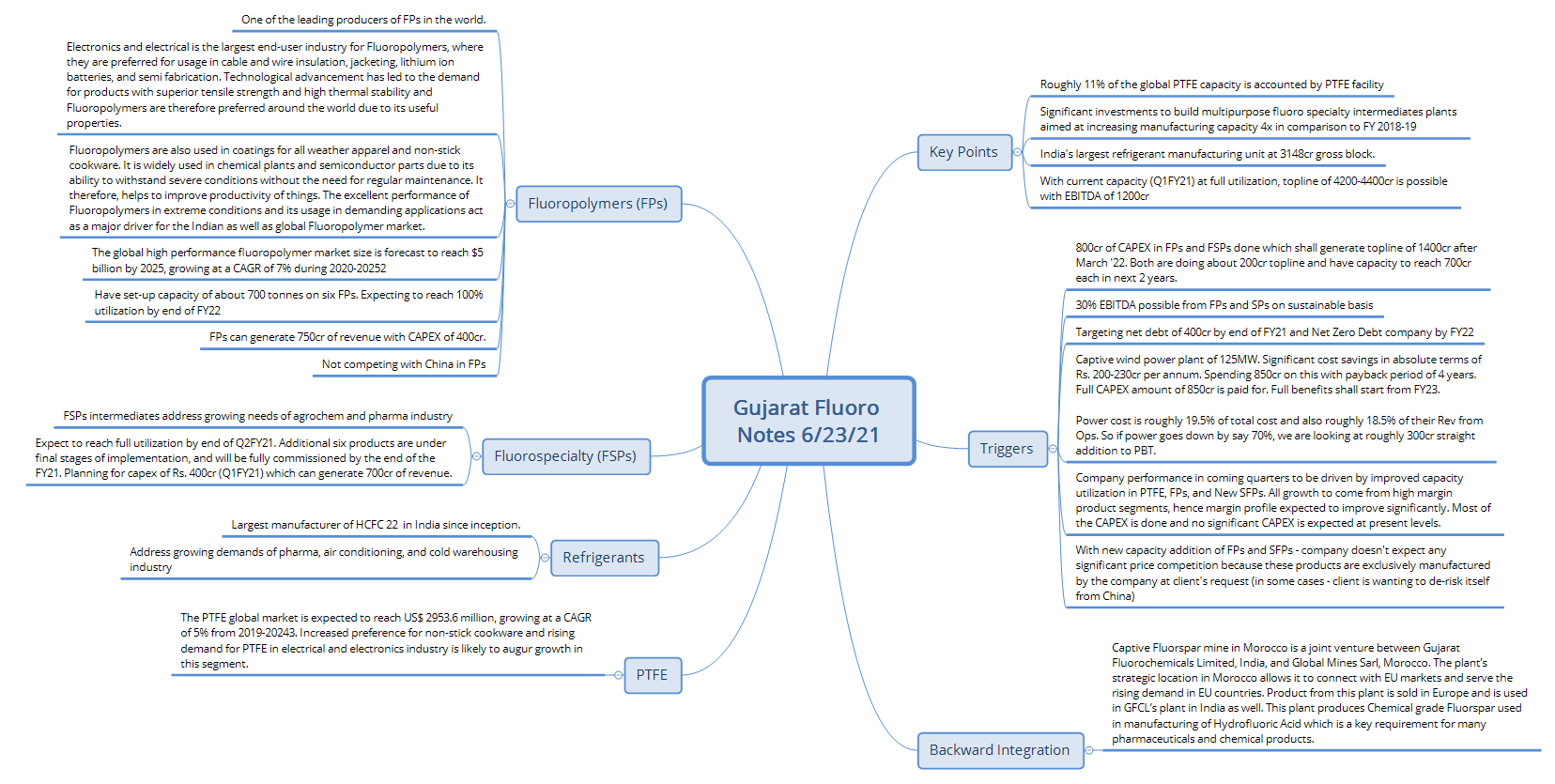

Background

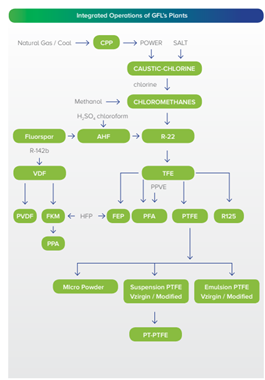

Gujarat Fluorochemical Limited (Fluorochem) is a major player in Fluorine Chemistry in India with a major focus on PTFE, Specialty Fluorochemicals and Specialty Fluoropolymers. FLUOROCHEM was setup in 1987 to manufacture refrigerant gases in collaboration with Stauffer Chemicals and Stearns Catalytic near Vadodara. The company was a major player in CFC gases (R11, R12, R22) with Refron brand. In 2007-08 FLUOROCHEM established a Chemical complex in Dahej with captive power plant, Caustic soda, Chloromethane plant and PTFE/Teflon plant. R22 which was subject to progressive production cuts due to environmental norms was used as feedstock for PTFE. FLUOROCHEM erstwhile known as GFL also ventured into multiple unrelated areas like Inox Leisure (1999)/Inox Wind (2009). In 2011 FLUOROCHEM entered a Fluorspar beneficiation process to completely backward integrate. With complete backward integration in Fluoropolymer manufacturing FLUOROCHEM expanded into monomer/polymer capacities and ventured into multiple Specialty Fluoropolymers/Fluoroelastomers like FEP, PFA, PTFE micropowders etc. The company also ventured into Fluorospecialty chemicals.

Customers segments

Fluoropolymers are majorly used in very specialized applications which require non adhesive, low friction properties along with extreme heat, corrosion resistance, difficult weather and harsh chemical conditions. FP finds usage in automotive, aerospace, semiconductors, electronics, common household appliances. FPs because of their physical properties are also expected to find increasing usage in EV batteries and 5G where thermal requirements are significantly stringent.

Fluorospeciality chemicals {FSC) are intermediates used in agrochemical and pharmaceutical industries. Company has commercialized seven molecules and is looking to add more. This segment has large growth opportunities and is a proxy to the growth of pharma, agro chem, electronic and polymer industries. Further, it is planning to incur capex for additional six products and has guided for its commissioning by end FY21. There is also a strategic need of both domestic and overseas customers to de risk from China.

Refrigerant gases are no longer the focus area for FLUOROCHEM. FLUOROCHEM today majorly manufactures R22 as feedstock for FP. It still continues to sell R22 in retail and also as feedstock to agchem/pharma companies.

Chloromethanes consists of three products Chloroform, Methylene Dichloride (MDC), Carbon Tetrachloride (CTC), as of now Fluorochem is the only producer of of MDC and CTC in India.

Caustic Soda

Chloromethanes and caustic soda are in some ways a byproduct since the entire process of manufacturing FSC/FSP/Refrigerant gases requires significant amounts of Caustic/Chlorine/Chloromethanes. In the rest of the discussion, we will be majorly focusing on FPs and SFCs.

Main Products/Segments and Capacities

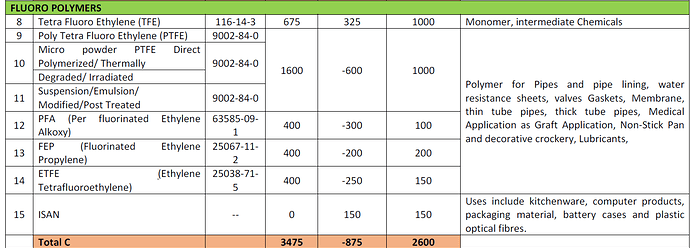

The major segments are PTFE (33%, 20000 TPA), Specialty/New FP (10%, 8500 TPA (FKM 2500 TPA, FEP 1000 TPA, PFA 750 TPA, PPA 600 TPA , MicroPowders 1200 TPA, VDF Monomer 2300 TPA, PVDF Monomer 1400 TPA)), FSC (12%), Chloromethanes (13%, 87500 TPA), Refrigerant gases (14%), Caustic Soda (12%, 110000 TPA) as per Q2FY21. The currently commercialized molecules in FSC are ETHYL DIFLUOROACETATE, 2,6-DICHLORO-4-TRIFLUOROMETHYL ANILINE, DIFLUOROMETHANE SULPHONYL CHLORIDE, BROMO TRIFLUOROMETHANE, ETHYL 1,1,2,2, TETRAFLUOROETHYL ETHER, 2,4 DIFLUOROBENZYLAMINE, 1,3-DFB, TRIETHYL ORTHOFORMATE.

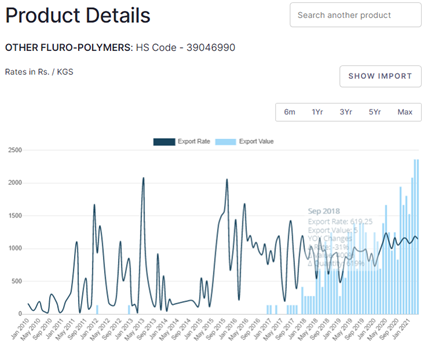

Exports (~50% of Sales in FY2011) are mainly PTFE and its grades, FSC and FSP. The company has nearly 11% of the PTFE capacity worldwide.

Backward Integration

FLUOROCHEM produces HCFC22 from Anhydrous Hydrogen Fluoride (AHF) and chloroform. AHF is made from fluorspar and Sulphuric Acid. Fluorspar is produced in Morocco and chloroform is made from Chlorine in the Chloromethane plant at Dahej. FLUOROCHEM has captive power plant based on coal and natural Gas. Thus, from basic materials like salt, Sulphuric Acid, Methanol, coal and gas FLUOROCHEM builds the entire value chain.

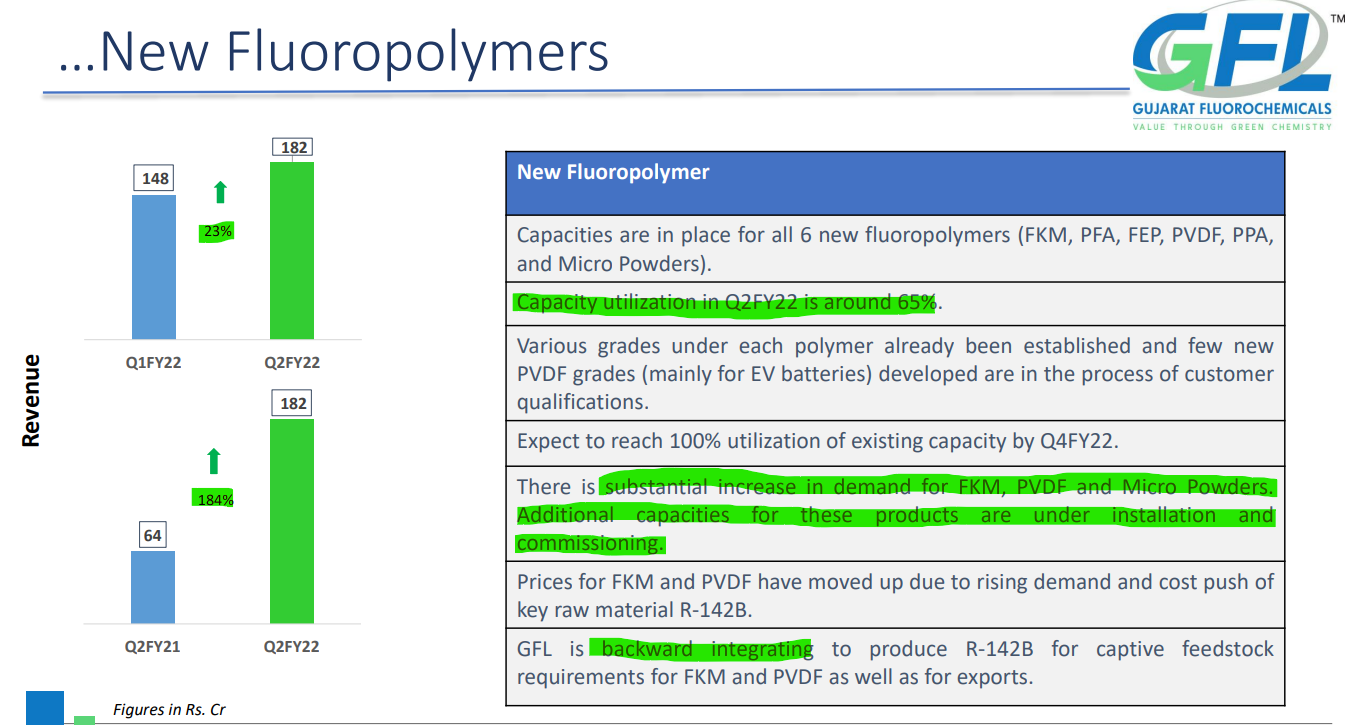

Upcoming capacities

The company in its presentation has said that it is working on several new products which have been developed in-house R&D and is planning to incur additional capex of Rs 3.0-3.5 bn in the FS chemicals. In the PTFE segment it plans to add around 400 TPM (3000 TPA) capacity. In the new FP segment it plans to add 450 TPM (3000 TPA) capacity.

Recent Environmental Filing

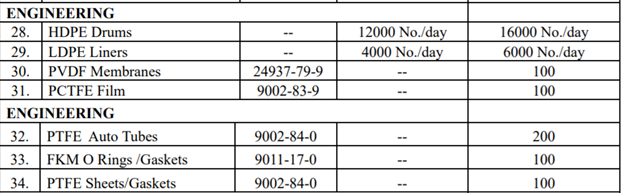

More interesting is the recent environmental filing where the company has indicated of a capex of 1100 cr. Most of this is going into SFC and also into forward integration of PTFE/SFPs. The company has also indicated that it will enter the end product market in PTFE/SFP by venturing into PVDF membranes, PCTFE film, PTFE auto tubes, PTFE sheets/gaskets and FKM O Rings/Gaskets.

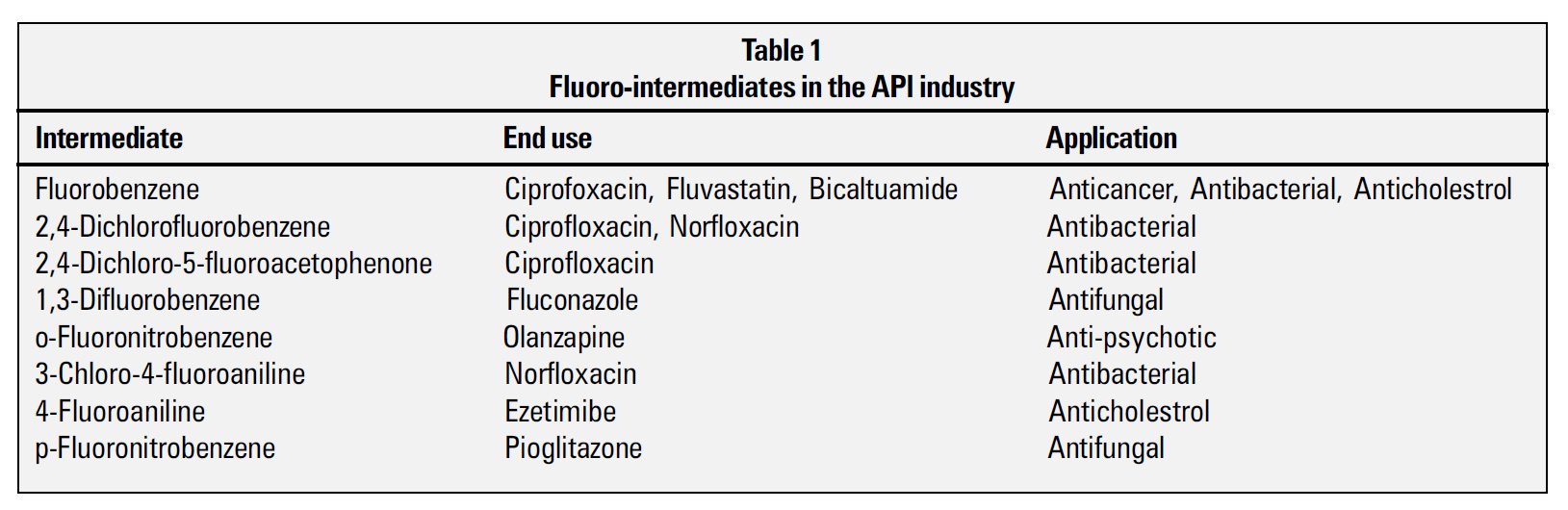

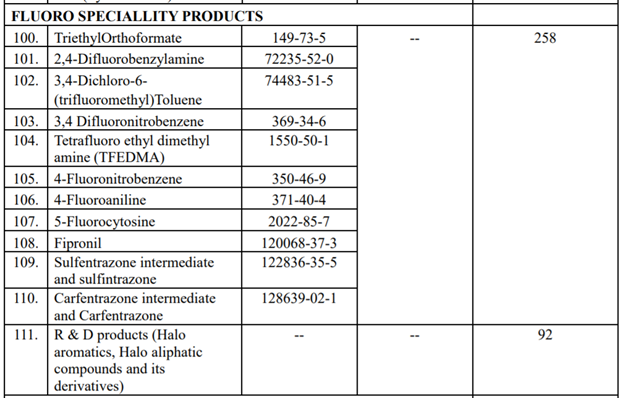

The list of FSC is huge with some of them being intermediates. Some interesting ones which actually look like agchem technical are

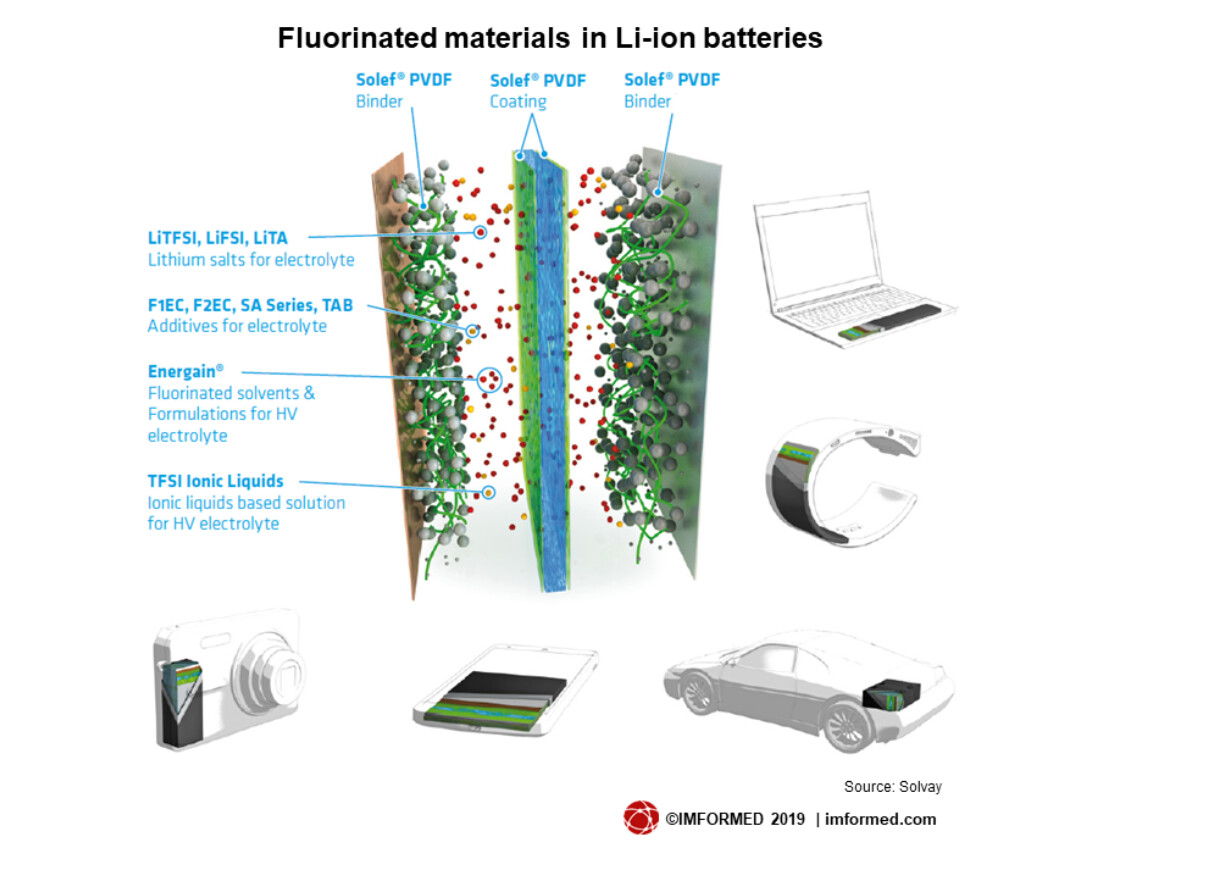

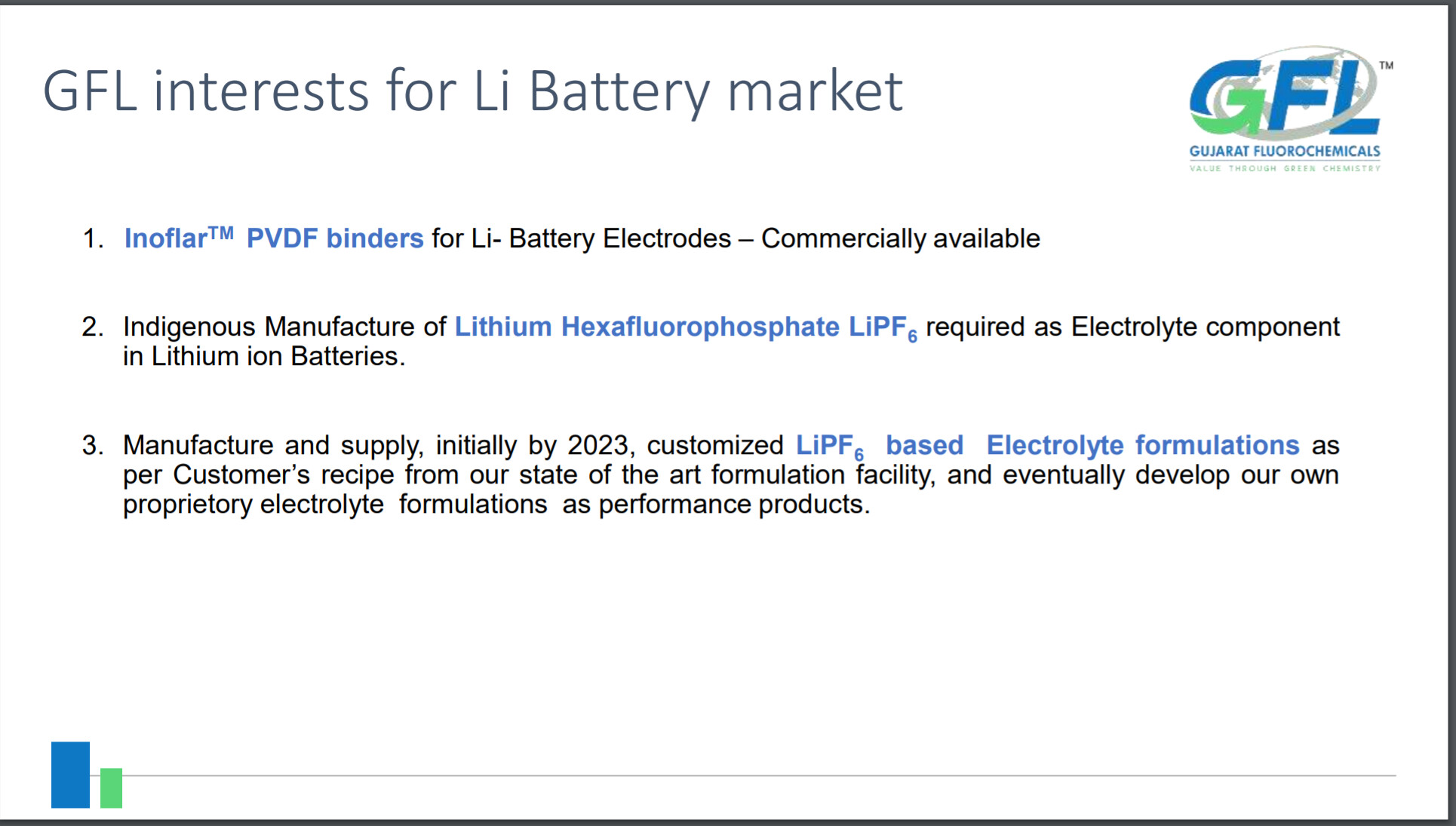

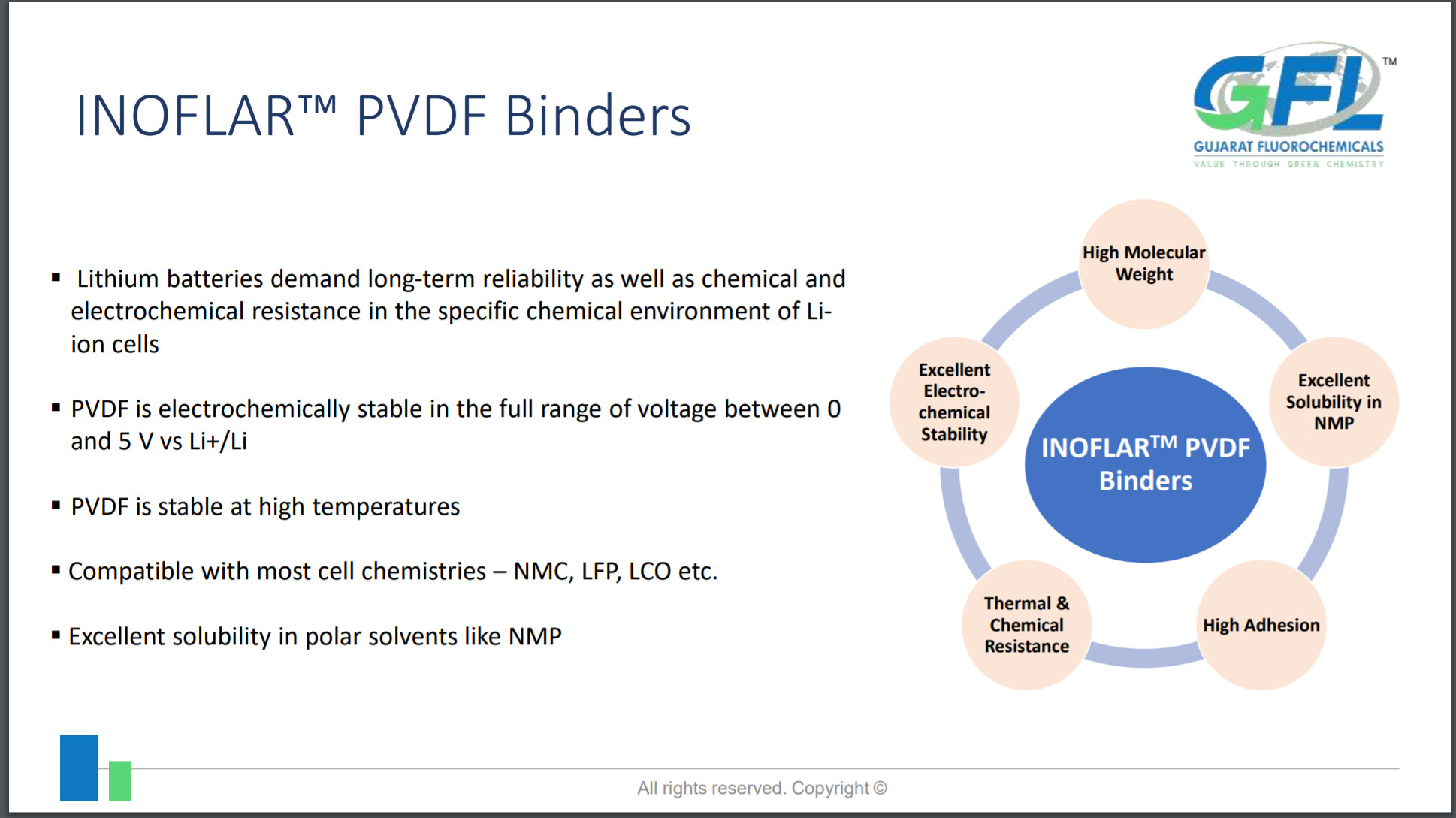

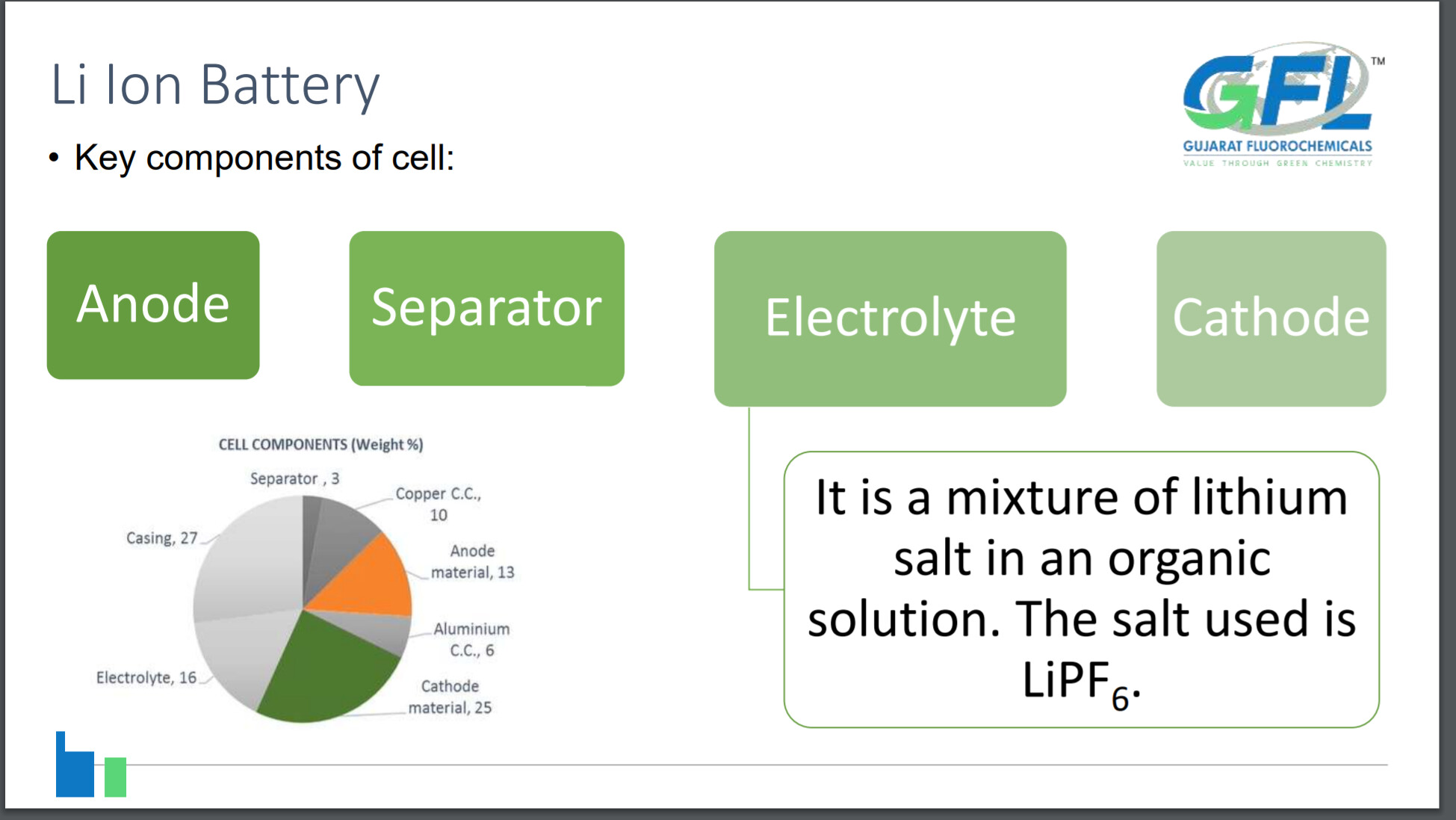

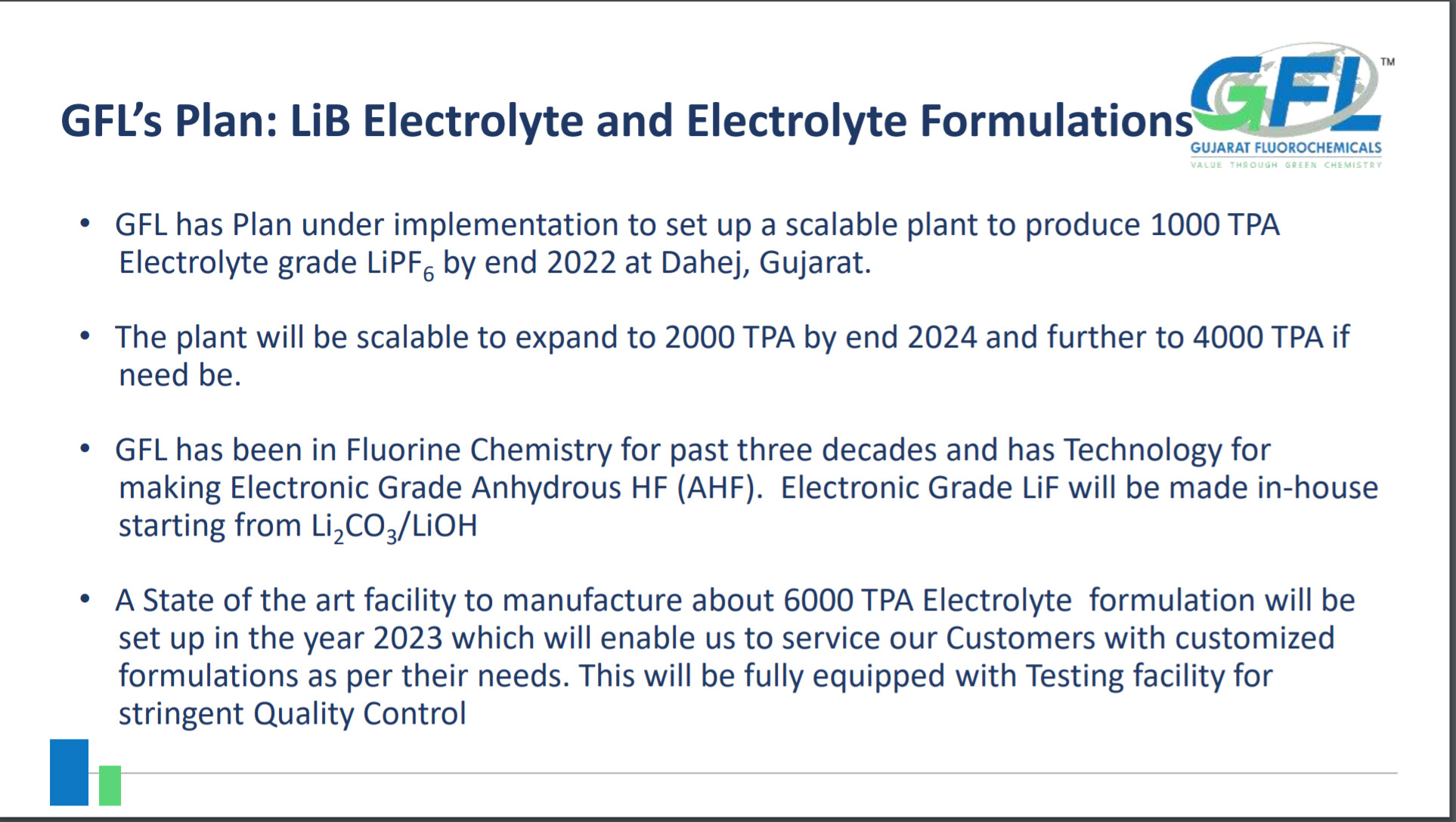

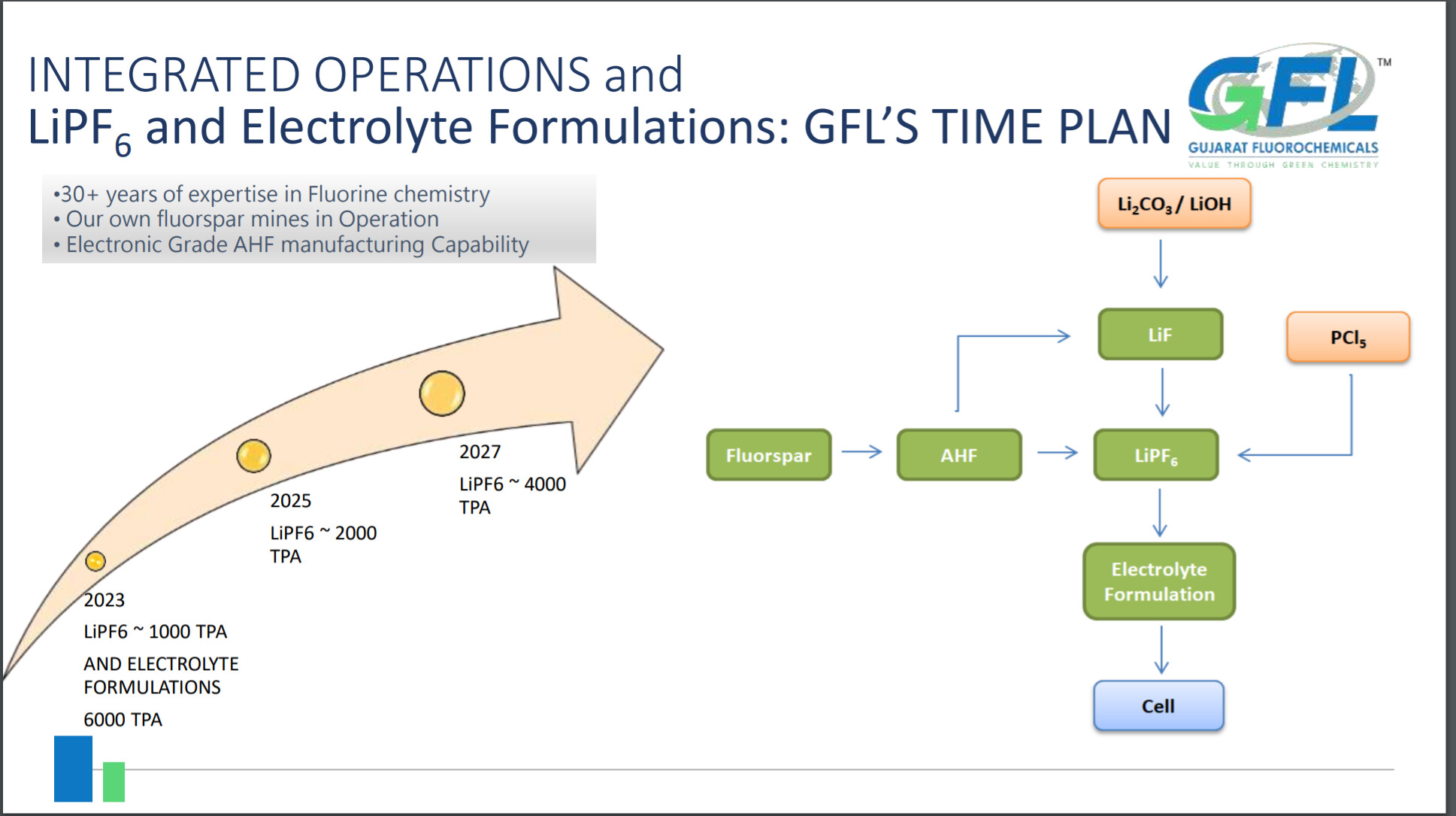

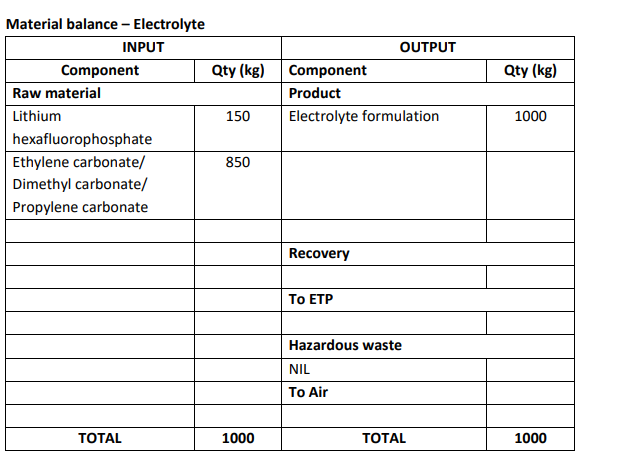

LiPF6 is another interesting product since it is used as electrolyte in Li-ion batteries

Opportunity Size and Competition:

FP:

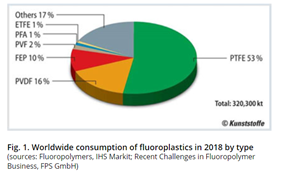

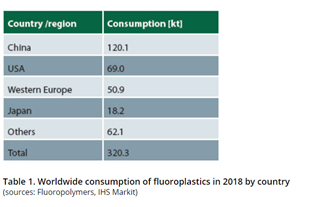

Worldwide consumption of FP including PTFE is around 320 kt. n 2018, 320.3kt of fluoroplastics were consumed worldwide (Table 1). By comparison, global consumption in 2015 was 270 kt.

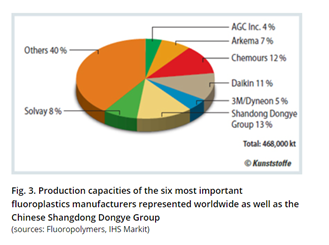

The worldwide production volume of fluoroplastics in 2018 was 316kt. In terms of market share, production integration, geographical presence and breadth of the product portfolio, The Chemours Company, USA, is currently regarded as the largest manufacturer. Other leading suppliers with two or more worldwide production sites are AGC Inc. in Japan (formerly the Asahi Glass Company), Arkema in France, Daikin Industries Ltd. in Japan, 3M/Dyneon in Germany and Solvay SA in Belgium (Fig. 3). In addition, there is the Chinese Shandong Dongye Group, Ltd. which owns the world’s largest production plant for PTFE. As of now Gujarat Fluorochem is the only manufacturer of FPs in India. Fluorochem has around 11% of the total worldwide PTFE capacity.

Disc. Invested

TBCNavinFluorineInitiation.pdf (1.2 MB) IDirect_LaxmiOrganics_IPOReview.pdf (485.0 KB) overview-of-the-fluorochemicals-industrial-sectors (1).pdf (264.1 KB) Fluoro Intermediates.pdf (99.9 KB) Gujarat Fluorochemicals - Q2FY21 Result Update - 13 Nov 20.pdf (417.0 KB) Gujarat Fluorochemicals - 1QFY21 Result Update - 01 Aug 20 (1).pdf (213.2 KB)Environmental FIling.pdf (2.3 MB)