In this post, I am sharing a few of my notes and observations in my research on the global competitors in this space.

- 350 g of FPs per car is used - such as Seals, gaskets, transmission components, cables, hoses, increasing amounts for Fuel cell membranes, electrolytes, and separators of Li-ion batteries.

- In aeronautics - used for fire retardant coatings, elastomers for gaskets and cables which on average

are 1km-cables made of FPs per passenger in planes - IN 2012 - total FP production was 223,000 tons while it’s forecasted to be close to 400,000 tons by 2022.

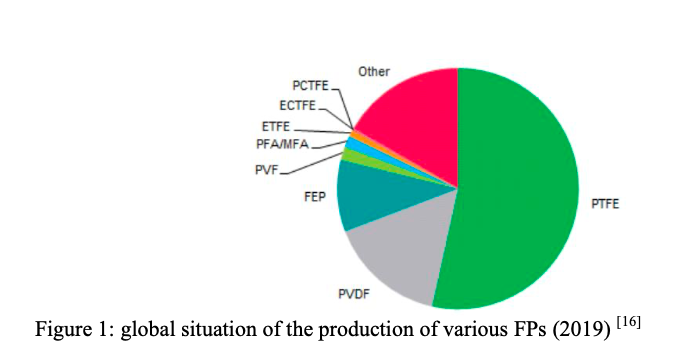

- production of different classes of FPs as of 2019 were: (source)

*PTFE dominates the market while FEP is expected to increase much faster than other FPs. - Per Rupesh’s question above - in one of the attached documents, under Photovoltaics, it was mentioned that the PVDF and PVF (Tedlar by Dupont) are the two commercially available candidates. So, yes there are two variants and the consumers/customers will have to pick from one of those two. On Arkema’s website, it is stated that their PVDF is better as they have a higher content of Fluorine in it.

- Kynar® 3-Layer PGM TR Film: ~59% fluorine in outer layer

- Generic PVDF Films: <50% fluorine and

- Typical PVF Films: < 41% fluorine. Link: Photovoltaic Was curious to find what GFCL had as its Fluorine content in its PVDF, could not find it clearly.

Was going through a few of the competitors out there globally who have a say in the products that GFL manufactures/caters to, to see if they have any Capex plans, what they are saying about the opportunities etc. Below are my notes on Dongyue, Chemours and Arkema: (not exhaustive by any means).

Dongyue Group:

- During 2020, the Group has completed the R125 expansion project for the refrigerants segment to cope with the growing market demand. During the period, Future Hydrogen Energy completed the first phase of the new proton exchange membrane (PEM) production line, with a production capacity of 500,000 m2, which is now in operation, providing a guaranteed basis for the future marketization of Future Hydrogen Energy’s proton exchange membranes.

- In terms of fluorinated polymer materials, the Group is constructing 20,000- ton PTFE scale expansion project, which can cope with the current market environment of PTFE supply shortage.

- it is expected that the first phase of the project, a 10,000- ton polytetrafluoroethylene plant, will be completed in 2021, which will increase the Group’s production capacity of polytetrafluoroethylene by 25% upon completion

- The projects under construction also include a 5,000-ton FEP project that will double the Group’s FEP production capacity upon completion

- a 2,000-ton PFA project that can significantly increase the Group’s production capacity for high-end fluoropolymers at a high price level and will create substantial revenue and profit for the Group upon production and market launch

- the Group will conduct further in-depth research and development on the four major industries of fluorine, silicone, membrane, and hydrogen to extend to the high-end of the industrial chain and promote the application of fluorosilicone materials in 5G, new infrastructure, new energy, and other areas

- Although the Group has a huge production capacity of R22 and is significantly affected by the quota system, the Group has used the saved production capacity of R22 to the production of fluoropolymer in order to cope with the increasing market demand for fluoropolymer, as R22 can be used as raw material for the production of fluoropolymer. With respect to the shortfall in the refrigerants’ market after the phase-out of R22, the Group had strategic deployment to respond to the shortfall and the Group would continue to strive to strengthen its position as the world’s largest producer of refrigerants. The Group has the largest production capacity of R22 in the world.

- Over the years, Shandong Dongyue Chemicals Co., Ltd., a subsidiary of the Group, has a worldwide reputation for providing high-quality products, leading the market with its primary products, green environmental refrigerant, which ranked first in terms of size, technology and market share over the world; and it is an excellent supplier to domestic and overseas famous enterprises including DuPont, Daikin, Mitsubishi, Haier, Hisense, Gree, Midea and Changhong.

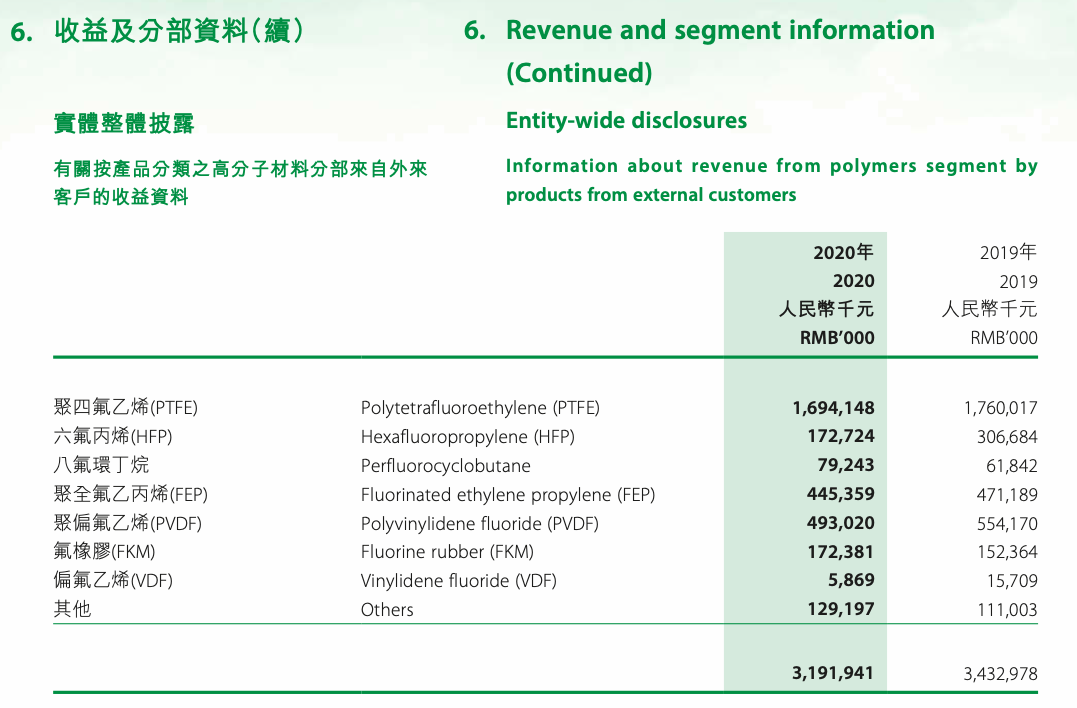

Segment wise break up for Dongyue:

The Chemours:

- We now manage and report our operating results through four reportable segments: Titanium Technologies, Thermal & Specialized Solutions, Advanced Performance Materials, and Chemical Solutions. Thermal & Specialized Solutions (formerly Fluorochemicals) and Advanced Performance Materials (formerly Fluoropolymers).

We divided our Fluoroproducts segment into two new reportable segments—Thermal & Specialized Solutions (TSS) and Advanced Performance Materials (APM). - Our Thermal & Specialized Solutions (TSS) segment is a leading, global provider of refrigerants, propellants, blowing agents, and specialty solvents. has held a leading position in the fluorochemicals market since the commercial introduction of FreonTM in 1930.

- Our TSS segment competes against a broad variety of global manufacturers, as well as regional manufacturers in the Asia Pacific. We have a leadership position in fluorine chemistry and materials science, broad scope and scale of operations, market-driven applications development capabilities, and deep customer knowledge. Key competitors for the Thermal & Specialized Solutions segment include Honeywell International, Inc., Arkema S.A., Orbia, and Daikin Industries, Ltd.

- Developed markets represent the largest consumers of fluorochemicals today. Global middle-class growth and the increasing demand for automobiles, refrigeration, and air conditioning are all key drivers of increased demand for various fluorochemicals.

- The primary raw materials required to support TSS segment are fluorspar, sulfur, ethylene, chlorinated organics, chlorine, and hydrogen fluoride. These are available in many countries and are not concentrated in any particular region. We pursue maximum competitiveness in our global supply chains through favorable sourcing of key raw materials. Our contracts typically include terms that span from two to 10 years, except for select resale purchases that are negotiated on a monthly basis. Qualified fluorspar sources have fixed contract prices or freely-negotiated, market-based pricing. We diversify our sourcing through multiple geographic regions and suppliers to ensure a stable and cost-competitive supply.

- Our Advanced Performance Materials segment is a leading, global provider of high-end polymers and advanced materials - as a diversified portfolio that includes various industrial resins, specialty products, membranes, and coatings. Serves a broad range of markets, including consumer electronics, semiconductors, digital communications, transportation, energy, oil and gas, and aerospace, among others.

- Our APM products are sold under the brand names Teflon, Viton, Krytox, and Nafion. Teflon coatings, resins, additives, and films serve as the key underpinning for a variety of industrial and commercial applications, including semiconductor infrastructure. Viton fluoroelastomers are used in automotive, consumer electronics, chemical processing, oil and gas, petroleum refining and transportation, and aircraft and aerospace applications. Our Krytox-branded lubricants are used in a broad range of industrial applications, including bearings, automotive friction management, and electric motors. Nafion membranes are critical components in chlor-alkali processing and flow batteries, as well as the hydrogen electrolyzers and fuel cells which underpin the hydrogen economy. Key competitors for this segment include Daikin Industries, Ltd., 3M Company, Solvay, S.A., Asahi Glass Co., Ltd., and Dongyue Group Co., Ltd.

- The primary raw materials required for the Advanced Performance Materials segment are chlorinated organics, hydrogen fluoride, and vinylidene fluoride.

Could not find info on all their plant capacities easily. above is just my notes from their AR and recent conf calls

Arkema:

-

Over the years, the Group has built up unique expertise in materials science, in terms of bonding, coating, and substituting traditional materials with lighter, more sustainable and more efficient ones. Arkema has regrouped these skills into its three Specialty Materials segments (which is roughly 80% of Sales)– Adhesive Solutions, Advanced Materials and Coating Solutions – and in April 2020 presented its ambition to become a pure Specialty Materials player by 2024. the fourth segment is intermediates which is roughly 20% of Sales & is cyclical in nature.

-

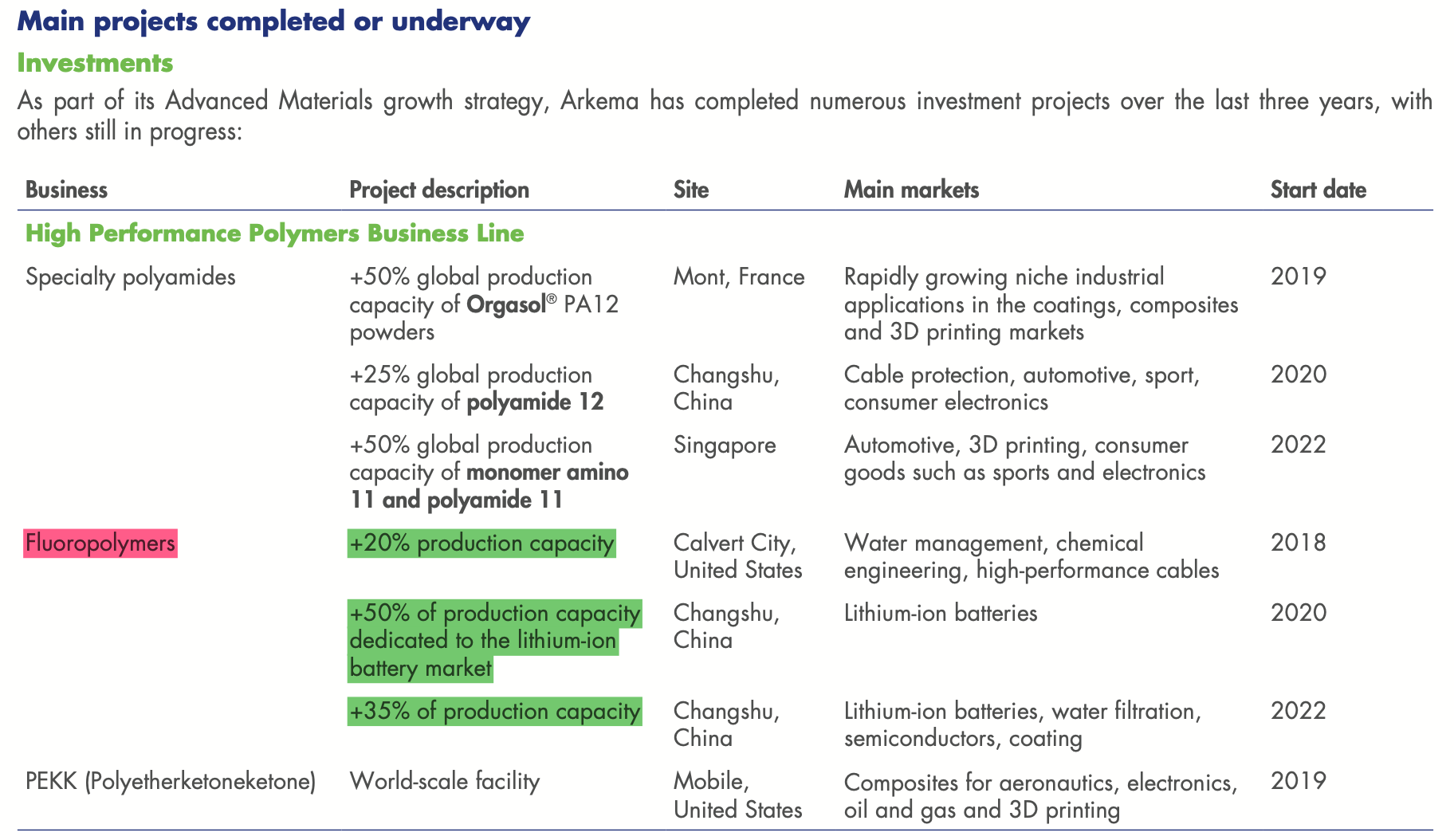

The Advanced Materials segment includes High Performance Polymers and Performance Additives - To develop this segment, the Group has made major industrial investments, notably in thiochemicals in Malaysia, PVDF in China and molecular sieves in France, as well as some acquisitions, in particular ArrMaz. Last year, we were also able to move forward with our growth investments, including the start-up of the methyl mercaptan unit in Malaysia, the new adhesives plant in Japan, and increased PVDF production capacity in China dedicated to the battery market.

-

the Group aims for recurring capital expenditure to average around 5.5% of sales per year, with around 40 to 45% dedicated to growth projects.

-

The US$150 million investment announced as part of the partnership with Nutrien to produce anhydrous hydrogen fluoride, the main raw material for fluoropolymers and fluorogases, which will be carried out by Arkema at Nutrien’s site in the United States. Start-up of the unit is expected in 2022.

-

In 2020, R&D expenditure totaled €241 million, representing 3.1% of Group sales. R&D expenditure as a percentage of sales varies between businesses. It is higher in specialty areas and particularly in the Advanced Materials segment, where R&D helps find solutions for customers and respond to the major sustainable development trends. Arkema’s R&D teams comprised more than 1,600 researchers in 2020, spread across three regional research and innovation hubs.

$ 10% for the corporate research program - research efforts on high potential cross-functional areas such as batteries, composite materials and hydrogen storage;

$ 39% for the Advanced Materials segment - In the field of polymers, the Advanced Materials segment’s R&D develops polyamides, PVDF and PEKK for the lightweighting of structures by substituting metal parts with thermoplastic composites in the automotive or aerospace industry, and are used for new production techniques such as 3D printing which enable optimal design of complex parts. -

Solutions for batteries -

The Kynar® fluoropolymer, for example, is used in the main components of lithium-ion batteries – in the electrodes as the binder for the active phase and as a protective coating for the separator. These products play a very important role in the battery’s lifespan and performance. They are therefore the focus of continuous innovation. Lithium salts, synthesized from the Group’s various chemistries are also used inside batteries, to move lithium ions from one electrode to the other. Battery manufacturers need lithium salts, like the Foranext® electrolyte, that can withstand the increasingly demanding conditions of use, including high temperatures and rising electrochemical potential. -

Materials for photovoltaic cells -

Photovoltaic cells are made up of a number of highly technical organic materials that protect the silicium layer from outside elements. Arkema harnesses its performance materials expertise to bring to this market a large number of innovations, such as: -

Apolhya® grafted polyolefins, which are used for the encapsulation or protection of photovoltaic cells;

-

Kynar® fluoropolymers, for backsheet protection; and

-

Bostik Vitel® polyester adhesives, which are used for binding photovoltaic backsheets.

-

Electronics solution platform - its fluorinated electroactive polymers (Piezotech®) caters to electronics segments, such as organic, flexible and printed electronics. - making them central to the development of next-generation sensors (pressure, deformation, infrared, etc.), actuators (haptic, medical, microfluidic, etc.) and flexible transistors for use in various next-generation products such as screens, solid-state cooling systems, energy recovery systems, printed loudspeakers, etc

- Certain Foranext® high-purity fluorinated intermediates play an important role in the various stages of the manufacture of semi-conductors, where they are used to selectively eliminate matter through plasma etching.

-

Following the start-up in December 2020 of a 50% expansion of fluoropolymer production capacity for battery applications at its Changshu site in China, Arkema announced on 23 February 2021 that it was again investing in this site to increase capacity by a further 35%. The new expansion, which is scheduled to come on stream before the end of 2022, will notably serve the fast-growing lithium-ion battery sector, as well as the water filtration, construction, and industrial coatings and semiconductor markets.

-

Moreover, on 7 June 2021, Arkema announced plans to develop the supply of 1233zd, a new generation of fluorospecialties with no or minimal emissive impact, to support increasing market needs for sustainable solutions in insulation materials and in an emerging application in batteries for electric vehicles. As part of these plans, an agreement to manufacture 1233zd in China was finalized with Aofan, whose initial production capacity of 5 kt/year is expected to start mid-2022. At the same time, Arkema will accelerate its detailed planning of 15 kt/year capacity at its Calvert City site in the United States, which is expected to start end-2023 for an estimated investment of US$60 million.

-

volume growth: Continued strong growth in batteries, consumer goods, electronics, and transportation. Volumes up 13.3% YoY Strong increase in High-Performance Polymers volumes, in particular in batteries, sports, and bio-based consumer goods.

-

To support the exponential growth in demand for lithium-ion battery cell materials in Europe, Arkema also announces a 50% expansion of its Kynar® fluoropolymer production capacity at its Pierre-Bénite site. These polymers are used as separators coatings or as cathode binders. New innovations and product ranges will also be offered, such as Kynar® CTO, the new Kynar® PVDF made from renewable sources. This new extension should come on stream in the first quarter of 2023. (Arkema accelerates its investments in batteries)

-

Jan 21,2022 - Due to strong demand for lithium-ion batteries, and other important markets, Arkema’s previously announced 35% fluoropolymer capacity increase at its Changshu site in China is now revised upwards to a capacity increase of 50%, with no change in the expected start-up date (end-2022).

-

With this PVDF capacity increase, Arkema accelerates its development in China in order to meet the strong demand from its partner customers in the lithium-ion battery business and support the significant growth in the water filtration, specialty coatings, and semiconductor sectors. Arkema, a global leader in PVDF production, also recently announced a 50% PVDF capacity increase at its Pierre-Bénite site in France, which is scheduled to come on stream in the first quarter of 2023.

-

7 capacity expansions in the last 10 years. ( from their quick 15 min webinars on Electrode binder solution and Separator coating solutions ) link: PVDF Solutions for Lithium Ion Battery

I will share in another post on Daikin, AGC, and Solvay shortly.