Didn’t want to make a gyan giving post.

With that disclaimer:

-

I’m thankful to everyone who has taken the time to comment, point out flaws in companies I follow, and share their knowledge of industries with me. That’s been the major learning for me this quarter - reaching out and talking to more people helps, as like minded investors work hard in their circle of competence, and it’s impossible for us to learn many different things alone.

Through them, I’ve learnt about industries, how to track different moving parts, and companies that I earlier placed in the too difficult basket. Aegis is a prime example of this, and it’s all thanks to friends like Harsh, Anish and Chet who explained the different moving parts in Aegis in detail.

-

This has also helped me with discovery. I’m not into taking credit for an idea, and being first to a good idea isn’t important to me. What’s more important to me is clarity in a thesis. Through talking to all of you, I’ve been exposed to new ideas, new case studies to look for and learn from.

Malhar, it’s amazing how many interesting companies you’ve sent me.

-

The next learning has been for me to just reach out to people at different levels of management. Not for guidance, but for insights into data that would have taken months to understand better. This is through writing to them, organising calls, or just through earnings calls. The most recent example that comes to mind is the Spaces with Dr. Velumani where anyone listening had the chance to ask questions.

On Lux, I sold after listening to people from the industry explain the dynamics of cotton. I didn’t think the results would be this bad. Will be keenly watching if the market punishes it in the next few quarters.

On Piramal’s pharma side, despite my love for pharma, I’ve had my hands burnt in the sector repeatedly now. I’m thinking of either playing the cycle (Alembic with capex optionality), or look for companies where there’s a clear specialisation that’s available cheaper (maybe Artemis). I initially thought Piramal’s NBFC would be a really nice play, as it’s trading at roughly 1 year forward book value, but then realised I already have bet on an average lender that may slowly do better, in AB Capital.

As said before, if I become a better investor, it’s largely a function of those around me. I got very interested in Shivalik after talking to Sahil, as I had placed it in the too difficult basket.

I’m slowly getting over my valuation bias of rejecting expensive companies, and instead studying companies that are of great quality with a well positioned industry structure before thinking about the valuations I’d like to pay for them. Aptus is an example for this, but I’d still like it cheaper.

Shivalik was at around 24x trailing when I bought in, I thought it was reasonable given that there are maybe 6 players that have their capabilities globally, and their addressable market falls in multiple fast growing end industries.

Aegis is another example of a top quality company that could potentially be a coffee can candidate.

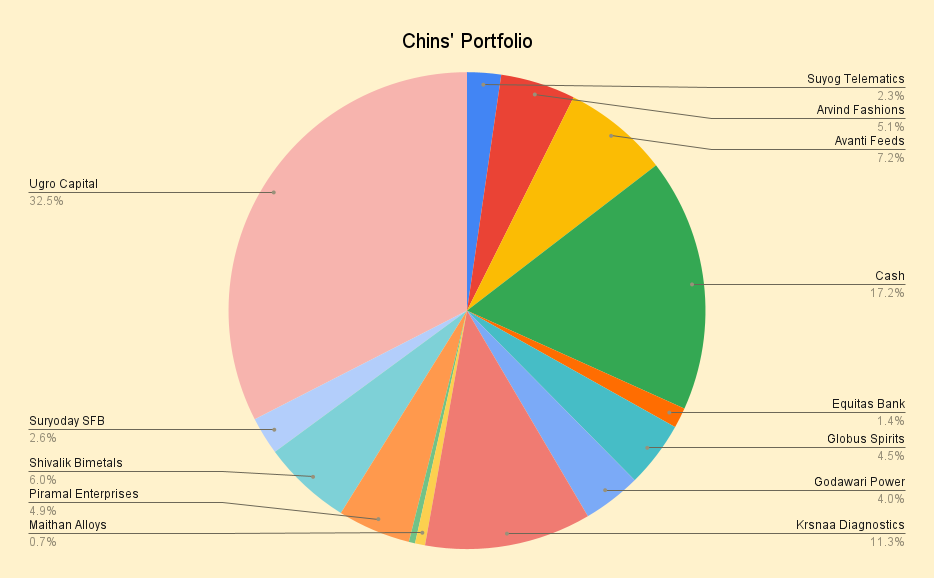

No fixed aim. I’m focusing on process, getting better at framework, entries and exits. I think those affect outcomes more than aiming for X%. Taking on larger risks doesn’t guarantee returns. I hope to be just contrarian enough to be right eventually. Currently Krsnaa and Ugro polarise people well beyond this point…

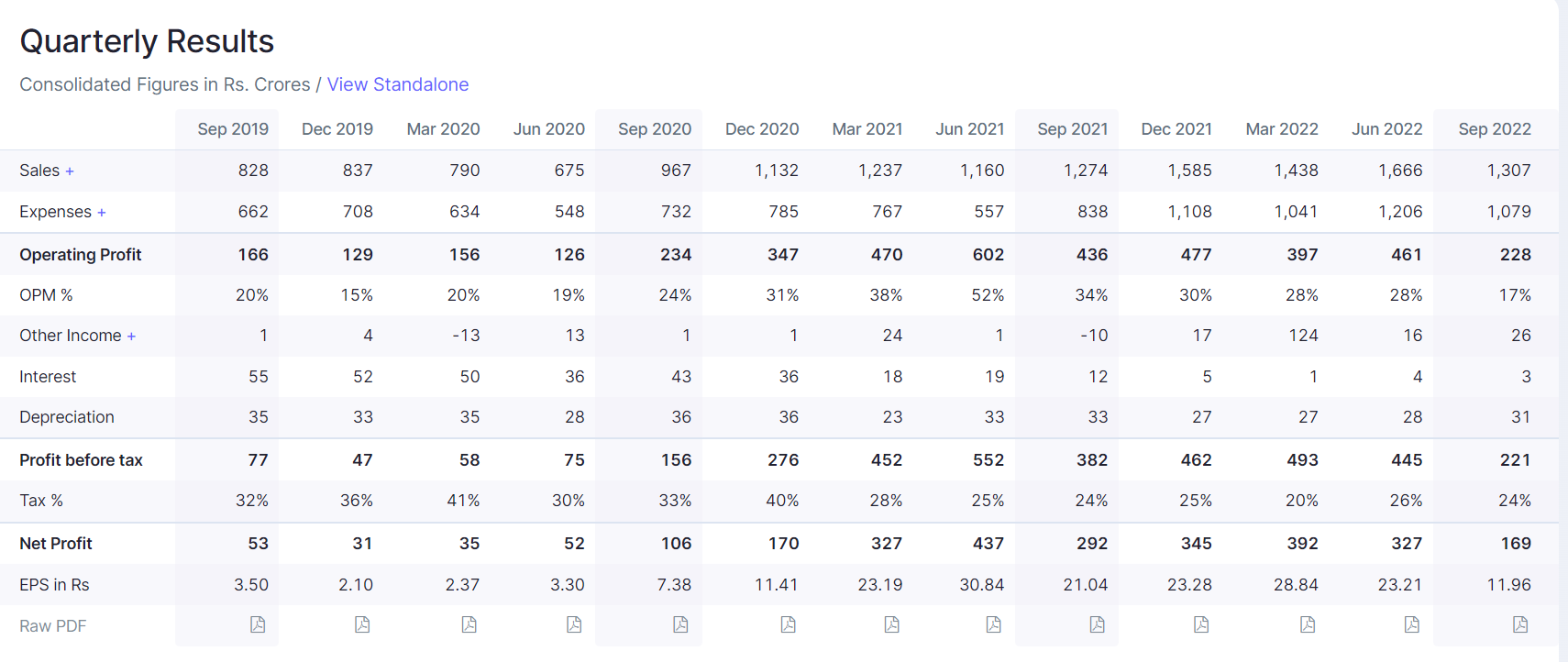

I don’t think this is Arvind’s best ever quarter, but it’s nice to see EBITDA margins rise. The point I’m trying to work out is what the best case is for their margins. Global peers in their space can do 20% EBITDA margins. Can they ever match this?

I have a short write up on Twitter if you’d like to read general thoughts on Arvind.