Gufic receives approval from NMPA, China for Prilocaine API

ff6466b7-fa92-48d5-afd7-e4337d33fb39.pdf (291.9 KB)

Gufic receives approval from NMPA, China for Prilocaine API

ff6466b7-fa92-48d5-afd7-e4337d33fb39.pdf (291.9 KB)

Hi all,

I was trying to analyse this company. It looks like the company does not gives segment wise results, they just publish a pie-chart. How do you analyze the segment wise numbers, any particular way or just a rough estimations?

| Manufacturing Facility | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Unit-1 (Navsari) | Botulinum Toxin Facility, Lyophilized/Powder Injectables Facility, Natural Products (Topical/Liquid), API Facility | |||||||||||||

| Product | Capacity | |||||||||||||

| Lyophilized | 18 mn vials p.a | |||||||||||||

| Ampoule | 12mn p.a | |||||||||||||

| Ointment | 6mn tubes p.a | |||||||||||||

| Lotion | 6mn bottles p.a | |||||||||||||

| Syrup | 6mn bottles p.a. | |||||||||||||

| PFS | 2.8mn PFS p.a. | |||||||||||||

| Unit-2 (Navsari) | Lyophilized Injectables Facility, Capability to manufacture Liposomal Amphotericin B and Depot Injections (This is EU approved) | |||||||||||||

| Product | Capacity | |||||||||||||

| Lyophilized | 30mn vials p.a. | |||||||||||||

| PFS | 30mn PFS p.a. | |||||||||||||

| Belgaum Facility | Natural Products Facility | |||||||||||||

| Product | Capacity | |||||||||||||

| Capsule | 60 mn p.a. | |||||||||||||

| Powder | 3.6 mn p.a. | |||||||||||||

| Unit-3 (Indore) | Lyophilized/Powder Injectables Facility, Capability to cater to regulated markets such as US & EU |

|||||||||||||

| Product | Capacity | |||||||||||||

| Lyophilized | 36 mn vials p.a. | |||||||||||||

| PFS | 15mn PFS p.a. | |||||||||||||

| Liquid Injections | 60mn units p.a | |||||||||||||

| Penem Block (Navsari) | Dedicated facility for Penem Carbapenems (Lyophilized / Dry Powder Inj / Oral Solids / Dual Chamber Bags) | |||||||||||||

| Product | Capacity | |||||||||||||

| Lyophilized | 3mn vials p.a. | |||||||||||||

| Dual Chamber Bags | 24 mn IV bags | |||||||||||||

| Dry Powder Inj | 30 mn Vials |

Penem Block in Navsari commercialised in the recent quarter, and the Indore plant is expected to commercialise operations by Q2FY24.

Disclosure: Invested

You seem to have research this very well ( especially how well versed you seem to be with names of the formulations). A few questions:

The best question Common Stocks and Uncommon Profits ( one of the all-time-great investment books) asks companies:

What are you doing that your competitors aren’t, yet ?

For Gufic, it was lyophilised injectables at one time where the industry seems to now moving. In the future what do you think that it could be?

They spend 8-10% of revenue in R&D but judging future R&D is perhaps too difficult for a lay investor. (Scuttlebutt HELP!). What factors does this community think it could be for Gufic to give better growth than the industry?

Q1-FY2024 call notes

Personal comment:

CEO Pranav is well versed with the pharma knowledge, strategy, and qualitative aspects of opportunities they are chasing. He refers Mr Rongta (CFO perhaps) for all questions that involve quantitative aspects. (No comments or judgement. Just an observation)

FY23 annual report notes

Long term aim

New product development, launches & R&D

Company developments

Capex (187.6 cr. vs 87.45 cr. in FY22)

Geographical segment & financials

Exports to 20+ countries, 190+ products with 150+ products under pipeline in 40+ countries

Received 4 new international approvals from Columbia, Uganda and Ecuador

Key markets: India, Germany, Switzerland, South Africa, Russia, Canada, Brazil, Europe

Sales returns: 110.2 cr. (vs 68.95 cr. in FY22)

Sales return provision: 6.4 cr. (vs 7.6 cr. in FY22)

Geographical breakup

No Single Customer accounted for 10%+ of revenues in FY22 and FY23

Forex

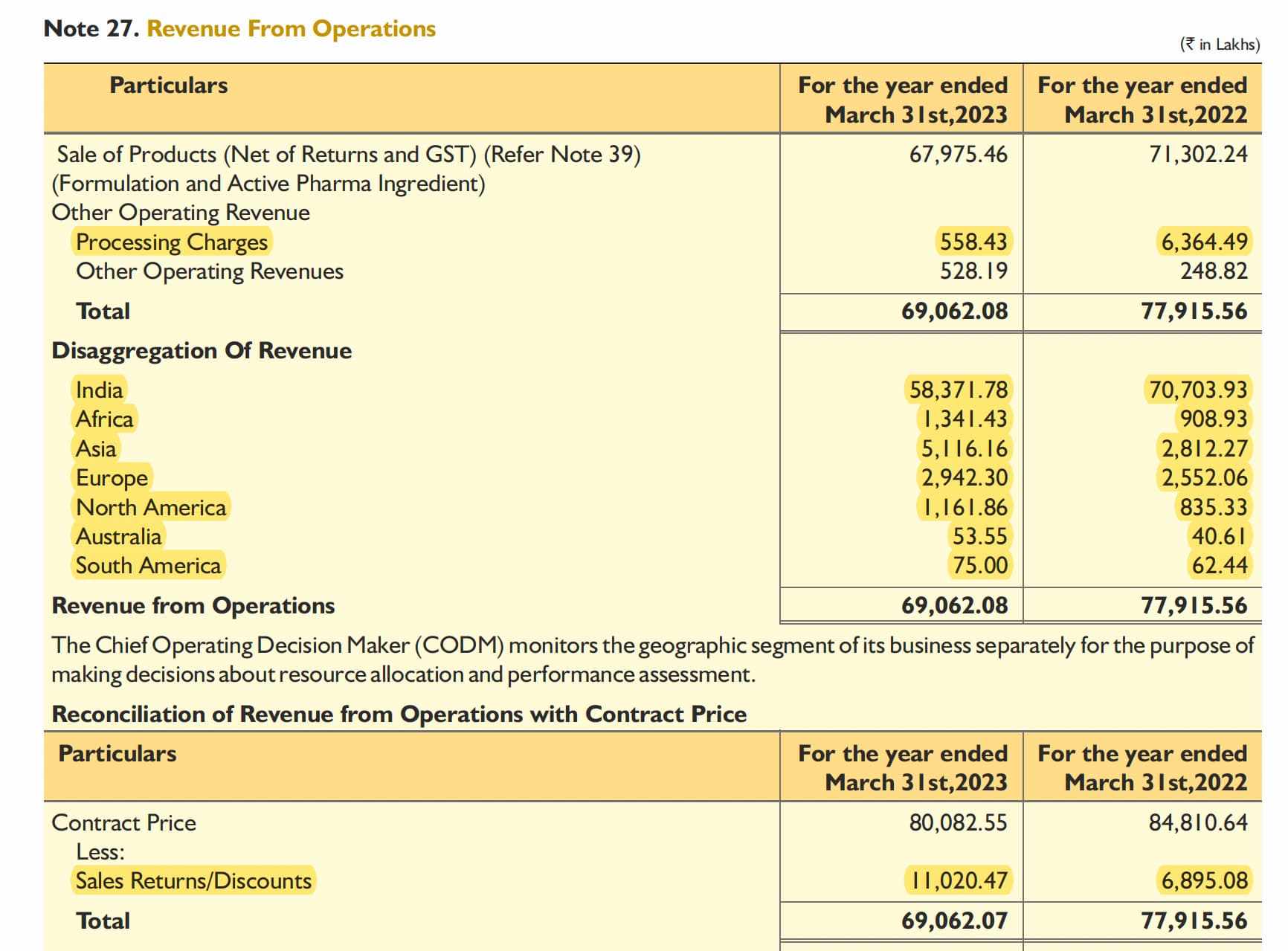

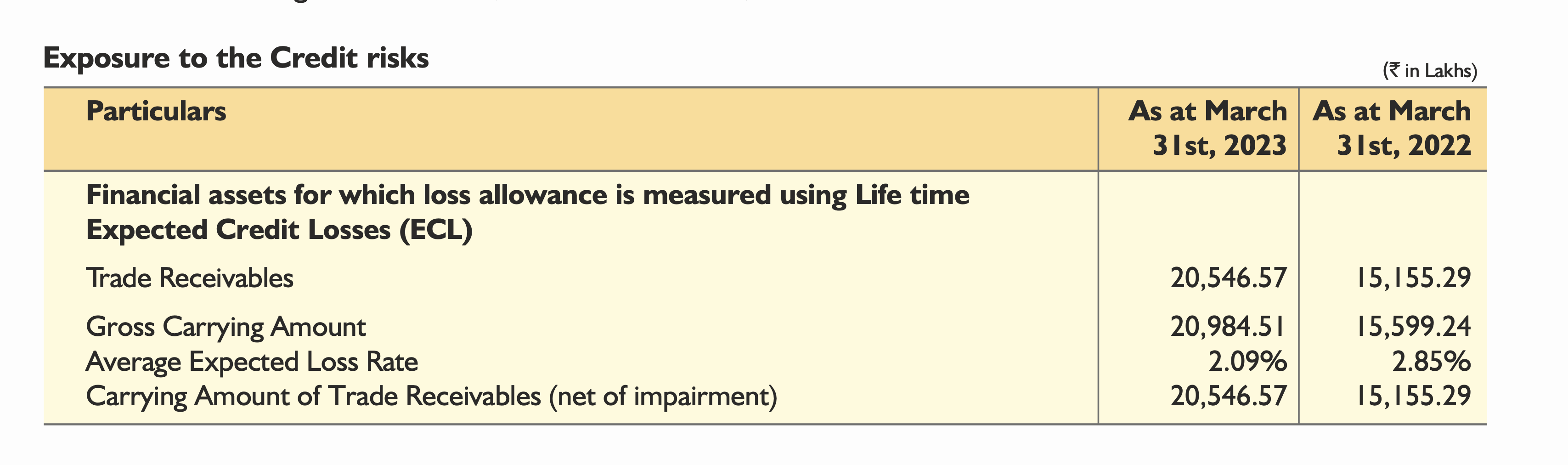

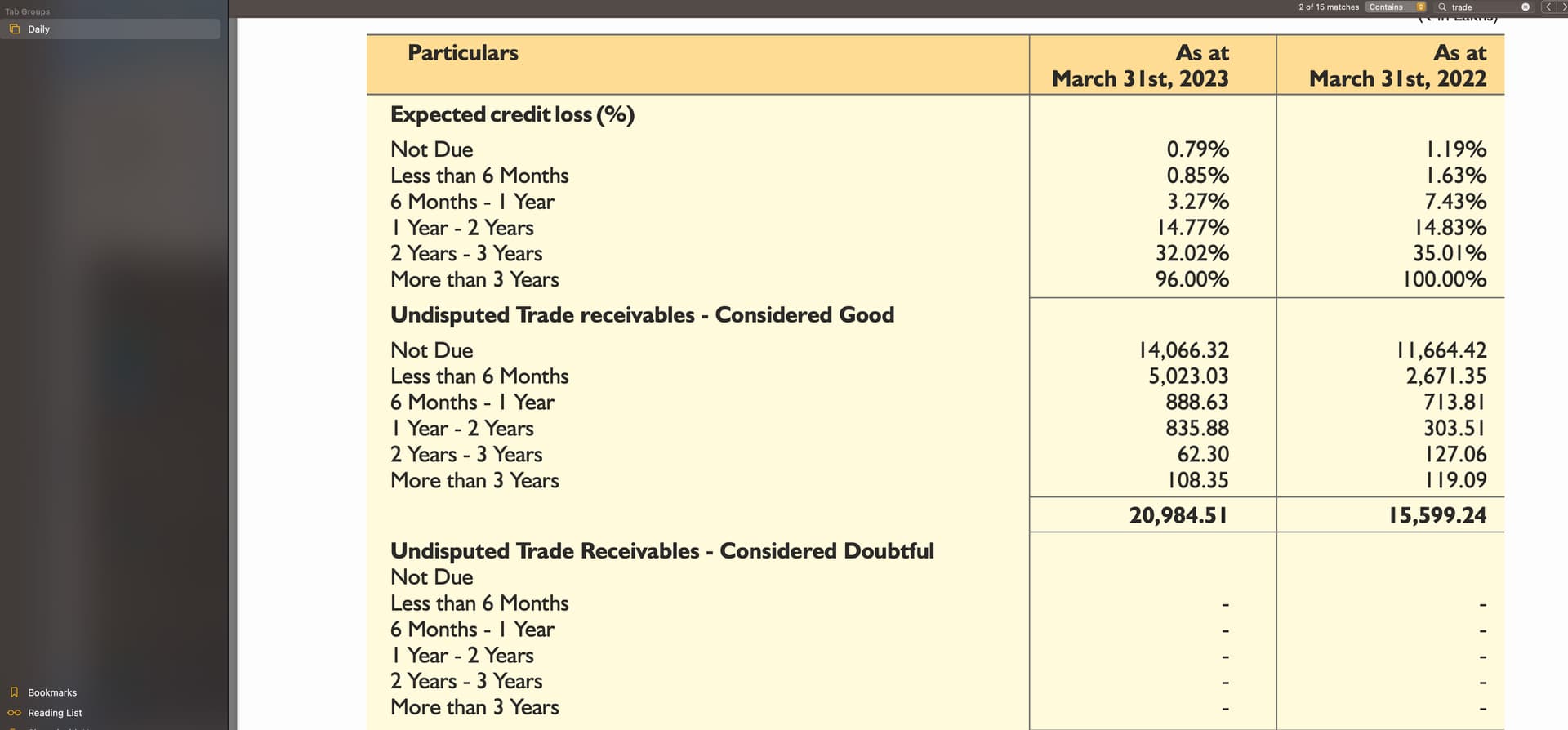

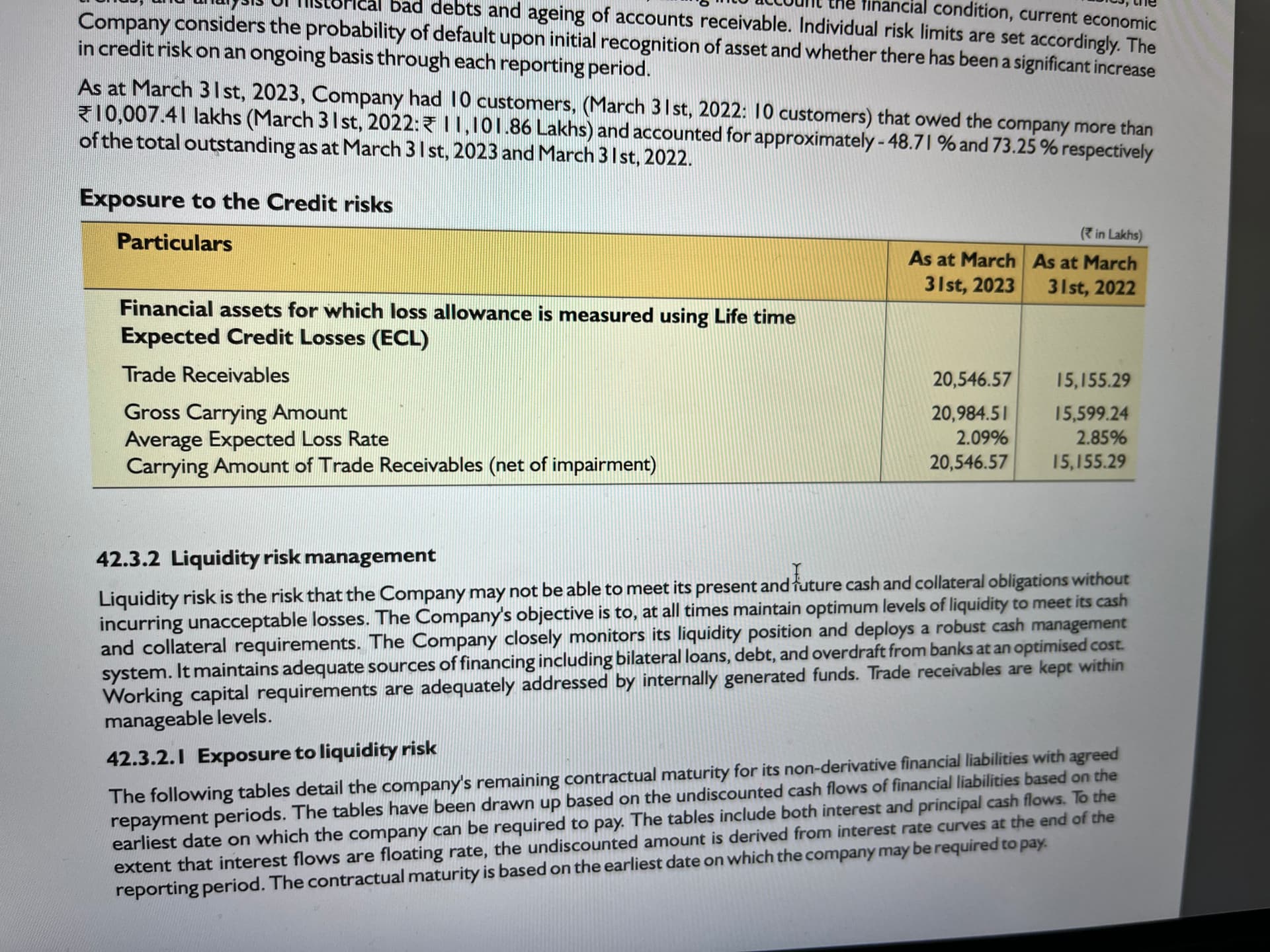

Trade receivables (huge red flag): impairment of 69 cr. (vs 39 cr. in FY22)

Credit risk increase: In FY23, they had 10 customers (same as FY22) that owed them 100 cr. (vs 111 cr. in FY22) and accounted for 48.71 % and 73.25 % respectively

Miscellaneous

General trends

India’s drug pricing authority sanctioned 12.1% price increase for scheduled drugs

Over 60% of APIs are procured from foreign sources, with certain APIs exhibiting import dependency rates of 80% to 90%

500 Indian API manufacturers contributing about 8% in global API Industry

India supplies 20% of generics globally

Indian Pharma Industry had growth of 7% in 2022 with market size of Rs. 1.94 cr. Chronic therapies grew by 9% and acute therapies by 5%

IPM has grown at a CAGR of ~11% in domestic and ~16% in exports over last 2 decades

Disclosure: Invested (position size here, no transactions in last-30 days)

Need to see credit impairment with these two data points . ECL has not gone up much & Need to get clarity from management but receivables are still in considered good bracket .there is a increase of 6 cr in dues past 6 months vs past year .

disc:invested

The second picture is important.

140cr is less than 1% default probability. Overall he expects 2.1% to be bad debts out of total debtors of 209.84cr. And it says Undisputed Trade Receivables - Considered Good, in Considered Doubtful the section is blank.

It is scarily presented by writing the words “Credit Impaired”, because only 1.08cr of debtors seems to be impaired at 96% default probability.

Rest of “credit impaired” debtors seem to have a much lower default probability rate.

He had also said in one of the concalls 2-3 qtrs ago that the working capital increase which has impacted cash flow will reverse in the coming FY, we should see positive OCF again in 6 monthly statement. Nevertheless we should ask about this in next concall to have 100% clarity. Hope this helps.

Average expected loss rate has decreased as a trend, still doesn’t answer what you pointed out and should be clarified on call.

But, as receivables took a jump, this might show the current average expected loss rate lower

Just an Observation

Gufic Biosciences was founded in 1970 as an injectable manufacturer (lyophilisation) and then exited API & formulations business by selling its top 6 brands to Ranbaxy in 1997. It re-entered formulation in 2007. It is a R&D focused pharma company (8-10% of revenue) whose business is distributed as such

Domestic Branded segment: 50% revenue with Gross margins 55-60%. Engaged primarily in critical care (life-death operation), Infertility, among others.

Contract Manufacturing (30% revenue contribution at 30% margins) of lyophilised formulations for all top pharma cos of India (one time 170cr topline jump in FY22 earnings for Remdesivir)

Exports (15% revenue contribution) to mainly developing countries and few developed markets like Germany and Switzerland

API (5% revenue contribution) 50% is captive consumption reducing dependence on Chinese APIs.

My understanding is the company primarily runs CMO business along with branded segments as cash cows to fund extensive R&D expenditure. Both father-son duo and rest of the management are experienced & educated in pharma. Son (CEO) studied at John Hopkins (World rank 1 in biotech).

Moat: Pioneering new technologies (drugs and drug delivery systems)

They have consistently brought new technology to India. Lyophilisation is the process of freeze-drying liquid injectable formulation to powder form for easy transport. They were pioneers in this tech but it is now a commoditized market so they are investing in scale- one of the largest lyophilisation capacities in the world. Similarly they are the only Indian co to have got a licence to handle Botulinum Toxin and made a product as effective as Botox (Very toxic).

Key Thesis Pointers

Company just finished a huge capex, new lyophilsation factory will start in September. Operating leverage will begin to play out and management consistently tries to do backward integration (captive API production, CEO mulled making plastic bags for dual-bag chamber tech in the future in concall).

Apart from core business growth in CDMO and branded segment, technology advancements can give pleasant surprises as company regularly brings new technology to India. As the pharma sector picks up again, institutional buying will be the real driver of stock price as it is an established name with competent promoters and track record.

Questions/Risks I’m evaluating

Disc: invested @270 (15% of portfolio)

Gufic Bio Company overview and Q1 FY 24 review -

Geographical revenue breakup (aprox)-

Domestic formulations - 50 pc

International formulations - 13 pc

CMO - 28 pc

APIs - 9 pc

Domestic business break up -

Critical care - 52 pc

Infertility division - 23 pc

Others - 27 pc

Critical care division-

Making a comeback post inventory liquidation in late 2022 & early 2023

Company has presence across 6000 hospitals with 92 molecules

Company to soon launch of Delbavancin (used against acute bacterial skin infections)-first company to launch it in India

Fertility Division-

Recently launched Human Menopausal Gonadotropin(HMG) - used to boost success in IVF cycles. Trials are on to establish company’s product efficacy vs Intl Mkt Leader

High growth continues in Dydrogestrone

Q1 FY 24 business highlights -

Gufican and Gufibis Oils ( orthopaedic oils for pain relief ) continue to gain Mkt share - can experience substantial growth going fwd

Successfully launched Zinc Based multivitamin tablets. Getting good Mkt response

Successful completion of split face trials of Stunnox (Botulinum Toxin - used in Chronic migraine, Spastic disorders etc) against the Mkt leader have yielded remarkable results - instilling confidence in the Doctors

Company Infrastructure -

Field force > 1000 ppl

Has one of the largest Lyophilisation capacities in India for CMO

Makes in-house APIs in- anti-fungal, Anti-biotic and Anesthetic therapies

International business spread across 20 countries - Europe, LATAM

Manufacturing facilities-02 at Navsari, 01 at Belgaum, 01 at Indore

Last 4 yr finances -

Sales CAGR - 18 pc

EBITDA CAGR - 31 pc ( margins up at 19.9 from 13.1 pc in FY 19 )

PAT CAGR - 38 pc ( margins up at 11.5 from 5.4 pc in FY19 )

Q1 FY 24 outcomes -

Sales - 195 vs 165 cr

EBITDA - 36 vs 33 cr (margins @ 18.6 vs 20.3 pc)

PAT - 21 vs 21 cr

Delbavancin - can be a good molecule as it has wide usages before Ortho / Cardiac surgeries. Priced in India at 1/5th the International prices. Can be a good revenue driver in 3-4 yrs in India

Can also be launched quickly in Intl Mkts

Dual Chamber Bags launch scheduled in Q2

Indore facility Capex to go live in Q3 FY 24 - should be a nice tailwind for CMO business

Share of exports in total sales currently at 18 pc of sales

Margin compression in Q1 due increased R&D expenses in Q1

Likely to grow 15-20 pc in topline, EBITDA this yr (bare - minimum)

Likely to maintain 19-20 pc EBITDA margins this yr

Disc: not invested. Intend to buy. Biased. Not SEBI registered

I attended Gufic’s AGM where some of my earlier highlighted concerns got clarified. I have highlighted them below.

As a side note, Pranav Choksi’s energy is contagious. I think he went on for more than 1.5 hours talking at length about their plans, and answering each question with incredible detail. This guy is crazy passionate!

Its incorrectly mentioned in AR, anything beyond 60 day receivable is mentioned in credit impaired. Actual impairment is very low.

Gave extra credit to sell covid products

Sales returns only happen in domestic business (& not in contract manufacturing or exports). 4-5% average sales returns in domestic business (2-3% product due to damage + 2% sale returns which are then resold to other customers). So overall ~3% is sales returns in normal scenario

Split between divisions

Management also shared their thoughts on how they approach the hospital business, which I found pretty useful. They categorize hospitals into 1) primary – single doctor (25-50 beds), 2) secondary 75-100 beds, and 3) tertiary – large hospital chains. In terms of segments, they categorize by

What is very interesting is they are directly reaching out to hospitals and will sell via their own direct channel where they get a daily idea about demand from individual hospitals. In a way, they want to be a 1-stop provider for all hospitals.

Currently, around 180-200 people are promoting their products via hospital channel.

Miscellaneous

Disclosure: Invested (position size here, no transactions in last-30 days)

Decent Set of results.

Receivables continue to be stretched, and the reason was explained in the last call, however expect them to work on their working capital.

Indore plant should start this month.

Any other opinion on the results are welcomed to understand better

Dics: Invested and biased

Gufic Bio - Q2 and H1 highlights -

Q2 financials -

Sales - 215 vs 175 cr

EBITDA - 40 vs 33 cr ( margins at 18.5 vs 19 pc )

PAT - 23 vs 20 cr

Domestic business - has 8 business units with a field force of > 1000 ppl. Products cover 15 therapeutic areas

CMO business - 50+ products, one of the largest lyophillization capacities in the world

APIs - specialises in anesthetics, Anti-Fungals, Anti-Biotics

International business - exports to over 20 countries

Current facilities -

Unit -1 Navsari - makes Ampoules, Ointments, Lotions, Syrups, Lyophilised powders, PFS (pre filled syringes)

Unit -2 Navsari - Lyophilised powders, PFS

Gufic Belgaum - Oral Solids - natural products

Upcoming facilities -

Unit - 3 Indore - Lyophilization, PFS

Completion by Sep 23, revenue contribution from Q3

Penem Block - Dedicated facility for Carbapenems (lyophilised, oral solids, dual chamber bags, dry powder)

Botulinum Toxin facility at Navsari - to make Botulinum toxin API and formulations in partnership with Prime Bio, USA ( used in Pain management , Derma and Neurology )

About 50 pc of company’s revenues come from Domestic business. Critical Care + Infertility care form about 70 pc of domestic business ( 45 + 25 pc each )

About 30 pc sales are from CMO business with 10 pc sales each from Intl and API business

Company has received DGCI approval for launch of Delbavancin ( used in acute skin and bacterial infections ) in India. Seeing good traction

Company sells to 50 pc of all IVF clinics in India

Company’s SPARSH division - has been set up to do the business like a wholesaler of 92 + molecules based Injectables to over 1000 hospitals in India. Currently, this division has a field force of about 40 ppl and is doing a business of about 3-4 cr/month. Expecting a good ramp up in the Sparsh division

Also launched SeraSeal under the SPARSH division. It’s an innovative homeostatic agent aimed at stopping bleeding on contact. Finding wide acceptance

Dydrogesterone ( infertility product ) - grew 20 pc QoQ in Q2. Sales expected to double in this FY

Company conducting trials for its own HMG ( human menopausal Gonadotropin ). It increases the success rate of IVF cycles. Trials are on vs established international player’s product

Q2 growth mainly led by Domestic mkt that’s doing much better

Rs 100 cr were raised by the company via preferential allotment. The same shall be used for Debt repayment

Deterioration in working capital cycle due - CMO business pick up and launch of SPARSH division where the payments are received from MNCs / Hospitals only after 90-120 days

Disc: holding, biased, not SEBI registered

Gufic came with good set of nos, with sales growing by 23% and EPS by 15%. They have been doing very well in domestic market, with broad based growth across their keys division. Working capital seems to have normalized to precovid levels. Concall notes below

FY24Q2

Critical care :

Sparsh

Have touched 1,000+ hospitals with the 92 molecules that were launched across 12 states, will 4 mores states in upcoming quarter. SKUs has increased to 96 molecules

PCPM is currently 6-7 lakhs , whenever it reaches 10 lakhs, they add more people in a given region

Currently doing 3 cr. monthly revenues and targeting to reach 6-7 cr. run rate by end of FY24

Have increased frontline strength from 28 to 42 people

Ferticare

Healthcare, Stellar and Spark

Added ENT specialty to portfolio

Polmacoxib is poised to emerge as a leading OTC brand of painkiller

Exports

Received 1 new product approval in Sri Lanka, Chile, Myanmar and Malaysia and approval for an injectable product in Australia

200+ registered products across regulated and semi-regulated markets, 150+ in pipeline

Navsari plant will be running at fully utilization by July 2023

Working capital cycle

Collection cycle is CMO division has increased to 120 days

In sparsh division, now they are directly billing the hospital with payment cycle of 60-120 days . This is resulting in higher working capital, however there is no margin leakage to distributors and they get access to buying data of hospitals

In branded division, receivable days have been coming down (45-50 days)

Dual chamber inventory is of ~22 cr.

Motilal 100 cr. fund raise : 50% will go towards term loan repayment with rest going towards increasing CC limit

Disclosure: same as before

Looks like there is significant drop in meropenem prices which is one of the key product for Gufic criticare division. Innovator Pfizer brand Meronem 1gm is available at MRP of 1067.00 which use to be 2-3 times higher few quarters back. Usually innovator brand commands some premium over other generics. When Meronem is available at such price, other generics brand companies also start adjusting their price. Gufic was negotiating with Govt for higher price of 40-50% to launch their dual chamber meropenem. Q3 concall may provide some insights on the same.

Management view from Q2 concall:

Hi Spartan,

Where can I find a Meropenem and Carbapenem price chart over the last few years? Cheers!

Split Face study with Stunnox( Gufic brand)

Conclusion - The result of Stunnox is similar to other international brands of Botulinum Toxin A