Apologies for being late here. I know results season got over long ago. The last time I wrote, Shaily, Genesys, Strides results had come and I had taken a position in Holmarc. Ceinsys and Wockhardt had not come out with results.

I have been writing in individual company threads as I felt the deep dives belonged there, rather than here. Ceinsys result is discussed here. Since then the concall as well happened and most of these assumptions were confirmed by the management. I made some mistakes in my split calculation though my general assumption on how to look at the numbers were right. The wainganga-nalganga river linking and IDDP for MMRDA summing up to 500 Cr must still be in the works as they are not yet disclosed. Orderbook should be strong around 1700 Cr once these are confirmed.

I was also quite surprised by the way market reacted post Mumbai elections. It clearly was a large hurdle going by market reaction. Now that its out of the way, we can focus on the fundamentals. The company announced a 330 Cr order from JJM MH extending last year’s order of 248 Cr. It looks like there might be lot more to come here just in MH. Going by the TPI (third-party inspection) work they are doing for JJM in UP in Lucknow, Chitrakoot and Devi Patan, I wouldn’t be surprised if they land some IoT work there also in JJM.

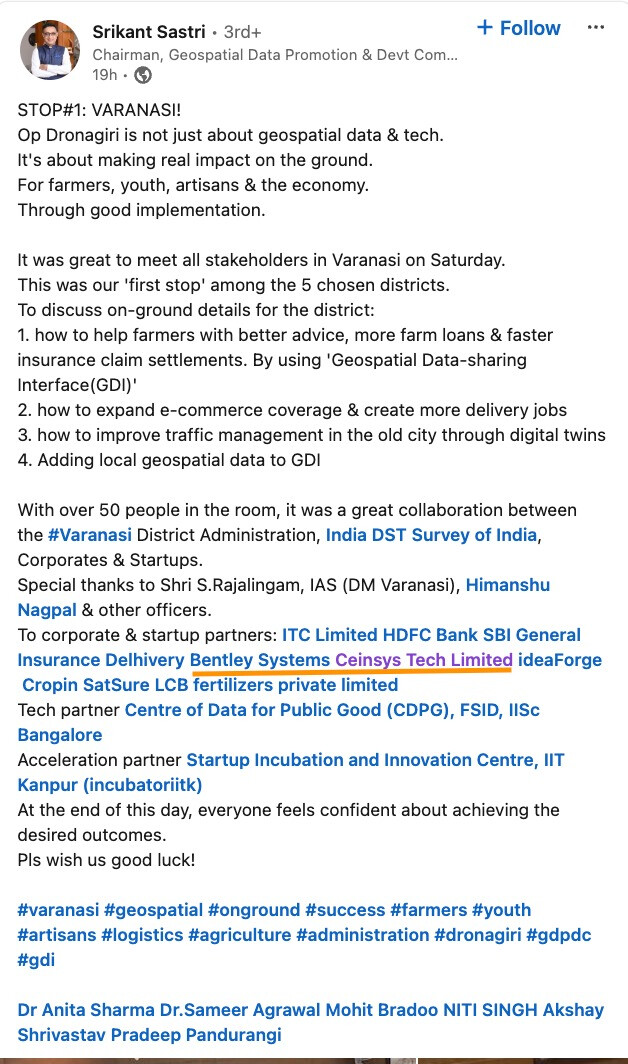

Recently noticed that Ceinsys is a corp partner for the recently launched Operation Dronagiri.

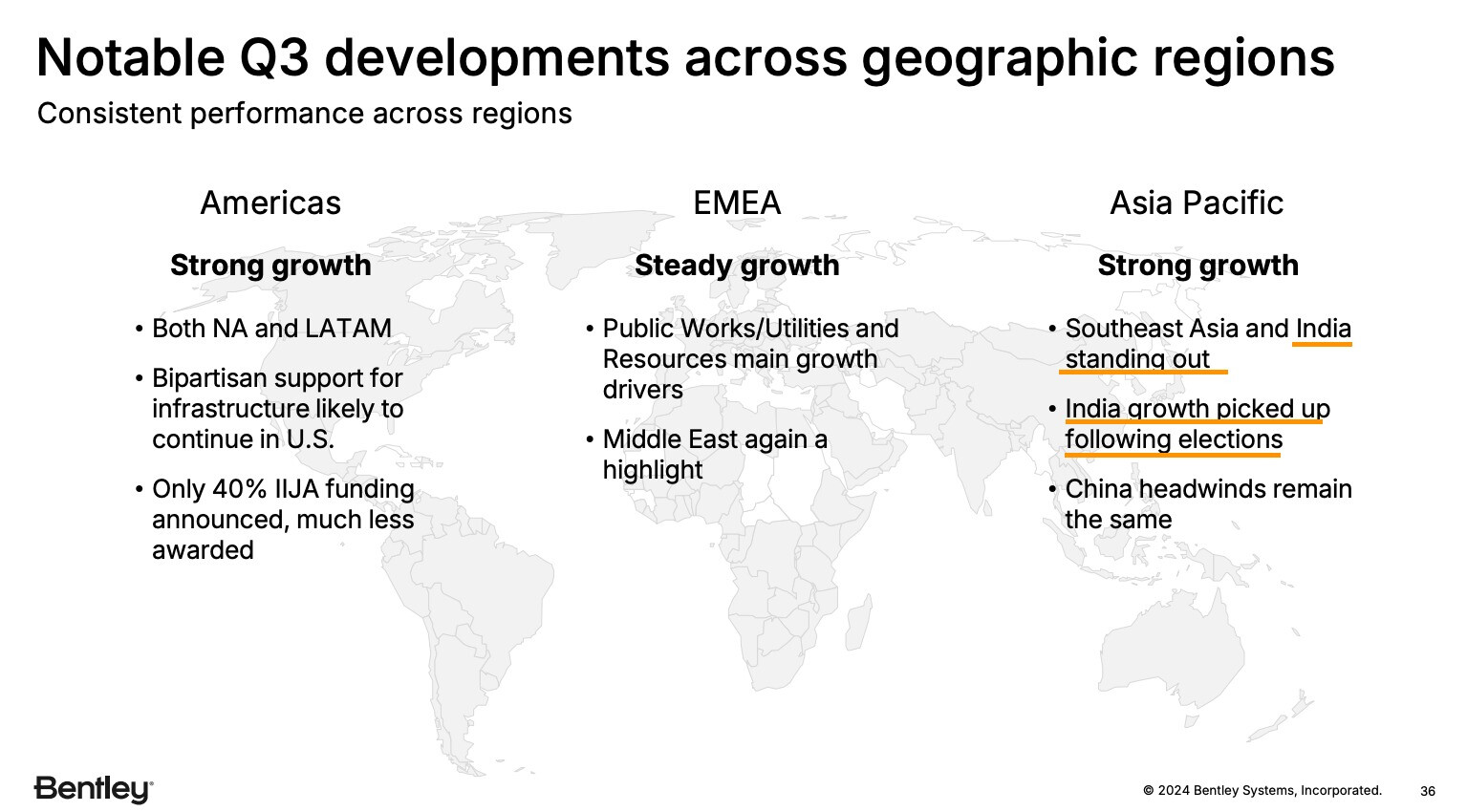

Also noticed how much importance Bentley systems who Ceinsys partners with for geospatial software and licenses is giving India

Other than this, on Wockhardt, I have summarised my thoughts on holding it for a year in the company thread. Everything is going as it should and as per the recent dispatch, there’s another case in US where WCK 5222 has been used on compassionate basis on a cancer patient to counter NDM-producing pseudomonas and Kleb with IMP, OXA-48 resistance mechanisms and the patient recovered subsequently to undergo liver transplant and resume chemo. Also interesting is the fact that the failed therapy included Cefiderocol which is not known to work well in NDM producing strains. This reasserts the superiority of WCK 5222 over CFD that we were seeing in studies (2nd post in the Wockhardt thread) in the real world as well. Presence of these strains in US, increases potential value of WCK 5222 - to put it in perspective, Cefiderocol is $16k per treatment if I remember right.

Made some more headway in Holmarc as well as the causes for tailwind is now apparent. Have couple more posts in the thread as well discussing results and capabilities.

Most of the stocks in the pf have done phenomenally well, backed by strong fundamentals.

Market has refused to listen to bearish views and views claiming that largecaps are cheap. Small/Microcaps have held up quite well this time as expected since fundamentally they are the ones benefitting the most from govt. policies. Post elections, there’s a pickup in tendering and order flow across sectors benefitting from govt. capex from geospatial, defence, railways, infra, space etc. This is going to be the age where the wheels come off globalisation and there’s more local production and that means getting rid of efficiency of global supply chains to put up local capex and put tariffs to protect it. Holding on to consumption stocks and waiting for tax cuts to spur consumption which used to work in the past may not be the govt.'s priority.

Disc: Invested in mentioned names.

P.S. I might stick to writing in company threads since my style has changed so much since I started writing here few years back. Will also attempt to start own thread to write about things that interest me, and about value in general, not just financially