Q1 FY23

Few comments and TODO items based on Q1 results -

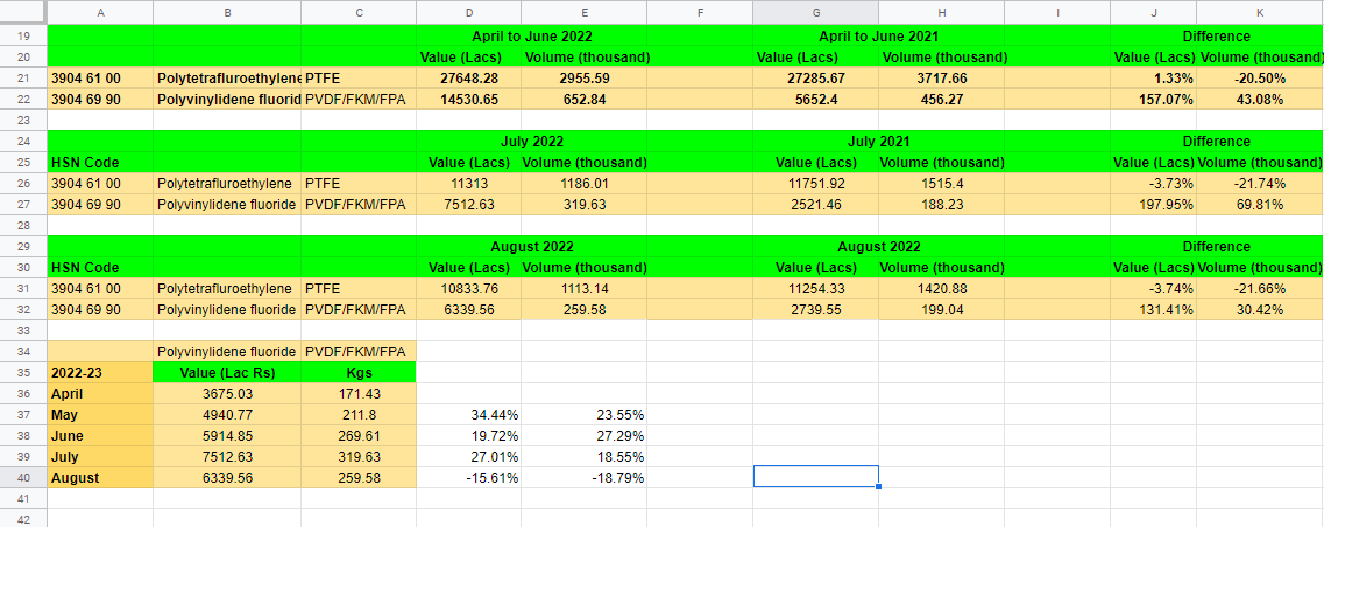

PTFE

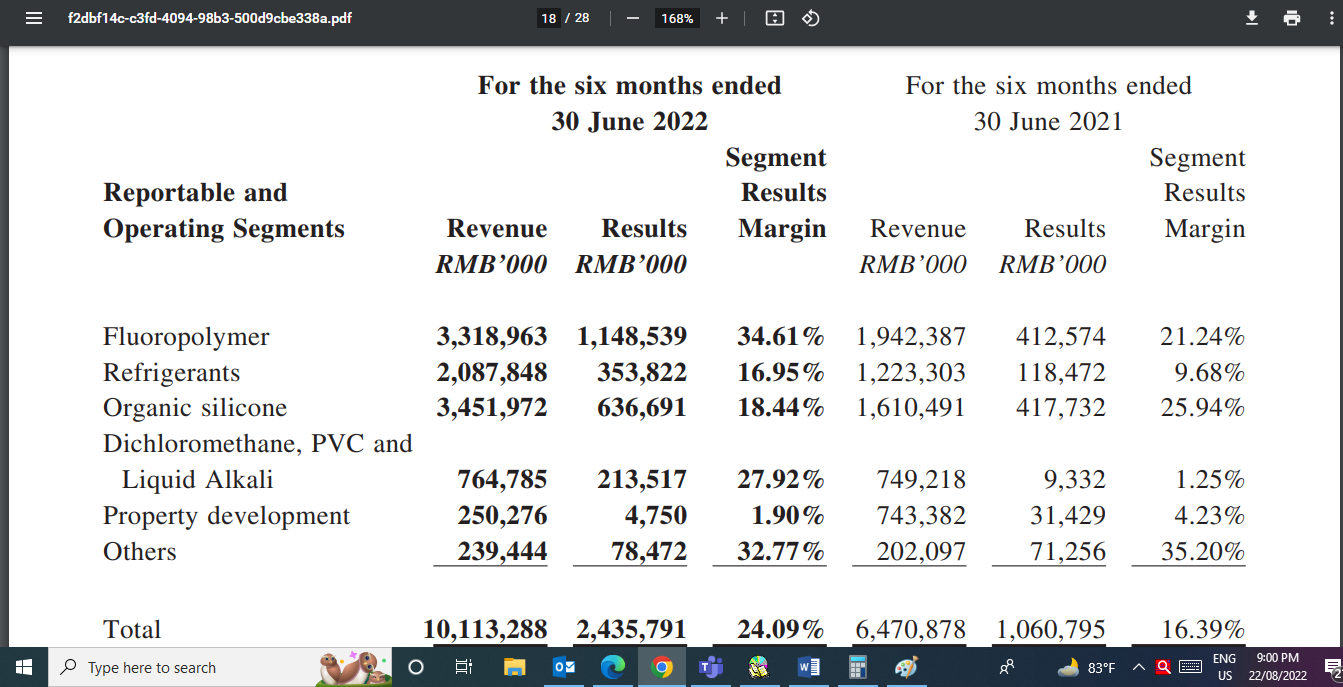

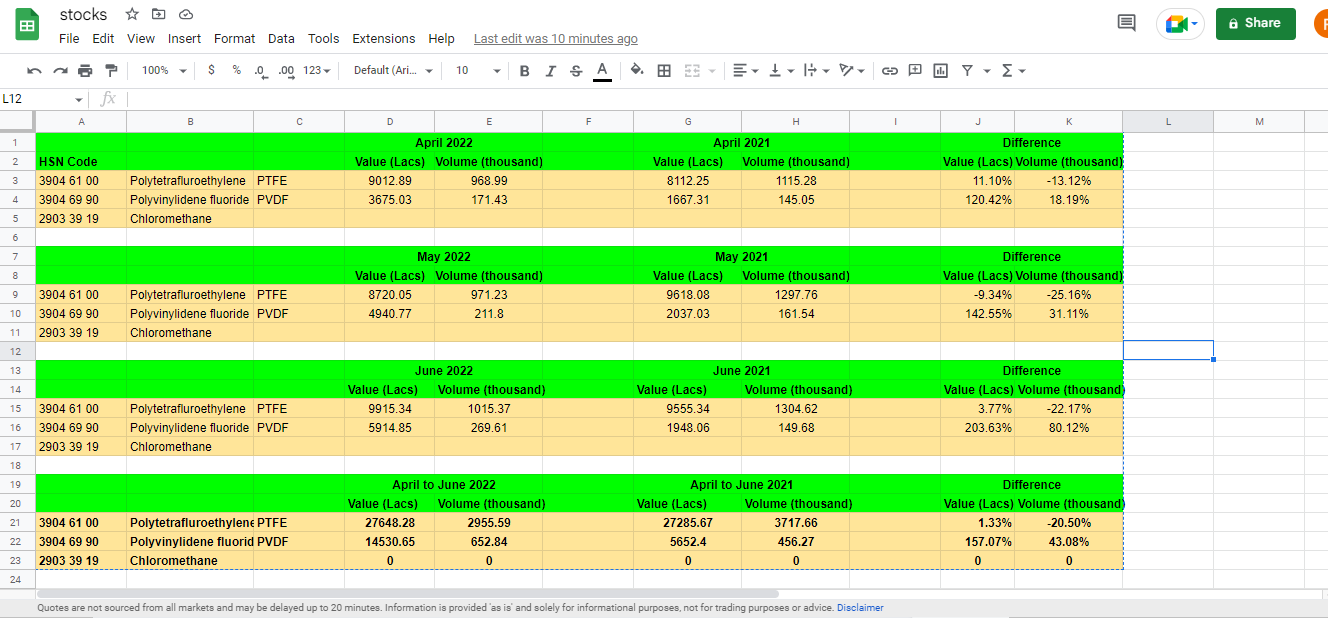

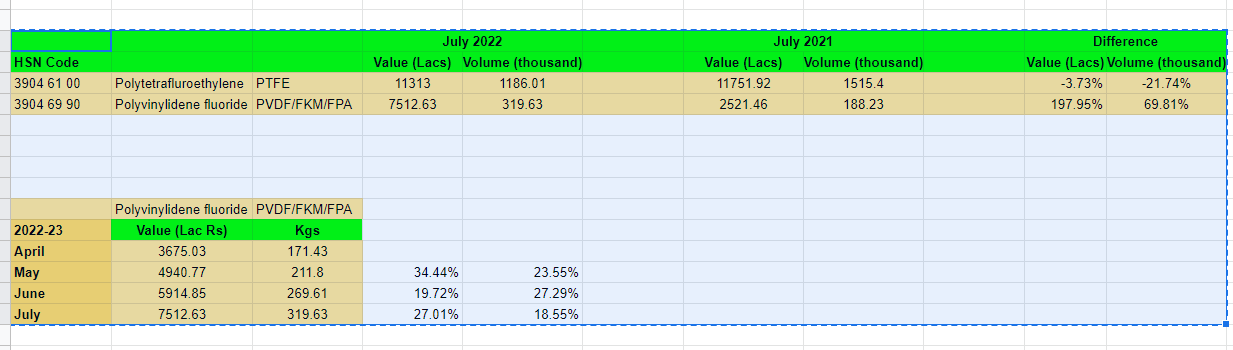

PTFE capacity is roughly 1500 TPM (Value Added - 900 TPM and Regular 600 TPM). PTFE prices have gone up due to 900-950 rs due to various reasons. At 900rs, the monthly revenue potential comes to 135cr and annual revenue potential comes to 1620cr.

With 25% capacity addition by Q4 exit, capacity comes ~1900-2000 TPM and annual revenue potential goes to 2000cr.

SRF PTFE capacity, which is for regular grades, comes online by Oct’22. We need to track PTFE prices, especially in domestic market when that happens. Also management claims of developing various specialised grades for PTFE and hence some sort of competitive advantage will be put to test from FY24.

We also need to keep tracking PTFE prices in global market with export restrictions on HaloPolymer.

TODO - Look at market sales and realisation trends of HaloPolymer and also Dongyue in PTFE. We need to see if HaloPolymer does dumping in Indian market (although there is ADD on it).

Overall, PTFE will remain 2000cr +/- 200cr type of business for GFL from FY24. How much to analyze this segment other than sharp drop in PTFE prices is one’s own call.

New Age FP

New Age FP capacity was 700 TPM at the start of FY22 - out of which 250 TPM was micro powder PTFE. Micro powder PTFE should really be counted in PTFE itself but nonetheless, real new age FP capacity is 550 TPM.

This 700 TPM capacity has gone to 1100 TPM at the beginning of FY23 and will be 1500 TPM by the exit of FY23.

TODO - Try to find out how much is micro powder PTFE capacity out of new 800 TPM capacity that comes online, mostly all the new capacity is towards PVDF, FKM etc. but it would be good to go through EC etc. and ask management.

New Age FP have 50% more realisation than PTFE. So at 18$ average realization, revenue potential for FY24 comes to 1500 * 18$ * 78 * 12 = 2525cr. So ~ 2500cr of entire new segment is going to be created which is going to have higher margins.

TODO - Find out the new age FP capacity by FY24 exit (should be another 400-500 TPM).

Another thing in this segment is incoming forward and backward integration which can lead to margin expansion -

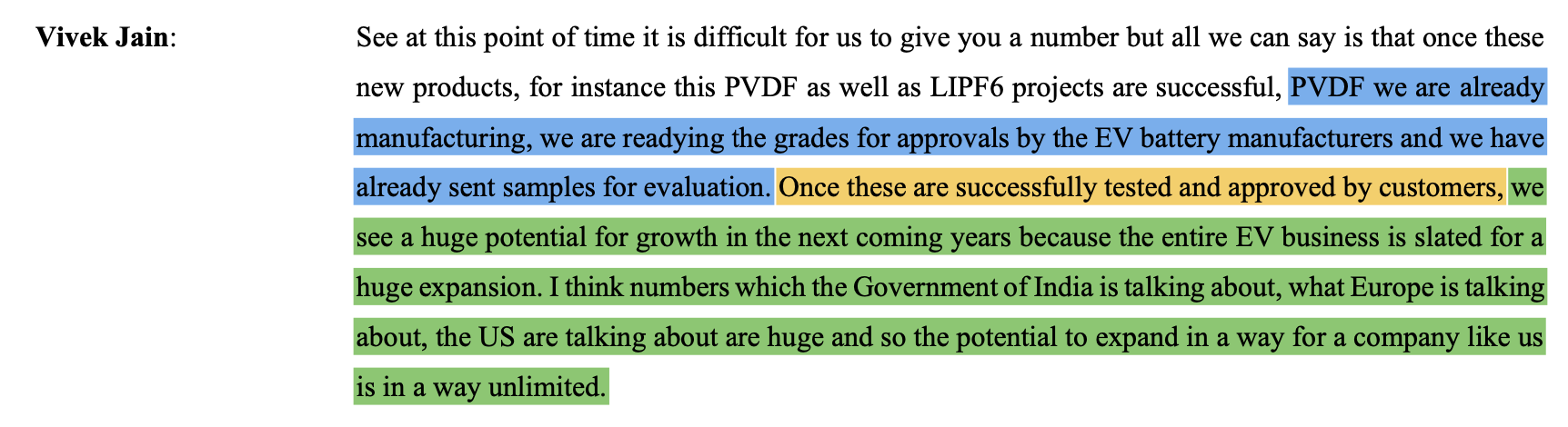

- PVDF binder is slightly more complex product than plain vanilla PVDF. Sales of PVDF binder have not started yet. PVDF sells at 18-20$ currently. I am hoping PVDF binder sells at at least 25$ and that is one lever for margin expansion (forward integration).

- Similar is the case for PVDF films which is also a sort of forward integration.

- Another thing is that company has already backward integrated till R-142B in PVDF/FKM chain. There is one more step of backward integration coming up with VDC - hopefully by FY23 exit.

TODO

- We need to map PVDF current capacities and expansion of few big players like - Arkema, Solvay, Dongyue etc. We need to map how much of this capacity is in Europe, China and Rest of the world. This will help us clearly get market formation in PVDF and potential early hints about PVDF pricing trends.

Overall, a very strong 2500cr segment with margins better than company average is coming in revenues. How much of this is factored in valuations is one’s individual call.

Battery Chemicals

In Q1 call, company stated ambition of creating another segment of battery chemicals (LiPF6, additives etc.) which will be of size 2000cr in medium term. Initial capacity would be 2000 TPM and initially sales will be to export markets and then towards domestic markets.

TODO - We need to find out realisation of LiPF6 and margins that other players make. We need to understand the chemistry chain and how much backward integration can GFL do. We need to have some estimate of ROCE in this segment. If globally some player has achieved some sort of competitive advantage (LG Chemicals ?), we need to understand the source of that competitive advantage.

Another item in TODO -

Find out capacity of R-142B and VDC and how much will be used captively and how much will be sold in open market. (I think in Q3/Q4 concall, this info was given - need to look up).

Disc - Invested and extremely biased. No transactions in last 30 days. Not a buy/sell reco.