7 Likes

I think this has been the general assumption made on this vertical so far based on what I have seen in the AGM and concall transcripts. I think its fair considering the absolute lack of expertise in this vertical.

What we however should keep in mind is that bulk of the capital for this is from a US venture fund $15m (125 Cr) and another $13m (100 Cr) from promoters.

Nobody puts in this kind of money without clarity. The diworsification we are worrying about isn’t coming from internal accruals but from external capital and that’s a pretty big difference.

With that assumption I dug in a big deeper and here are the findings.

Key leads comes from the SAST disclosure

and the fund raise doc

Its clear from one of the earlier disclosures that Rare CP is also same ultimate beneficiaries Raisoni and Mehta

The people who are investing are Tarun Raisoni and his wife Rashi Mehta. What are their credentials? They co-founded Rahi and built it to a $400m revenue business (3200 Cr) in 10 years between 2012-2022.

The company was then sold to Wesco for $217m and Rahi became Wesco data center solutions.

Rahi’s capabilities?

So this is where Ceinsys’ data center capabilities are going to come from. From an investor who has built a 3200 Cr revenue company in 10 years and sold it for $217m and has then gone on to found Gruve in Feb of this year (Around the same time Ceinsys announced pref allotment). Gruve has since then done two acquisitions in SecurView and Netserv (both Pune based companies with around 100 Cr revenues).

Ceinsys has also hired the ex-CFO of Rahi who was instrumental is building Rahi alongside in the APAC market

So I think we can lay all apprehensions of lack of expertise in data center business to rest. Now the team is coming in with capital and expertise and we can only hope they repeat what they did at Rahi with Ceinsys. What would be even more amazing is if Ceinsys is involved in some way with Gruve which has people with serious skillsets - from the two guys that built Rahi along with Tarun Raisoni, the guys that built SecurView and Netserv and also a person who built a successful networking and virtualisation startup and sold to Google Cloud. I would be surprised if that happens but at the very least we should have a strong data center vertical in the next couple of years.

This too should now add up. I don’t think management’s guidance that pvt. sector revenues should be 50% in the next 2-3 years is completely baseless. Let’s see how it plays out

Disc: Invested since Oct '23 and no recent transactions

86 Likes

I will be interviewing an industry expert who’s working in smart city / geospatial vertical with a large MNC.

Interested investors / researchers can post their questions as comments in the shared Google doc.

16 Likes

I have written below my investment thesis on Ceinsys tech

Since the risks are high when I invest in small & micro caps ,I personally like a company with the following attributes :

1)Good management with strong execution skills & skin in the game (bcos we are betting on the jockey )

Sagar Meghe’s (Promoter ) political career has been marked by his involvement with multiple political parties and his efforts in both politics and business. His career has been shaped by a blend of familial influence, a strong commitment to education, entrepreneurial initiatives, and a vision for regional development.

After joining BJP in 2014, Sagar Meghe’s political career has been influenced by his family’s strategic shift and their connections within the party. The move to BJP was largely driven by the influence of Nitin Gadkari, a senior BJP leader and personal friend of the Meghe family, who played a significant role in welcoming them into the party .

Sagar Meghe does not appear to hold any active responsibilities within the BJP . After facing political setbacks, including a significant defeat in the Lok Sabha elections from Wardha, Sagar Meghe reportedly moved to Dubai with his family.

Apart from him the management team is professionally managed with diverse experience. Ex .Mr. Prashant Kamat - WTD, Vice Chairman and CEO Mr. Kamat is the Whole Time Director, Vice Chairman, and Chief Executive Officer at Ceinsys Tech. He was previously the Chief Executive Officer at AllyGrow. As a techno-commercial professional, Prashant has a progressive career of over 28 years which is characterized by significant accomplishments and increasing responsibilities. He has a proven track record in operations, finance, strategic marketing, business expansion, and new product development.

Skin in game -The company raised 235 cr (at 559/- share price )recently where Rare capital came in as strategic partner .The promoter themselves invested close to 100 cr !

Rare capital (main partners ) brings in Ceinsys’ data center capabilities (not physical but tech enabled , scale of Amazon & Google ).They have built a 3200 Cr revenue company in 10 years and sold it for $217m .

2)A company which has competitive edge /Right to win and have clear focused “strategic intent “ for years .I can clearly see “sustainable profitable growth “atleast for next 5 years –all the 3 words are very important for me –sustainable ,profitable and growth !!

Ceinsys tech is a technology-driven organization that specializes in offering Geospatial and ER&D solutions by providing independent opinions, actionable insights, and efficient solutions across private and government enterprises across the utility, infrastructure, natural resources, and Manufacturing sectors .

KEY INISGHTS - Current predominantly in government tender business where their hit rate of tender to order is 90%+

.I think its because of political connections , first mover advantage ,good team with width and depth of knowledge (well qualified team 82Engrs,PhD.M.Tech.MS,18%- MBA,ITI-Diploma holder ) having been there for long with VERY LOW 1% attrition rate and a very lucrative retention rate of repeat customers of 40%+

From where growth will come From :

The company is leveraging on India’s projected geospatial market growth which is expected to grow at CAGR of 13.5% by 2025.

The company is focused on capitalizing on substantial funding opportunities provided by government initiatives such as National Infrastructure Pipeline (NIP), Jal Jeevan Mission, and Namami Gange program, with a proposed budget of approximately USD15 Billion for water-related projects .Companies order book is now 1000 cr + L1 bid of another circa 300 cr majorly in this area (Present large Geography is Maharastra + UP ,seed geography is Bihar ,Jharkhand and Rajasthan –hence growth will come from Geographical reach also)

Focused on tapping the growth avenues in smart water management and renewable energy sectors, as India’s aims to add over 340 GW of renewable capacity by 2030.

The acquisition of Allygrow allows Ceinsys Tech to broaden its service portfolio by incorporating Allygrow’s expertise in core engineering design, development, and manufacturing engineering services. This expansion is particularly significant in the automotive and aerospace sectors, where Allygrow has established proficiency

In 2018, Grammer AG, of Germany(USD 2.5 Bn revenue company ), specializing in automotive interiors and commercial vehicle seats, teamed up with AllyGrow, to form a joint venture in India (70% Ally Grow, 30% Grammer). The JV is functioning as an extension of Grammer AG’s R&D Centre and providing high end engineering services to Grammer global locations.

Establishment of a new vertical MEG-Next which focuses on innovative product development activities related to Metaverse, Ed- Tech, Gaming (not right strategic fitment as per me,lets see ) and Mobility

3)Company should have pricing power

Operating margin beyond 15 % + with increasing sales according to me is a good sign of pricing power .

4)Available at reasonable valuation ,which we all want .

Its not cheap but reasonably valued through reverse DCF method .If we expect 20% share price cagr return for next 10 years the implied PAT growth is 24% cagr which I think this company can achieve given sales growth would be above 15% cagr because of sector tailwind hence operating leverage would play in and PAT growth would be above 25% cagr (see past track record below for 5 years ,sales growth 7% ,PAT growth 59% ) .I expect this to be like Tata Elxsi in Geo Spatial sector !

5)Risks:

- Political risk

- Cultural integration (not sure of Organization structure )

- Debtors risk in Govt outstanding

6)Key things to watch out for me :

- Top line growth according to me would be above 25% pa for next 3 years with improved Operating margin %

- Mix of revenue split between Govt. & Private orders (expect to be 50:50 over 2-3 years )

- Geo spatial and ER&D revenue mix (would be 50:50)

- Geographical penetration beyond Maharashtra and UP

- Data Centre revenue

Discl : Invested and hence views may be biased

54 Likes

There are some NICE questions (3 ) marked in this document .

I am answering the same using google search and AI ![]()

1)The geospatial assessment for the Kaleshwaram Project was conducted by WAPCOS, a Government of India organization. WAPCOS was responsible for carrying out reconnaissance and LiDAR surveys in and around the reservoir area, which were used to prepare the Detailed Project Report for the Kaleshwaram Project

2)Question )What is that the companies specialised in this sector hold compared to L&T or other big companies. Example: Bidding of recent project wainganga nalganga river project?

Ans - Specialized companies in the geospatial sector, like Ceinsys Tech, have certain advantages and capabilities that set them apart from larger conglomerates such as Larsen & Toubro (L&T) when it comes to bidding and executing projects like the Wainganga-Nalganga river link project.

Advantages of Specialized Geospatial Companies

- Expertise in Geospatial Technology: Companies like Ceinsys Tech specialize in advanced geospatial technologies, which include GIS, remote sensing, LiDAR, and digital twin creation. This specialization allows them to offer precise and innovative solutions tailored to specific project needs, such as detailed surveying and hydrology studies

1

](https://www.nbmcw.com/news/ceinsys-tech-wins-rs385-cr-bid-for-wainganga-nalganga-river-link-project.html)

3

. - Focused Services: These companies often focus exclusively on geospatial services, enabling them to develop deep expertise and deliver high-quality outputs quickly. This focus can be a significant advantage in projects requiring detailed geospatial assessments and planning

- Agility and Innovation: Specialized firms can be more agile than larger companies, allowing them to adopt new technologies and methodologies faster. This agility is crucial in fields where technology is rapidly evolving, such as geospatial data analytics

3)Question - In the future years, do you see impact based on government priorities or will geospatial remain a strong beneficiary in the years to come without any explicit government intervention?

Ans -The future of the geospatial sector appears promising, with or without explicit government intervention, due to several factors that drive its growth and integration into various industries.

Factors Supporting Geospatial Growth

- Technological Advancements: The geospatial sector is benefiting from rapid technological advancements, including the integration of artificial intelligence (AI) with traditional geospatial analytics. This combination enhances predictive capabilities and allows industries to respond swiftly to changes, thus increasing the demand for geospatial technologies

1

. - Market Expansion: The geospatial analytics market is projected to grow significantly, from USD 89.23 billion in 2024 to USD 209.81 billion by 2032, at a compound annual growth rate (CAGR) of 11.28%

1

. This growth is driven by increased adoption across various sectors such as agriculture, infrastructure, and urban planning. - Industry Adoption: More industries are recognizing the value of geospatial data for decision-making and strategic planning. This trend is expected to continue as companies seek to leverage spatial data for operational efficiency and competitive advantage

1

.

21 Likes

This is From VTS founder which got acquired by Ceinsys recently in USA. he has mentioned about a MSA with Major telcom player.

32 Likes

Very good result .

Very good growth on Cash flow ![]()

Consolidated numbers looks a bit lower growth % than standalone bcos of employee cost at corporate level absorbed in consolidated.This should be taken as positive bcos they have order which is 7X of revenue hence employee cost to be front loaded as revenue will accrue over 2-3 years

I like their strategic approach to business .Their core is “Geo spatial “ that also India and public sector but they are extending the core to private sector and more important to ER&D and overseas. Hence if one analysis the revenue that way one would see a big derisking of business happening (which is reflected and will get reflected in segmental revenue )

Ceinsys qtr 3 results 121124.pdf (4.5 MB)

11 Likes

1 Like

Results look great on a surface level but even greater things are hidden underneath the numbers.

The standalone topline shows 78 Cr which is split under geospatial 43 Cr and Technology solutions 35 Cr. Margins for geospatial segment is 39% and TS is 32%. While this may look outstanding, it is not the right way to look at it in a business like this. H1 FY25 is a somewhat better comparison and even there margins are stellar (Geospatial 24% and TS 41%).

Recently the company has changed its segments where segments which were previously reported under geospatial are now partly clubbed under technology solutions. From one of the earlier calls

These projects (IoT, digital project management systems, inspection work) have a geospatial component but bulk of the value-add is from elsewhere so these are now reported as technology solutions. Technology solutions also of course includes the AllyGrow business which was amalgamated with Ceinsys and so gets reported under standalone (AllyGram JV profits are reported under consol). AllyGrow topline would be around 13 Cr or so per quarter (52 Cr topline from earlier memory). If this is removed from TS, then 22 Cr from TS used to be earlier reported as geospatial. So while it may look like there’s no growth from geospatial YoY, the right numbers to compare are 40 Cr from last yr vs 65 Cr from this year (43 + 22) to compare apples with apples which is ~60% growth.

On a consol basis PAT is relatively muted due to

- Higher employee costs (22 Cr in standalone vs 33 Cr in consol).

- Higher tax outgo - 9 Cr for Q2 when PBT was 21 Cr (15 Cr in H1 FY25 is same as tax for whole of FY24)

The VTS employees + Kelly Yagi + Data center employees in Singapore I think contribute to bulk of the increase in consol along with 5.27 Cr of ESOP expense. VTS and Data center business should contribute to profits going forward so this drag should be lower. If you normalise for these, consol PAT should be almost 18 Cr levels for the quarter

The other thing to note is the healthy cash flow from ops - 57 Cr in consol and 52 Cr in standalone. While the company has had healthy cashflows, it has never even crossed 50 Cr on a whole year basis but has crossed it in just H1 when business is generally H2 heavy.

The company has received 62 Cr from equity and 43 Cr from warrants (~130 Cr more will come in when warrants are converted)

The overall cash levels in the company have gone up from 30 Cr in Mar '24 to 205 Cr in Sep '24.

Now even if you add this 105 Cr from dilution, cash levels are up by 70 Cr from internal accruals!

We know that ~52 Cr is from CFO and looks like bulk of the rest (~15 Cr) has come from dividend from AllyGram

205 Cr cash + another 130 Cr from warrant conversion when it happens puts a very healthy 335 Cr on the balance sheet for acquisitions.

Coming to the acquisition, i noticed an escrow to the tune of 38 Cr. Not sure if this means some acquisition is close to completion.

The last two highlights - the orderbook now stands at 1200 Cr as of Sept '24. There’s L1 of 500 Cr on top of this after this date that we know of - 385 Cr wainganga-nalganga river-linking and 115 Cr IDDP for MMRDA. So overall order book should be around 1700 Cr.

The other things is the working capital days which has trended like this

237 days → 190 days → 108 days

this is nothing short of phenomenal for a B2G facing business. The balance sheet and CFO also confirm this claim by the management as receivables are down YoY despite growth in revenues and healthy CFO of 57 Cr in standalone.

So yes, while the growth is phenomenal, there’s more here when you look deeper that the numbers are telling from order book, working capital, cash flow, scope for margin improvement etc.

Disc: Invested. No recent transactions

115 Likes

Ceinsys Tech Limited Q2 FY25 Earnings Conference Call Summary

This is a summary of the Ceinsys Tech Limited Q2 FY25 earnings conference call hosted by Choice Equity Broking Private Limited on November 14, 2024.

-

Key highlights of the quarter and first half of FY25 include:

- Revenue growth: Operational revenues grew 54% year-over-year to ₹90 crores for the quarter. For the first half, it reached ₹164 crores, a 46% growth.

- Profitability: EBITDA grew 71% year-over-year to ₹17 crores for the quarter and 42% to ₹30 crores for the first half. Net profit was at ₹12 crores (149% growth) for the quarter and ₹24 crores (82% growth) for the first half.

- Strong order book: Total order book stood at ₹1210 crores as of September 30, 2024, with geospatial and engineering services contributing 76%.

- Successful fundraise: Ceinsys raised ₹235 crores through equity and warrants, with ₹105 crores received during the quarter.

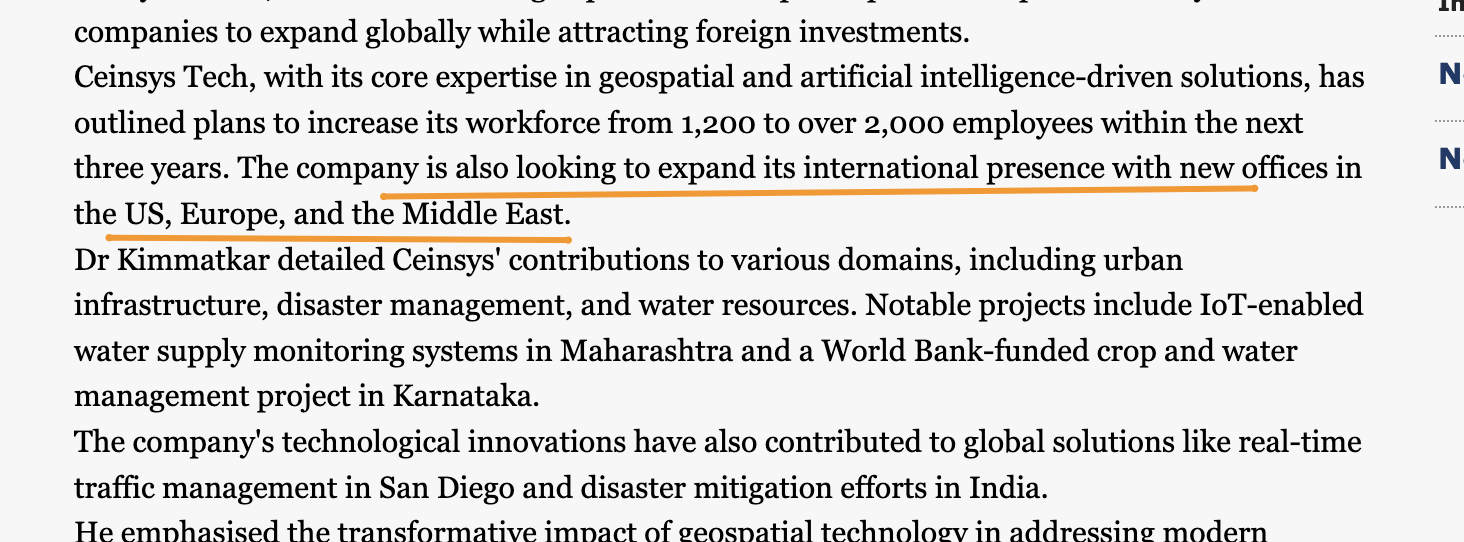

- Strategic acquisitions and investments: The company acquired a geospatial company in the US and invested in data center capabilities.

-

Question and Answer Session:

- Financial position and margins:

- Ceinsys has a cash surplus of ₹172 crores and net operational cash surplus of ₹68 crores.

- The company expects margins to be sustainable.

- Geospatial segment and differentiation:

- Ceinsys focuses on the digital side of geospatial services, leveraging digital data, longitude and latitude information.

- They differentiate themselves from EPC companies by focusing on planning and digital solutions rather than hardware.

- Unbilled revenue and escrow account:

- Unbilled revenue is recognized for work completed but not yet invoiced.

- The escrow account balance represents funds received from customers for ongoing projects.

- Employee stock options:

- 1% of issued capital was granted to John, the CEO of the acquired US geospatial company, and Rashi Mehta, the Finance VP in the US.

- Inorganic growth and acquisitions:

- Ceinsys is actively pursuing acquisitions, with one transaction already closed in the US.

- The company is in active discussions with three companies and may issue non-binding term sheets soon.

- Standalone vs. Consolidated financials:

- The consolidated EBITDA is slightly lower due to investments in business development at the subsidiary level.

- Subsidiaries are profitable and the investments are for the benefit of the group as a whole.

- Revenue seasonality:

- Ceinsys expects some seasonality to continue, with Q4 typically being the strongest due to government-related business.

- However, diversification efforts may lessen the seasonality impact.

- Tax rate:

- The higher tax rate in Q2 was due to a dividend received from a JV company, which is taxed separately.

- Geospatial and technology solutions focus:

- Both geospatial and technology solutions are expected to contribute substantially to future revenue.

- The segment classification was revised based on anticipated contributions over the next few quarters.

- Data center vertical:

- Ceinsys is investing in data center capabilities, focusing on design services including liquid cooling technology.

- Telecom sector opportunity in the US:

- The acquired US geospatial company specializes in scanning telecom towers, creating inventory data for major US tower companies.

- Order book and bid pipeline:

- The total order book is ₹1210 crores, with an additional bid pipeline of approximately ₹400-500 crores.

- Maharashtra and Uttar Pradesh are the major contributing states to the order book.

- Ceinsys’s competitive advantage:

- The company focuses on bidding for projects where they have strong competencies and credentials, leading to a high win rate.

- Their experienced workforce and low attrition rate contribute to their success.

- Subsidiary merger:

- Allegro Technologies, the subsidiary, will be merged with the parent company.

- The US subsidiary will remain a separate entity.

- Financial position and margins:

Overall, Ceinsys Tech Limited reported strong financial performance in Q2 FY25, driven by revenue growth, increased profitability, and a robust order book. The company is actively pursuing strategic acquisitions and investments to expand its reach and capabilities, with a focus on both geospatial and technology solutions. While some revenue seasonality is expected, Ceinsys aims to mitigate this through diversification efforts. The company is optimistic about its future prospects and expects to achieve significant growth in the coming years.

24 Likes

Thanks for the Con-call summary.

Just wanted to add few more points.

Management guided for 1000 Cr revenues in 3 yrs.

Also Sounded very bullish on data center vertical. They are not going to own DC or assets as such, It will be design-setup-Maintance only so not much capital intensive.

Also there were questions on winning orders due to political connections, Management mentioned they are capable of winning irrespective of who or which party is in power. They are winning tenders based on technical qualifications and prior experience in executing such projects.

26 Likes

one interesting thing on the call (to me) was the amount of answers Prashant Kamat gave - he wasn’t on the last call.

Upon further digging his background seems to be quite interesting he seems have led a ERD business back in the day for Mahindra after which he started Allygrow and it seems Ceinsys has pretty much acquihired him -

14 Likes

Was looking into the fine prints of recently rolled out BharatNet Phase 3 tenders (Polycab, HFCL, ITI, STI has won few out of the results announced so far).

Realized that there are stages of BharatNet Project where GIS services is integral part of the scope of work:

- Pre-deployment - Optimal route planning, topology based project planning, network management planning etc.

- Deployment - Third party validation, progress tracking

- Post Deployment - Nation assets mapping and consolidation (by NIC under BhartMap portal (link)

Not surprised, Ceinsys has done similar GIS mapping activities for BSNL in past (likely under BharatNet phase 1 or 2):

GIS-Asset mapping of Optical Fibre Cable laying route - Ceinsys

Overall GIS opportunity size under BhartNet:

BhartNet Phase 3 appears to interesting opportunity (off-course, GIS will be a small component of entire project):

- BhartNet Phase 3 tender is for Rs 1.39 lakh crore (INR 65,000 Cr. capex and the balance Opex up to 10 years)

- Aims to upgrade existing 214,000 gram panchayats (from linear to ring topology network architecture). Also to connect 47,000 new gram panchayats under BhartNet networks.

Just to assess the scope of work from GIS perspective:

- Middle Mile:

- Current OFC length of 6.92 lakh Fibre KM to be upgraded

- ~ 2 Lakh Fibre KM new OFC roll-out

- Additionally, there will be scope of last mile FTTH (fibre to home) connecting 2.5 Lakh gram panchayats to 6.5 lakh villages and subsequent households.

- Above numbers added together will tie very closely with the overall OFC opportunity estimate shared by HFCL MD:

This could be an interesting opportunity - more so since the overall pie is large and they have been one of the vendors to BSNL in past for similar project.

Disc: Invested in Ceinsys, no transactions in last 90 days.

Tarun

27 Likes

3 Likes

Hello All,

I’ve created a business model for Cyeinsys based on the following key details:

The management has an order book of ₹1200 crore, with an execution timeline over the next few years.

They have provided guidance for ₹1000 crore in revenue in the near term.

To remain conservative with the execution timeline, I’ve projected ₹1000 crore in revenue by FY27.

I notice that many of us are tracking or invested in this stock. Kindly review my financial model and share your thoughts. Your feedback would be greatly appreciated.

15 Likes

Take the exit pe as 15-20 if growth saturates or market cycle changes as 10 year back 25-30% growing companies were plenty at 10-15 pe which is rare now but these cycles change some experienced persons say this. A selling criteria will be when the stock reaches tripple digit pe. Or when we will judge that growth rate will slow down…we just need to check Financial year starting orderbook to that financial year revenue conversion ratio. For example fy24 revenue is around 225 cr and starting orderbook was 250 cr approx. Whereas for Fy25 the starting orderbook was 700 cr…so we know the growth is going to accelerate (this was my buying point around 700).

Now at end of Q2 orderbook is 1200 which as Q1 end was 900 cr. So only sign of revenue acceleration. Plus it’s a new sector geospatial so market will give a high pe till the growth rate maintains or accelerates. The moment there will be indication of growth slowdown it will be better to exit. This is very plain and simple to understand when growth will slowdown.

38 Likes

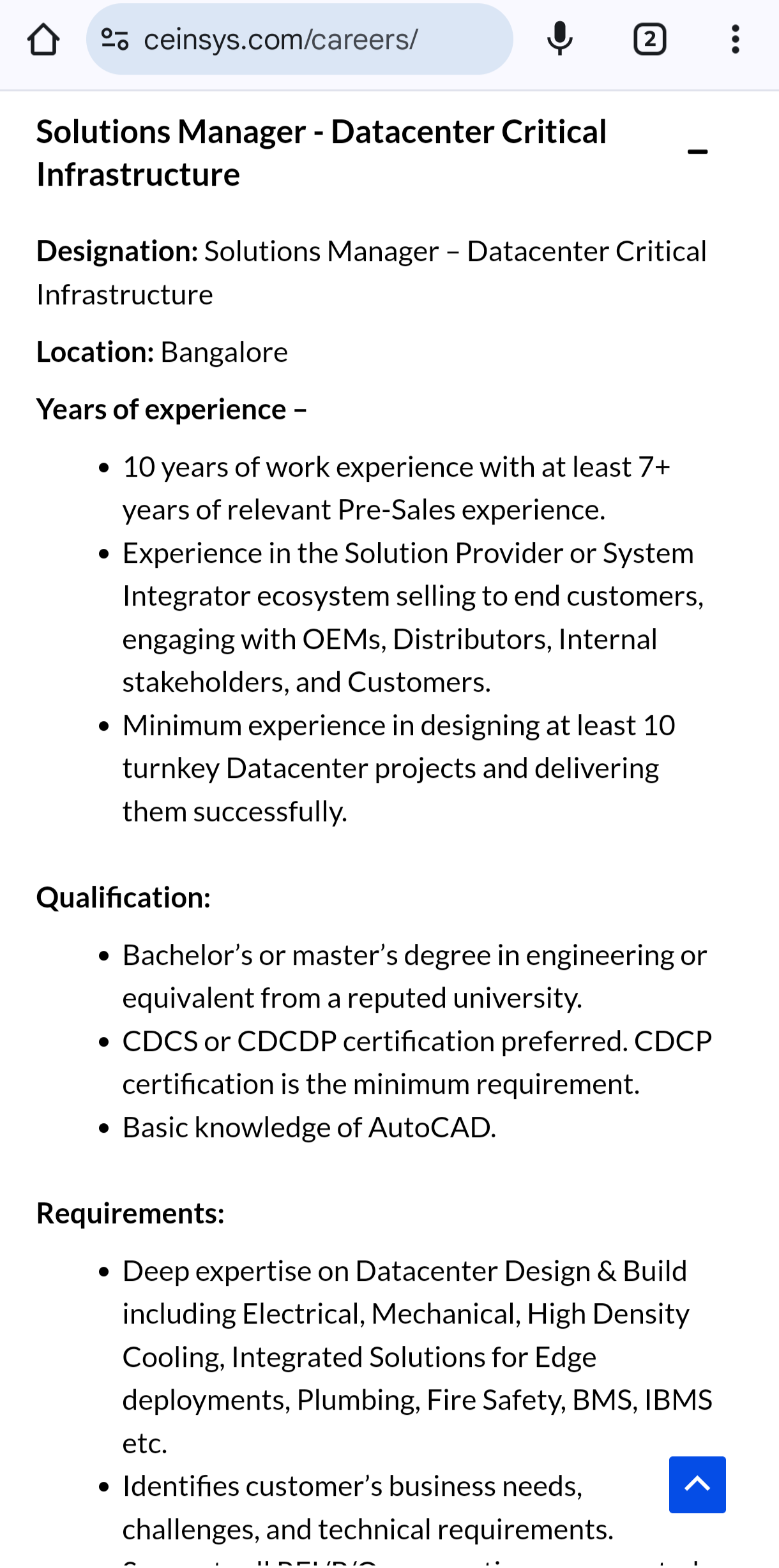

They have one opening in their careers page for datacenter. Looks like they keep options open in new areas. I don’t get the relationship with geospatial.

5 Likes

We can assume it’s Revenue to be 1k cr in 2027. And considering same NPM%, PAT would be 134cr. So expected MCap for FY27 should be 6700cr(50 PE is normal in this segment).

With current Mcap of 3k crore, we can safely assume it’s 2x Mcap increase from current. Price we can expect 3700 in FY27.

Disc: Invested from low levels and still holding tight for very good future.

14 Likes

8 Likes