@valorem please don’t call me sir. I should update the thread more often.

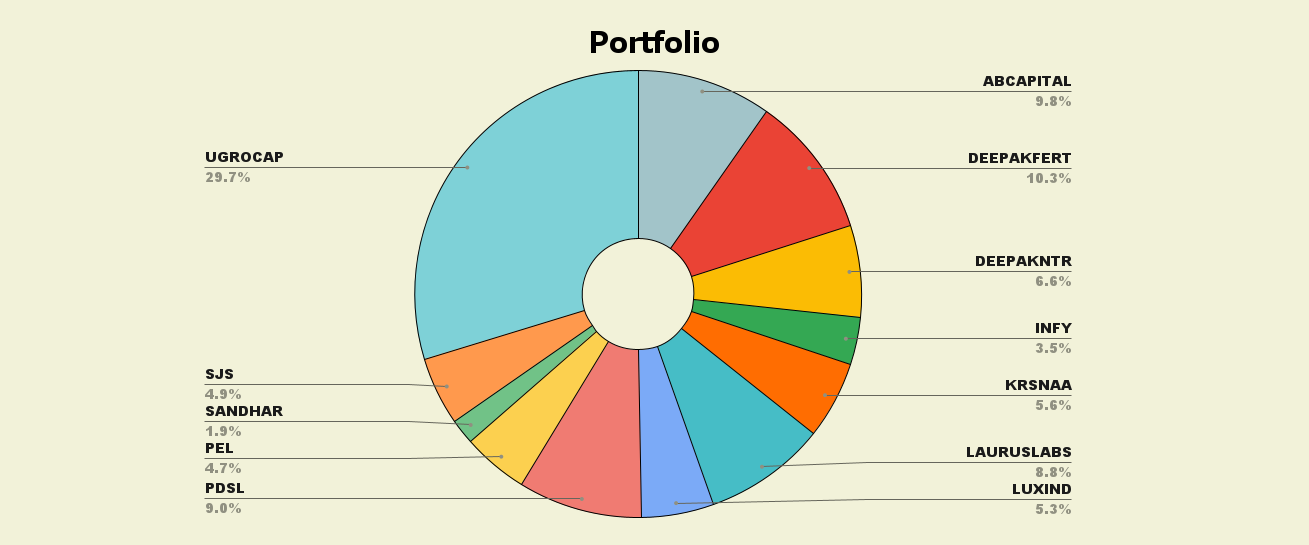

Current portfolio:

I want to summarise my current investment framework. I like companies that have reasonable valuations, and have various triggers for growth and re-rating. I go over weight/underweight depending on how near these triggers are to playing out, relative to valuations.

Some examples in case those reading this thread haven’t heard of some of these companies before.

PDSL: Had a loss making subsidiary that was at an inflection point 6 months ago. This is reflected in the change in bottomline between FY21 and FY22, and the RoCE improving from 17% in FY21 to ~38% in FY22. Business is unique in the listed space, keen to see how perception changes after the RoCE improvement shows up on Screeners.

AB Capital: Market is valuing the company by the sub-par RoAs/RoEs of 2018/19, while metrics have significantly improved, and PAT growth in FY22 is ~50%. Share price doesn’t reflect this growth. Most of the financial companies I track are reporting higher disbursals, lower provisions and better NPAs. Yet, financials have been beaten down by the market.

Sandhar: I’m currently underweight on Sandhar as it’s going to have a weaker Q4 than last year. While valuations are cheap, the triggers for growth are the commissioning of three plants that haven’t been reported to the exchange. I added to my position in March, but will add more between Q4 and Q1. The discovery of SJS made me want to split allocations between the two, as SJS today is the company Sandhar wants to be in 5 years.

I’m also studying companies where there is a lot of pessimism (prices/valuations are cheap), and RoCE/margins are well below historic means. From this, I have a watchlist of companies I would like to study to understand if this is structural or transitory, and have candidates to buy in the near future. Some of the candidates are:

Avanti Feeds: Company’s margins are at the lowest in a decade, on account of higher RM costs and the insane shipping prices seen in the last 6 months. PAT margins of 3-4% has to be the business bottom, I’m studying the company to understand the business and triggers better.

Granules: Tushar Bohra’s presentation at IIC had me interested in Granules, and the potential they have to replicate their leadership in other molecules. Currently, margins are depressed, and prima facie looks like the next two quarters will be weak. As with Avanti Feeds, I’m studying the business to understand triggers.

I haven’t bought any Deepak Fertilizer in the last four months, the position size has organically increased due to price action. I’m wary of the earnings peaking until the ammonia capex comes onstream, but I have an argument to make about the business and the gross margin mix. I’ll share on the company thread later.

Currently, I’m sitting on ~10-12% in cash, as I expect a number of companies in my coverage universe to post a weak Q4. Price movement in a lot of names does not show this is priced in, and perhaps we’ll see the market punish select pharma/chemical names as it has IT.

Overall, I think FY23 is going to challenge our stock picking

I’ll write a short note on my earnings expectations from my companies soon.