I have made a few modifications to the portfolio:

-

Sold 2% position in Transpek. Company is facing some headwinds in their end markets along with price compression in their end products. What I particularly dislike is their delayed capex plans despite them running at fully capacity for sometime. I am looking to buy Ultramarine as an alternate, as they are doing modular expansion and have similar business profile.

-

Sold remainder 2% position in Chamanlal Setia. Despite 20% drop in volumes, they were able to report higher profits due to smart raw material procurement done in October. Basmati cos are currently doing very well due to decadal high basmati prices, and I want to take money out as I dont know how long the basmati cycle will last.

-

HDFC merger into HDFC bank takes 4% HDFC position out of portfolio and replaces it with a 4% position in HDFC bank. I will likely scaleup HDFC bank to 8% at some point in the future

-

Reduced position size in Sharda Cropchem from 4% to 2%. Global agchem companies are facing higher pressure compared to domestic cos and I want to tactically allocate more to domestic facing cos (see #5)

-

Added 2% allocation in Dharmaj Crop Guard as they have been doing exceedingly well, having grown sales at 30-40% CAGR in past few years. As their technical plant come onstream this quarter, their margins will get a boost. I am expecting 20-25% sales growth with some margin expansion over the next few years, resulting in high EPS growth. Current valuations are not very demanding

-

Increased position size in SGRL - PP from 1% to 2%. SGRL annual report was a delight to read and management is very confident about future growth. This is a company which can likely trade at very high valuations as they have a very differentiated business model, as seen in high margins and ROCEs

-

Increased position size in Geekay wires from 1% to 2%. Despite a 4-5x jump in prices since I initiated the position, valuations haven’t increased significantly as earnings have just exploded. In their annual report, they mentioned about their order book being full and them doubling capacity in nails. Recently, I came to know that Geekay is one of the only 2 Indian companies who are approved to sell pneumatic nails in the US. Also, the anti-dumping investigation came out in their favor, which gives further fillip to their business. On trailing basis, they are only trading at 10x earnings

-

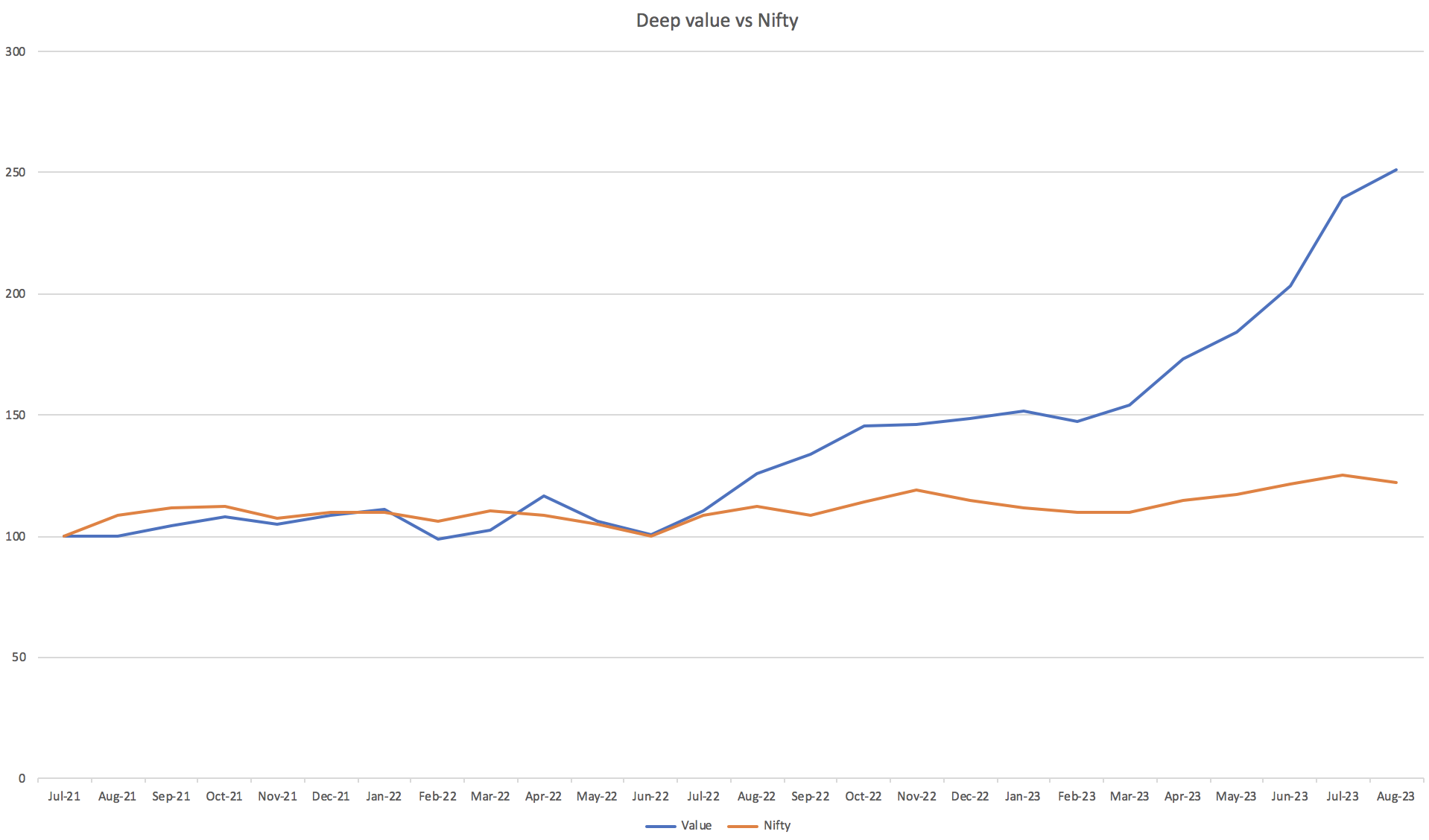

Added 2% position size in Worth Peripherals in deep value basket. This is a business currently not doing well, but I like their execution since their IPO in 2017. They are cheaply valued, and I hope to sell at 2x PB in the next couple of years. I feel its a low downside opportunity, where downside is capped at Rs. 90-100. Given the spectacular success I have witnessed in deep value strategy, I will now be initiating new positions at atleast 2% position size

-

Added 2% position in Godrej Agrovet and 1% in KSE Ltd. Thesis in both is of mean reversion. Both companies are into feed manufacturing and their margins were adversely impacted in last couple of years. As a result, both are trading at cyclical lows in terms of EV/sales. Margins have started recovering since last quarter. The additional kicker in KSE can come from a potential of Godrej acquiring them, as they already own some stake in the co and are in the same business line

-

Reduced position size in Aditya Birla AMC from 4% to 2%. A number of their equity schemes have been doing badly of late. In terms of strategy, Aditya Birla schemes are exactly reverse of HDFC AMC, where Aditya Birla focuses on high return metrics often combined with obnoxious valuations, whereas HDFC is much more value focused. Value has made an amazing comeback in the past year and I am looking to buy more of HDFC AMC.

-

Added 2% position in Mayur Uniquoters. Growth in exports is back for Mayur, and its likely that they grow sales at 15% for the next few years, which along with margin uptick can result in 20%+ EPS growth. If that happens, it can be a doubler.

My current thoughts on a few portfolio companies:

- I want to reduce position sizes in Ajanta Pharma and Gufic Biosciences as pharma companies have done exceedingly well in past few months (this basket is up 37% YTD for me) and I want to reduce allocation to companies which are trading at higher end of their valuation bands. I think Ajanta is the most differentiated midcap pharma co, however they have been topping out at 6-6.5x sales, with current valuations being ~6x sales. Gufic is also trading at higher end of their valuation band.

- I want to increase Aegis’ position back to 4%. Over time, clarity has emerged about the sustainability of LPG as a good alternate to LNG in industrial applications. I was earlier confused if this replacement was due to one time arbitrage in pricing between the two fuels, whereas the management was confident of this sustaining for atleast 2-3 years. Its turning out that management were spot on (as reflected in much higher LPG imports into India vs LNG). Aegis has a very very differentiated management.

- I want to increase position size in Kaveri seeds to 4%, finally their growth has started kicking in due to their focus on rice and other vegetable seeds. Additionally, they are doing exceedingly well in export market. Its uncommon to get a market leader with high return metrics at such low valuations (10x earnings) in Indian markets.

- I want to increase position size in Manappuram to 4%, as growth is coming back and they are trading at very cheap multiples.

Updated folio is below, cash remains at 2%.

Core compounder (40%)

| Companies | Weightage |

|---|---|

| I T C Ltd. | 4.00% |

| NESCO Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 4.00% |

| HDFC Bank Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Gufic Biosciences | 4.00% |

| Aegis Logistics Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

| P.E. Analytics Ltd | 2.00% |

| Aptus Value Housing Finance India Ltd. | 2.00% |

Cyclical (47%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 2.00% |

| Stylam Industries Limited | 2.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Sundaram Finance Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

| ANUH PHARMA LTD. | 2.00% |

| Shree Ganesh Remedies Ltd - PP | 2.00% |

| Aditya Birla Sun Life AMC Ltd | 2.00% |

| Dharmaj Crop Guard Ltd | 2.00% |

| MAYUR UNIQUOTERS LTD. | 2.00% |

| Godrej Agrovet Ltd. | 2.00% |

| KSE LTD. | 1.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (9%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 2.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| RKEC Projects | 1.00% |

| Worth Peripherals Ltd | 2.00% |