Apart from daily market acquisitions Parent company Godrej Industries yesterday aquired more .5% stake in the company through bulk deals. Investor Balram Singh Yadav sold 10 lakh equity shares in Godrej Agrovet at Rs 570.01 per share on the BSE, the bulk deals data showed. promoter Godrej Industries was the buyer in a deal, acquiring 9,76,047 equity shares in Godrej Agrovet at Rs 570 per share.

Seems like promoters are quite bullish on future operations. Turnaround may be not far.

Hi, I see the longer version of story, not effected by 2-3 years. GAL has a long way to go to spread its wings. I have it in my bag for a longer time period. Next 2 yrs will be very good for its animal feeds business.

Like many firms across sectors, rising input costs are hurting margins and profitability. Revenue growth was healthy but flat profit growth…I see it hurting valuations of many companies across the board…the impact has been varied and the confidence of street on the abilities of a business to protect its margin in these times would define the magnitude of correction…the mid-term growth/de-growth would finally depend on actual execution…

Disc: Was invested in past, mildly tracking. Not a buy/sell recommendation. Views for academic purposes

Share price can rise but even if palm oil prices double and sales double the total revenue will only increase by 10% as most revenue comes from animal feed business.Also i read online not sure that palm oil can be substituted by coconut oil which india produce but is 2 to 3X expensive then palm oil ,if this gaps lower people might switch to alternative oils

It also sits at strong support level and i think is fairly price .i will be making a small tracking position for swing trade on monday.If you gather more information please share would be helpful over the weekend.

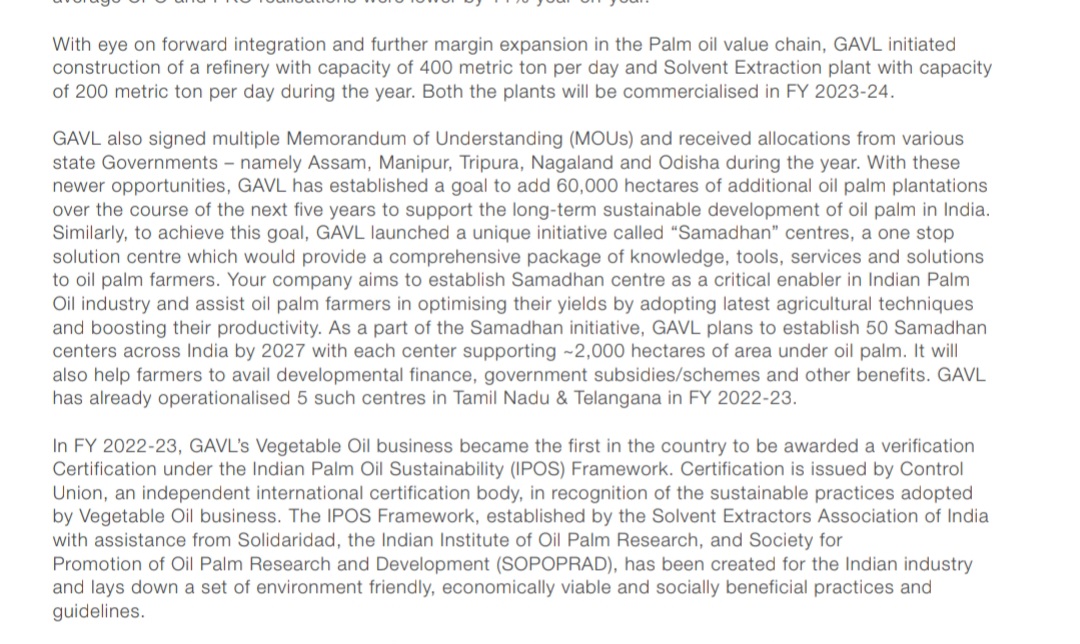

Godrej Agrovet has formula based pricing model with Indian farmers. Agrovet gets only 25% of Palm Oil price. So no doubt with rise is prices Agrovet gains but biggest beneficiary is farmer.

Fair set of numbers after many quarters. Most segments did well this time except diary segment, which also had an exceptional item of 17cr. Believe stock is currently at a support range.

Agri Sector

– Provides livelihood for ~55% of India’s population. This number has been de-growing and is expected to further reduce over the longer period.

– From FY16 to FY22, agri exports grew at a CAGR of ~7.5% (from ~$32B to ~$50B)

– Detailed report on agri sector - here

–

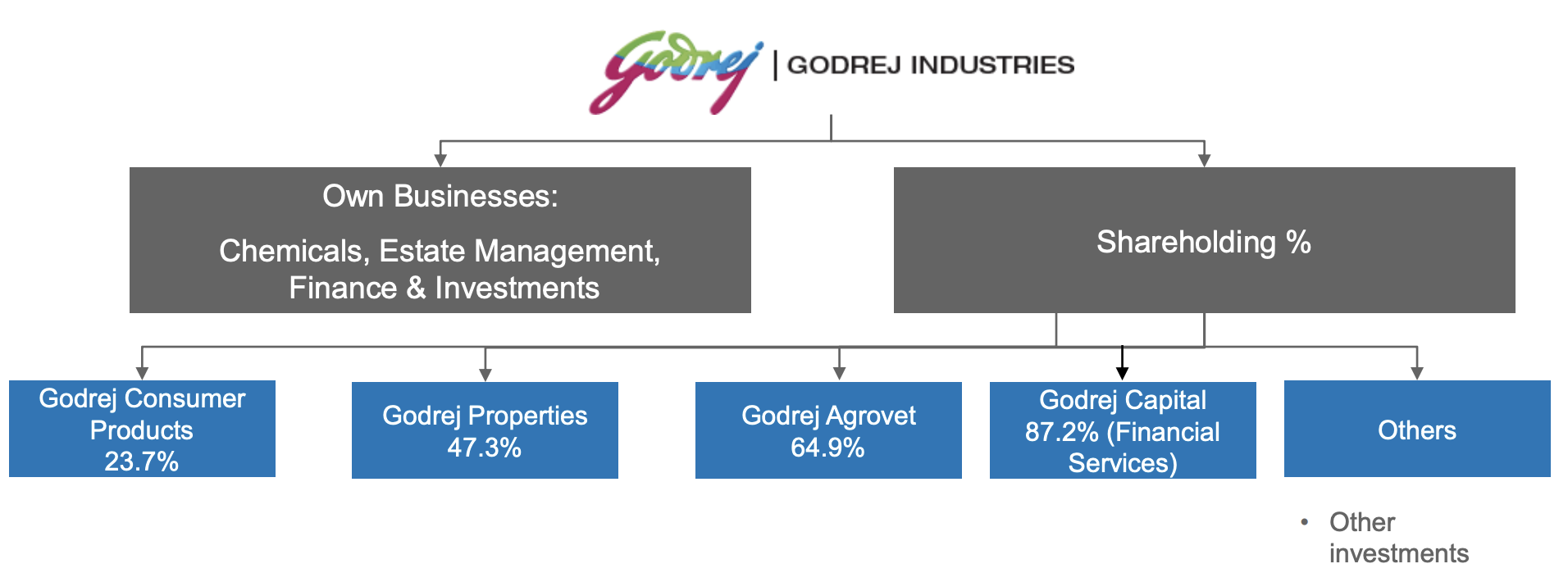

Company also has a couple of Joint Ventures and some investments in UAE. One of the JV is in Bangaldesh (agrochem) and another is a VC firm that invests in agri-startups.

Has some investment in UAE but I have never been interested in their UAE investment so I’ll skip it.

Seasonality and Triggers

During Drought: Cattle feed sales increase. However, other costs also go up and the impact is nullified at present [Page 7]

Company is involved in a seasonal sector. However, it is working to reduce the seasonality effect

Can take 5 to 7 years for the new processes to be set up and come into action

(infrastructure requirements, regulatory approvals, crop protection business, et cetera)

Capex

Herbicide Plant worth Rs 500 Cr - to be commissioned by Dec’24

Valuation Comfort

There are a lot of different metrics that you can look at. However, this attracts me:

Market Cap (9300) <= FY23 Sales (9300)

Market cap at ATL v/s Profit at ATH: (Market Cap 5 years back was around 12k)

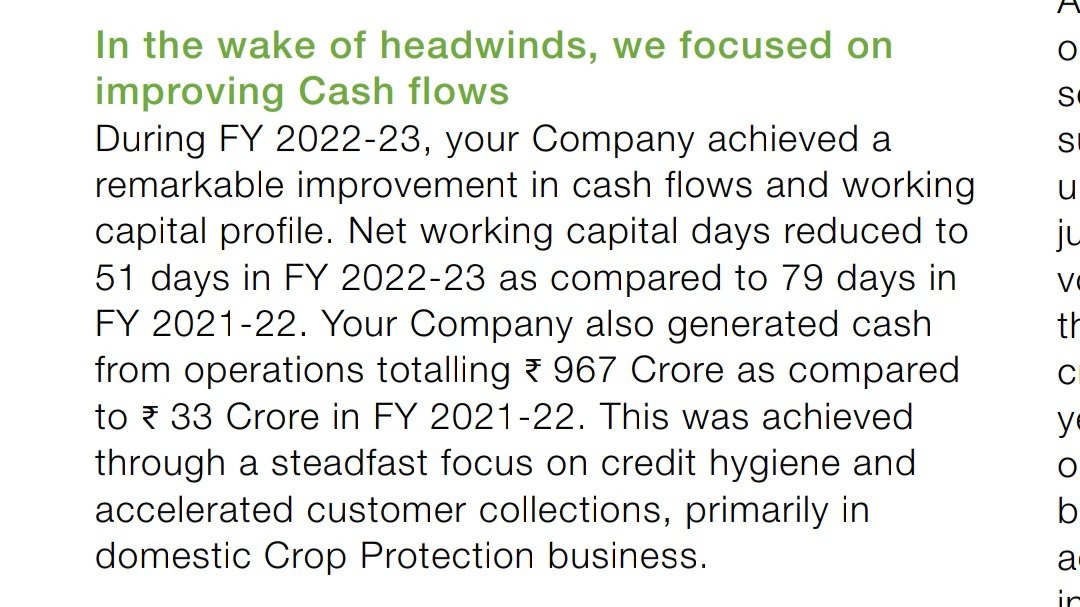

Mixed bag results. Margins got impacted. However, sales were highest ever. Improvement in WC cycle & collections.

● Poultry & Processed food

Achieved 1000 Crore milestone, top line growth of 28%

Planning to improve margins by scaling volume growth & accelerating e-commerse channel & brand building.