Before we move on to the learnings from the concall, I think it’s important to pause for a moment.

The investor presentation this quarter gave me a lot of important details to some unanswered questions from higher up in the thread.

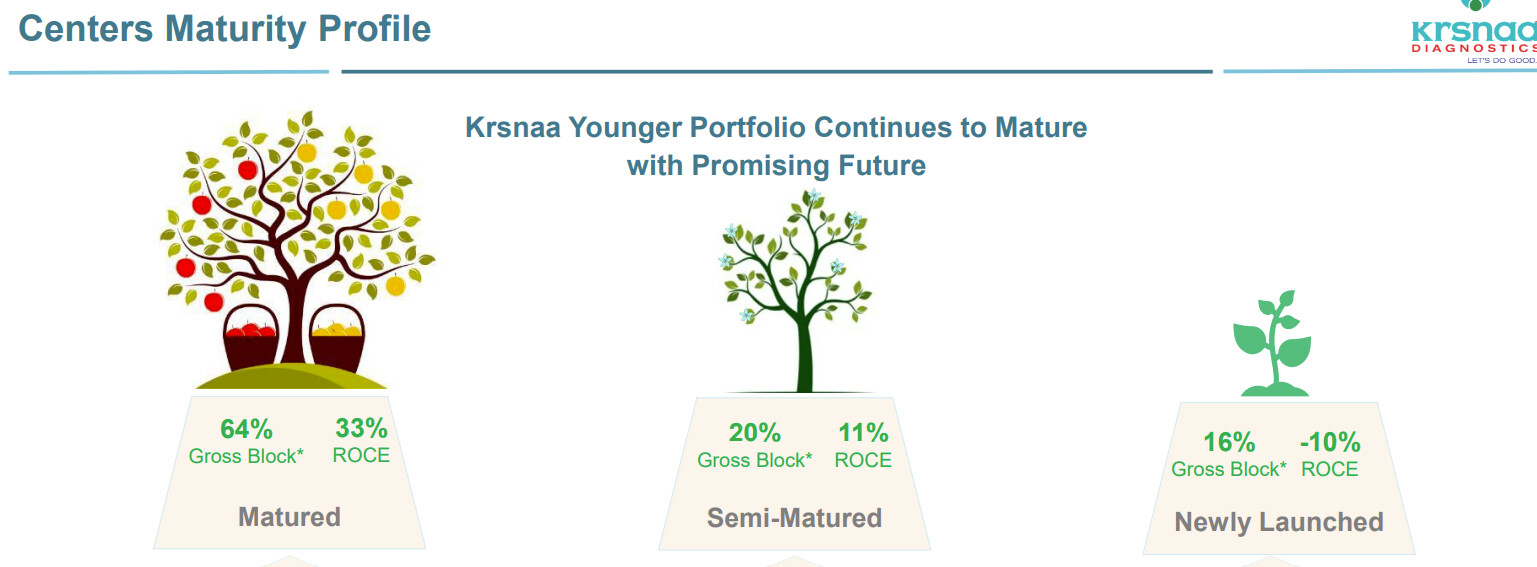

1. On the RoCE profile of mature centres

An important concern for me was around the RoCE profile and asset turns.

-

As a reminder, due to the higher receivable days, (and a percentage of payables being vendor financing), RoCE profile would be lower than the industry standard.

-

Since they’ve been rapidly expanding, a key question for me was what their most successful centre was, and the utilisation / asset turns in those centres. Or in other words, what’s the best case scenario for their newly opened centres, as they mature?

Sahil remarked in this post that the RoCE profile of the business could be in the 30% range, especially from mature centres.

In the investor presentation, we got an answer to these questions, and this observation was very close!

They tell us that the mature centres generated 33% RoCE profiles (in a year where covid revenues were 7% of the pie), and since the consolidated RoCE is 18%, we should be seeing a gradual increase over time as the centres mature, or as operating leverage kicks in. This is in line with Dr. Lal that puts out 32% and Metropolis’ 28.5%.

In addition, there’s been a downward trend in receivables, but this has been pointed out in previous posts.

2. What about 1mg and the competitive landscape?

There are two answers to this question. On the difference between rural/urban competition, and pricing.

We know that Krsnaa has a radiology mix that traditional pathology players don’t offer. I’m uncomfortable with the characterisation currently on Twitter that 1mg and Healthians have priced tests so low that it’ll run all the other players (including Krsnaa) out of business, or will hurt their margins.

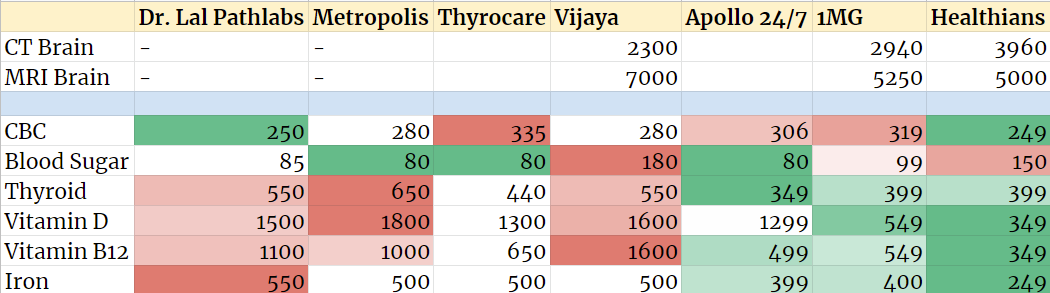

Here are the prices of some common path tests taken. I took the prices off the websites for these different players and I’ve colour coded them to differentiate between cheap and expensive providers. Take a moment to notice how 1mg and Healthians offer much better rates on tests like Vitamin B12, Vitamin D and Iron. Thus, the observation could be true for the players offering tests marked in red.

This is where nuance is important. Here’s the same price list, but now with Krsnaa included:

It’s clear that 1mg and Healthians lower pricing is nowhere close to the offering Krsnaa brings. If we’re calling Tata 1mg and Healthians disruptors, Krsnaa belongs to this list.

Here’s the second bit of nuance. Metropolis’ investor presentation (based on a report from Bain) tells us that price isn’t everything. An analysis on just price is unlikely to be accurate, and it isn’t the sole determinant of success.

Focus on the top half first.

-

Note how doctor recommendations in urban areas is important for acute illnesses. Price isn’t on the map at all.

-

For chronic and preventative illnesses, convenience takes top priority.

Now for Krsnaa, the bottom half of the page is relevant.

-

Doctor’s recommendations are important in non-metro cities, and Krsnaa has a presence in government hospitals, the first port of call.

-

Price now plays a more important role in preventative and chronic illnesses.

-

The relationship with the lab, convenience, are soft data points (apart from things like Google reviews, and data derived from footfall like repeat customers).

It’s really interesting that two different companies have different strategies on beating new entrants with attractive pricing. This is a nice live case study (as is the paints industry) as @Worldlywiseinvestors has been writing about to see which of these strategies wins. Lower pricing vs. the doctor’s recommendations / branding…

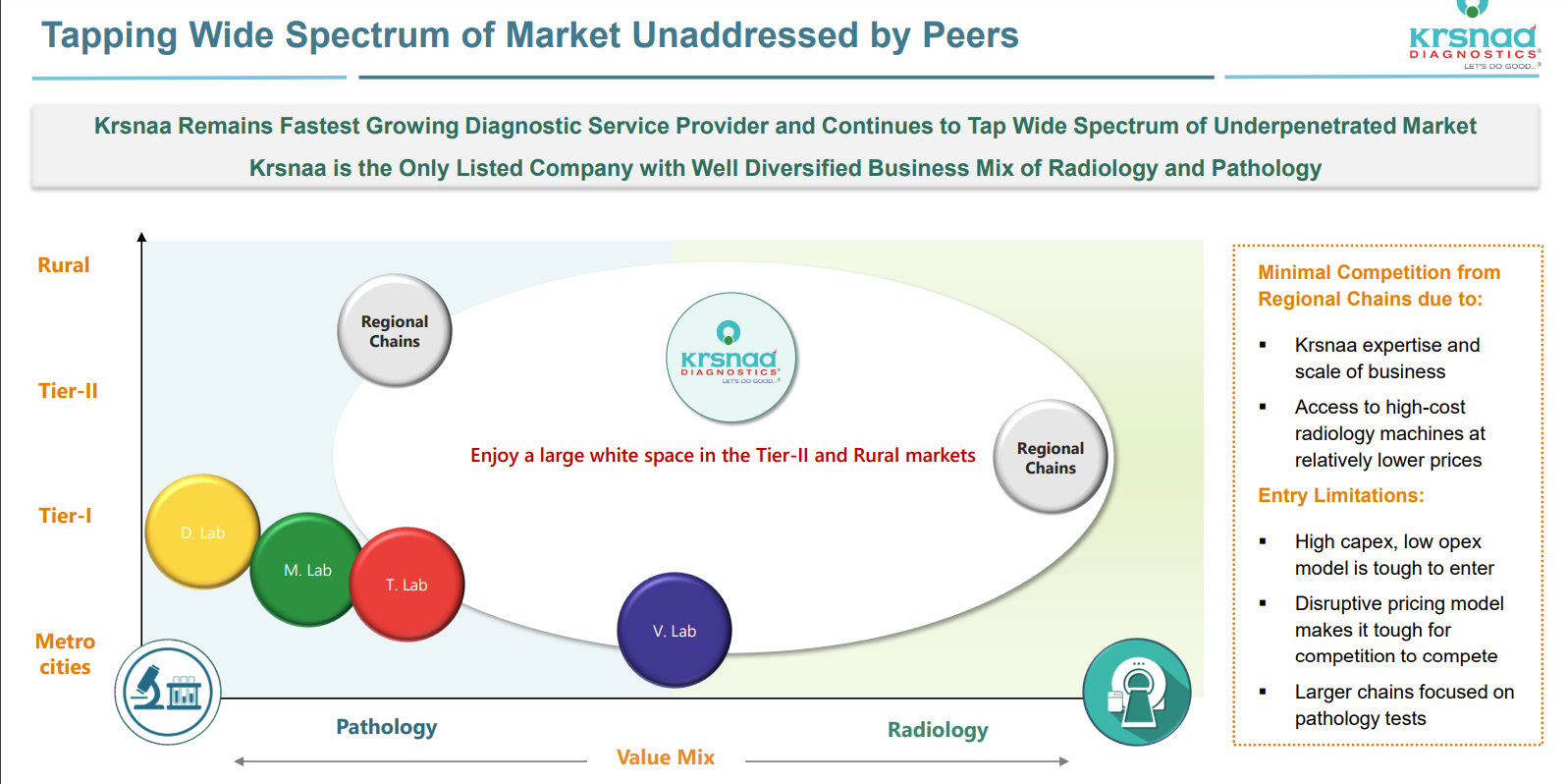

Krsnaa’s investor presentation wonderfully captures the whitespace it is targeting:

For a brilliant page by page by page walkthrough of the investor presentation, please see @sahil_vi’s thread on Twitter: