I’m not a fan of IPOs at all, and most of them last year have priced in years of growth. Keeping this in mind, I initially approached Krsnaa with a negative bias. This thread is a story of why I changed my mind, and why I believe Krsnaa deserves the attention of investors on the forum.

-

A company that has scaled tremendously in the last decade.

-

A bet on rural healthcare, built out of a differentiated business model.

-

A valuation gap between peers, and operating leverage to come.

-

Least exposure to one off covid revenues in the industry (covered in the thread)

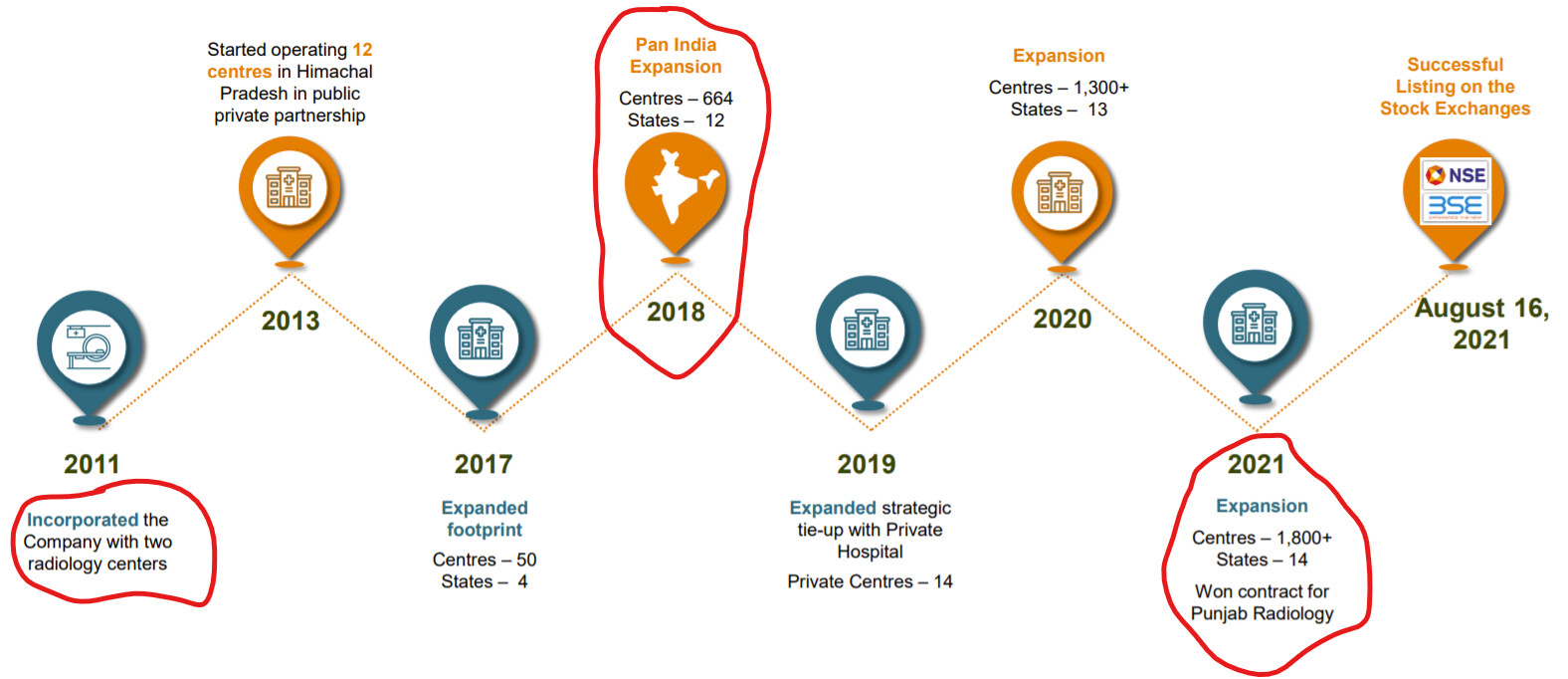

This is a company that has over 1800 diagnostic centers in India, spread across 14 states. What surprises me the most, is that it’s only ten years old. Founded in 2011, they managed to scale operations from two radiology centers in 2011 to over 1800 today.

How did they do this? While competitors worked to build standalone diagnostic centers in tier 1 cities, Krsnaa focused on winning tenders for the government’s private-public partnerships.

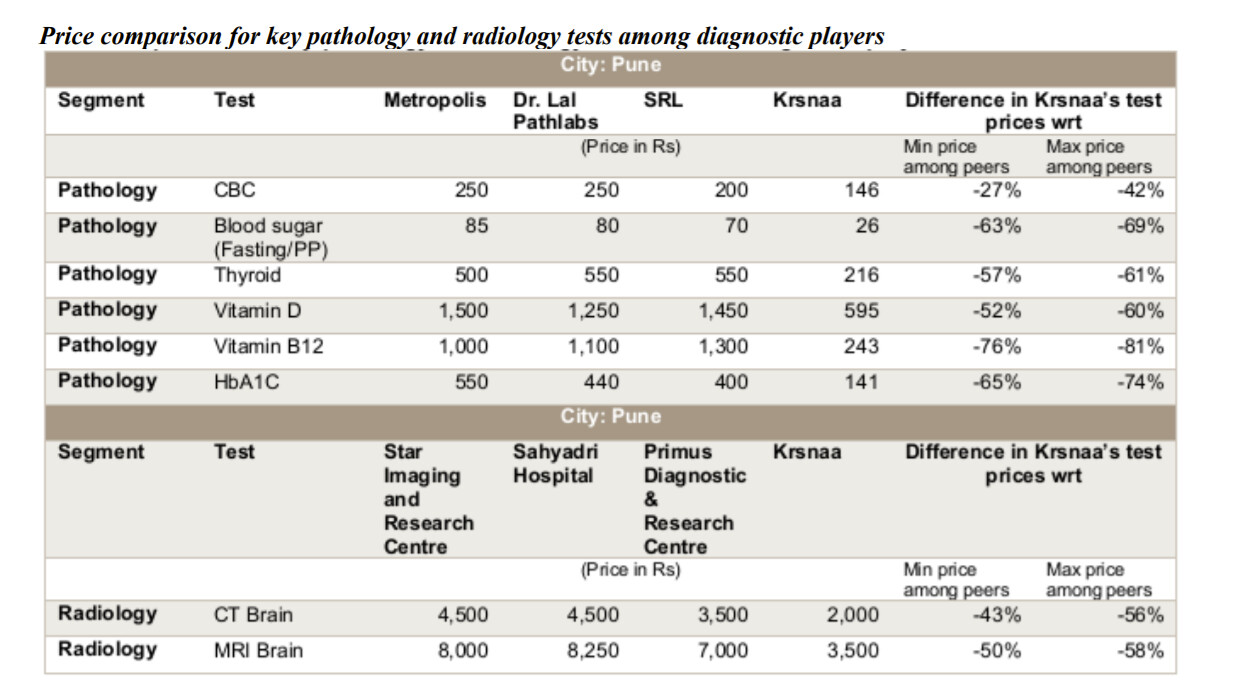

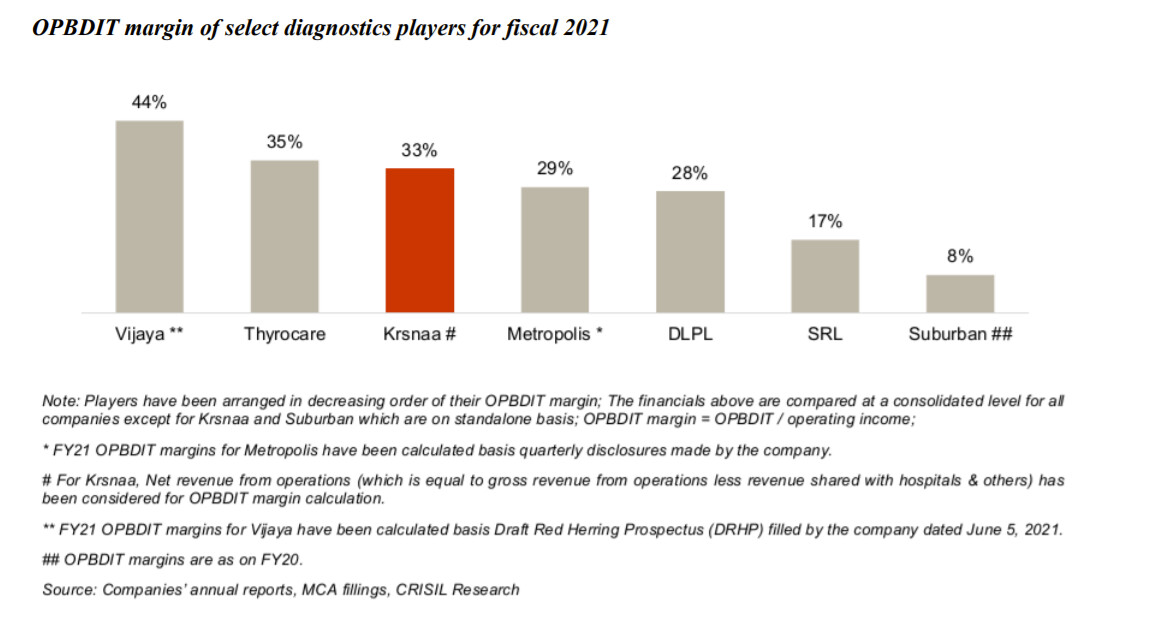

The second thing to note alongside scale, is that Krsnaa is the one of the cheapest providers of diagnostic tests:

Vijaya Diagnostics’ DRHP tells us that urban diagnostic centers account for 76% of India’s diagnostic revenue, while rural centers form 24% of the revenue. The reasons are fairly intuitive:

-

Mostly government hospitals in rural areas that have basic facilities.

-

Rural patients often travel to tier 1/2 cities in order to take a diagnostic test.

The government, in a bid to solve this problem, set up the PPP model. Here, they invite private players to set up the same urban MRI/X-ray machines in rural government hospitals. To make the offer attractive, they provide free space in the hospital, and utilities like water/electricity varying contract to contract. The private companies need to set up the room to standards, and bear the cost of equipment and staff.

1. Features of a PPP tender

-

Tenders are published on the government website, there is a minimum threshold of size and experience companies need to have in order to be eligible.

-

After inviting bids and a technical evaluation, the lowest cost offer for prices of various radiology / pathology tests wins the bid.

-

Prices are locked in, winning bids cannot change the prices of tests offered at will.

-

The tender is awarded for 7-10 years.

Now, Krsnaa has won 80% of the tenders they’ve bid for. They’ve explained that this is usually because smaller regional players offer to take up the tender for one or two hospitals, they sweep entire states at a time. Secondly, they’re the lowest cost offer on the table.

1.1 If Krsnaa don’t control how much they charge for tests, how are they competitive?

This is a concern I had while reading through the PPP tender documents. If Krsnaa wins a tender by setting test costs at 2000 rupees, it cannot increase prices above this should raw material costs go up, staff costs, etc. This takes away from their ability to respond to changing macro cycles.

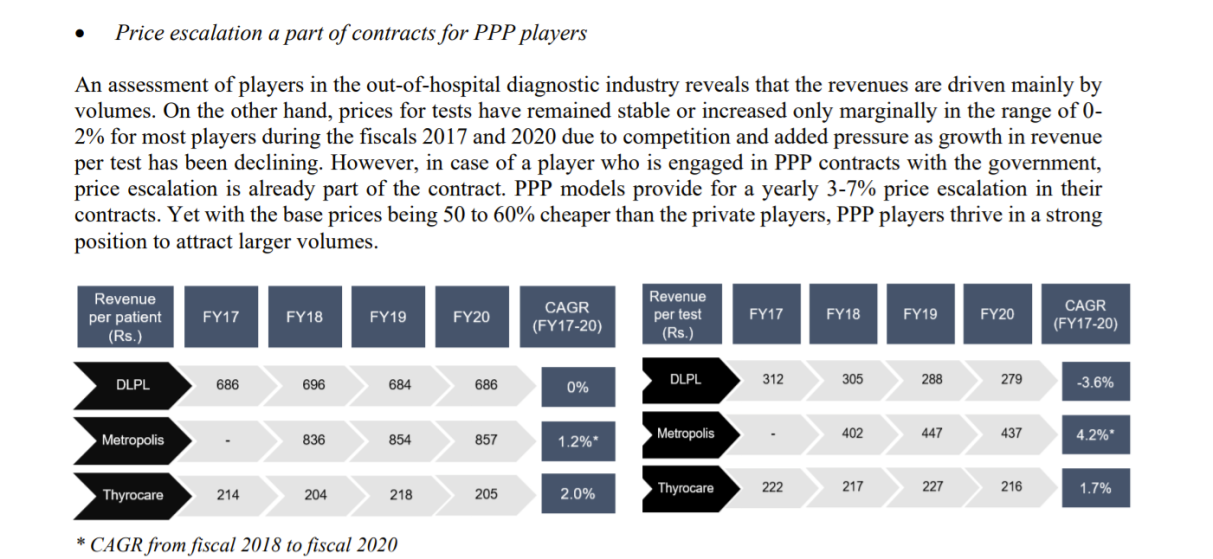

However, PPP tenders have annual price increases of 3-7% written in the contract. Is this too little? Krsnaa’s management answers a definite no, and argues that it’s industry leading:

1.2 How is Krsnaa is able to price tests this low and still deliver high EBITDA margins?

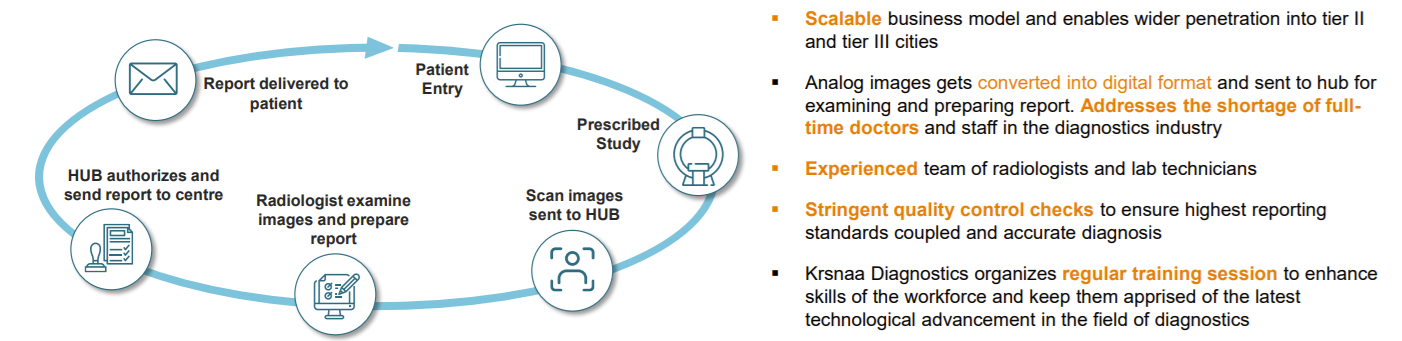

Rural centers are often difficult areas to send qualified doctors / staff to, and this has been a barrier for a long time. Krsnaa has got around this by having all of their doctors in Pune, and having rural centers send the scans through the internet to their hub.

Secondly, they have a relationship with their equipment suppliers (Wipro GE and Fujifilm), and are able to get these at a discount to peers. This allows them to place competitive bids in the PPP tenders, and saving on rent improves the margins.

Key takeaway: A large part of Krsnaa’s revenues is secured in ten year contracts under the PPP model.

Investment Pointer 1: Krsnaa stands to benefit from increasing spend by the government on rural healthcare

Market opportunity on the PPP model alone is estimated to be 13,500 Cr. by 2023, growing at around 15% CAGR from FY21 numbers. Krsnaa’s current revenues are 400 Cr. in FY21, which showcases the opportunity size.

Government is cognizant of this gap and is trying to bridge it via the PPP model.

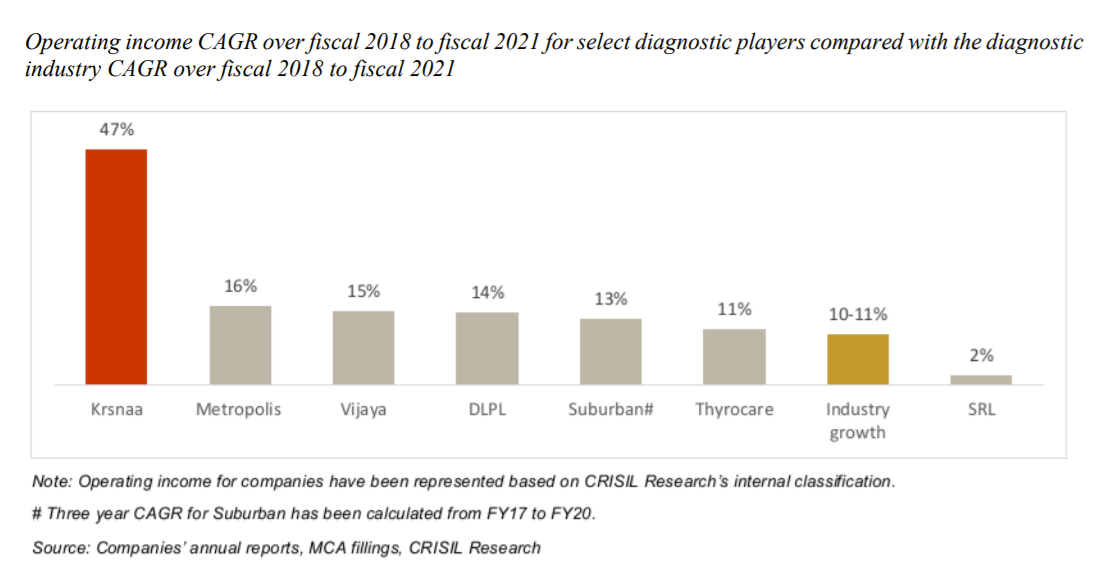

According to Krsnaa’s DRHP, it has grown at 47%, mostly on the back of adding hundreds of new centers.

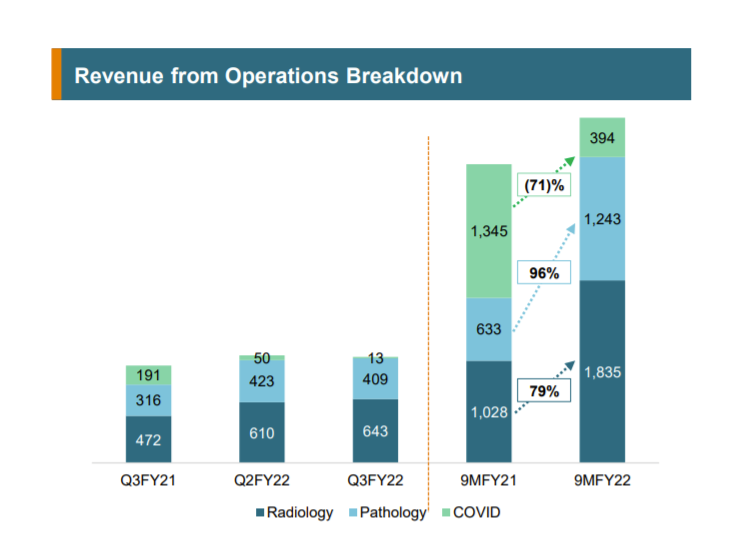

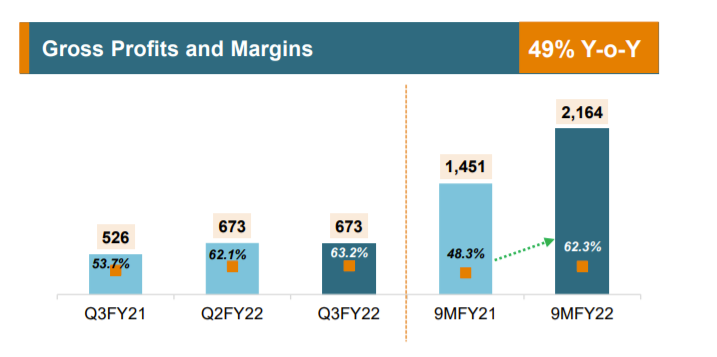

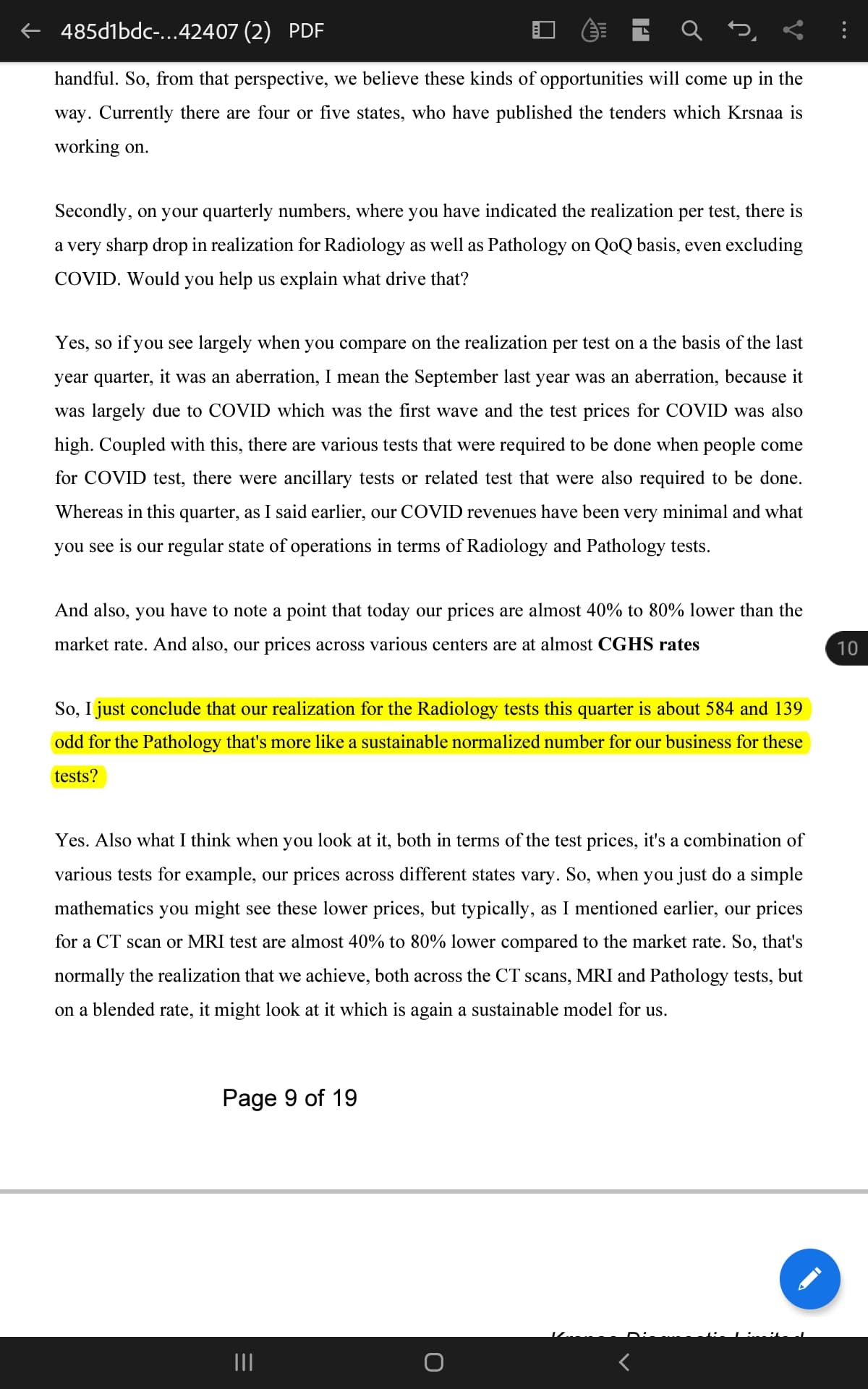

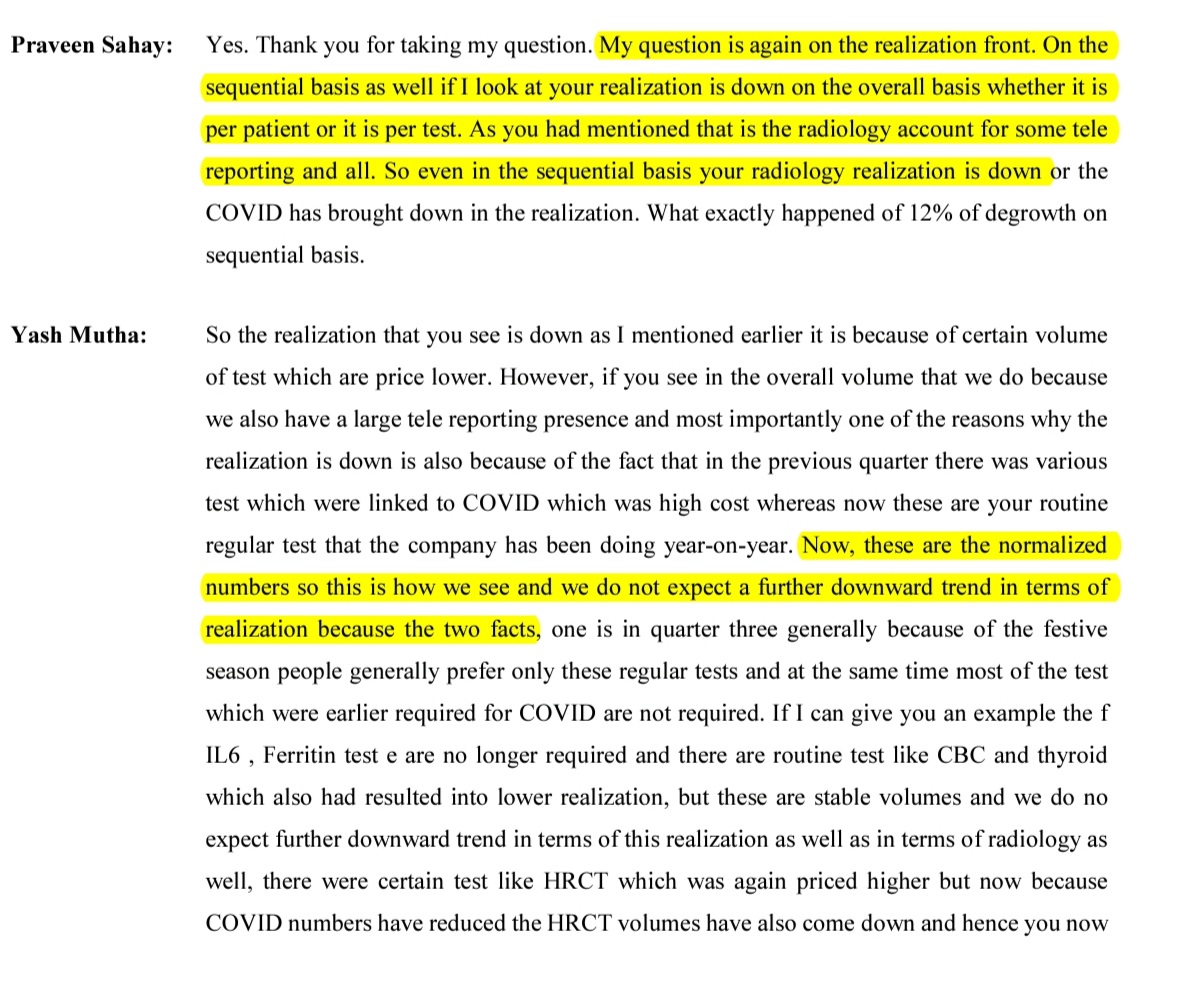

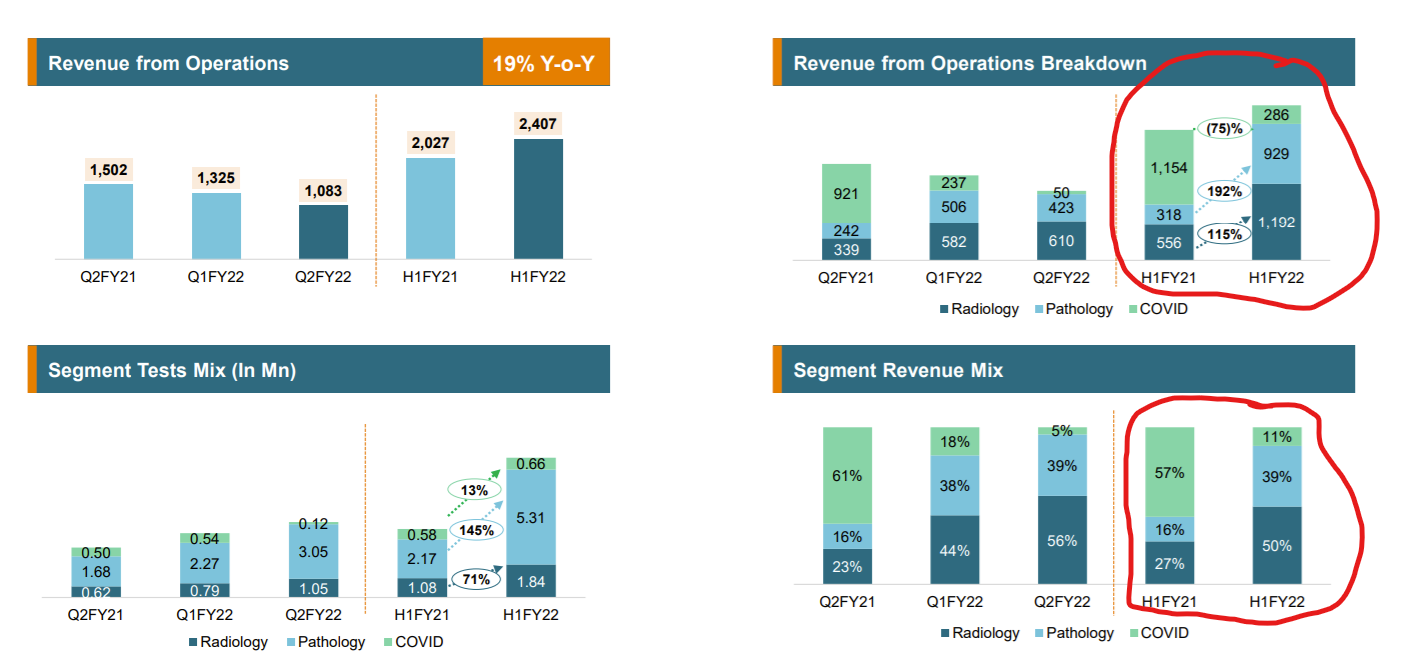

- While Covid was a one off for test providers, the core business has been outperforming in H1FY22.

Investment Pointer 2: Significant operating leverage may play out

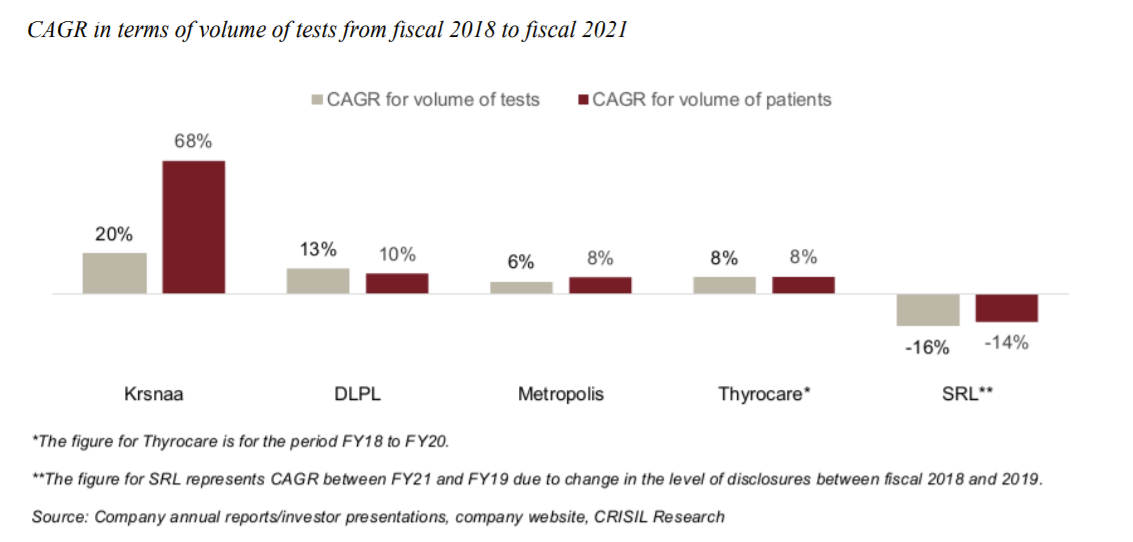

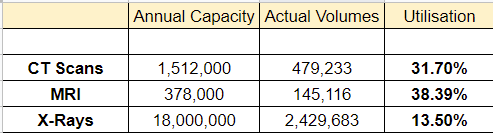

Krsnaa tells us that they have a huge headroom for tests:

-

With less than 40% utilisation (industry standard is 60-70%), Krsnaa stands to benefit from increased uptick of patients taking their tests. Management expects to improve this every quarter going forward.

-

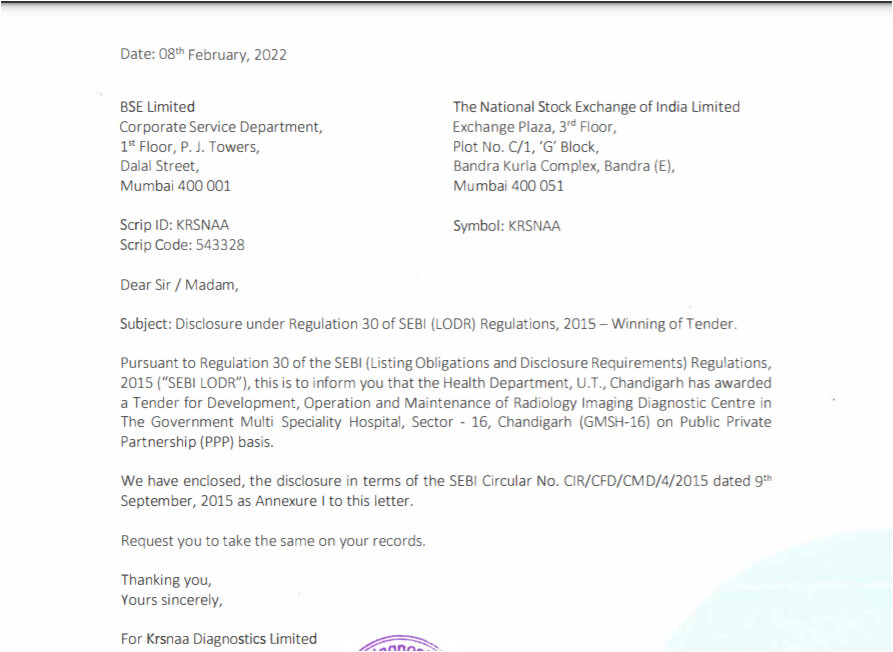

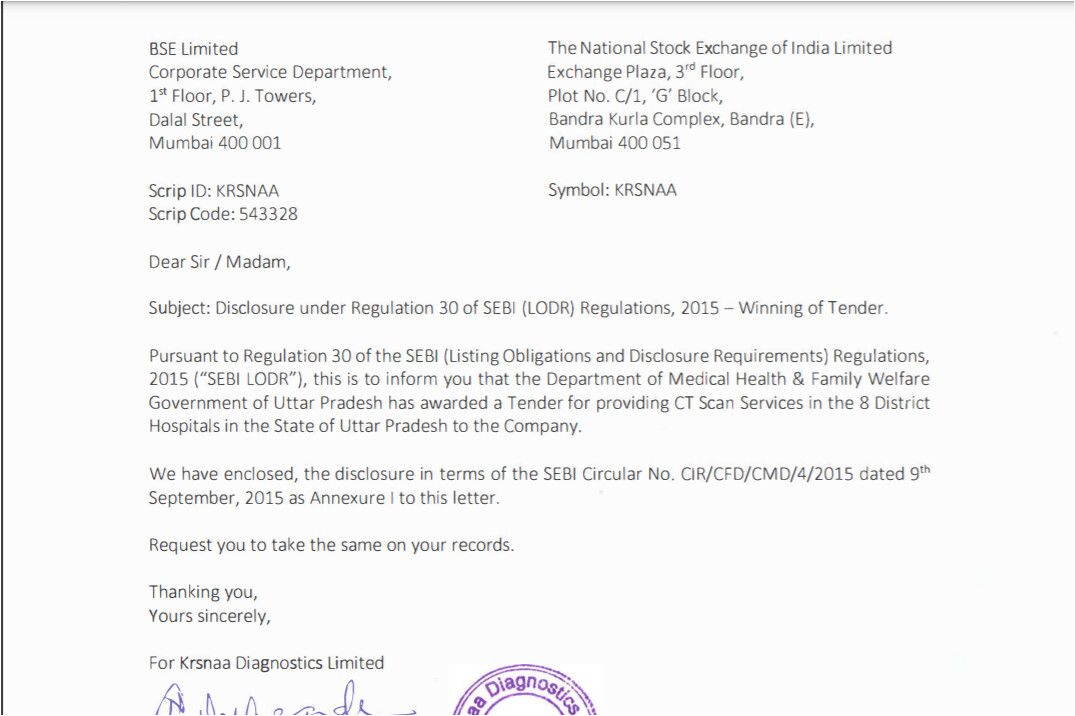

Krsnaa has recently been awarded a tender in Punjab for a number of centers. This is currently live in Q4FY22 and will add on to the capacity available.

-

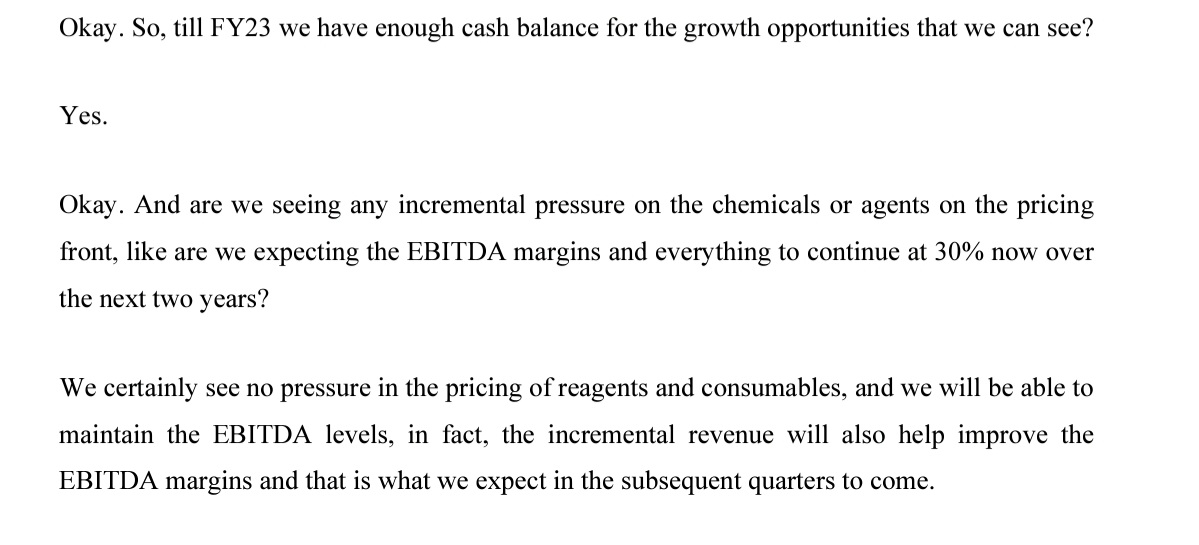

Management has alluded to FY23 sales being between 600-700 Cr. This clocks in to around 25-30% topline growth. With better utilisation of centers, margins should steadily improve, aided by the annual price increases.

This means that Krsnaa is between 3-3.54x FY23 sales. Peers are trading at obscenely rich valuations for similar margin profiles.

| Company | Price to FY21 Sales |

|---|---|

| Dr. Lal Pathlabs | 14.87 |

| Metropolis | 12.8 |

| Vijaya Diagnostic | 13.81 |

| Krsnaa | 5.37 |

Risks

- The lack of flexibility to increase test costs may hurt them in a high inflation environment.

- Capacity utilisation may never hit 60%.

- Receivable days are between 60-90 to get money from the government. They may not pay up

- Counter argument: they have not had a single bad debt/missed payment in the last decade.

- Rural India may continue to prefer going to urban centers over government hospitals.

- Diagnostic companies may see a de-rating post covid, and evaluating fair valuations may be tricky.

To do:

- Detailed information on management.

- Information on the landscape between radiology and pathology.

- Information on the convertible preference shares that have hit FY20 and squared off in FY21.

Disclosure: Invested in Krsnaa Diagnostics. All views may be biased. I am not a SEBI registered advisor. Please do your own due dilligence.