Q1FY24 Results:

- No sales growth YoY.

- Reduction in materials cost increased YoY profit

Links:

Q1FY24 Results:

Links:

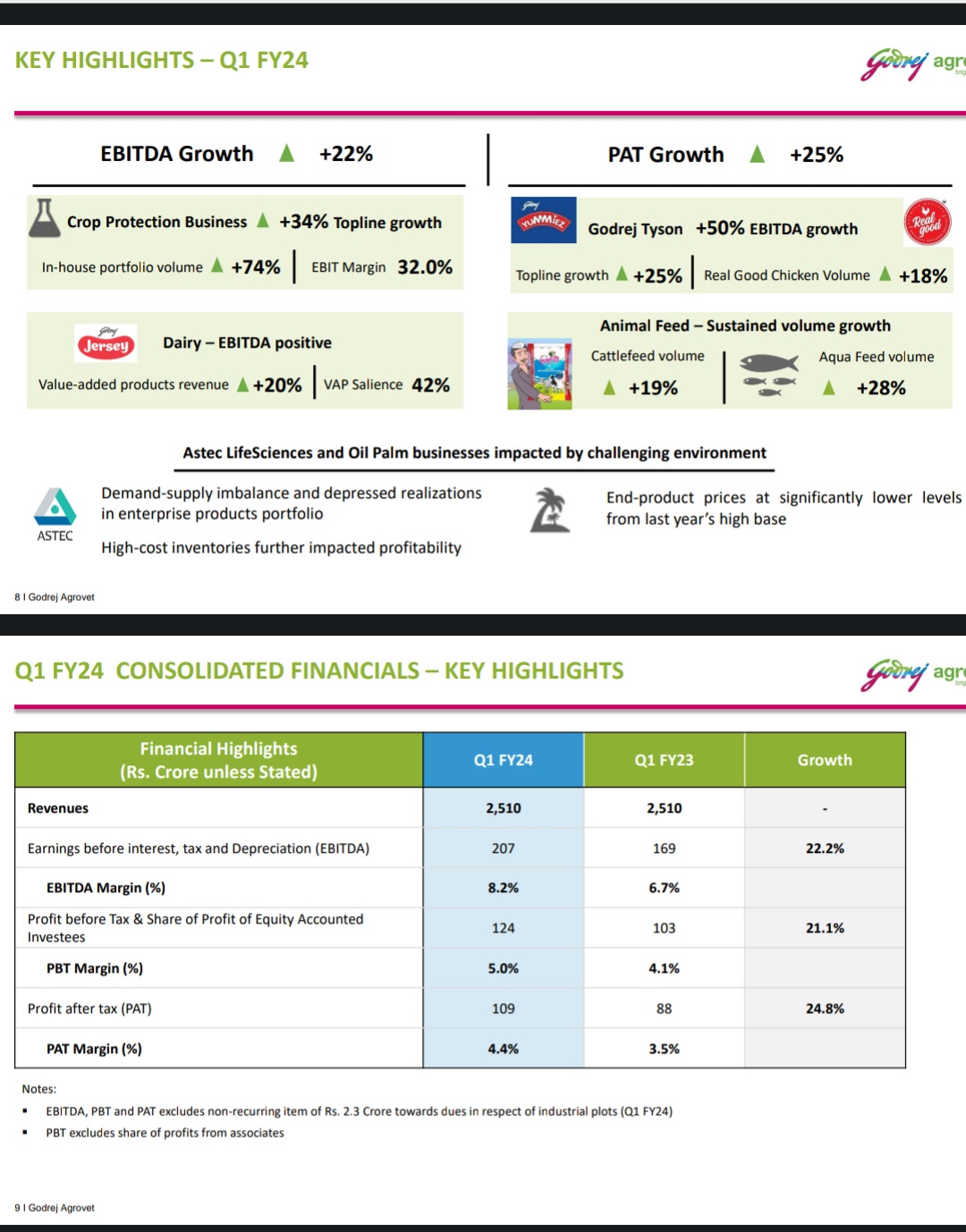

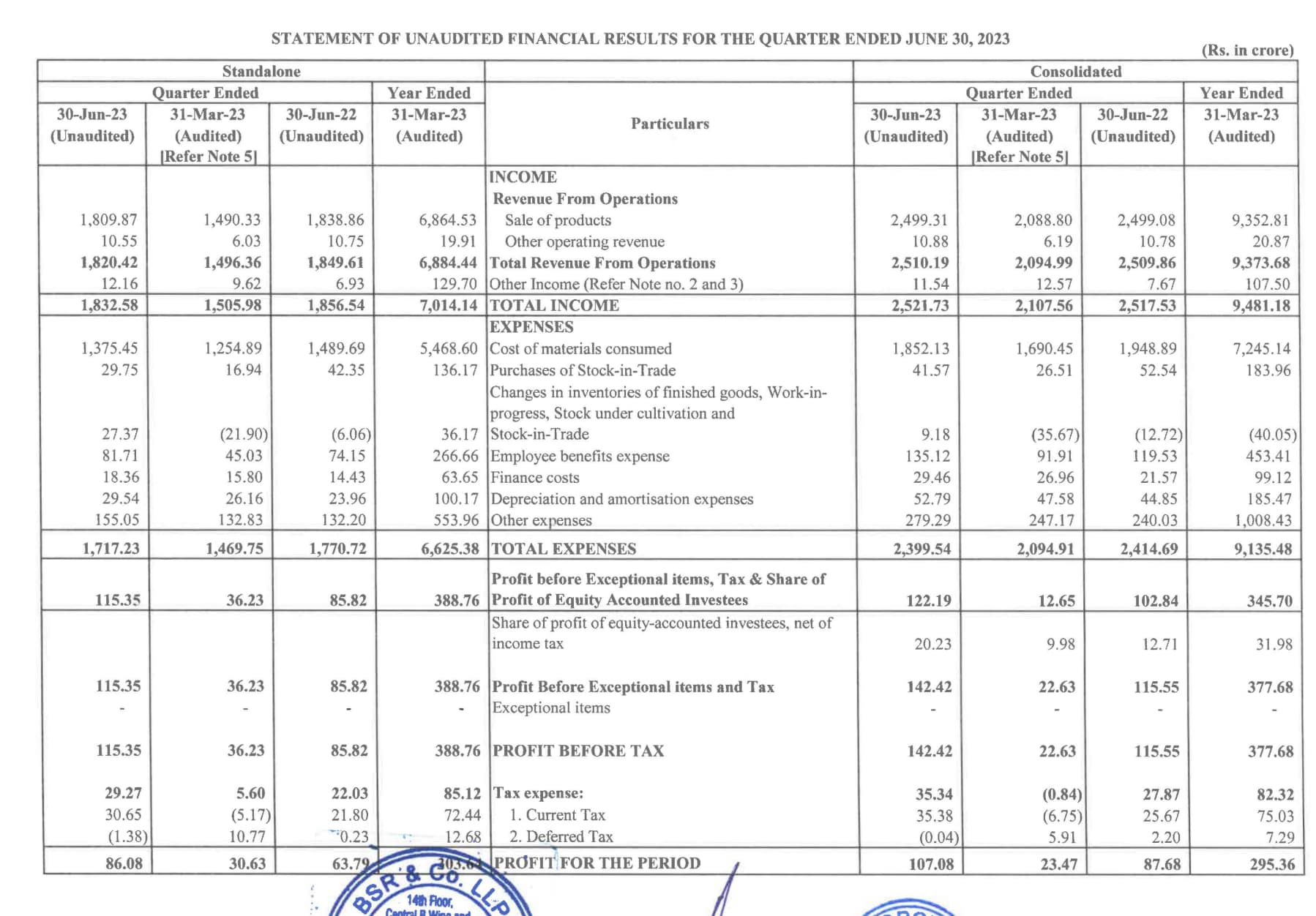

In my view, Results are actually good…

Their operating margins were shrinking since last few quaters… Finally there is a big uptick there.

Ebidta margins at 8.2% vs 6.7% YOY, it was about 4% last quater…

Going forwards one need to see, if they can sustain this margins and at the same time increase their topline…

They have guided for 11-12k topline this year, so I am expecting better sales numbers going forward.

The company is experiencing good traction on their crop yield enhancer product (Double) due to a change in packaging structure.

Rajavelu NK, CEO – Crop Protection Business, Godrej Agrovet, says “It is encouraging to get amazing feedback from our channel partners in Maharashtra, Madhya Pradesh and Gujarat. The overwhelming acceptance of our innovative packaging, coupled with the unwavering momentum we enjoy in the market, fills us with great optimism as we eagerly anticipate the upcoming Plant Growth Regulator (PGR) season.”

Previous guidance: FY24’s topline should be between 10 to 11k.

Guidances from concall Q1FY24:

Astec: Some products still have headwinds… Aiming to double revenue from CDMO biz ever year for the new couple of years… However, FY25 onwards target is 20-25% growth.

Dairy Biz (15% FY23 Revenue): “Hoping to be PBT positive in this quarter”

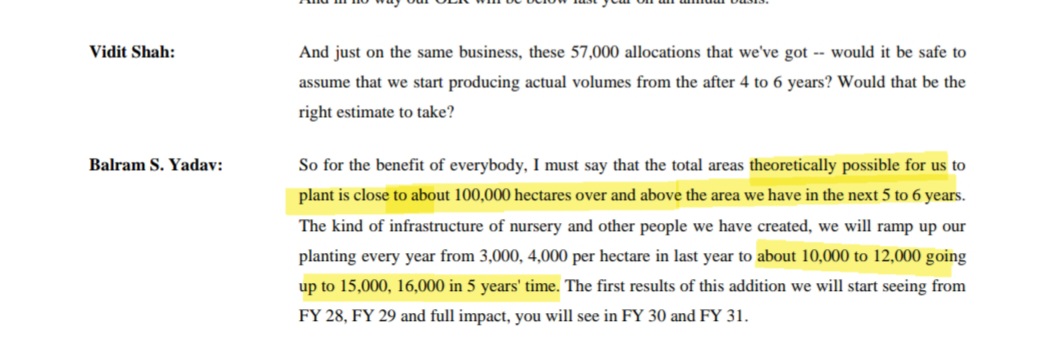

Palm Oil (13% of FY13 Revenue): “No way our OER will be below last year on an annual basis… Possible for us to plant is close to about 100,000 hectares over and above the area we have in the next 5 to 6 years. The kind of infrastructure of nursery and other people we have created, we will ramp up our planting every year from 3,000, 4,000 per hectare in last year to about 10,000 to 12,000 going up to 15,000, 16,000 in 5 years’ time. The first results of this addition we will start seeing from

FY 28, FY 29 and full impact, you will see in FY 30 and FY 31.”

Animal Feed (50% of FY23 revenue):

a) EBITDA margin should be back to FY22 levels - Q1FY23 is @4.2% (If I am not wrong them margin was 5ish% in FY22)…

b) Volume growth 8% to 10%

Demergers? “We are working on I thi… So I think we are moving in that direction there”

Link to transcript: https://www.bseindia.com/xml-data/corpfiling/AttachLive/9b353407-ab98-4ec9-b64f-633d7969c3c6.pdf

Godrej Agrovet

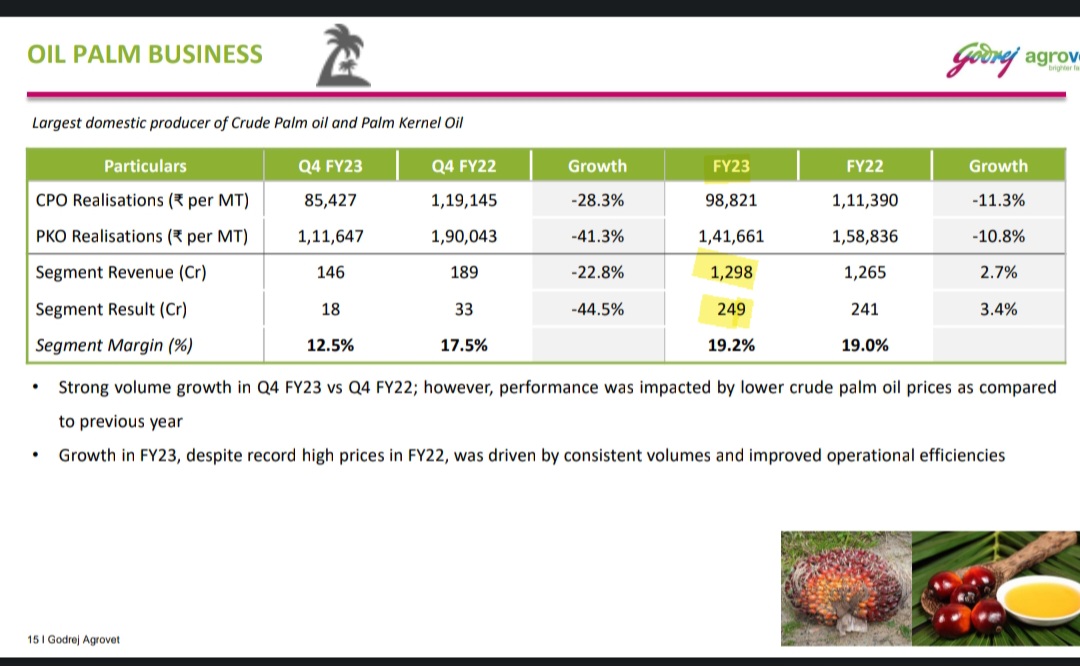

On Palm oil business - some interesting stats - from their concall.

Their existing Palm oil plantation of about 25k to 30k Hector

(45k Hector in total, but 60% mature )

This year Palm oil revenue: 1300 Cr, PAT of 249 Cr.

From new allocation ( in Odisha & Telangana )=Theoratically possible Plantation is close to 100k Hector

That’s about 4X from current levels ( 25-30 k Hector ) in next 5-6 year…

Moreover, Goverment is encouraging more palmoil production at home and thus, in my view, this allocation of land MAY increase going forward as well…

All in all, I am expecting significant jump in revenues from palm oil business going forward. Obviously not in short term but in long term.

Disc: Invested, biased views

The company entered into an agreement

Source: Link

Disclaimer: Invested (Portfolio). Not a buy/sell recommendation

Precision Fermentation and the Disruption of the Palm Oil Industry - Rethink Disruption

Will Precision Fermentation be a threat to the company in 10-15 years?

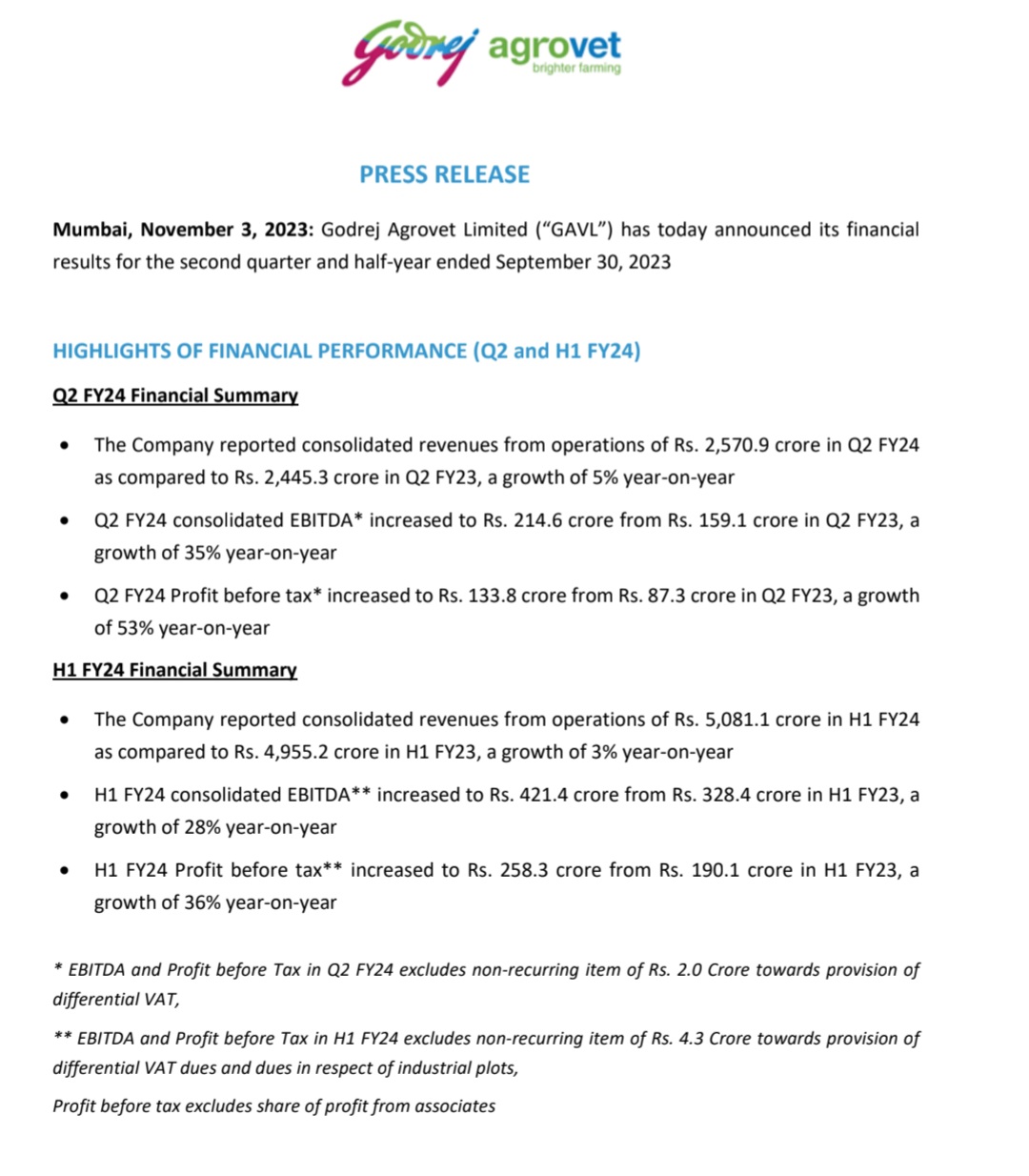

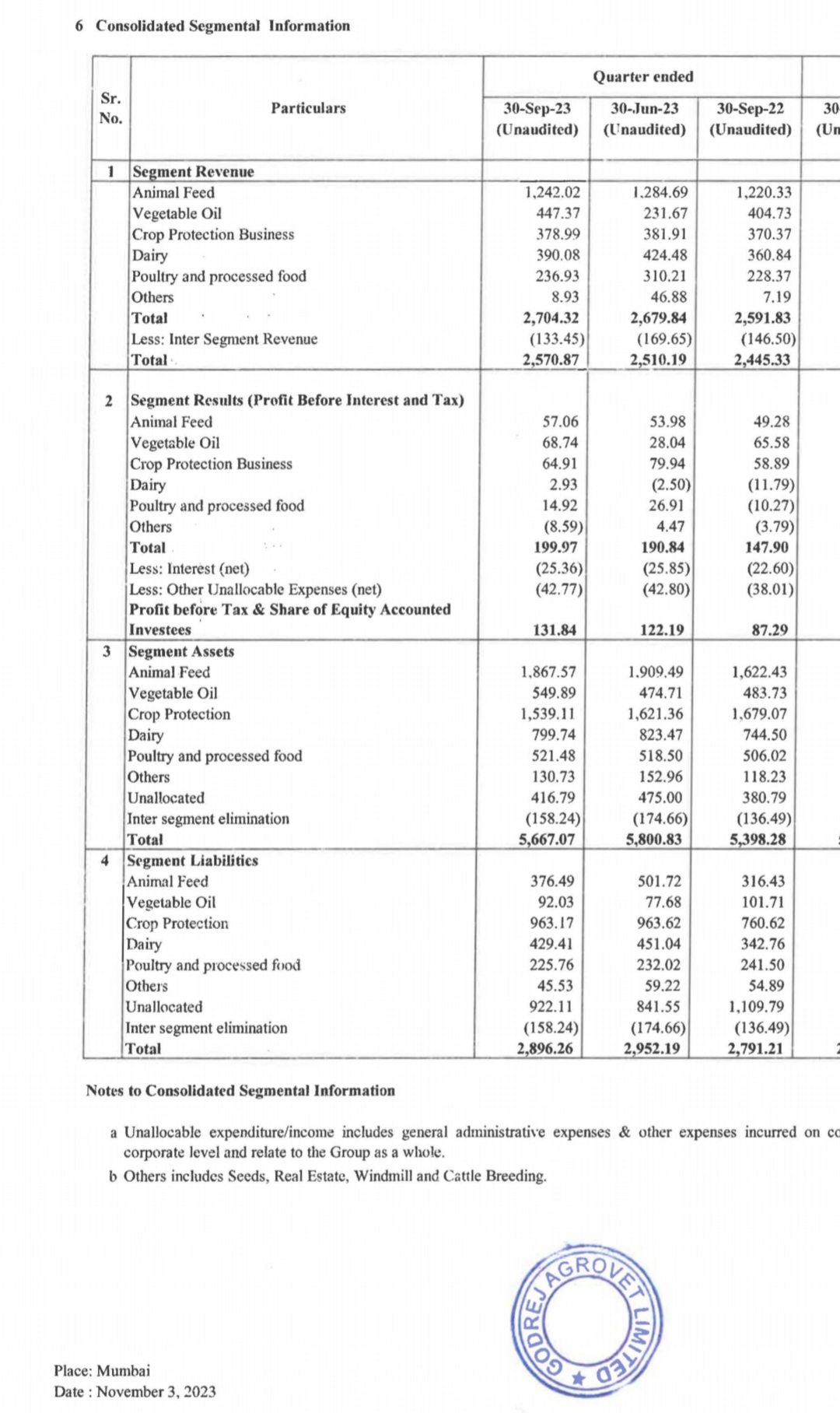

Good result by Godrej agrovet…

Revenues up by 5%

Ebidta up 35% YoY

PBT up 53% YoY

Dairy Segment has turned Positive this quater as well…

Disc: Invested. Added more recently as well.

What worked

What didn’t work

References: Presentation and Press release

Disclaimer: I may or may not be invested in Godrej Agrovet or its subsidiaries. I am not SEBI registered and this is not a buy or sell recommendation.

Godrej Agrovet -

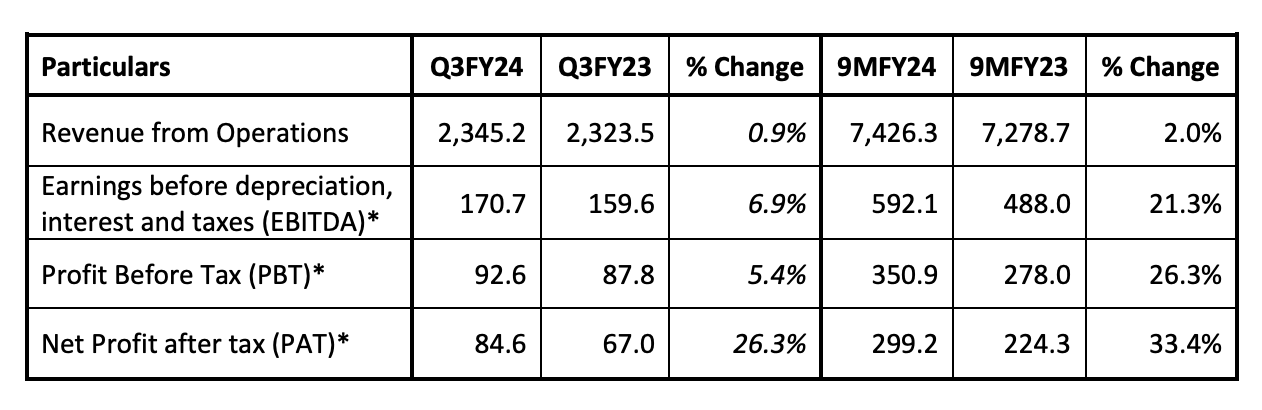

Q3 FY 24 concall and results highlights -

Revenues - 2345 vs 2324 cr, up 1 pc

EBITDA - 171 vs 160 cr, up 7 pc ( margins @ 7.3 vs 6.9 pc )

PAT - 85 vs 67 cr, up 27 pc

Segment wise revenues -

Animal Feed - 1291 vs 1272cr, up 1.5 pc

Vegetable Oils - 355 vs 362 cr, down 2 pc

Crop protection- standalone - 172 vs 100 cr, up 72 pc

Astec Lifeciences - 51 vs 117 cr, down 56 pc

Creamline Dairy - 366 vs 348 cr, up 5 pc ( sale of Value added products grew by 20 pc )

Godrej-Tyson foods - 223 vs 280 cr ( due sharp fall in live bird prices )

ACI-Godrej JV - 610 vs 600 cr, up 1.7 pc

Percentage of sale of value added products in the Dairy business increased to 36 pc vs 32 pc YoY

Investing aggressively behind Astec’s CDMO business. Should yield good results in medium term

Expecting better margins in Animal feed business in Q4 on the back of better realisations. Realisations for 9M FY 24 @ Rs 1435 / Ton vs Rs 1200 / Ton for 9M FY 23. Expecting these realisations to improve further

Witnessed healthy growth in cattle feed and aqua feed business. Was partially offset by de-growth in poultry feed business

Astec’s CDMO revenues got deferred from Q3 into Q4. Expect a better outcome in Q4

Seeing recovery in live bird prices in Q4. This should aid growth in Godrej Tyson business. Should also help in the recovery in layer feed and poultry feed business

Astec’s R&D engine should start firing as we go fwd. Should help in both CDMO and enterprise business. Expecting to grow CDMO business @ 30-40 CAGR for next few yrs

Astec’s enterprise business continues to be under pressure. The overstocking of agrochemicals in global mkts was to the tune of 12-18 months of consumption. Complete inventory correction may take some more time

CDMO business steady state margins are 5-7 pc higher than enterprise business

Disc : hold a small tracking position, biased, not SEBI registered

Godrej Agrovet -

Q4 and FY 24 concall and results highlights -

Q4 outcomes -

Revenues - 2134 vs 2095 cr, up 2 pc

EBITDA - 158 vs 87 cr, up 81 pc, margins @ 7.4 vs 4.2 pc

PAT - 66 vs 23 cr, up 180 pc

FY 24 outcomes -

Revenues - 9561 vs 9374 cr, up 2 pc

EBITDA - 743 vs 630 cr, up 18 pc, margins @ 7.8 vs 6.7 pc

PAT - 359 vs 295 cr, up 21 pc

Segment wise sales, EBITDA -

Animal feed - 5008 vs 4957 cr, EBITDA @ 231 vs 176 cr. Good growth seen in cattle feed and fish feed segments partly offset by poultry feed segment

Vegetable Oils - 1221 vs 1298 cr, EBITDA @ 173 vs 248 cr. This segment saw margin compression due lower output prices

Crop Protection - 815 vs 596 cr, EBITDA @ 254 vs 74 cr. Good performance driven by higher sales of In-House and In-Licensed products

Astec Life - 458 vs 628 cr, EBITDA @ NIL vs 89 cr

Business is showing signs of recovery in Q4 ( in CDMO segment ). First three Qtrs were very tough for the generic business

Creamline Dairy - 1573 vs 1501 cr , EBITDA @ 67 cr vs (-) 11 cr. Dairy segment witnessing a structural turnaround led by cost efficiencies and increase in share of value added products to 36 pc of total sales ( LY it was 32 pc )

Godrej Tyson Foods - 986 vs 1003 cr , EBITDA @ 71 vs 34 cr. Branded business grew by 15 pc in FY 24. Aim to take the branded business to 80 pc of the total before FY 28

Company seeing moderation in fish feed prices in Q1

Seeing some stabilisation in Palm oil prices. Don’t see them falling any further this season

Some new CDMO products are likely to be commercialised wef Jul/Aug at Astec Lifesciences. CDMO business should continue to do well in FY 25 as well. Yet to see a recovery in the generic business. CDMO business is likely to cross > 50 pc of total Astec’s business in FY 25

Creamline Dairy’s business hit an EBITDA margin of 8 pc in Q4. Aim to take the percentage sales of value added products from 36 to 40 pc in FY 25. Company’s focus continues to be on value added products

Expect good growth to continue in cattle and fish feed segment. Growth in poultry segment is a lot more challenging as the industry is much more organised. Animal feed business’s margins were highest in Q4. Company expects the same to continue in FY 25 as well. EBITDA / Ton for animal feed was 1525. FY 25’s EBITDA / Ton is expected to be much better

Yummeiz brand and Real good chicken operate at EBITDA margins of 35 and 15 pc respectively. The EBITDA margins of non-branded live bird business varies between (-) 25 to (+) 25 pc

Earlier the company was into plantation and extraction of crude palm and palm kernel oil. Now they also have solvent extraction and refining plants. They aim to keep adding value to this segment to de-commoditise the business

Consol Capex guidance for FY 25 @ 250 - 300 cr

Disc: hold a small tracking position, biased, not SEBI registered

with dairy business just turning around overall even a 15% topline growth and share of palm oil increasing the ROCE would show a good improvement in 6-8 quarters