If the efficiency is similar, is the price difference between the product a reason to go for stunnox and not the other?

Yes, I think stunnox having the same efficiacy as a Botox / or other highly used botulinum toxin, and if stunnox is priced at a discount, that will be one of the reasons to go for that.

1 Like

Gufic Bio -

Q3 results and concall highlights -

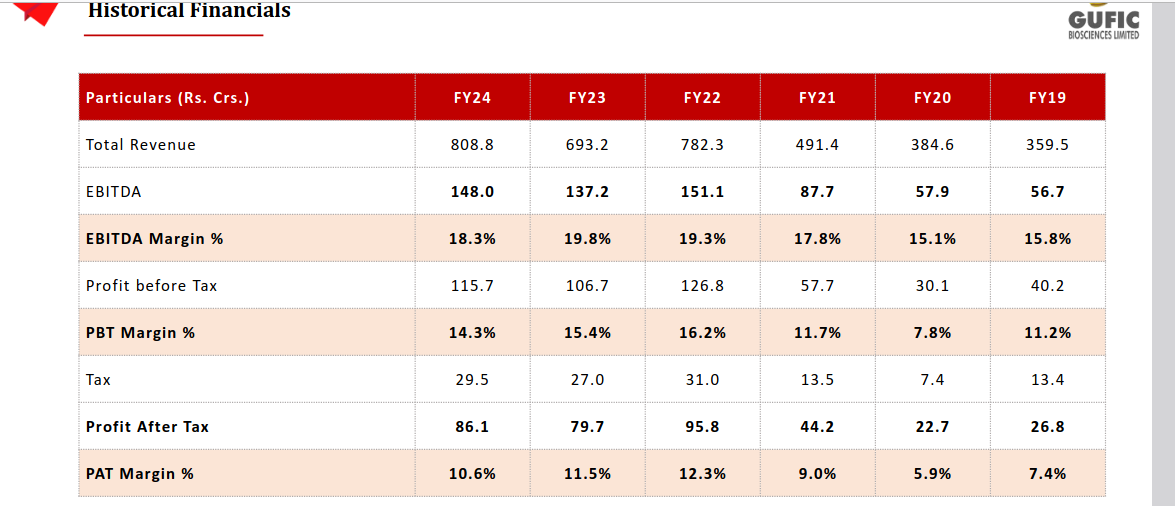

Revenues - 202 vs 177 cr, up 13 pc

EBITDA - 37 vs 34 cr ( margins @ 18 vs 19 pc )

PAT - 22 vs 20 cr

New launches -

Cavim ( Ceftazidine Avibactum - used against bacterial infections ) - receiving encouraging response

First company to launch dual chamber bags of Merofic ( used in severe bacterial infections )

First company to launch Dalbavancin Injection

( used against acute skin infections ) in India

Company maintained market leadership in 2 of its products - Polyfic ( Polymyxin - used against Urinary track bacterial infections ) and Micafung ( anti fungal injections )

Company’s Botuulinum Toxin brand - Zarbot

( used in chronic Migraine’s treatment ) is gaining good acceptance among neurologists in India

Have launched Guficin - to address recurrent implantation failures in the treatment of infertility. Early feedback indicates encouraging results

Sparsh division ( basically selling 90 + injectable molecules directly to 1000 + hospitals ) - has added 70 new hospitals each month in Q3

Indore Capex - progressing well. Capacity to have capacity to make 52 million lyophilised injections and 60 million liquid ampoule injections and 30 million liquid vial injections. This will be the world’s largest single site injectable facility

Segment wise sales -

Domestic formulations( 56 pc of total sales ) - Mainly led by critical care ( 38 pc of domestic sales ), 27 pc of domestic sales come from infertility division, rest comes from mass marketed products, cosmetic brands, Sparsh division

Critical care grew by 16 pc in Q3

Fertility division grew by 18 pc in Q3

Mass marketed products grew by 14 pc in Q3

International formulations( 18 pc of total sales )

Contract manufacturing( 23 pc of sales )

APIs ( 3 pc of sales )

R&D spends for next two years expected to be at around 9-10 pc of sales as the company commercialises new products from its Indore facility

Expect to commercialise the Indore facility by Q1 FY 25. Early plan is to shift a part of domestic business from Navsari facilities to Indore to de-bottleneck the Navsari facilities wrt International orders. By end of FY 25, expect capacity utilisation from Indore at around 25 odd pc as the facility will only be catering to domestic mkts. As they get global approvals in FY 26,27 - capacity utilisation is likely to improve rapidly

Have raised Rs 100 cr from Motilal Oswal MF via preferential allotment ( in Q3 FY 24 )

Already have backlog of orders from Brazil, Germany, Canada. The shifting of domestic production from Navsari to Indore should help company to meet these orders

Disc: holding, biased, not SEBI registered

5 Likes

Wrote a blog on Gufic

Disc - holding and SEBI registered

2 Likes

Hi All,

In the Q3 Concal FY24, the Arisia center was discussed extensively where they would offer anti aging treatments (368 products/services) for all parts of the body including vaginal rejuvenation and also vaginal tightening and mentioned that the costing is from INR 5,000 to INR 15,00,000. They have mentioned that they are close to break even + 10% and would mimic this model at a national level. Would large number of people pay such a price for this segment to be significant for the company? The company mentions the number of footfalls are increasing atleast 10% month on month but what would be scale they can hit.

VPers, please share your thoughts.

Disclosure : only tracking, not invested

1 Like

So Arisia can be a very interesting segment. It was started to create awareness of their botox segment. I was the one who had asked about it on last concall. He had earlier guided to open more centres with a franchise model, but only once his first centre unit economics stabilise.

Skin clinics are a super tough business to run, look at Kaya for eg. He is smart to have not opened more centres until profitability is achieved. But if they do things right, manage to open multiple centres, this could reach upto maybe 5-10% of revenues in the long run, consider it to be optionality for now

Disclosure- invested, recommended, one of my largest positions

5 Likes

So according to your assessment, what are the main growth drivers?

Stunnox

Immuno-therapy

increased capacity of lyophilization

domestic formulations

Gufic has been coming with quite muted numbers in past quarters along with huge pressure in working capital. Management is always very bullish, its good that the 100 cr. capital raise derisks their balance sheet significantly. Concall notes from last couple of calls below

FY24Q3

-

9M revenue breakup

-

Domestic: 56%

-

38% critical care (16% growth)

-

27% ferticare (19% growth)

-

24% mass market (14% growth)

-

5.5% Sparsh

-

Remaining aesthaderm (42% growth)

-

-

Exports: 18%

-

CMO: 23%

-

API: 3%

-

-

Critical care

-

Reached 1,500+ hospitals (50 government hospital)

-

Polyfic became #1 in Polymyxin-B injection market

-

Micafung was market leader in Micafungin market

-

Launched dual chamber bag with Merofic DCB

-

-

Ferticare

-

Launched Supergraf (ultra-purified HMG)

-

Recurrent implantation failure: launched Guficin alpha

-

-

Sparsh

-

Have reached 1,017 hospitals

-

Have increased frontline strength from 42 to 44 people

-

-

Healthcare, Stellar and Spark

- Good growth witnessed in DD1 group products including DD1 extended release

-

Exports

-

Approvals: UK (2), Australia (1), South Africa (1), Mexico (1), Nepal (4), Tanzania (3), Myanmar (2)

-

190+ registered products across regulated and semi-regulated markets, 150+ in pipeline

-

-

Capex

-

Commercialization & capitalization will happen in March end

-

Delay has been because they increase number of lyophilizers from 3 to 6

-

Indore capacity utilization will be 20-30% in FY25, 30-40% in FY26. In FY25/26, will sell in domestic markets. From FY27, once they get site approval for export markets, utilization will improve

-

-

Working capital cycle

- Inventory for dual chamber bag has started coming down. Will maintain 18-22 cr. inventory on a steady state scenario

-

R&D can reach 9-11% for Indore validation batches

-

Target to commercialize 2 products in USA via CMO in FY25, will start in USA as a CMO with a marketing partner

-

Prime bio collaboration: 60-40% profit sharing with 60% going to Gufic

-

175 cr. term loans + 150 cr. working capital limit (70-80% utilization)

FY24Q4

-

FY24 revenue breakup

-

Domestic: 58%

-

Exports: 20%

-

CMO: 21-22%. Should reduce to 15-17% in FY25

-

API: 4-5%

-

-

Critical care

-

Reached 2,000+ hospitals

-

25%+ market share in Caspofungin, Micafungin, and Polymaxin-B

-

Gained 15% market share in ceftazidime + avibactam market (2nd rank)

-

In-licensed a novel pain management solution from a Taiwanese company (patented until 2031) for India market (synthetic analgesic with mechanism like an opioid without associated side effects; doing phase 3 trials in India)

-

Launched Dalbavan, a second-generation lipoglycopeptide antibiotic used for serious bacterial infections

-

Have witnessed pricing pressure which has resulted in slower revenue growth (API pricing has also come down)

-

-

Sparsh

-

Have reached 1,400+ hospitals (30 SKUs)

-

Have increased strength from 44 to 66 people (expanded in Gujarat)

-

-

Aesthaderm

-

Zarbot is prescribed by 100+ neurologists

-

Botulinum toxin contributes 25 cr. (aesthetics + neuro). Another 5-6 cr. comes from other products

-

-

Exports

- 200+ registered products across regulated and semi-regulated markets, 150+ in pipeline

-

Capex

-

4 lines in Indore, will start filing in global markets in November 2024 and expect inspections in 2025

-

Spent 8-12 cr. on validation batches

-

-

Working capital cycle

-

Have extended longer working capital cycles to hospitals, nursing homes and infertility centers. This should reduce by 40-50 cr. by September 2024 and back to normal by March 2025

-

Seeing improved gross margins due to direct business with hospitals

-

-

Should do 950-1000 cr. sales in FY25 and 15-20% growth in next 3-4 years

Disclosure: Invested (reduced position size to <1%, sold shares in last-30 days)

2 Likes

Went through the concall Q1FY24.

Pranav Choksi said the company is expecting Rs 1500 Cr in '27-'28 (3-4 yrs from today) at better margins.

Bull scenario:

Gufic does 1800 cr (additional 30% over guidance) in 3-4 years, margin 20% (200bps more), PAT 240 cr. If current valuations sustain, price ~2.5x

Base scenario:

Gufic does 1500 cr (as guided), margin 19% (guidance expected to improve), PAT 180 cr. Say PE ~30, price ~1.6x

Bear scenario:

Gufic manages 1200 cr (30% lower than guidance), margin 18% (no improvement), PAT 130 cr, PE goes back to 5yr median, price ~1x

Bear scenario looks less likely (possibly recency bias), anything between base and bull case is a good bet in my opinion.

Invested. Looking to buy more on dips.

4 Likes

Very flattish numbers from Gufic, they are running at full utilization and have prioritized better paying customers (aka exports) as their receivable cycle got very stretched in FY24. Indore is supposed to commercialize in September. Concall notes below.

FY25Q1

-

Running at full utilization which has resulted in slower growth

-

Navsari at peak can contribute 700 cr ., with product mix can reach 1200-1500 cr. Can reach total revenues of 1500 cr. in next 3-4 years (Indore + Navsari)

-

Have given ESOP to head of Indore plant and head of certain marketing team

-

FY24 revenue breakup

-

Domestic: 50-55%

-

CMO: 25-30%

-

Exports: 8-20%

-

API: 5-7%

-

-

Ferticare

-

Introduced extended-release formulations of Dydrogesterone

-

Formed a specialty task force – Fertimax to focus on 3 products (dydrogesterone 20/30, Guficin Alpha, Supergraf)

-

Fertimax comprises 40 personnels; 15-20 new + 18-20 existing

-

Their product basket is like BSV (recently acquired by Mankind)

-

-

Spark, Stellar & Healthcare

-

Introduced new molecule in the proton pump inhibitor market: potassium channel inhibitor

-

Introduced Gufispon for cervical spondylosis

-

Strechnil’s market ranking improved from 5th to 2nd

-

Sallaki tablets have 50%+ market share consistently

-

-

Sparsh

-

Launched dual chamber bag Tiecoplanin, dual chamber bag Biapenem, and S Pantoprazole

-

Launching contrast media

-

Expanded to Tamil Nadu, expanding team to 85 people (from 66)

-

-

Exports

-

New approvals: Lithuania (Vancomycin IBE 1000 mg and 500 mg powder), Sri Lanka (COLBACT 2 MIU (Colistimethate sodium for injection BP 2 MIU) and Stripole (Pantoprazole for injection 40 mg))

-

210 registered products across regulated and semi-regulated markets, 150+ in pipeline

-

Faced capacity problems for Germany, UK, Portugal

-

-

Indore capex

-

Validation of 2 lines finished, commercial production should start in September. Commenced product site transfer from Navsari to Indore

-

Lines 1&2: lyophilization (validation to be completed in September)

-

Line 3: liquid vials (validation completed)

-

Line 4: ampoule (validation completed)

-

Indore will double their capacity

-

In Phase-1, will launch 58 products with 26 being tech transfer from Navsari

-

Targeting 25 lakh lyophilization vials and 10 lakh liquid vials in September

-

30-35% utilization in FY26, 60% in FY27 and full utilization in FY28

-

Capex: 300 cr.+

-

Will start filing dossiers by January 2025

-

-

Working capital cycle

-

Peak debt: 175 cr. term loan + 120 cr. working capital (~300 cr. at peak )

-

Will only repay starting FY26, will use debt for working capital in first year of operations

-

Longer receivables to hospitals, nursing homes and infertility centers have reduced, prioritizing better paying customers (lost 15-20 cr. sales because of this)

-

Disclosure: Invested (no transactions in last-30 days)

5 Likes

Company’s profit is the same for the last 12 quarters. 12 quarters is 3 years.

Imagine no profit growth for 3 years. Despite this it admirable to see your confidence in the company.

The question one needs to ask is, “Is it possible the company is misleading investors about the future like they have been doing for 3 years?”

3 Likes

That is because they had covid related sales in ‘21 and ‘22. I would recommend you read the calls during that period to get the exact numbers.

This was expected and communicated by the management

5 Likes

FY21 and FY22 had Covid bump up. So limited growth in FY23 is understandable. What about FY24?

Promoters keep spinning stories according to their convenience

For FY24, the topline grew by ~17% (good in my humble opinion). It did not translate into bottomline due to contraction in margins (various reasons mentioned in concall, pls have a look).

Now if the issue is why FY24 profit didn’t grow YoY and this single year performance is the only reason we should badmouth the promoters - I would personally refrain.

Very few companies (like Abbott) grow consistently and every single YoY - that is the beauty of running a business. Sometimes there will a black swan event (Covid) that will boost sales like never before, other times the top and bottom line will look inconsistent. Long term is what matters. Look at Divis Labs for example. Terrible growth in past 2-3 years - does it mean Mr Murli Divi is selling dreams?

Gufic grew topline by 21%CAGR and bottomline by 35% CAGR in 10 years! It has undertaken Indore capex that will help it double its sales in 3-4 years and improve margins.

Nice story to keep track of… maybe invest if you are a hopeful person like I am. Maybe not.

Disclaimer: Invested in Gufic. Exited Divis few months ago.

Cheers!

6 Likes

Great company with Great management , with innovative product .

but I have few concern valuation is bit hefty if does not support growth

than big concern,

another thing to not financial is that calculate interest that company

capitalize and check again . you find different view ,

although my view is that business can grow at 15-20 % as management

guided , but working capital is stretch and reliance on debt and long

watch debtor days have to closely watch.

3 Likes

You always want to look at stocks with the lens of opportunity cost. It is easy to get carried away by management narratives and hope, and that would be okay if opportunities were few and far between. However, there are some wonderful opportunities, even in the pharma sector that are much better positioned and whose management always walks the talks (case in point is Caplin Point which has been growing consistently for more than 20 quarters in a row).

We as investor have this bias that patience is a virtue and our patience is almost always rewarded and the more we spend time studying or following a company, the more we get married to its story. The fact is, patience can destroy your wealth if you put it in a bad company and the common thing about good and a bad company is, they both tell a good story. So judge a company not by the story they tell, but the numbers they deliver.

Disclosure: I was invested in this company two years ago but have since exited.

1 Like

pretty decent growth over the medium term. The Indore plant will more than double capacity. So, Gufic will be a different company in another three years’ time.

dis: holding

3 Likes

Thank you for sharing your thoughts.

Our discussion has boiled down to this:

Gufic had extra boost in the top and bottom line in FY21 and FY22. Hence FY23 didn’t look nice. FY24 has good topline growth but bottomline suffered due to margin contraction by ~200bps.

1 year which is FY24 has not lived upto our expectations and that too only in the bottomline.

Is 1 year enough to take a call on a company? Does ~16-17% growth in this 1 ‘bad’ year mean nothing and we start calling a 1 year patience a bad virtue?

I am a fan of the likes of Abbott, but I understand it is a business in action not my excel sheet. I choose to give it time. I guess this is why we call investing an art and not a science.

Either of our opinions can go wrong - that is why we are all learners of the market.

5 Likes

Hi,

Does anyone have an idea whether the company’s existing and new facility is USFDA approved?

Do they have any sales from US? and any plans regarding that in the future?

Gufic has > 85% sales from domestic market, some 5% from Asia and EU each. Lower from North America.

Need to go back to check if there is any USFDA approved plant but based on sales it looks like it is not needed. Request you to look at company presentations.

3 Likes