biggest Opportunity in next 2-3 years (post dec 2023 quota freeze) (?)

- Timeline for starting on Class III Refrigerants like R-32 and R 410A critical for Gujarat Fluorochem as Quotas will be decided based on production achieved till Dec '23 end? GFL is unlikely to have production ramp up/dumping route scope available like the Chinese have? vs Country Quotas ?

- Easy/Difficult Fungibility of Capacities (between HFPs, other FPs, Refrigerant classes). This is a key understanding required.

If we all can put energies into taking this forward, I think GFL Q3FY23 Concall interaction/ questioning can be qualitatively that much better.

Study Direction 1

HFP: the rising star of fluorine chemicals (Global Supply Deficit situation 2023-2025 (?)

HFP (hexafluoropropylene), produced from pyrolysis reaction of R22 (Class II refrigerant), is the

most important monomer within the fluorine chemical family.

HFP is one of the building blocks of high-performance materials in the fluorochemical space. In terms of total number of end products, HFP triumphs among fluorine chemical monomers. Leading fluorochemical companies in the world including 3M, Dupont and Daikin have specialized in HFP derivative product R&D.

Different from other fluorine chemicals like PVDF and LiPF6 which are downstream products, HFP is a fluoro-monomer which is used as an intermediary for the production of multiple high performance

fluoropolymers including PFA (perfluoro-alkoxy polymer) for proton exchange membrane of hydrogen fuel cells, HFE (hydro-fluoro-ether) for semiconductor chillers and IDC immersion coolants, and FKM (fluoro-elastomers) which is a type of special rubber used in sealing and piping for aerospace and high-end vehicles.

Chinese companies are new to the field of HFP derivatives?

Gujarat Fluorochem key (HFP and TFE) derivative products are FKM, FEP and PFA

Production for R22 as a Class II refrigerant is likely to drop to 32.5% of its respective baseline in 2025E, from 65% level currently. Reduction in supply of refrigerants should increase the average sales price (ASP) for R22 for both feedstock and refrigerant uses, offering support for future HFP ASP increases (?)

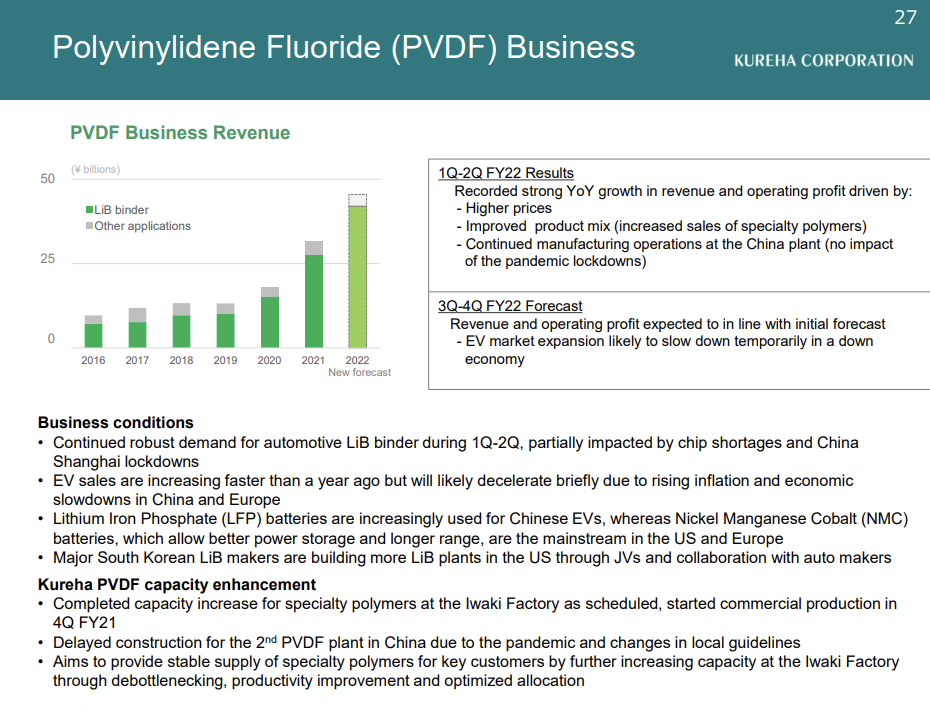

Recent changes in ASPs are a great indication of the supply situation. Both LiPF6 and PVDF are showing downward pressure while price for HFP stays resilient. [Source: Credit Suisse Fluorochemicals Report 6 Dec, 2022]

China+1 may drive significant change non-china (US/EU/India) and govt discounting and ADDs may keep coming (?)

Study Direction 2

Refrigerants: Class III bigger Opportunity (?)

Most of battery Energy Storage Systems (ESS) adopt Class III refrigerants such as R32 or R410a (blended refrigerant of R32 and R125). Total consumption of refrigerants will increase with respect to rising installation of renewable capacity and increasing penetration of ESS incorporation in the installed capacities of renewables.

Total new capacities of battery ESS is growing exponentially at 82% CAGR in 2022-2025E and 38% in 2025-2030E which will lead to drastic increase in demand for Class III refrigerants. Demand from ESS thermal management might be the leading driver in refrigerant consumption for the upcoming years (?)

Likely 2023-2025 Cyclicality (Surplus/Deficit) Picture (?)

LiPF6 ↓↓

LiFSI ↑↑

PVDF ↓

Refrigerants ↑↑

FKM/PTFE/PFA ↑

Disclosure: Invested