FLUOROCHEM, Monthly - This business got demerged out of erstwhile GUJFLUORO (currently GFL post demerger) in 2019 and has taken 18 months to go past the price it listed at post demerger. It has broken out of that on the monthly with strong volumes last month.

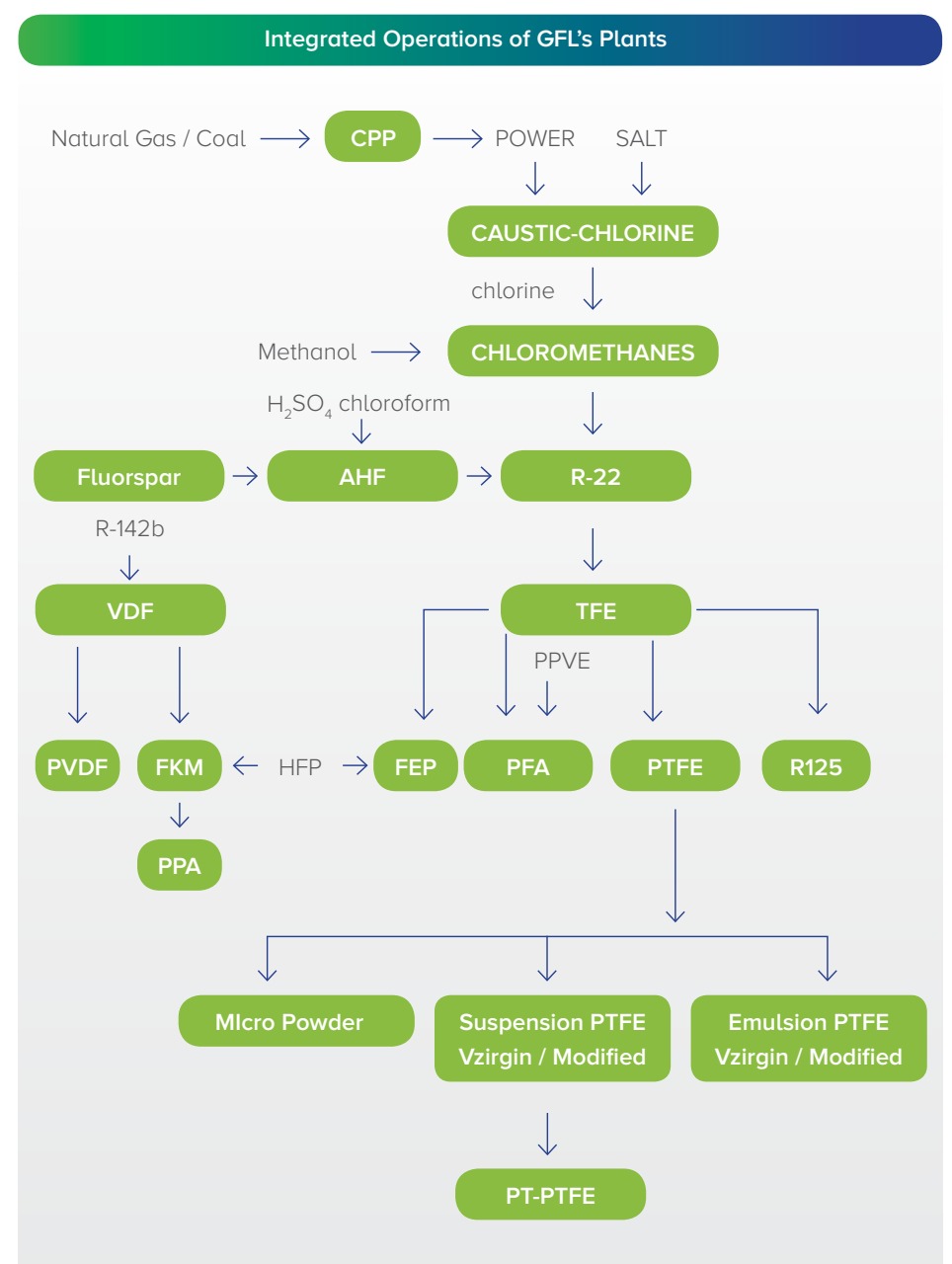

Fundamentally, the business is well covered in the Gujarat Fluorochem thread. The management seems to have demerged the specialty chemical business on purpose and appears to be more focused on the same going by the EC filings requesting clearance for almost 150 products, most of it for various fluoropolymers, end products of fluoro polymers like HDPE drums, LDPE liners, PVDF membranes, fluoro specialty chemicals in the pharma and agrochem space (some of the trifluoromethyl molecules -CF3 seem to have several applications in pharma drugs), LiPF6 which finds application as an EV battery electrolyte etc.

The valuation is almost on par with a peer like SRF but is way cheaper than a Navin Fluorine. I believe this lies somewhere in the middle and as the Fluoro specialty chemicals and fluoropolymer value-added product contribution increases (around 20% at present), the valuation multiple has lot of headroom to approach Navin Fluorine on a relative basis.

Some parts of the last concall (June '20 is the latest and there doesn’t appear to be one after it) I thought added more information on near-term dynamics of the business which should improve the margin profile.

This is where management was saying most of the contribution will come from value-added PTFE, fluoropolymers and fluorospecialty chemicals

A lot of contribution seems to come from auto so a near-term upcycle in auto can contribute to better numbers in fluoropolymers (wire sheathing, dashboard plastics, gaskets, o-ring)

Current capacity can contribute to an EBITDA of 1200 Cr

This was the interesting part where there was a sort of a guidance on fluoropolymers (170 Cr to 700 Cr) and fluorospecialty chemicals (180 to 600 Cr) - Almost four-fold and three-fold increase

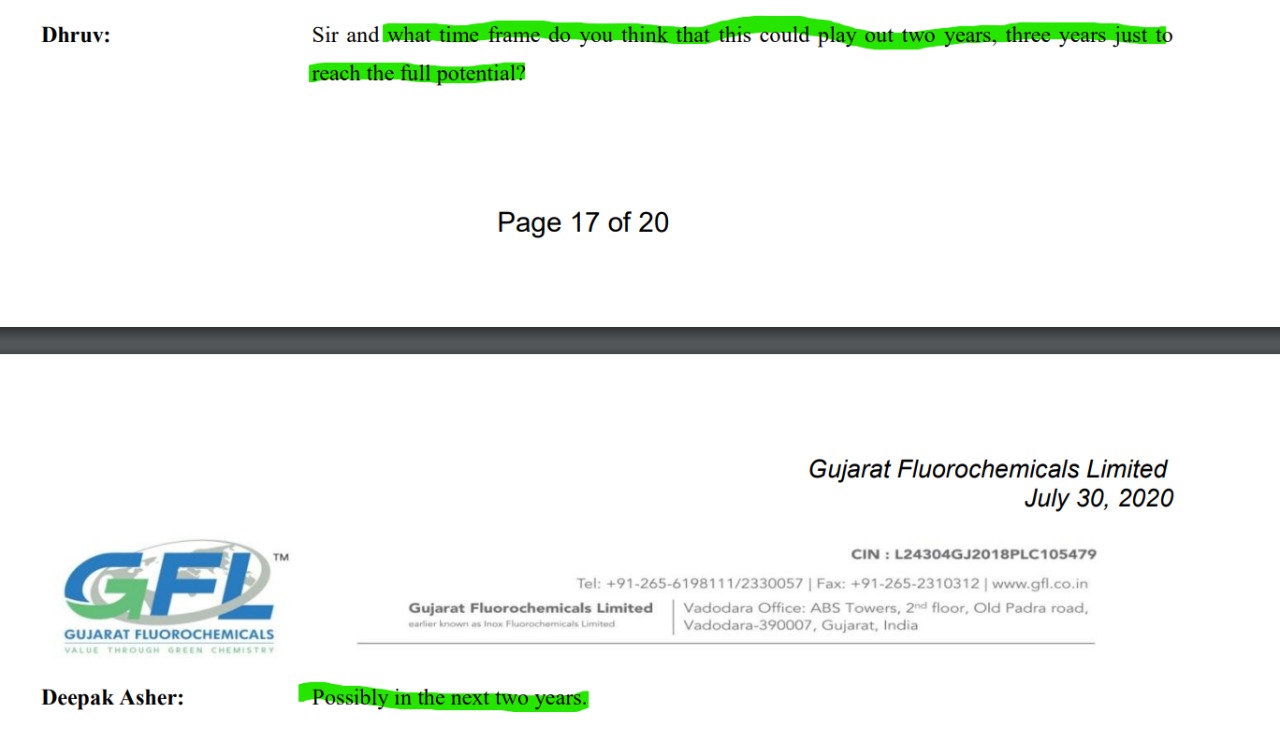

In a timeframe of 2 years

This could be a China+1 play. Management could also be looking at non-Fluorine chemistry for future growth.

Another interesting part in the above was the efficacy of fluorinated molecules in drug delivery. I checked this and there were couple of research articles on nature here and here. The latter especially speaks about trifluoromethylation (-CF3) and the complications in creating such molecules. There are several such molecules in the EC filing, so the company seems to have a strong R&D capability.

This is a true blue specialty chem company, taking basic RMs like fluorspar (from captive mine in Morocco), coal & gas for power, sulphuric acid, methanol and common salt and producing multi-step chemistry value-added products and intermediates.

Posting these here since the VP thread is for Collaborators only. Apologies as the technical analysis in this post is perhaps too little.

Disc: Have positions around 1200 after reading the VP thread and doing some own research