• Gufic group is in the business of manufacturing and marketing injectable products since late ‘70s

• Navsari facility is a WHO GMP certified injectable manufacturing unit, catering to general and hormonal products

• Gufic currently has 9 Lyophilizers catering to total capacity of 19.2 million vials per year

• Gufic’s lyophilizatoin product includes antibiotic, antifungal, cardiac, infertility, antiviral, and proton pump inhibitor

• Pharmaceuticals contribute 88% and API business contributes 12% of the revenuw

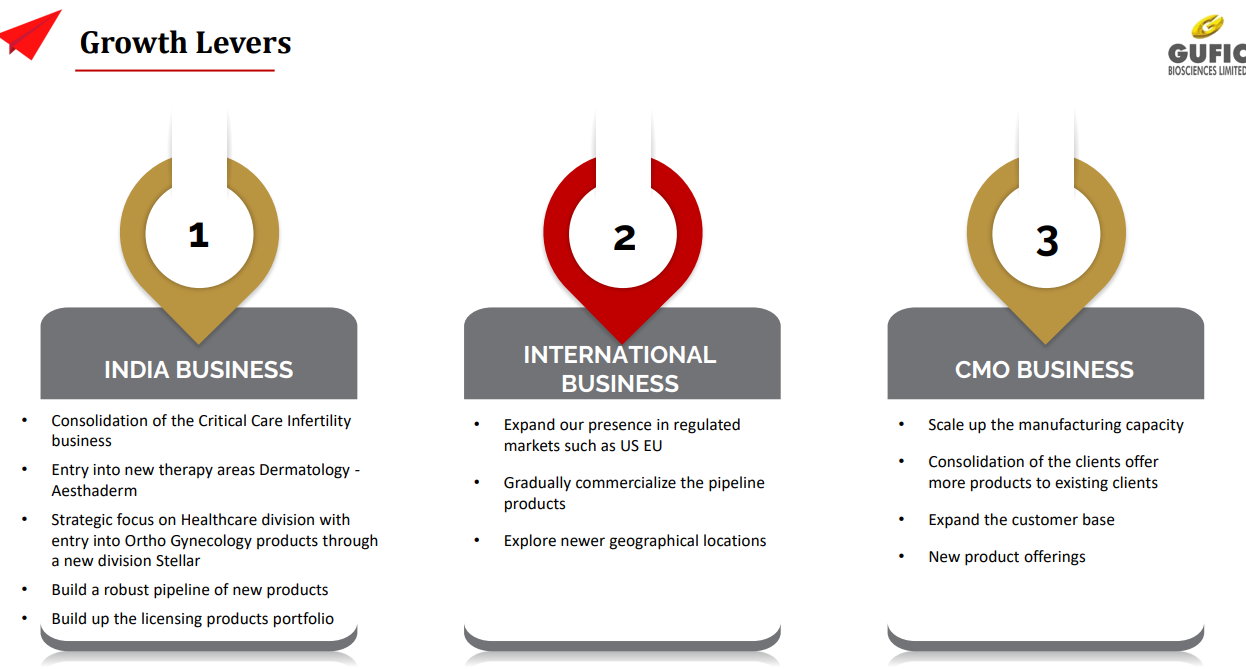

• Gufic Stellar: A newly created specialty SBU with specific focus on Orthopaedic and Gynecological products in various segments like Pain, Infection, Pregnancy, Lactation and bone and muscle products. Focussed markets are metros

• Gufic Aesthaderm: Venture into the potential sub-chronic segment of Aesthetic Dermatology focus on Moisturizing agents, Anti-aging, Hyperpigmentation, Sunscreen and Pre/ post procedural products

• Building Covid-centric products like anti-infectives, Sepsis products and Peptites

• 30 active projects in pipeline, initiated 3 clinical trials in India in the field of anti-virals, resistant bacteria infections and Dermatology

• API business: Categories of API manufactured are Anti-Fungals along with their Intermediates, Anti-bacterials and Anesthetic agents. Plans to add 6 new products

• Gufic would be the first company to launch an indigenously manufactured Botulinum Toxin (for wrinkles and sagging skin) in collaboration with Prime-Bio,USA.

• Technical collaboration with Lucas Meyer, Canada & France for developing Aesthetic dermatology

• Having 12 Brands

• Exports 12%

• Quite strong in Critical care

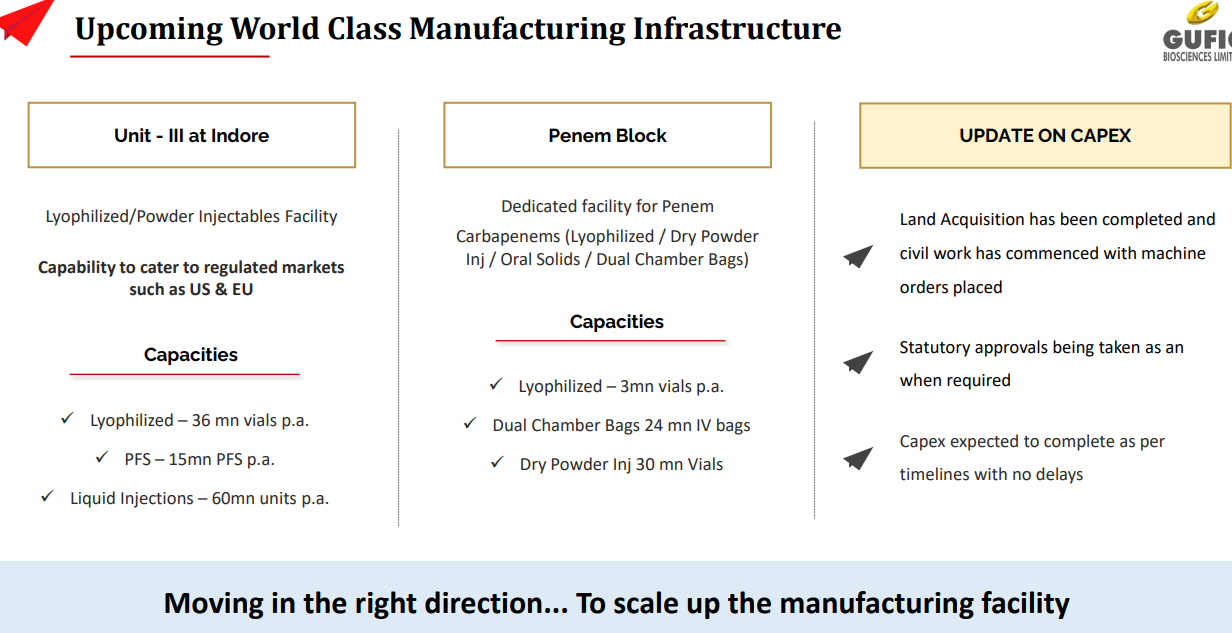

• Capex for increased capacity of lyophilized and anti-fungal products is fully operational

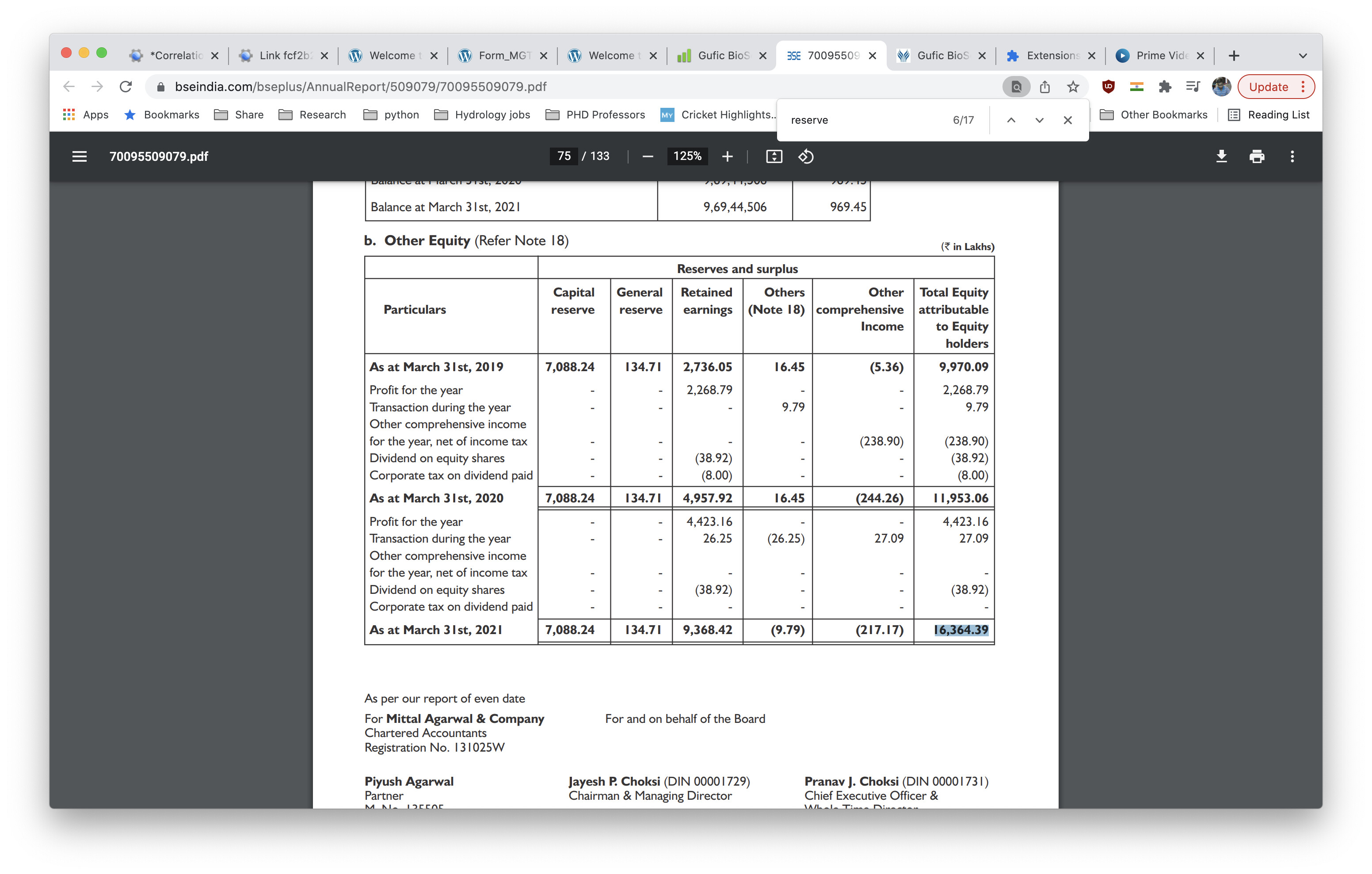

• Cash and cash equivalents amounting Rs 4.52 crore as on 31st March 2020

• Negotiating with international companies for in-licencing innovative concepts in Dermatology

• Deterioration in operating cycle beyond 130 days leading to consistent increase in working capital utilization thereby resulting in stretched liquidity

• Company’s gross cash accruals are sufficient to meet the long term repayment obligation for the medium term

• Amalgamation with Gufic Lifesciences Private Limited

• Post-merger, total Lyophilizers installation capacity increases to 37.2 million vials per annum

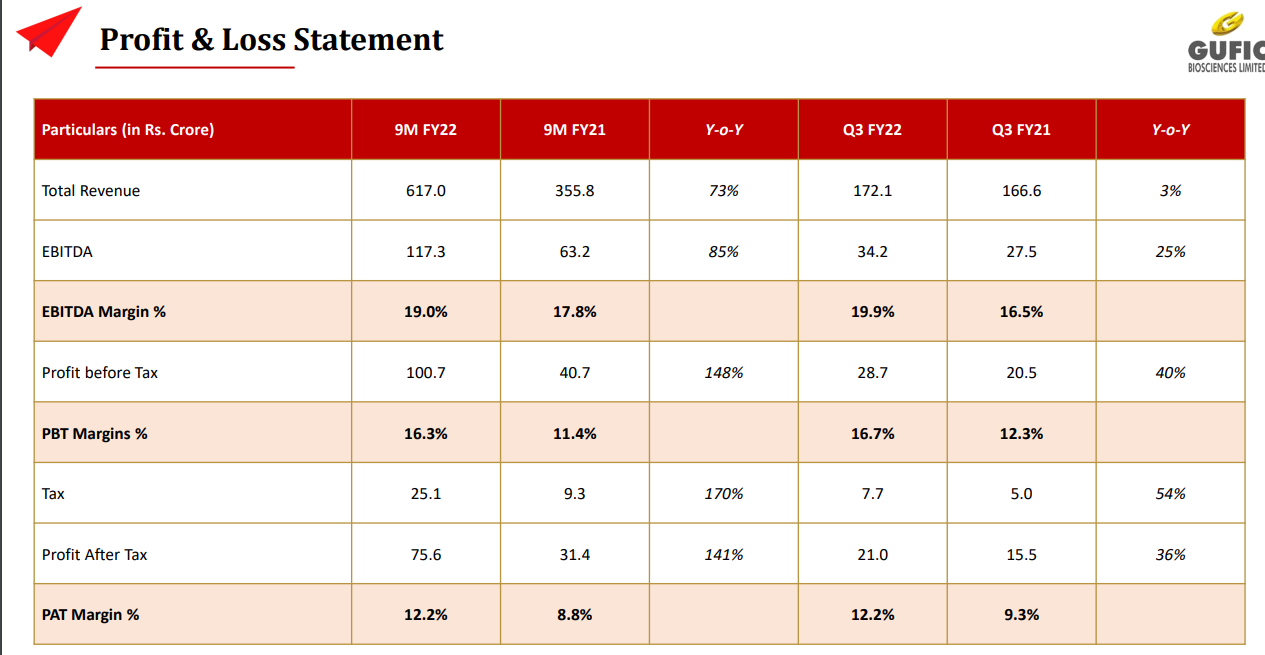

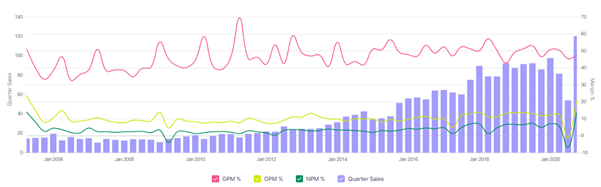

Company performance

Important highlights:

PE : 40

ROCE: 22.1%

ROIC: 18.3%

ROE : 26.7%

ROA : 11.2%

Debt to Equity: 1.18%

EBIT to Sales: 12.8

Yearly sales growth for 10 years: 19%

Promotors holding: 65.75%

Risks

- Company is entering into high competition Aesthetic dermatology, this is a major deviation from it’s core business of manufacturing and marketing injectable products. They could have leveraged their past experience and explored new Theurepatic areas. We need to monitor all-round progress of this division / line of business

- Merging the management’s personal owned Gufic Lifesciences Private Limited could unduly dilute the equity of the listed company. Appropriate stock conversion ratio is important for investors value for money

What are the opportunities

- 12 Successful brands

- Post merger, capacity will more than double

- If they are successful in high margin Aesthetic dermatology, company would get FMCG valuation

Disclosure: Did not invest, will invest in small quantities from next week. Would like to remind that the risks mentioned are very important to note. This write up is not for recommending either way.