I joined their concall. The R&D unit is also going to benefit Crop protection and Animal feeds business. The company’s Godrej Tyson Foods business has benefited from the lockdown, it currently has around 30 percent market share in Frozen Non-vegetarian food business and around 7-8 percent in vegetarian frozen food business. I personally feel this company is a very decent bet for anyone betting on agriculture/ animal husbandry theme. It is still available at near IPO prices despite revenues and profits growing by 30-40 percent since listing and astec lifesciences having gone up multiple times in the period. Here is how i managed to value the business - Current Market Cap - 8900 crores. Value of Subsidaries - Astec Lifesciences 62 percent of around 1900 crores = 1178 crores, Godrej Tyson JV = Valued at 40x of PAT (conservative value) ( 2800 crores, Agrovet share 1400 crores), Creamline Dairy = 500 crores (conservative value) (Valued at 15x = 500 crores). If we take a holding company discount of 50 percent for Astec Lifesciences, the value of subsidaries is around 2500 crores give or take. This puts the value of standalone entity at around 17.7x without factoring in any growth. I expect the company to grow at around 15 percent for next 3-4 years and 20 percent for Godrej Tyson and Astec Lifesciences.

I have created a separate thread for Astec Lifesciences. I would recommend/suggest having deeper discussions about astec specifically on that thread since it is a separate public listed company.

As a Brand, Jersey began its journey 34 years ago with a focus to build the milk business. Over the years, Jersey has created an exciting product portfolio and become a household name and a preferred dairy brand amongst millions of homemakers in southern India. Keeping in mind the evolution and its association with iconic brand Godrej, Jersey started on the path of forging a new, improved brand identity. The new design language flows from the strong legacy of the brand incorporating the promise of trust and quality personified for over a century by Godrej. Jersey is now Godrej Jersey.

.

Raj Kanwar, Chief Executive Officer of Creamline Dairy Products Limited, said, “The new logo that resembles a smile will help us resonate with multiple stakeholders across product categories. As we expand our portfolio and focus on driving accelerated growth in value-added categories, it is imperative to maintain uniformity in the design theme."

Today Rajya Sabha passes 3 bills related to farmers. And prima facia reports suggests that it will benefit the Agri procuring companies like Godrej agro.

Giving some extract below

"The bill on Agri market seeks to allow farmers to sell their produce outside APMC ‘mandis’ to whoever they want. Farmers will get better prices through competition and cost-cutting on transportation. However, this Bill could mean states will lose ‘commissions’ and ‘mandi fees’.

The legislation on contract farming will allow farmers to enter into a contract with agri-business firms or large retailers on pre-agreed prices of their produce."

+1. I totally agree with you. Dairy Play - i) Majority stake in Creamline. ii) 70% in Maxximilk. Agrichemicals - 55% in Astec Lifesciences. And many more.

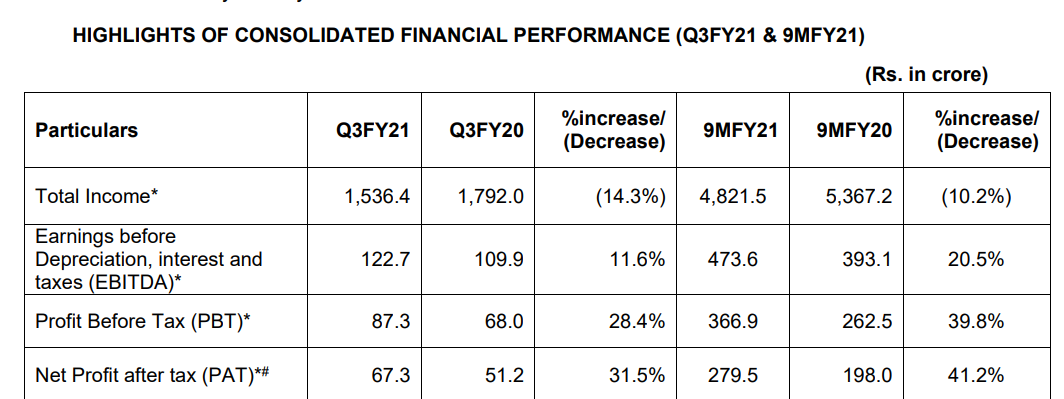

All segments have given better margins and overall EBIDTA jumped 25% for the 1st half of 2021 compared to the first half of 2020.Seems like all positive news except the revenue part which was down due to Covid-19.

Please find the link below for the investor presentation.

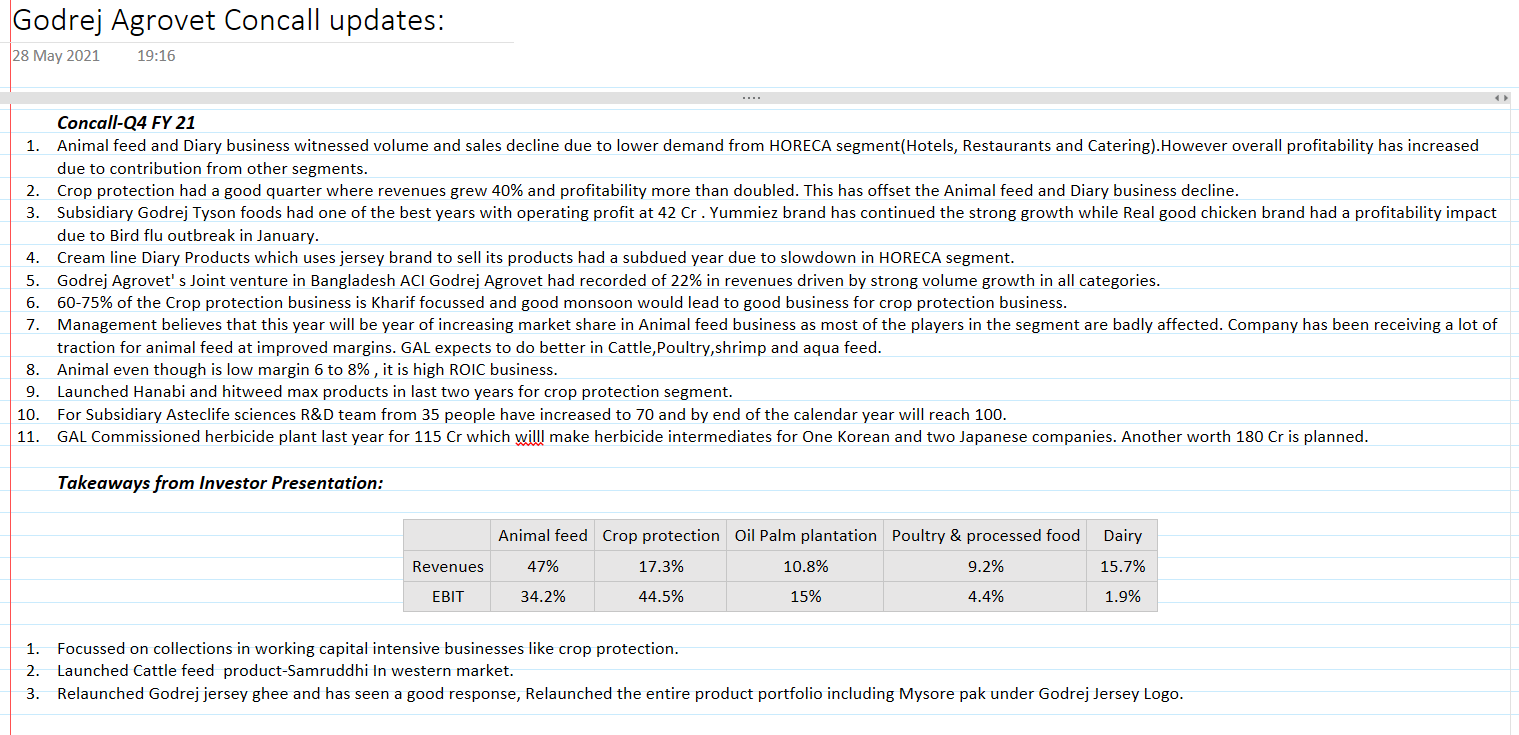

Decent set of numbers all around. Some interesting points made in concall.

Expecting Astec Lifesciences to maintain a bottomline growth rate (no guidance on topline) of 20 percent till the new R&D Centre is executed which shall be either end of FY 2021 or start of FY 22.

Expect Crop protection business to grow over previous years revenue and profitability despite a disappointing H1FY21. Some major changes made on efficient working capital which will result in more efficient cash flow and lower working capital cycle.

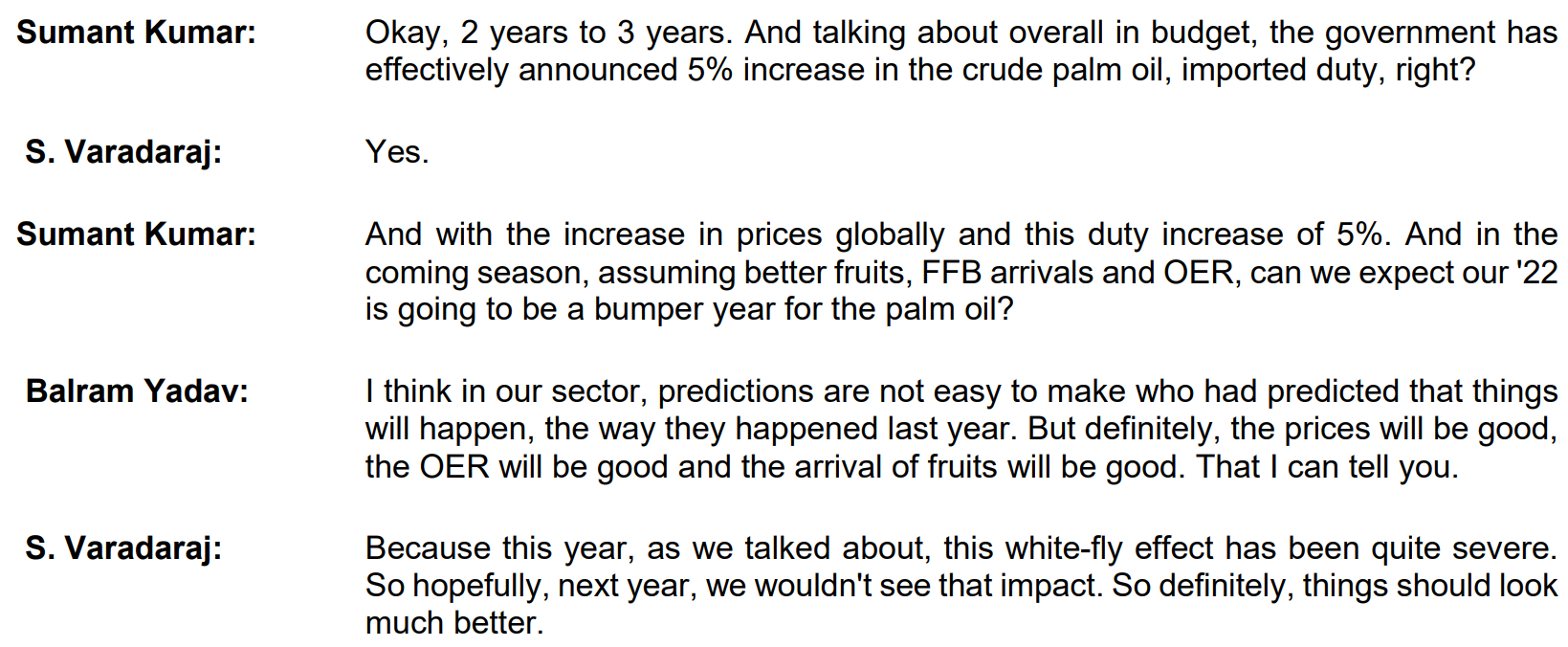

Palm oil business did well primarily due to rise in prices, management expects elevated prices may sustain due to low supply. Palm oil business could have had a bumper quarter since prices and yields have gone up by around 35 and 36 percent respectively but was affected due to white fly attack.

Animal feed business was affected due to lower demand. Segment margin improved due to lower input prices.

Demand is not good for Creamline Dairy. Currently hold around 9-10 crores of inventory, expect surplus supply will end around start of next year

Expect margins of godrej tyson foods to sustain around per Q2 numbers (around 6.3%)

Bangladesh JV will grow around 20 percent topline and 25-30 percent bottomline in the current year. Will be number 2 player in Bangladesh from number 3 in animal feeds business.

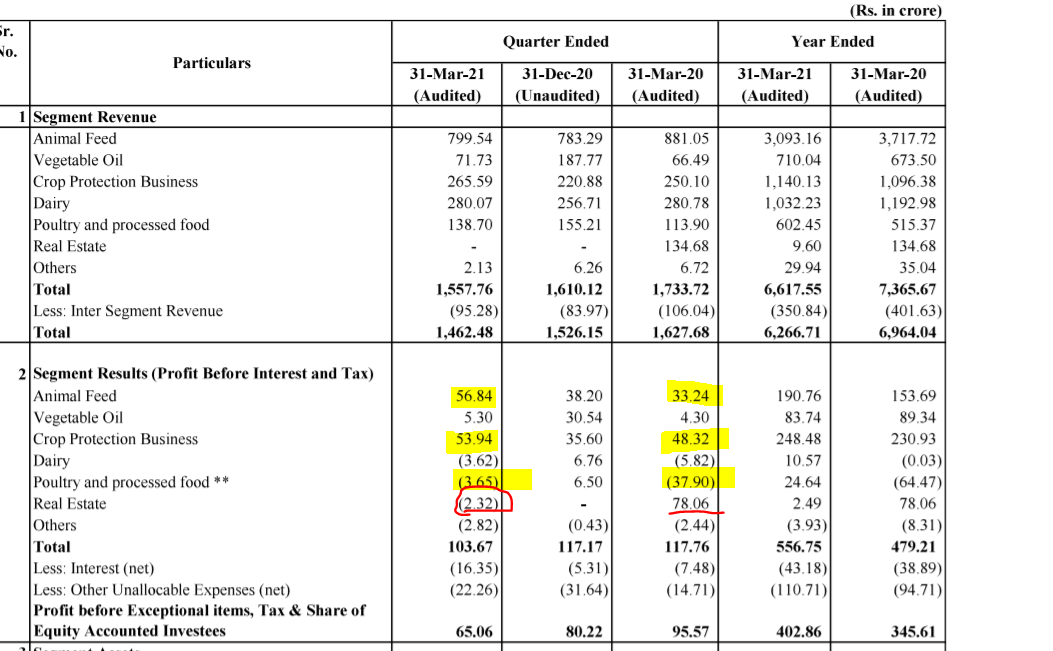

Segment-wise, most of the segments have seen an increase in profitability in the first nine months compared to the previous year.

Animal feed segment results grew by 11.2% year-on-year, despite 16.5% and 19.1% decline in volumes and sales.

Consolidated revenues and segment results in crop protection segment grew by 3.3% and 6.5%, respectively, as Astec LifeSciences posted robust performance in the first half.

Our poultry and processed foods focused subsidiary, Godrej Tyson has

reported 15.5% revenue growth with EBITDA of Rs.41.1crore compared to a loss in the previous year.

Low procurement prices benefit Creamline Dairy and EBITDA has grown by 16.8% in the nine month,despite a 17.5% revenue decline.

However, vegetable oil segment was impacted by white-fly attack which lowered FFB arrival and oil content in the fruit. Therefore, segment result declined by 7.8% in the first nine months.

Hi,

Results are out.

Revenue wise muted YOY.However considering COVID situation it should be fine,

Segment wise Improvement in terms of Profit in all segments except the real estate business which was a drag and dented the overall profits

If we compare the PAT excluding the exceptional items (real estate) in FY20, its a fairly positive number, although top line has some de-growth attributed to covid disruptions.

Animal feed, Dairy segment disappointed (Covid) while Food segment (Tyson), and oil palm segments done fairly well.

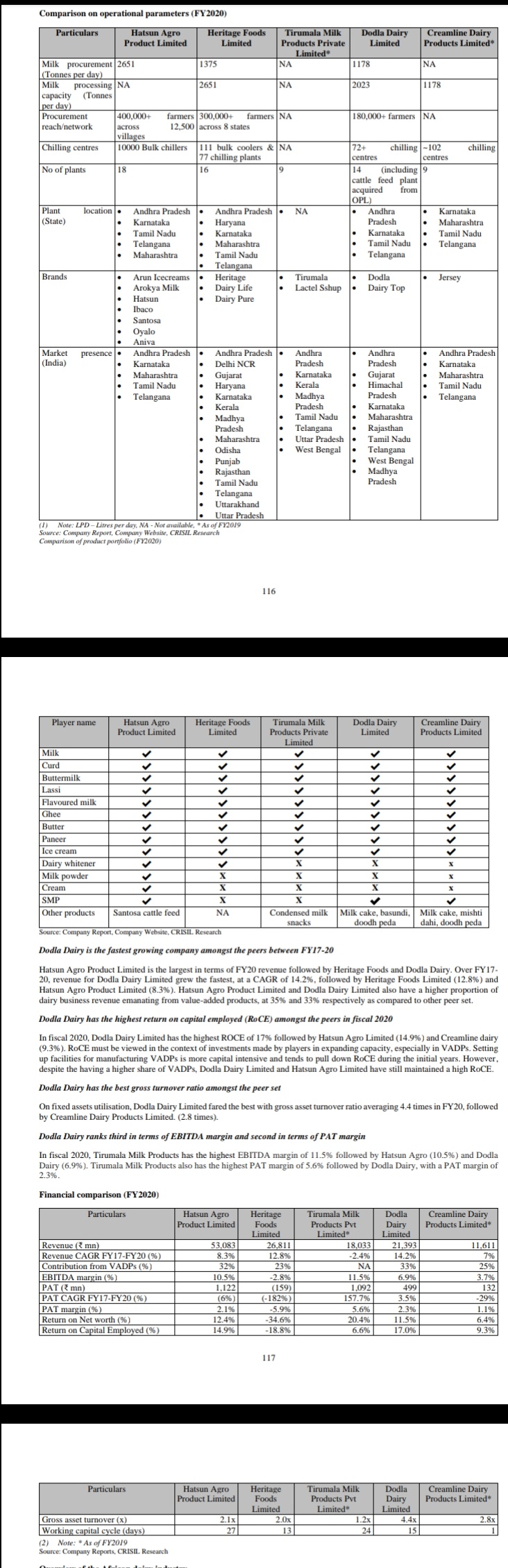

Here is the comparison of Creamline Dairy with other companies in the space and region. Creamline Dairy’s prospects looks decent and the market size looks big taking into account how well Hatsun Agro has done over the past decade.

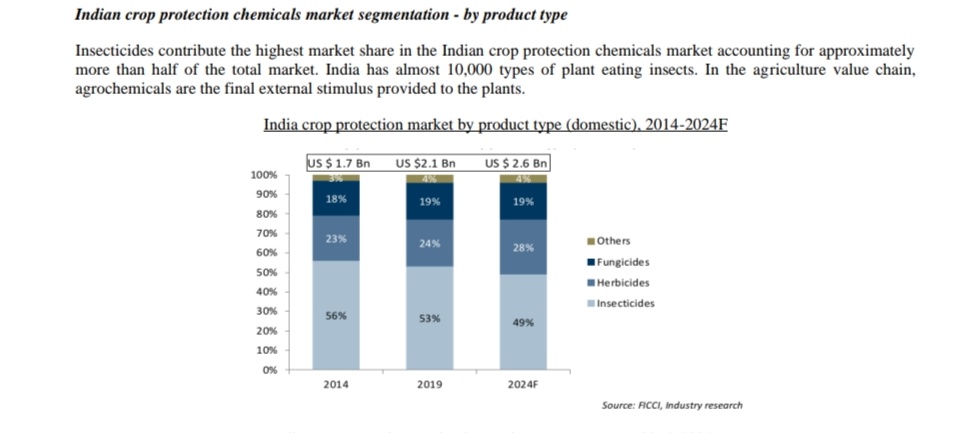

Also herbicides market is gaining market share and is expected to grow very rapidly compared to insecticides and fungicides which is a big positive for Godrej Agrovet crop protection segment and Astec Life Sciences.

Also attaching my views about why I believe Godrej Agrovet is probably best suited for a multiple year earnings growth.

Key points -

A bumper year in the palm oil segment as prices are up 77 percent year on year and last year fruits were destroyed due to a white fly attack.

HoReCa industry to comeback strongly with the second wave of covid seemingly slowing down bodes well for the Feeds and the live birds segment.

Crop Protection had a loss of 50-60 crores of sales due to lockdown in plant in the previous year, that would directly add to top and bottom line.

IMD has estimated to be a good monsoon in line with the last 2 years.

Other positive triggers are gaining market share in frozen foods business and Bangladesh JV growing at a topline of 20-25 percent and bottom line of 35 percent.

Technically Godrej Agrovet is on verge of multi year breakout, based on studies it could be probable candidate of demerger in long future , all depends on management.

actually there was a attempt in the past to merge astec life science with godrej agrovet and dropped due to opposition of minority share holder(main people sold almost of theirs now) so there are expectation of merger in the future infact G agrovet increased its holding percentage , so your version is surprising