Some data to chew about PVDF; size of opportunity (ballpark estimate), applications, growth, etc -

- The downstream applications of PVDF are in weather-resistant coatings (31%), injection molding (21%), lithium battery cathodes and separators (20%), and photovoltaic backplanes (8%).

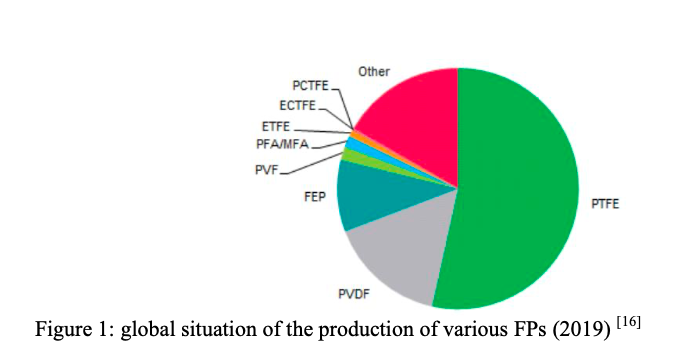

- The total global production capacity of PVDF is about 114,000 tons, of which the combined production capacity of overseas (read ex-China) companies Arkema, Solvay and Kureha Chemical accounted for 53%.

- Dongyue Group of China currently has a production capacity of 10,000 tons of PVDF. Except for the 8,000-ton new capacity of Shandong Huaan New Materials (of China), a subsidiary of Lianchuang, which was put into production in the second half of this year, most of the remaining new capacity is still in the EIA stage and is expected to be released after the end of next year.

Source: https://min.news/en/economy/e2cdc7552f9010388a45bb1a4702f686.html

- Among the several major uses of PVDF resin, the proportion of the lithium battery market has increased significantly from less than 10% two years ago to 19.90%, and with the huge development of new energy vehicles, the proportion will increase.

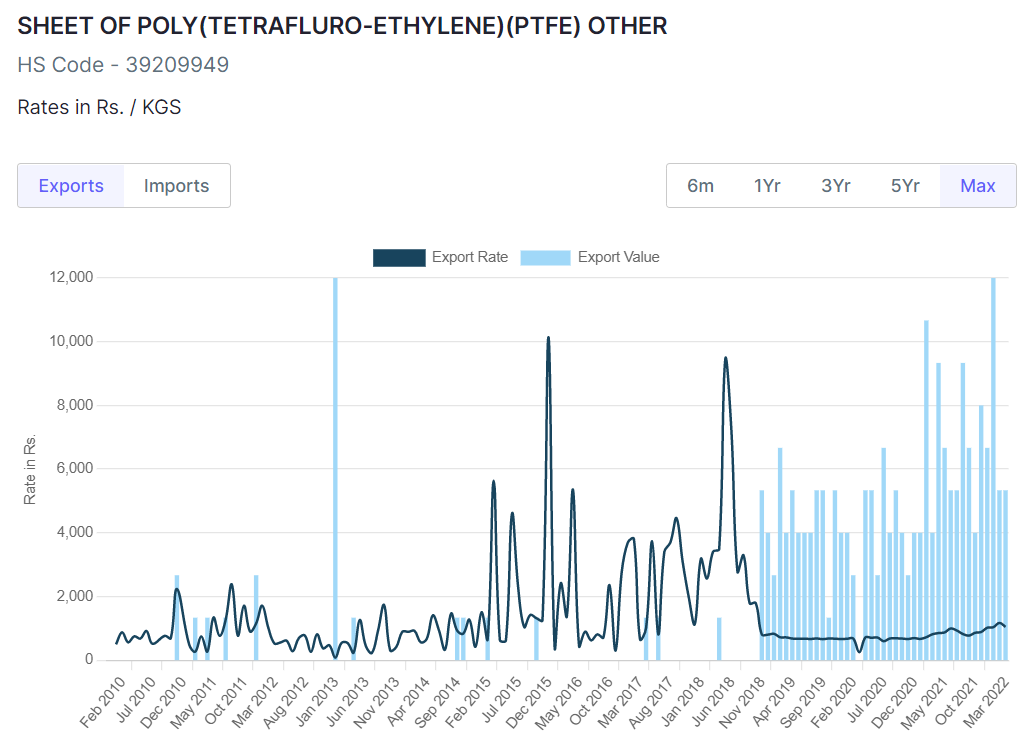

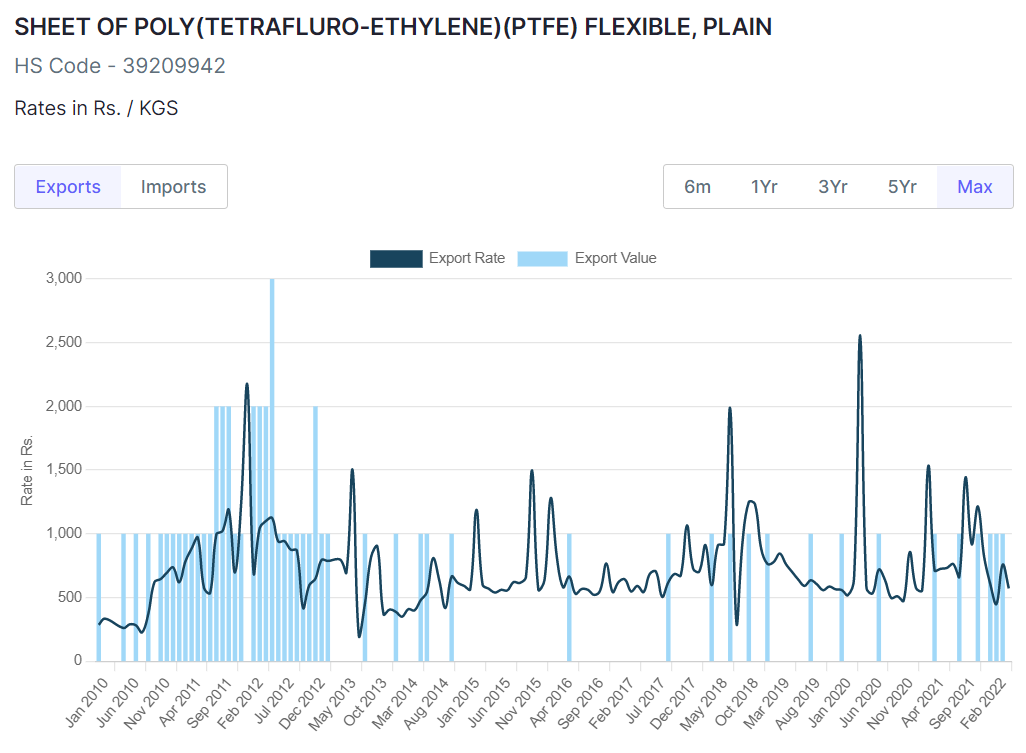

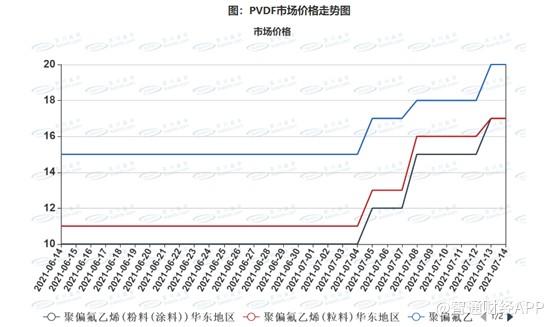

- The ex-factory price of R142b (raw material for PVDF) has risen from 15,500 yuan/ton in Oct 2020 to the 38,000 yuan/ton in Apr 2021, an increase of 145%! This is because of increase in demand and implementation of quota production. 1 ton of PVDF needs about 1.62-1.67 tons of R142b.

- The demand for PVDF resin (in China) is as high as more than 50,000 tons! At present, the total production capacity of all domestic (China) PVDF resin manufacturers is not 50,000 tons! Due to the rapid development of global new energy vehicles, the use of lithium batteries for PVDF resin has increased sharply. Global lithium battery giants CATL, BYD, Panasonic, LG, etc. have seized PVDF resin production capacity globally, resulting in a tight supply of PVDF resin in all industries , And the expansion cycle of PVDF resin is about 3 years, seriously lagging behind the growth rate of demand for lithium batteries.

Source: With soaring raw materials, where does the fluorocarbon coatings market go?

(April 2021 article)

Snippet about PVDF from GFL latest investor presentation (here) -

- Few new PVDF grades (mainly for EV batteries) developed are in the process of customer qualifications

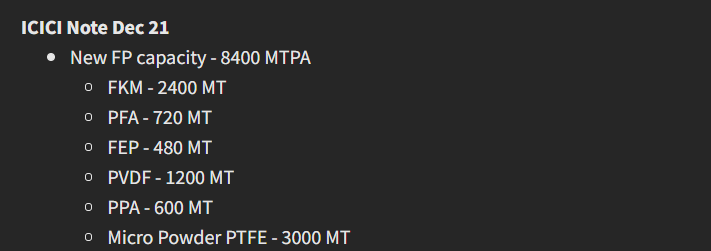

- There is substantial increase in demand for FKM, PVDF and Micro Powders. Additional capacities for these products are under installation and commissioning.

- Prices for FKM and PVDF have moved up due to rising demand and cost push of key raw material R-142B.

- GFL is backward integrating to produce R-142B for captive feedstock requirements for FKM and PVDF as well as for exports.

- GFL is in the process of setting up an integrated battery chemicals complex. In addition, GFL has developed suitable PVDF grades for cathode binder application.

- GFL is setting up India’s first PVDF solar film project which will be commissioned in the next financial year.