I have no idea from when Consol will stop being a drag. As of now they are paying Rashi Mehta, John Chwallibog through Technology Associates, USA which is a wholly-owned subsidiary of wholly-owned subsidiary AllyGrow (though both of them have no business with AllyGrow) but simply because this is the US subsidiary they have. VTS as well has been acquired through this step-down entity. VTS is not profitable AFAIK and Rashi is supposedly helping with acquisitions. I think a lot of the impact is due to expensing of ESOPs

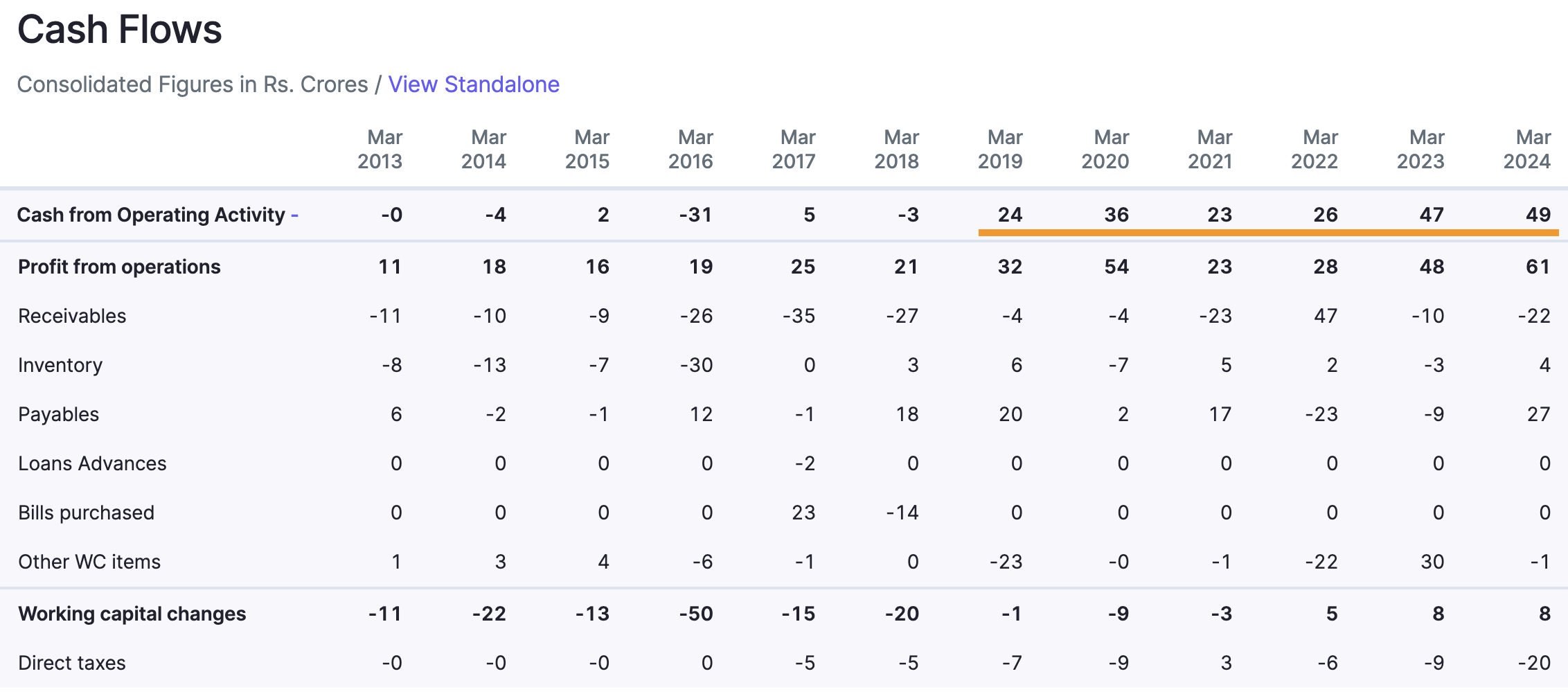

to the tune of 5.39 Cr in Q3 and 11.87 Cr in 9m FY25. This should be non-cash, so I think we should see CFO rather than PnL to see how well the company is doing. The management says the CFO for 9 months is a whopping 124 Cr.

To put this in perspective, the CFO has been ~50 Cr in last two years. The EBITDA → CFO of this company has been stellar which was one of the things I liked about it. To have 124 Cr CFO is nothing short of stellar.

It might be the case that lot of WC got freed up in Q3 and might get locked up by end of Q4 but at least as of now, it is very, very good. Its a EPC company with a nearly an IT company sort of cash conversion and WC days. So I think we should put the consol level drag to the tune of 6 Crs in PnL aside - its probably just the ESOPs being expensed out. alongside higher pay to the two individuals.

I don’t think they are doing anything on the data center side as of now. I dont think they will rush into anything since there’s strong expertise from the investors who have come in - I have discussed it at length here

On Genesys, I think there’s lot of older investors are exiting which is putting pressure on the price. The performance as per PnL is not bad to warrant the kind of selling pressure. We should however look at the CFO here as well by end of year to see how it is since depreciation is quite high (maybe rightfully so, since its in a sector with fast evolving tech)

Tariffs may work on generics but not sure what it can do to NCEs. Blue Jet current numbers are driven by Bempedoic acid intermediates. Its not easy to put up this sort of capacity in US in short period since the exclusivity ends in 2031, so time is of the essence for Esperion. Tariffs will very likely be borne entirely by patients. I think this applies to any product where there’s pricing power across industry.

Also its not easy to put up capacities in US without cheap labour for a lot of industries (like footwear, apparel, transformers etc.) and where supply chains are highly intertwined (CDMO, specialty chemical factories etc.). We should also think if it is even wise to put up capacity and the current US govt is voted out in 4 years and policy changes then. No one is going to commit huge capital with that uncertainty hanging in front of them even where it makes sense otherwise to do so.

Blue Jet P/E was 50x and growth was 100% as per my estimates, which makes PEG 0.5 - which means its highly undervalued. But its stupid to go by simple numbers like these without understanding underlying business levers, growth, moat etc. People who do not understand underlying business strengths/weaknesses use these as shortcuts and at extremes, they do function alright - but I have seen P/E of 15 which looked cheap become a P/E of 8 as well (see Natco for eg.). In general there’s no substitute for understanding businesses - things like index P/E, number of stocks above certain DMA etc., stocks hitting highs/lows etc. kind of metrics are good for timepass and will not help you make lasting wealth as you are bound to be out of the market just as its having its best time or not buy when its having its worst time etc.