hi…I liked this method…Can you please give me more info on this? how I can do it?

1 Like

Hi Mudit,

I shared the details in the post you’ve quoted. Is there anything in specific you’d like to know more of?

In general, I changed my framework from looking at moving averages, to thinking about valuations, earnings and eventually trying to time my entries closest to quarters showing growth. It’s for these reasons I wouldn’t be comfortable owning some of the companies mentioned in the title post of this thread

1 Like

I’ve been having private conversations with fellow investors off the forum, and they’ve contributed to me becoming a better investor over time. I thought I’d share how my approach to an industry has changed from the start of this thread, as I hope it will add value to those reading.

This may be obvious to seniors ![]()

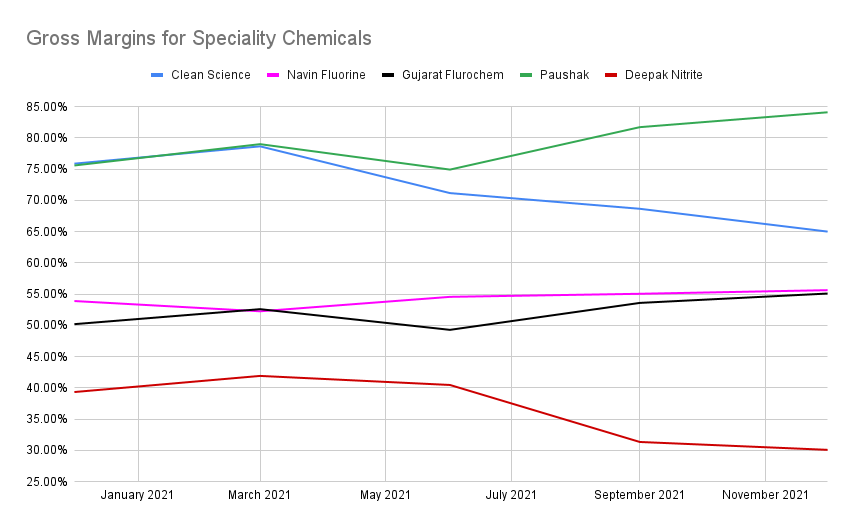

As gross margins are a measure of value add, I like to place companies into buckets based on their gross margin profile. In the chemicals space, this is one way to differentiate between a speciality chemical manufacturer vs a commodity player.

-

Paushak and Clean Science have the highest margin profile.

-

Speciality chemicals companies like Navin Fluorine, Gujarat Flurochem, Vinati (not shown) are in the 50%+ bracket.

-

By this metric, Deepak Nitrite’s phenol isn’t a speciality chemical. Revenues from other verticals / downstream products need to improve the gross margin mix into the higher brackets before one can make this claim.

-

In the Deepak Fertilizer thread, I had made the claim that TAN should be seen as a speciality chemical. Revisiting this through the lens of gross margins is difficult. Firstly, their TAN is a part of their subsidiary Smartchem, which had gross margins of 32% in FY21. However, this subsidiary also deals with other things like fertilizer subsidies, and trading, so one can’t isolate TAN’s gross margins.

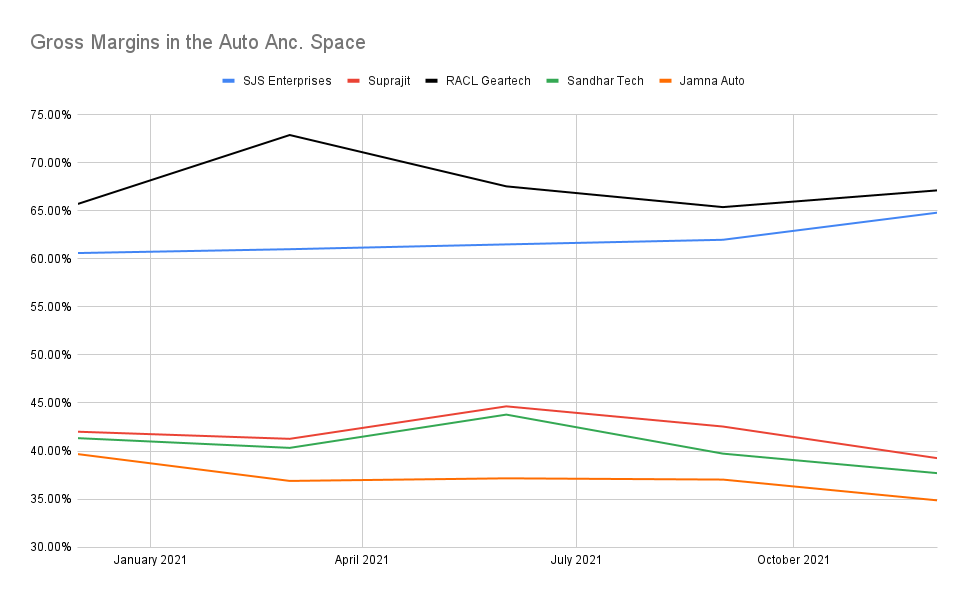

- Most auto ancs fall in the 35-40% gross margin bracket.

- RACL Geartech, SJS Enterprises and Sona Comstar (not shown) are amongst the auto ancs in the higher 60-70% bracket.

As gross margins are the maximum that EBITDA margins can reach, one can see how close/far the EBITDA margins are to the gross margin mix to see how much the company is losing to logistics and overheads (especially for export facing companies), and how much they can improve by cutting costs.

Thinking about Deepak Nitrite, I look at other companies in the sector with comparable gross margins:

| Company | Gross Margins | EBITDA Margins |

|---|---|---|

| Fineotex | 34.53% | 17.7% |

| Valiant Organics | 33.52% | 17.1% |

| Jubilant Ingrevia | 32.95% | 16.53% |

| Deepak Fertilizer | 32.61% | 18.00% |

| Deepak Nitrite | 31.33% | 21.92% |

| Laxmi Organics | 30.24% | 8.29% |

They have no right to be putting out such high EBITDA margins despite having gross margins of ~31%. A part of this is helped by being 80% domestic facing, but as an investor, it’s a nice sign of execution. If future capex into downstream products is margin accretive, one hopes that the company eventually moves into the 50% gross margin bracket.

I think Q1 of FY23 for Deepak Nitrite will continue to be painful, seeing degrowth YoY. It looks like the larger triggers for growth will play out towards the end of FY23 and in FY24. I’ll be using this time to accumulate a larger position.

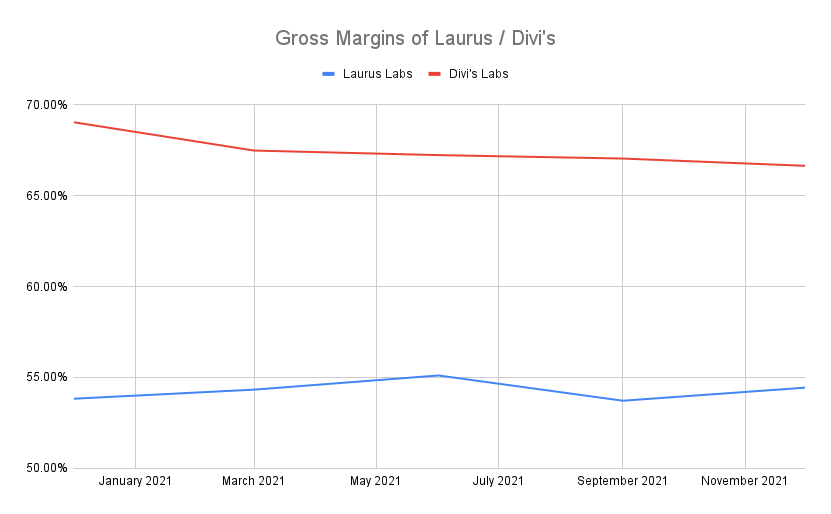

Considerations of gross margins in Laurus also show why it has a long way to go before comparisons to Divi’s are justified:

As they scale up the custom synthesis division, an investor hopes that the margin profile will look progressively different in two or three years.

On these lines, I’m studying two companies that could be bonafide speciality chemicals companies (the latter at very reasonable valuations): Chemcon Speciality, and Excel Industries.

33 Likes

Nicely expressed! It triggered a thought process in me would like to share, kindly ignore if it’s not productive…

I would relate to above that I also look for companies in simple words I would call them companies with “gaps to fill” as that is where the extra return may come…

We maximise our chances by choosing the worthy management & promoters who have this important task of filling this gap…(that is whom we think as worthy)

From my experience so far the crux lies in - The other important piece which we may knowingly or unknowingly miss. Infact even our chosen worthy management may miss this piece…it is the number of variables impacting the business for which we all have to bridge the gap…some or the other variable would simply come out from the back and ensure the gap remains or in worse case even broadens…also some variables remain dangerously unknown to all until they strike one fine day…

What we may do - either be thorough and along with that hope for the best… Or chose businesses with least variables, be thorough…and still…hope for the best!

2 Likes

Thank you. It’s an interesting post!

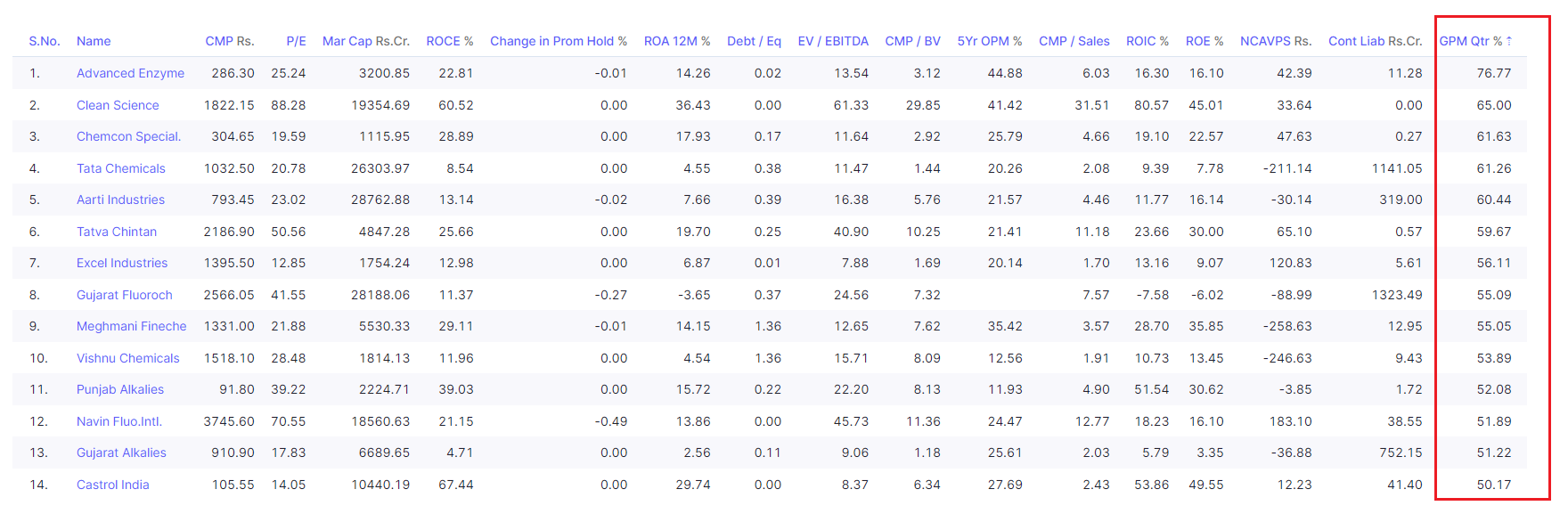

I filtered chemical cos with 50% gross profit margin in latest quarter (few cos haven’t posted Q4 results yet). You can see some bulk chemical names there as well. For a few, say, Meghmani Finechem, high gross margins have always sustained.

Yes, all things being equal, higher gross margins are better than lower ones but based on a co.'s strategic positioning, value addition may have different paths. For instance, a company can be the lowest cost producer, it may chose to get into specialty products or may be both. One thing we now know that the specialty chemical companies were not immune to margin contraction when it actually mattered. I would call Deepak Nitrite a bulk chemical company with scalability plus a diversified, niche product portfolio. And for me, that beats spec chem six days a week, twice on sunday. ![]()

4 Likes

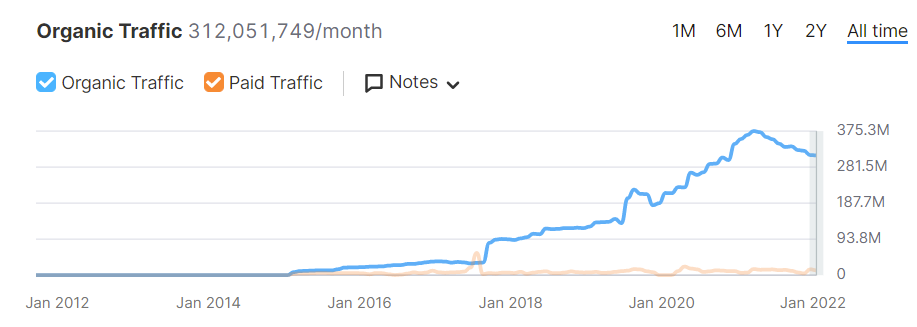

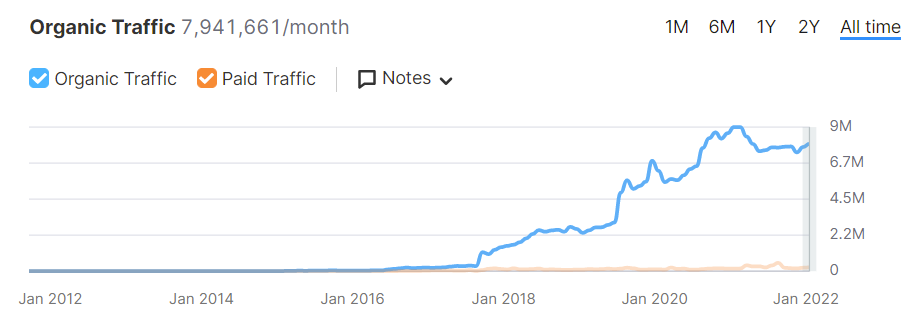

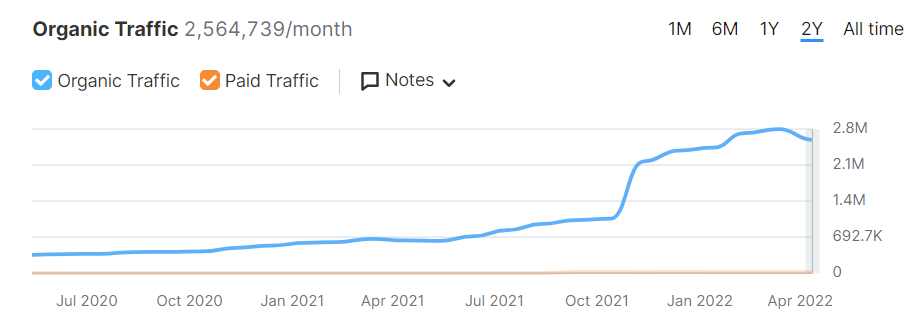

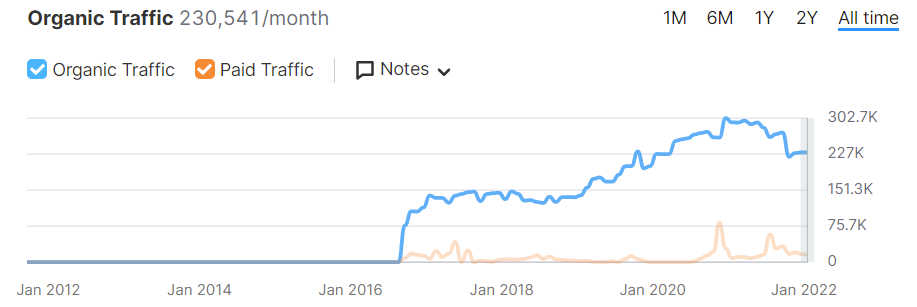

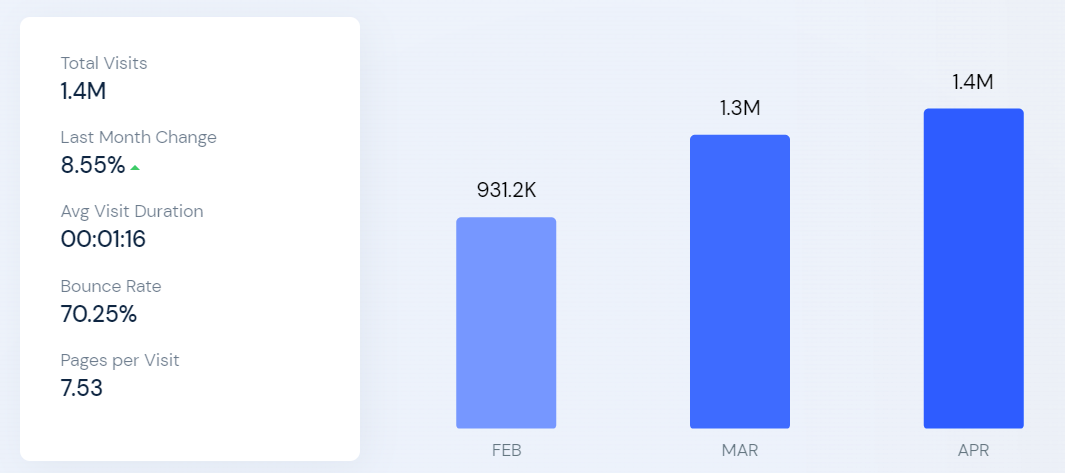

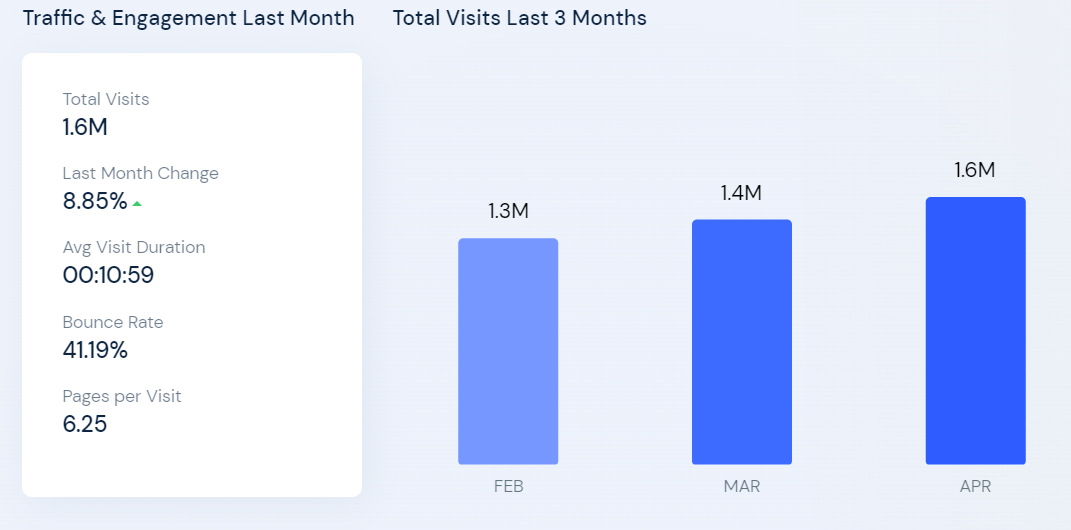

Came across a nice tool for analysing web traffic, and other data. Out of curiosity to see how covid affected e-commerce websites and how they’re doing right now, found some interesting insights on some listed companies.

Viewership over time

-

Amazon

-

Myntra

-

Ajio

-

Nykaa

-

Trent

-

Vaibhav Global (UK)

-

Nearly all of them went through a significant growth period post covid.

-

Amazon, Nykaa and Vaibhav Global have seen traffic fall off in the last year, while Ajio and Myntra have continued to see growth in traffic.

-

Trent and Nykaa have a long way to go before reaching traffic levels of an Amazon/Flipkart/Myntra.

Engagement

One can look further to see once someone visits, how long they spend on the site on average, and whether they leave without interacting (bounce rate)

- Myntra and Nykaa Fashion are almost identical on clicks and bounce rate, but people spend longer on Myntra than Nykaa Fashion.

- Trent has seen a recent surge in traffic in the last 3 months, but the quality of traffic is subpar. On average, 7/10 visits to the site end immediately with no interaction, and the average time spent on the site is a minute. They look the worst of the lot.

- Vaibhav Global ranks top for engagement metrics, with a 40% bounce rate, and a whopping 11 minutes spent on average: One should dig deeper to understand why they’re able to keep people engaged for this long. I’d bet it’s the $1 auctions that they offer.

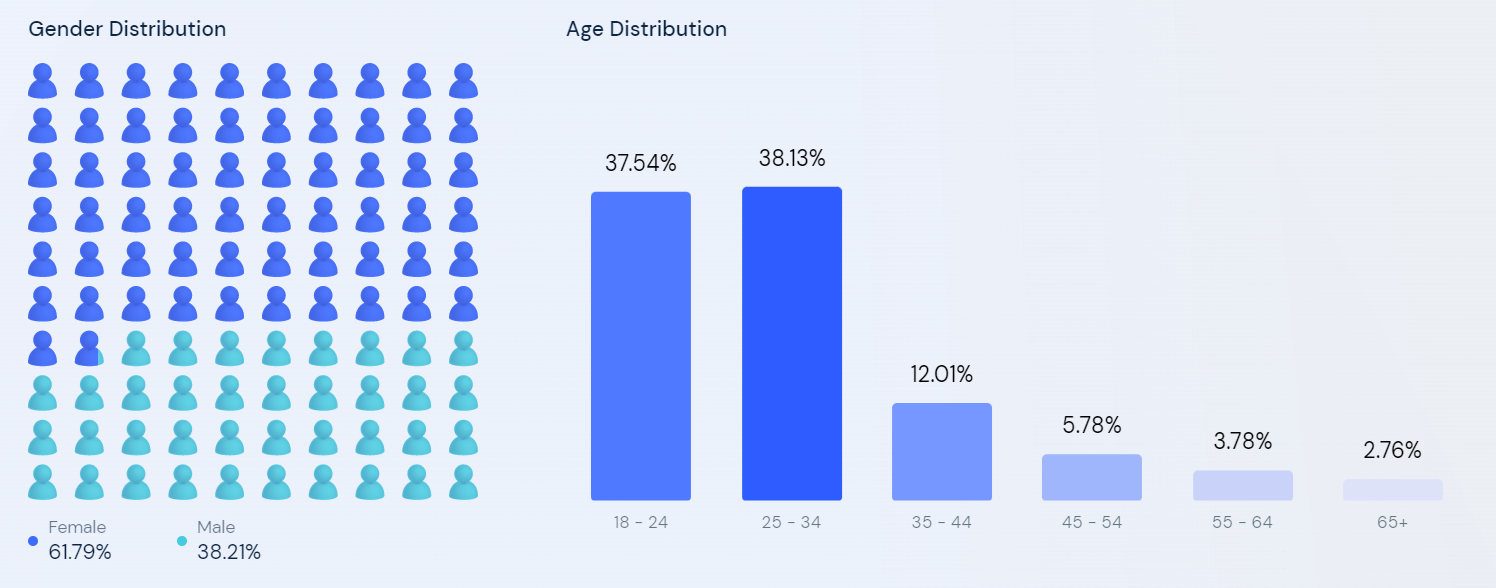

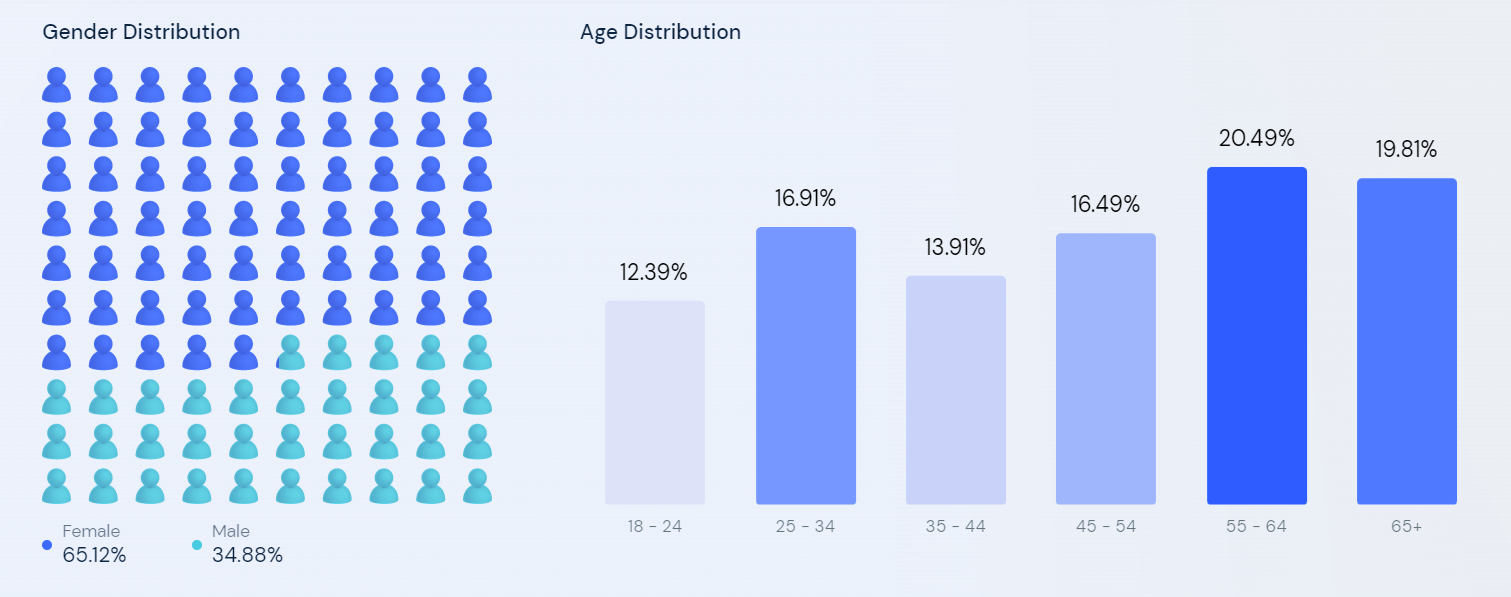

Demographics

- Sites like Nykaa, Myntra and Westside share common demographics of age distributions - they’re primarily popular with the younger age group.

- Vaibhav Global is the clear outlier in the demographic basket, seeing an almost equal split between age groups with a bias towards older viewers.

Clarifications:

-

Sites differ in counting traffic. Most articles on the topic reflect that tools like these often underestimate organic traffic.

-

Data differs in counting desktop vs mobile and app users which partially explains difference in numbers between pictures.

-

Data shouldn’t be treated as accurate for any investment decisions, but just an exercise out of interest.

-

Websites are semrush.com and similarweb.com should anyone reading want to look for themselves.

23 Likes

Excellent insights (as always), Sir.

- For Trent viewership chart, I think you have accidentally chosen 2Y instead of all time

- The Nykaa viewership chart is Nykaa BPC or Fashion?

1 Like

Hi Malhar ![]()

This was deliberate, you’ll see that viewership wasn’t noteworthy prior to that time.

Nykaa cosmetics in the first chart, Nykaa Fashion in the second.

2 Likes

Some thoughts through the last month of volatility.

-

Post market volatility, other companies in my watchlist have corrected significantly and offer equally good risk/reward. I have brought weight in AB Capital back down again to neutral. I couldn’t have timed the correction happening (or the piece by the Morning Context), and the company has delivered an excellent FY22.

-

The correction has of course been painful in some names, and I have thought about whether I’ve made a mistake constructing a small/midcap heavy portfolio. However, I think I’d lose more sleep if I owned fewer shares of Ugro or PDS, than I’d lose in fear of a drawdown. I remain stock specific in my approach, and if all the hard work results in a portfolio that delivers strong earnings over my investment horizon, that’s all I have in my control.

With the exception of Laurus, I don’t think any of the companies in my portfolio are expensive, or have a lot of growth priced in. -

I have initiated a position in Satia Industries at a share price of 115. The thesis has been covered very well in @Rafi_Syed’s excellent thread as well as by @kalpesh4430 I realised that the Satia thesis shares a lot of similarities with that of Filatex, but is the better investment overall.

Both have large capex plans but Satia’s has come onstream already. Both have a pipeline with a high margin optionality, and Satia doesn’t have an overhang with the IT department, nor a history of issuing warrants. -

I’ve deployed around 6% in cash, will be deploying 1-2% every week going forward.

- I have invested in a farm. An intelligent young investor introduced me to KPI Green, and I’ve been encouraging said person to write a company thread here on the forum.

Being deliberately sparse with details, farm operates out of an 850 acre plot of land in Gujarat, and produces solar power here. They have two business segments, where they either produce power on site, and sell it over the grid, or they develop, operate and maintain captive power plants for companies like UPL, Larsen, Cadila, over long term contracts.

Thesis is of a high growth company (that has used debt to build capabilities), with 50% EBITDA margins, and slowly improving PAT margins over a longer term as the debt profile reduces. While the share price has run up significantly, valuations are quite reasonable. I have taken an initial postition, and will slowly scale as I understand the longevity of the business model.

I’m happy to invite comments and discuss further, but I encourage those reading to look over the company for themselves: KPI Green Energy Ltd financial results and price chart - Screener

Next week, I will write an overview of how all companies in my portfolio performed during Q4.

20 Likes

Amazon is completely changing the retail landscape yet again. What’s surprising is that it’s through a physical brick and mortar store, not an online initiative.

They’ve opened 46 such stores, and one recently opened in my neighbourhood. I visited yesterday, and came away amazed.

There are no queues of any kind

One has to scan a QR code from the Amazon app to enter. (Look closely to see the scan gates in the picture above)

Once inside, it’s immediately evident that this is far different from a normal grocery store. Amazon has developed technology that uses cameras and AI/ML to track what items you take off the shelves (and put back), and automatically adds it to a virtual cart it keeps track of.

(Can you spot the cameras monitoring the shelves?)

You take items off the shelves, into your own bag, and can walk out of the store immediately. There is absolutely no scanning or queueing up to bill, translating into a seamless shopping experience. It’s so jarring infact, that I felt like I was shoplifting as I walked out of the store.

However, no alarms rang as I walked out, no security guards stared at me questioningly, and I received an accurate bill for all 12 items I purchased in my inbox, 30 minutes later.

Now put on your investor hat. Immediately, a lot of things stand out:

-

This store has the fewest number of employees needed to operate. I had a quick chat with the sole person helping people scan their QR codes; stores operate with as few as 3 employees sometimes, and larger stores have options like fresh food / deli counters which require more people.

-

Competitors like Sainsbury’s / Tesco easily have 3x the number of employees present (Atleast two in billing.)

-

The last revolution here that cut costs, and minimised queueing was in a self checkout counter. Uniqlo took this further by introducing technology that scans your entire basket in one go during billing. Amazon has completely taken out the need for any physical billing, and the offering is best in class. This is probably the only store in the world, where shopping physically is as seamless as shopping online.

-

The selection of products are almost completely own-brand products: dairy, veg, home essentials, the bakery. This is standard for any supermarket, but drives home the idea that they’re in complete control of inventory selection and costs.

In a cross section of products that one would usually buy in a week’s shop, see below how even more specialised products are own brand: they have ready meals, a selection of fruit, even my favourite buffalo mozzarella from a region in southern Italy. I would love a peak into the data that goes into product selections on the shelves: almost all of are the fastest moving items, with brilliant special selections for variety.

-

Amazon plans to scale the number of these brick and mortar stores over the years. They’ve chosen locations for these stores very smartly, and use up space in existing buildings. Prices of products are very low, and the experience is much better than a Waitrose that is located just opposite. I would imagine that the experience is so good that they’ll win market share easily.

-

What’s more, is that they can also use this to cross sell other products. Stores are equipped with Alexa, and you can ask information about products in stock, and also serve as offline advertisement for Prime.

-

Amazon now owns both ends of the grocery pyramid in the UK. They own a high end grocery chain in Whole Foods, as well as the convenience retail stores of Amazon Fresh. It’s absolutely amazing to see how yet again they find a way to innovate and dominate a market one wouldn’t immediately attribute as a strength.

-

Note how it’s also difficult for competitors to adapt quickly. To replicate the experience, you need to develop technology that works without bugs. Then, in order to add in camera infrastructure, you’ll need to rethink the entire ceiling + aisle configuration that’s currently organised according to their own consumer data. To rehaul this, you would need to shut the stores for 14-30 days to implement these changes. Amazon has rolled out new stores with this put into place. I think for these reasons, it’ll be a while before the technology hits Whole Foods.

-

Imagine the confidence to rollout this technology which operates 7 am - 11pm, 7 days a week, 365 days in a year. If I developed this, I’d agonise over bugs and loss of customers should there be any downtime / failure in recognising a product. There must be many well coded redundancies in the offering. Luckily, I have a few friends working in this space in Amazon. Will shortly write an update after reaching out.

I expect this store to be the highest margin small scale grocery store in its peer group.

44 Likes

Amazon Fresh: Part II

I reached out to a close friend who worked on the store’s machine learning tech three years ago. Sharing because I really enjoy stories of good (in this case, groundbreaking) initiatives taken by different companies.

In the last post, I’d written about cameras monitoring the shelves to notice what you take off them. The story I got was far more detailed. The secret to this tech isn’t the cameras alone! Instead, it’s something I missed on my first visit.

I went back.

Does anything stand out in this picture?

The shelves are weighing scales! They’ve carefully made a system that clocks in a change of exactly 432g when you pick up a box of pasta, and the cameras monitor who is picking up the items.

-

Every single shelf in the store is based off this tech. My friend working on this said it sounds easy, but the underlying tech is far from.

-

Shelves are incredibly sensitive to weight. Let’s say you pick up some loose veg from one of the shelves. Amazon knows that the potatoes you picked up are exactly 730g and can bill you directly without needing to go weigh a second time.

-

On the other end of the (ahem) scale, they are accurate enough to know when you’ve picked up a single bar of chocolate, or even some leaves.

-

Here’s where the cameras come in. In the picture above, two different leaves with different costs have the same weight. The cameras have a GPS of the store, and know based on your position that you picked up some Parsley. Or, out of a bunch of different birthday cards, which exact one you picked up.

-

What’s even more amazing is that I visited with my partner. Whatever items she picked up were also added on to my bill. Cameras recognise two people that have entered with the same QR code!

This tech was initially tested out of a small store near their HQ in Seatle. Friends pressure tested the system by juggling fruits and tossing cans of peanut butter to each other to see how cameras would react.

Back on with the investor hat.

- Amazon isn’t planning on dominating and running other grocery stores out of business. Far from it. They want to sell this tech to Sainsbury’s and Tesco! Now, in the previous post, we remarked how the downtime needed to add in this infrastructure would make it hard to replicate. Here’s Amazon’s solution: a cart that localises the weighing scales and scanning.

- This makes sure other stores don’t need the same infrastructure. Cart bills you in real time as you add / remove things from it, and you can walk out of the store immediately in the same way as Fresh stores.

- The ability for them to orgnise their shelves is powerful. It’s done in a way that “makes you look around for knick knacks”. In addition, they see what you move towards, when you change your mind, and what your habits are.

All of this is a great way to capture anonymised structured data, which is great for training ML models. Would be very expensive to get this data otherwise.

I also got an interesting tidbit: what Amazon is planning to roll out next for these stores.

A palm reader that scans the ridges and contours of your palm to create a unique signature. They then match this to the payment details stored on your account, allowing you to pay with your palm!

While this is a techincal leap from being able to pay with your phone, I wonder what the reaction would be to incremental convenience. You can walk out of your home with only your keys, and not worry that you need a wallet or a phone.

Today, I’m going back for some mischief making: to take items off one set of shelves, and leave them on an entirely different shelf to see what the system does. There is a series of videos on YouTube of people gaming the system by bringing in dupes of the same weight.

Disclosure: I’m weakly invested in Amazon through ETFs in family accounts. Thanks to @gurjota

for a series of great posts, and to @Lynch for pointing them out in the first place.

30 Likes

That scale based technology, I think this is already exist, when you scan an item and you don’t put in the bagging area, the till won’t allow you to scan the next item. But in this case it is more advanced. Regarding palm sensors, we recently moved into a new building and our office is equipped with these, you just wave your hand you don’t have to carry the employee badge anymore. One side things are getting super convenient for customers other side we are handing over our life to technology. And at the same time too much automation leads to less human resources thus less jobs in the market.

Basic needs of human being are

Roti - Mass production of the food (Vertical Farming, Genetically Modified Foods , CRISPR based agriculture )

Makaan - We are talking about 3D printed homes

Energy - Current Installed capacities are based on Nuclear Fission , where are Nuclear Fusion can produce more

Healthcare - Tele Doctors , Robotic Surgeries

This list goes on …

Sweden is already trying a model where they are asking people stay at home and do whatever you want to do we will give you fixed income ![]()

8 Likes

Royal Carribean Cruises Limited

Have you ever loved, hated, and admired a company all at the same time?

This week, I was on RCL’s newest cruise liner, launched a few months ago, sailing from Rome to Greece and Turkey. I loved the experience as a consumer, admired the diversity and policies towards workforce, but as an investment candidate, I hated it even more than an airline company.

The ship is among the Airbus A380s or Death Star of ships.

-

It has 16 decks, 15 restaurants serving global cuisine, and 2100 cabins for passengers.

-

Onboard there is a 180,000 litre simulator for surfing; an indoor skydiving wind tunnel; a large sports complex for basketball, football and bumper cars; a rock climbing wall, and more.

-

Company has invested heavily in entertainment, with live shows, concerts and comedy onboard.

-

Has an app which allows guests to organise activities and make reservations onboard seamlessly.

-

Flagship offering is an impressive theatre room costing $38 million. Has 18 projectors that fill the entire room with images, and screens mounted onto moving robotic arms. Even the windows have screens that turn the room into 270º of immersion.

The ship cost Royal Carribean almost $1 billion, and took 6 years from planning to construction.

Things I don’t like about the business

- Cruise companies require enormous amounts of working capital, much like airlines. A large portion of the food and activities onboard are included in the ticket cost (unlike hotels). In my opinion, the single biggest reason that the business is unattractive is due to diminishing marginal utility.

-

For first timers, the activities on board are new and refreshing. However, for the next five years, anyone who goes onto the Odyssey of the Seas will eat almost the same food as today, and have similar activities and an experience as I did. This is something one will only do once.

-

For a different experience, one would need a different itinerary, or a completely different ship. This is where it becomes complicated:

-

Summer destinations are the most popular for US and EU passengers. Revenues for the ship companies fall towards the winter season. To compensate for this, companies offer destinations in the southern hemisphere (South America, Australia and Africa), which recieve warm weather during December.

-

Not all ships can sail to all itineraries. Some require smaller ships, or there is an overlap of destinations sailing from the same port.

-

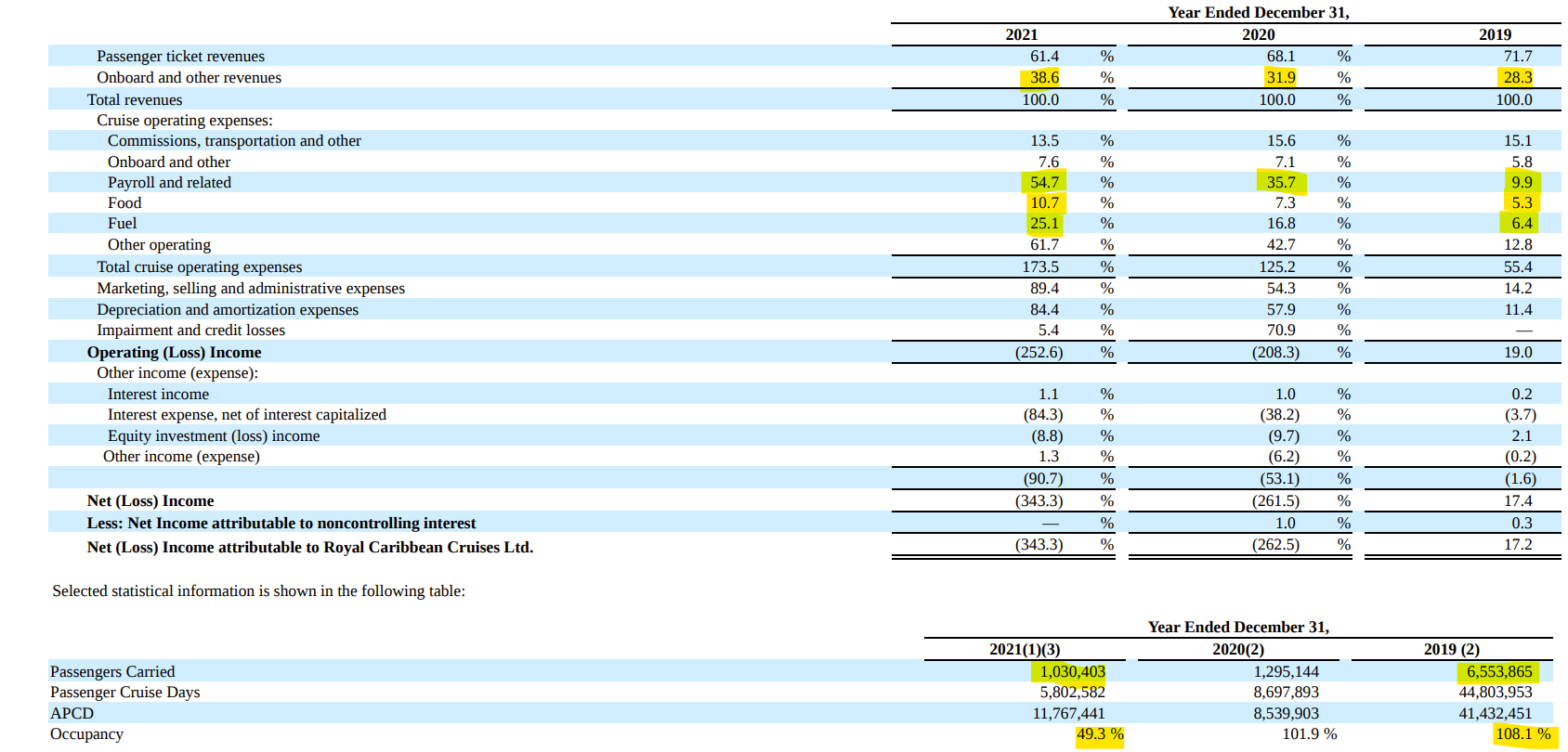

For a different itinerary, one would need to fly to a completely different port of sailing. This means added time off work, costs, and inconvenience of transfers. There are many more itineraries on offer to those sailing out of the US. This is reflected in the revenue breakup:

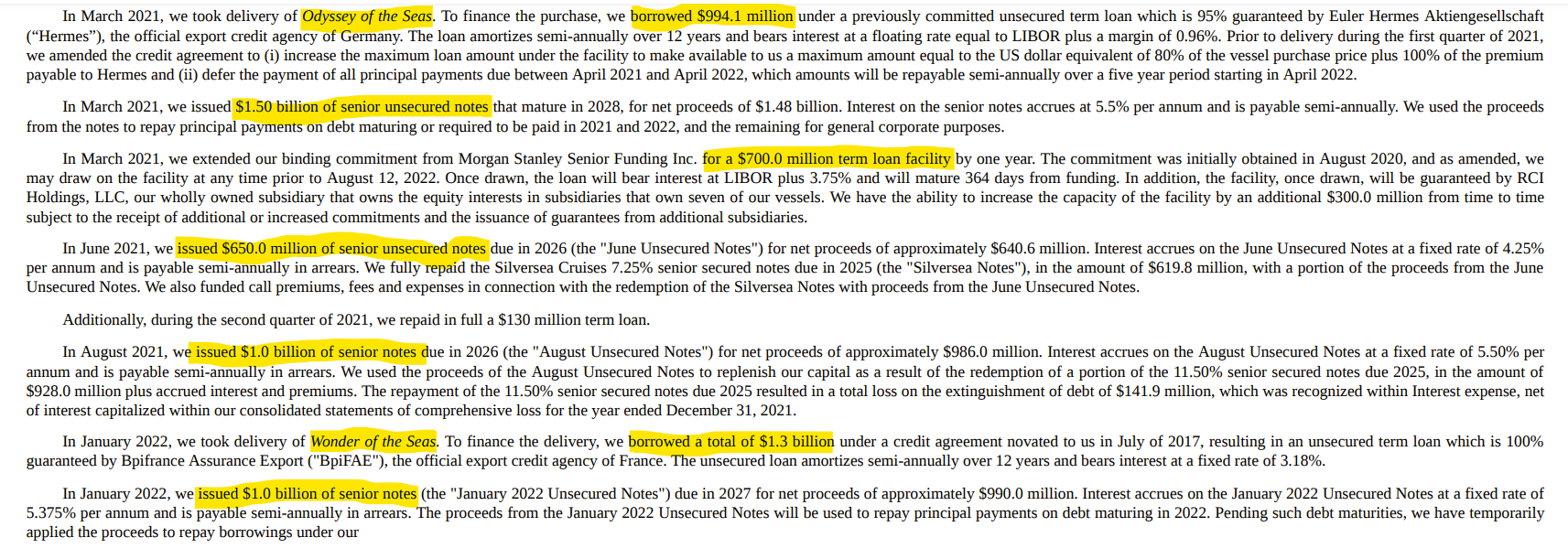

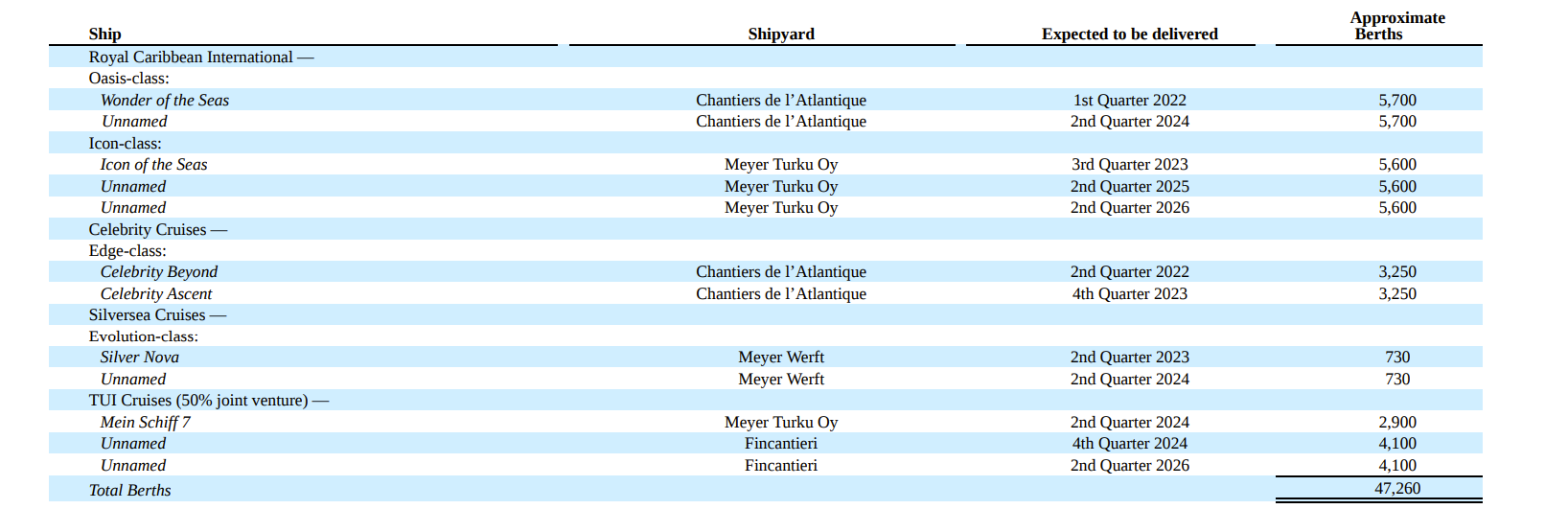

- Company continually introduces new ships - bigger, more advanced, more efficient - in order to save on costs and attract clients with the offering of sailing on The Largest Ship in the World. This needs large amounts of debt:

Much like chemical companies do debottlenecking instead of new capex, cruise companies often refurbish older ships every five years, as it is cheaper to upgrade technology and upholstery than it is to build a brand new ship. As an example, a refurbishment of one ship cost $150 million, and lasted 50 days. Here is their new ship order book:

While debt on it’s own is not a problem, a number of cruise companies took on much more debt to stay afloat (pardon the pun) during covid. What that has lead to now is significantly higher debt/equity for most cruise liners:

Now their game begins of having enough liquidity to make payments that come due ($8 billion for RCL in 2023), and refinancing loans to better terms. UBS’ analysts estimate that it’ll take the company until 2026 to bring debt back to pre covid levels.

Insights from Expenses

Note a few things in the expenses:

-

Company has focused on getting customers on board to spend more, and the percentage of onboard spending compared to overall revenue has increased 10% in two years! More on this shortly.

-

Payroll has increased as a % of revenue, but I believe it’s due to lower passengers carried overall compared to the crew in the last two years.

-

Stocking food, and resupplying from ports is a logistics enthusiasts’ dream. In a week, 60,000 eggs, 8,000kg of potatoes, over a million beans of coffee and similar quantities of meat are consumed. Then there’s the washing of tens of thousands of cutlery, bedsheets, etc. Sourcing managers on board the ship maximise costs by ordering local fresh produce when the ships dock, and buying different kinds of ripeness to have control of menus.

-

Fuel costs have risen significantly in the last two years, but will be helped by higher occupancy rates. RCL has always had over 100% occupancy in its ships pre covid. Management has been complaining about food and fuel supply chain problems.

Growth initiatives, and things I like

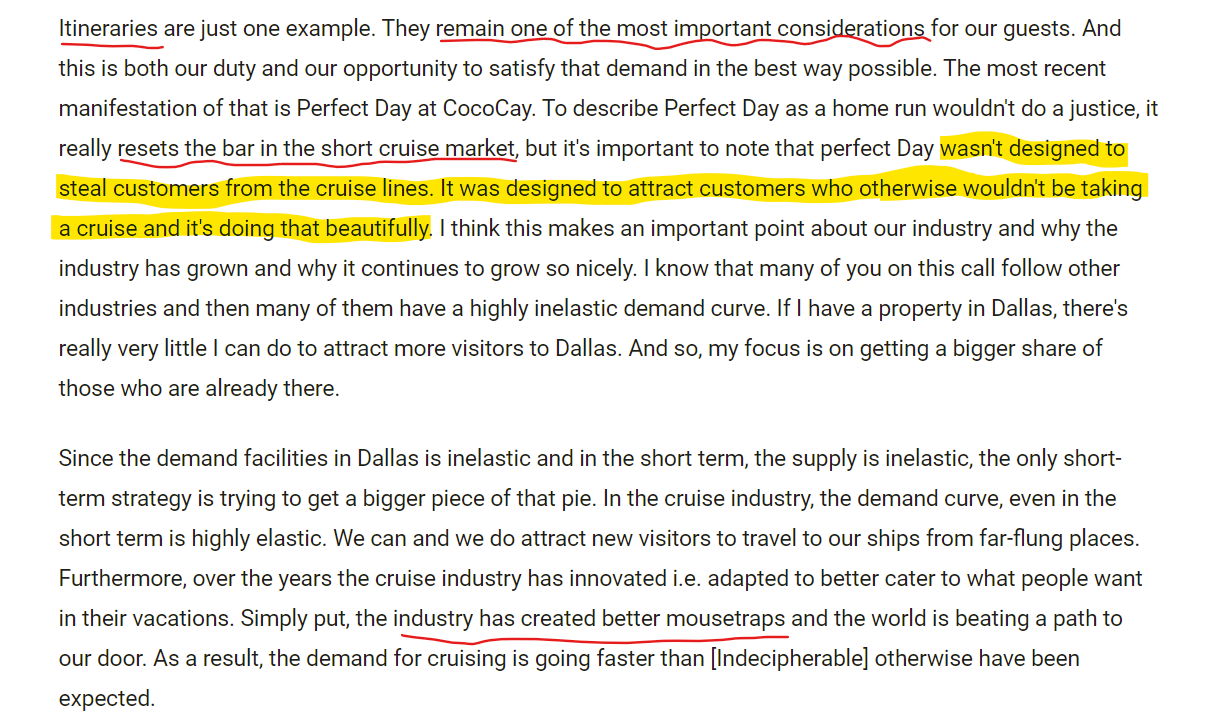

- Private Islands

Royal Carribean spent $250 million dollars to build up a private island in the Bahamas (they have multiple today).

Management’s explanation of the initiative is a fantastic argument:

Royal Carribean offers 230 weekend getaways to islands like these. They’re in complete control of the costs, and push customers to spend more on activities. Activities include high margin items like cabin rentals over the water, which it offers at $500 for a day.

As a bonus, they also allow kids under 12 to sail for free in order to win tickets from families who would otherwise need to look for sitters.

- Reliability

Competitors like Norweigian Cruise Lines have shut down restaurants on board in order to save costs, or have cancelled cruises altogether due to staff shortages. In addition, there was a large fire onboard a Carnival ship recently.

Royal Carribean has continued with its itineraries, and claims bookings are much stronger than competitors. In previous concalls from 2019, they’ve expressed regret at slowing down growth/orderbook when recession was looming. It looks like a company that steadily captures market share from competitors, and becomes stronger with every downcycle. The unique problem at the moment is the lifetime high debt.

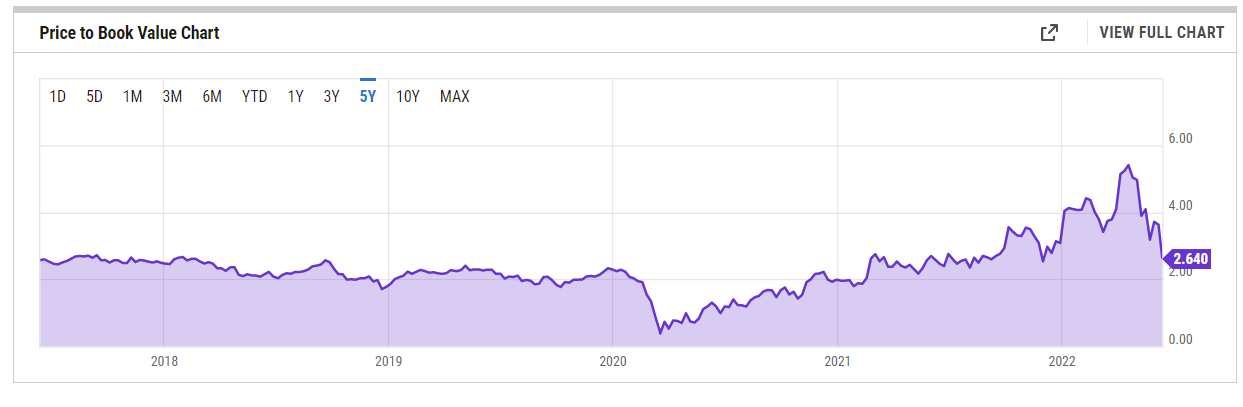

While the stock price has fallen 50% in the last year, valuations are still above historic levels due to the deteoration of book value in the last two years. Company has almost seen a stable 2x price to book in the years before Covid.

At current valuations, it still looks to be a high risk investment for little to medium reward. Pre covid operating margins were around 20%, with low teen RoIC. Should it fall much closer to book value, I’d be interested then as an investment opportunity.

As of now, I had a lot of fun learning about a new industry, and talking to people with all kinds of responsibilities onboard.

Will write about my experience with the unique counterfeit market in Turkey in the next post.

26 Likes

Hi sir, thank you for your contribution to this community. Please may you put up your updated current PF and if you think a recession is coming.

Thanks

1 Like

Some lessons from the last month:

- We’re biased in thinking our investments are privileged.

This month, I’ve seen more posts on how smallcap companies are a lot more sensitive to liquidity than those in the Nifty, or asked if I’m worried investing in them because the smallcap index has either run up sharply, or is volatile.

My reaction was that I don’t associate my portfolio to the smallcap index. They’re not smallcaps for the sake of being smallcaps - but rather fall in the bracket of being under owned with triggers I believe will play out. My portfolio is privileged: not random companies that happen to belong to the smallcap index. This is the bias. (Objectively one can answer this by correlating the portfolio returns to the smallcap index, or calculate beta, but I haven’t felt the need for those data points.)

Has the allegiance to earnings and valuations paid off in a tough market environment? Not entirely, these companies are as volatile as the rest. It didn’t matter if Ugro’s earnings have grown 292% this quarter, or Deepak Fertilizer at 144% YoY growth. Both are down from all time highs. I can’t choose what the market rewards, and when it chooses to reward a company, but I hope that probability is on my side.

There was a brilliant piece written a few days ago by Kedar sir on his experiences across two different cycles:

https://congruenceadvisers.com/blog-and-musings/f/a-tale-of-two-cycles

Some excerpts that resonated with me:

This said, for my highest conviction ideas, I’m not at all bothered by the drawdown. This brings me to:

- No one hands you conviction in a stock, it can only come from yourself.

To me, conviction is a function of time that I spend understanding the company and industry structure. It may take less than a day to form the outline of a thesis (Krsnaa’s pointers stood out immediately), but over a year to understand the finer details.

For example, I got PDS’ business model completely wrong in the title post of the thread, and it took a long time to understand how they headhunt entrepreneurs. In Ugro’s thread, we completely misunderstood the effect of co-lending in the initial days, and the early part of the thesis was on their ML models. It just isn’t possible to fully understand a company in a week.

Moreover, I’ve realised that I’m happy to stomach 10-30% drawdowns in certain companies, but not others that are either a tracking position, or I’ve been following for less than a quarter.

Then, the game is to keep turning over as many rocks as I can find, and read about different businesses. Work done 6 months ago in companies and watchlist are immensely helpful now, and maybe somehing I study today will pay off a few years from now.

Mentally feel like this goal has been met, and will be renewed for Q1FY23.

The companies I’m studying at the moment are: RPEL, Shivalik, Prevest and Gokaldas (at the behest of Sahil who also made me realise how much more work there is to be done on PDS), Exide and Artemis (at the best of @Lynch).

A big change in my method has been to better structure the watchlist, using Google Finance to set up how close companies are to my bear case esimates, and how my own upside changes every day. This allows me to be a little more objective with choosing candidates that have been studied, but discarded due to higher than comfortable valuations earlier.

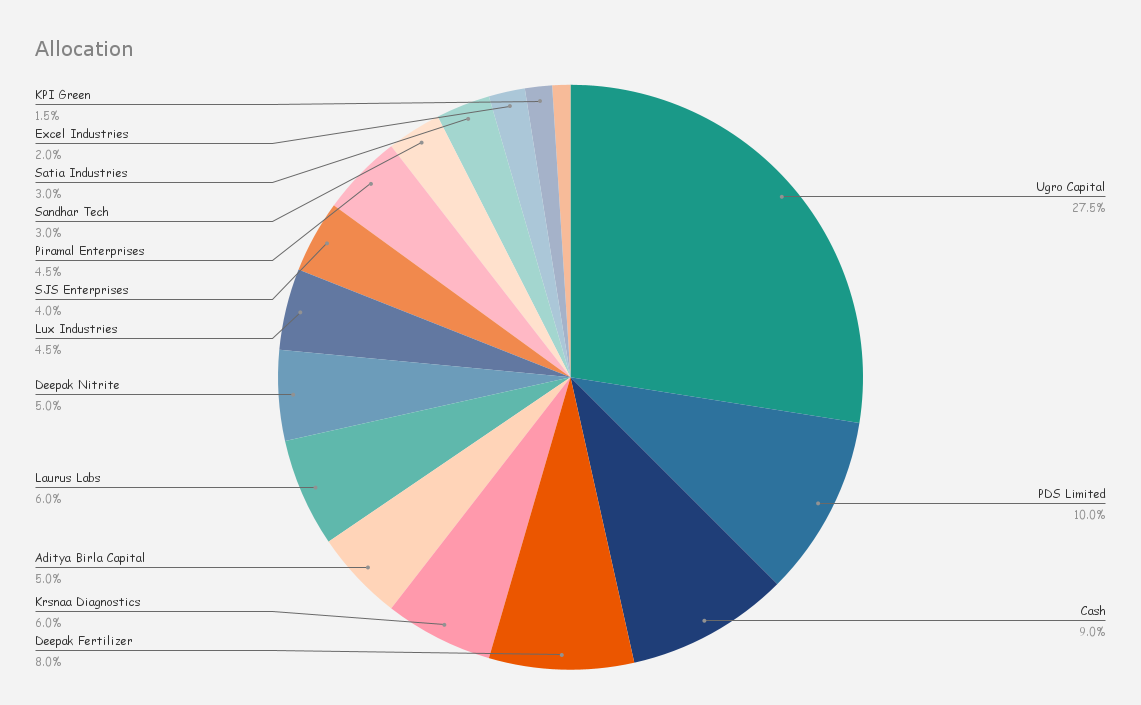

@valorem the portfolio is very similar to that shared above, I’ve slightly trimmed KPI Green to bring it back down to 3% allocations, after a sharp 80% upmove this month lowered risk/reward for FY23 guidance. I’ve also added more cash to the portfolio.

Forecasting macros is not my strength. I still remain loyal to my companies depending on their earnings runway, and the discussion on how this changes with any Western economic slowdown, or inflation itself needs to be granular and nuanced.

16 Likes

@Chins sir, as you have given such a high allocation to Ugro, I believe you expect it perform exceptionally. I understood your thesis, but could you please share the CAGR you expect Ugro to give (if you dont mind).

Thanks!

2 Likes

This is so true and I think we should double up on such companies in cases of sharp drawdowns on which we have substantial conviction while weeding out others, if necessary…

btw are you planning to raise cash from your own portfolio? How much percentage of overall portfolio as cash do you intend to be in if at all a long bear awaits us? Thanks

1 Like

The following is my base case expectation from my companies before FY23 starts. Will adjust after every concall.

CAGR Expectations

| Investment | Secular / Cyclical | Earnings Expectations | Period | Implied CAGR | Rationale |

|---|---|---|---|---|---|

| Ugro Capital | Cyclical | 45 Cr. | FY23 | 200% | Sharp reduction in OpEx for FY23, improving off book AUM. |

| PDS Limited | Cyclical | 300 Cr. | FY23 | 20% | FY22 was inflection point for profitability. |

| Deepak Fertilizer | Cyclical | 520 - 700Cr. | FY23 | -ve | Margins depend on commodity cycle. Enormous trigger in Q1FY24 which changes estimates. |

| Krsnaa Diagnostics | Cyclical | 140 Cr. | FY24 | 41.5% | Conservative estimate on management targets, dependent on ramp up of new centres. |

| Laurus Labs | Cyclical | 1100 Cr. | FY23 | 31.3% | Management targets, backed by cyclical ARV data, and new capex. |

| Deepak Nitrite | Cyclical | 1000 Cr. | FY23 | Flat | Key triggers depend on capex, and commodity cycles. |

| AB Capital | Cyclical | 2150 Cr. | FY23 | 25% | Higher disbursals, possible credit upcycle. |

| SJS Enterprises | Cyclical | 65-70 Cr. | FY23 | 25% | Management guidance, visibility of order book, and resilience to macro trends. |

| Sandhar Tech | Cyclical | 80 Cr. | FY23 | 40% | Ramp up of new capex, low base in FY22. |

-

One of my biggest learnings from last year has been that every company is cyclical.

-

There are different kinds of cyclicity in a business: that of demand, prices, costs, OpEx, CapEx, behavioural, etc. If I think a business is secular, it means I haven’t identified the cycle yet.

-

Krsnaa may not be cyclical in demand - diagnostics are crucial - but it went through a rapid cycle of expansion through the government’s drive of PPP tenders. If they hypothetically stop expanding new centres, discussions surrounding revenue growth would revolve around ramp up of utilisation (these two are not mutually exclusive).

-

A large portion of Laurus’ current revenue is dependent on the Tenofovir + Lamivudine + Dolutegravir cycle, which has a terminal risk approaching in a few years. Sure, the puck moves to non ARV molecules and many other verticals, but they will always have an associated cycle (molecules going commercial, off commercial, off Para IV protection, etc).

-

For the financials, it’s a credit cycle in availability of funds, lending requirements and RBI landscape, interest rates, creditworthiness, etc. I have exposure to a number of the larger private banks through the family portfolio.

-

Sandhar and SJS have the most obvious cycle, which was impacted by fuel norms, covid, semiconductor issues, and the lot. We’re firmly in an auto downcycle which should eventually turn.

-

The Deepaks are in the unique postion where I don’t believe FY23 will be a year of growth, but FY24/25 will be much much better due to various triggers.

-

Anyone hands you a forecast for PDS and claims to have done it accurately is lying to you (including me). One would need to individually forecast the 82 companies that make it up, and then argue a sum of the parts valuation. Management’s own targets amount to a 5 year CAGR of 30%.

-

Lux is facing unfavourable prices of cotton, and the single biggest question in economics: is underwear a discretionary spend?

-

A number of these plays I believe deserve much better multiples from the markets. For example, if Krsnaa is successful in trebling its profits by FY24, it’ll trade at single digit multiples. FY23 is also Ugro’s inflection point, and every quarter should be better than the last. Secretly, I believe if Ugro delivers on the NPA front as well as the RoE front, it should trade at 1x AUM, not 1x book.

For these reasons, even though there’s tremendous volatility, I’m optimistic for FY23. I still have maybe 6-7% in cash, and will add 5% more cash to the portfolio after planning for three years of expenses. I’m not tempted to sell companies where I think earnings can still deliver, as the drawdown is on market sentiment, and last year I got it completely wrong.

I am mentally prepared for a 20% fall in portfolio value.

@valorem I hope this answers your question on Ugro.

Disclosure: This is not investment advice, please do your own due dilligence.

19 Likes

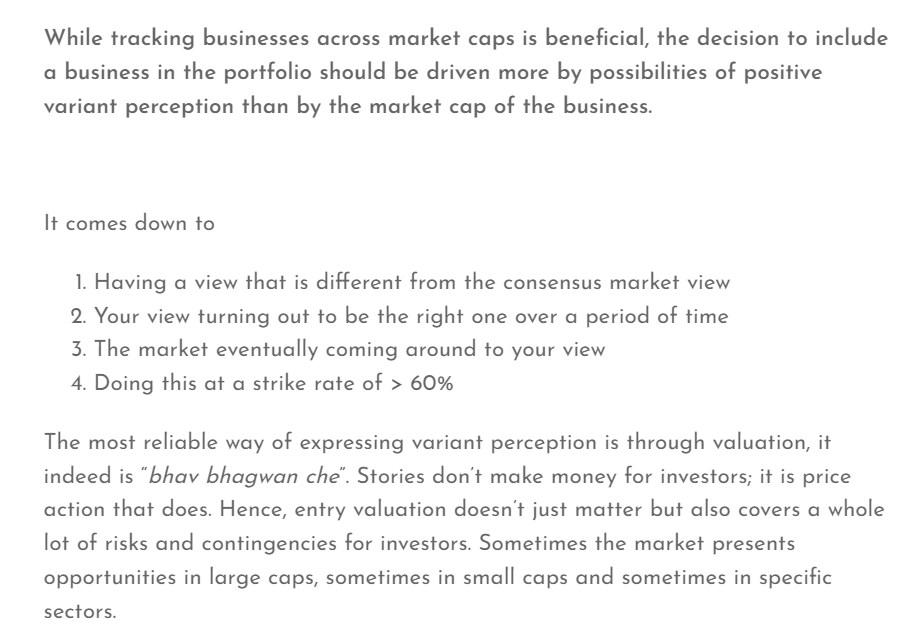

Diagnostics have seen a sharp correction and even the top 2 companies Dr Lal and Metropolis have not been spared. Investors are overly concerned about new entrants like Lupin and Tata 1mg and the impact they will have on industry margins.

If Krsnaa or any other listed player can maintain the 20% steady revenue growth they have shown in last 5 years, even with a contraction in gross margin of routine tests/checkup they can still compound profits at 15%+

Let me know your views on this

2 Likes

I’m not interested in Metropolis or Dr. Lal, and I don’t think Krsnaa is comparable as it has a completely different target market, and diagnostics mix.

This post examined the exposure different companies had to covid allied diagnostics in Q3, and the sharp correction in diagnostics is due to the realisations of covid related tests falling off a cliff.

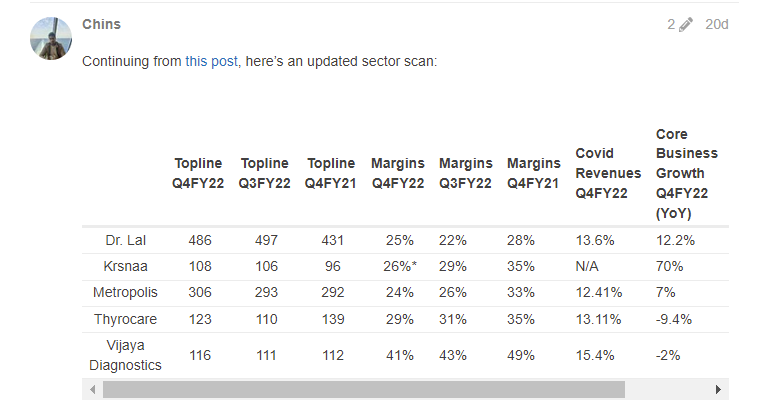

The argument from four months ago was that precisely the two companies you named have the most to lose going forward. Flash forward to Q4’s results, and this thesis played out:

I hope the core business growth in Q4 stands out, along with the exposure to covid revenues these players still have. A part of our thesis for Krsnaa is that we’re already at steady state margins without one-offs. (Except OpEx related items that will lead to a difference in standalone and consolidated margins.)

Something I think is Twitter narrative at the moment (or that current analysis excludes Krsnaa). Krsnaa prices its tests lower than Tata 1mg and puts out 28% (adjusted) margins. If this is a surprise, please see this post, where I’ve covered this in detail, and also addressed how price may not be the sole determinant for success for any new entrant.

Yes, but there’s a significant difference in valuations between all of these players and Krsnaa. More than growth, I think the risk Krsnaa has is a perception risk, where investors may never think a B2G facing company is attractive enough to deserve higher multiples. It’s still early days for the model; for Krsnaa to prove it can get its receivables; and ultimately when PPP tenders are renegotiated / extended; and its B2C rollout.

Please see Hitesh sir’s response on his thread on this point, and on how it may take time for the sector to regain the market’s fancy.

If you’d like even more detailed thoughts on Krsnaa, please see the thread where there has been wonderful collaborative work done on the company in the last six months:

8 Likes