By looking at the Geospecial market TAM in India and company’s growth prospects, PS ratio is a small factor. Real story is yet to be unfolded I think.

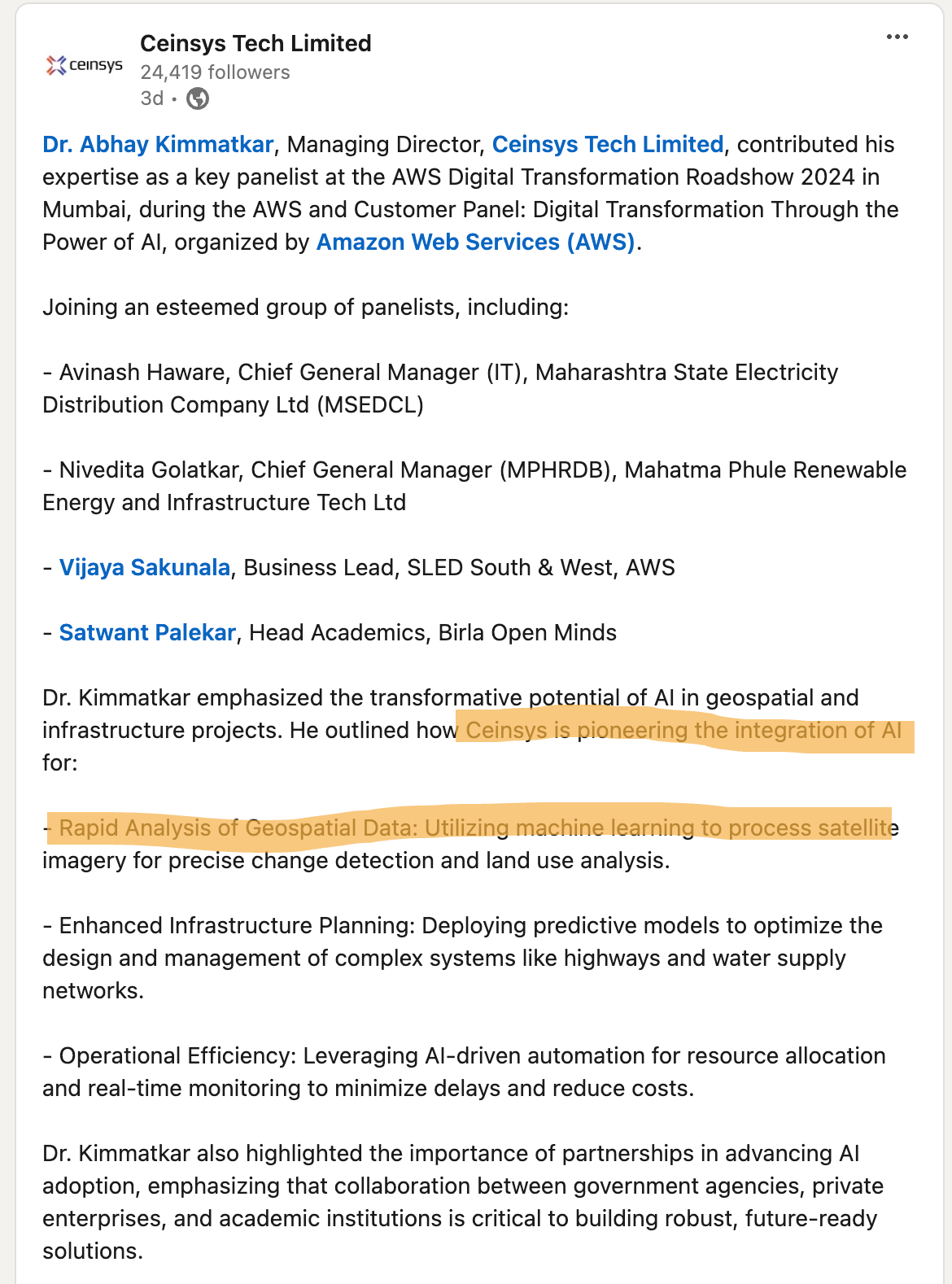

Interesting to note Ceinsys is seen around cloud players now. There is mention about AI for enhancing speed/efficiency of the Geospatial processes.

Ceinsys updates from the other thread.

Ceinsys came up with a PPT today.

So far water has been the driver for Higher revenues, need to check how the other 3 pan out next year.

Acquisitions to be watched out for …Also we can see a CTO for Meg-Nxt vertical at work since 2 yrs,can expect some interesting product suite here as mentioned by management in previous calls.

Slide 36 is a disappointment, unwarranted comparison as Market cap can change anyday.

These are not very intelligent moves. This always puts a question mark on management regarding their intention of pumping stock price.

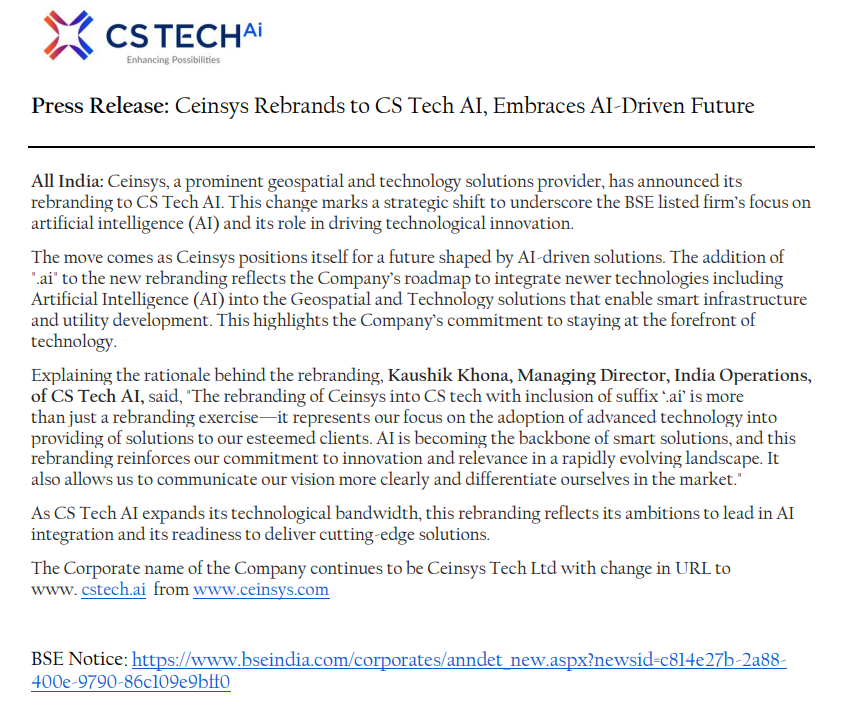

I have mixed feelings about this rebrand - it feels unnecessary unless it is really backed by a big shift towards AI, through some acquisitions. They do have some openings in AI like this

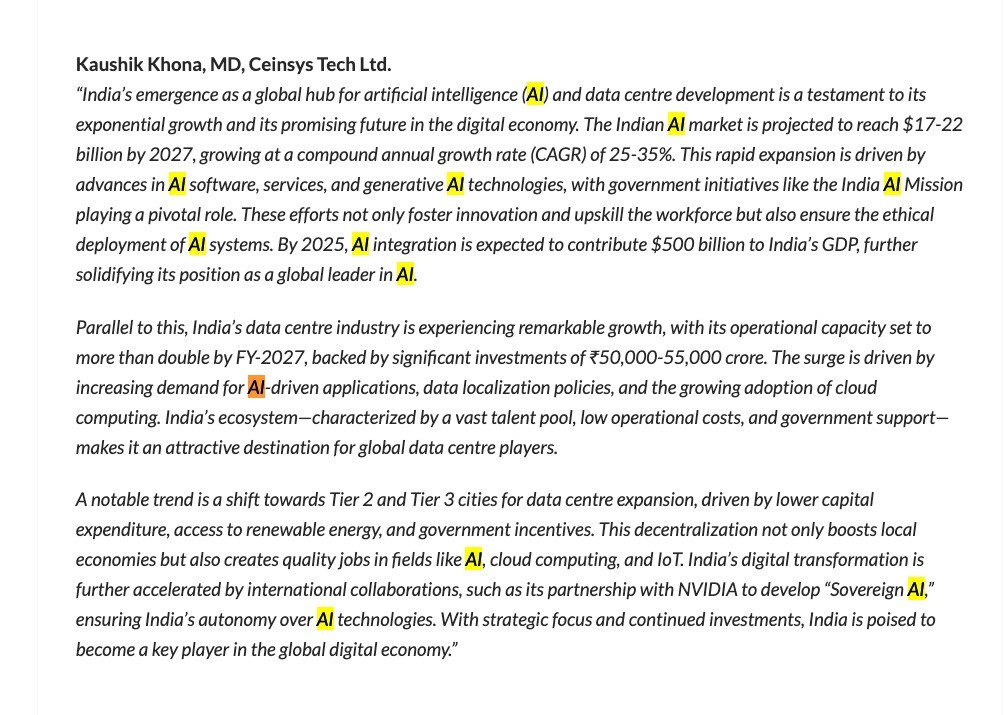

But it definitely doesn’t warrant a rebrand. Also the recent snippet from Mr.Khona for a business magazine mentioned AI 12 times and Geospatial - 0 times.

Other than the usual nonsense about market size and GDP etc., there’s something about sovereign AI and data localisation which are policy driven moves - I can only hope they are trying to participate in these ventures. But Ceinsys currently has zero capabilities in these. It can only come through acquisitions, if at all.

Of course all these are negatives but I mentioned I had mixed feelings - so what I am optimistic about is that the 8.16 lakh options granted to Rashi Mehta have an exercise price of Rs.1916 and a vesting period of 3 years.

Unless she adds substantial value to the company, these options will expire worthless because she will have to put in Rs.156 Cr to exercise these options. To put that in context, Rashi and husband Tarun Raisoni have already put in Rs.125 Cr in QIP (and promoter 100 Cr to protect himself from dilution) - this Rs.156 Cr is more than this QIP amount.

What I like about this is that the exercise price protects me as a shareholder from dilution. Also though John Chawallibog (from VTS USA acquisition) was granted options two weeks back, it was at an exercise price of Rs.1700 odd though both Rashi’s and John’s were filed for approval to the board at the same time. To put it in context Kamat’s options were at Face value of Rs.10 from ESOP '22 and vesting period was 2 years. Board recently changed vesting period to 3 years and the higher exercise prices are great to us as shareholders.

Now why is all this important? Because of Tarun Raisoni and Rashi Mehta’s background having founded Gruve and having built Rahi and sold it for Rs.1800 Cr - they bring in serious data center and AI capabilities and are in this with their own money and have option to build more value for themselves and cash in with the options.

When this new Ceinsys branding was done and AllyGrow was acquired and Kamat and Khona were brought in as well, there was transformation in this company. I can only hope bringing on Rahi founders in the QIP and granting them options and rebranding as CSTECH.ai also transforms the company. As of now I am divided on this since moves like this are cheap market cap grabs in general but given the circumstances the company finds itself in, I stay hopeful

Disc: Invested. No recent transactions

Excellent analysis as always. Why did Rashi accept for 1900+ exercise price when John was given for 1700?

For making it simpler here is what Phreak means.

To calculate the total value of the options granted to Rashi Mehta, we need to make some assumptions:

Assumptions:

- Current Market Price: Let’s assume the current market price of the company’s shares is Rs. ‘X’.

- Vesting Schedule: We’ll assume a linear vesting schedule (options vest equally over the 3-year period).

Calculations: - Intrinsic Value (per option):

- If ‘X’ (current market price) > Rs. 1916 (exercise price), then Intrinsic Value = ‘X’ - 1916

- If ‘X’ (current market price) <= Rs. 1916 (exercise price), then Intrinsic Value = 0

- Total Intrinsic Value: Intrinsic Value per option * 816,000 options

Example (Hypothetical): - If the current market price (‘X’) is Rs. 2500 per share:

- Intrinsic Value per option = 2500 - 1916 = Rs. 584

- Total Intrinsic Value = Rs. 584 * 816,000 = Rs. 475,424,000

- Total Value in Crores = Rs. 475,424,000 / 10,000,000 = Rs. 47.54 crores (approximately)

Note: This is a simplified calculation. The actual value of the options can be more complex depending on factors like:

- Volatility of the stock price

- Time to expiration

- Interest rates

- Vesting schedule (if not linear)

Disclaimer: This is for illustrative purposes only and should not be considered financial advice.

New order of 381 crores.

Company in talks with 3 other companies outside India for acquisition, expected to close by MARCH 2025.

expecting decadal long opportunity for geospatial companies to grow with government’s initiatives for GIS in ( urban infra, water management).

Larger orders >50 crs are expected to be complete within 12- 18 months time frame.

Expecting rev CAGR OF 60%/ EBITDA 64%/ PAT 35%.

slower EPS is due to conversion of warrants to equity.

Src~ aditya birla capital report on geospatial sector.

Excellent Results

CS Tech AI - Q3 FY25 Earnings Highlights

Order Book & Business Updates

- Total Order Book: ₹1,390 Cr (Dec 31, 2024)

- Water Infrastructure: ₹1,189 Cr

- Geospatial Solutions: ₹199 Cr

Major Contracts

- Maharashtra River Linking Project: ₹381 Cr

- IoT Water & Sanitation Project: ₹332 Cr

- GIS Enterprise Implementation: ₹29 Cr

- MADA Digital Transformation: ₹28 Cr

Technology & AI Growth initiatives

- MegNext AI Initiative launching for gaming, EdTech, and mobility

- AI automation driving margin improvements

- Data Center business evaluation expected within 2 quarters ( Disappointing to see Data centre has taken a back seat after so much of talk in the earlier calls with new investor coming in with Experience in DC)

US Expansion

- Strengthening U.S. & European presence through VTS acquisition

- Expanding private sector focus, Building U.S. business development team

Fund Raise & Strategic Investment

-

₹235 Cr raised: 70% for acquisitions, 20% for expansion and rest for working capital

-

Two acquisitions in final stages (geospatial & AI analytics)

-

Working Capital: Improved from 237 to 124 days (Mar '23 - Dec '24)

-

Cash Position: ₹125 Cr total (₹20 Cr operational)

Forward Outlook ( NOTE: Company not willing to give guidance but investors in call inferred the guidance )

- FY26 Execution Target: ₹550 Cr

- Revenue Goal: ₹1,000 Cr within 2-3 years

- Quarterly Order Pipeline: ₹400-450 Cr

- Bid Success Rate: 85-90%

- Tech Solutions: ~65% of revenue

The company recruited 384 employees throughout FY25, 277 are technical experts who enhanced its capabilities in AI and geospatial engineering and technology solutions.

Focused its hiring on the following areas:

-AI & Machine Learning and Geospatial Engineering and Mobility & Automation Solutions and Software & Data Analytics.

- to have sufficient resources to deliver new projects and expand existing ones.

- to expand its international business development team through strategic hiring in U.S. and European markets to boost private sector growth.

On US operations: The company has several acquisition deals in the final stages of evaluation with expected closure during the next 2-3 months. Allocated funds to expand its U.S. operations which raised business expenses and reduced profit margins.

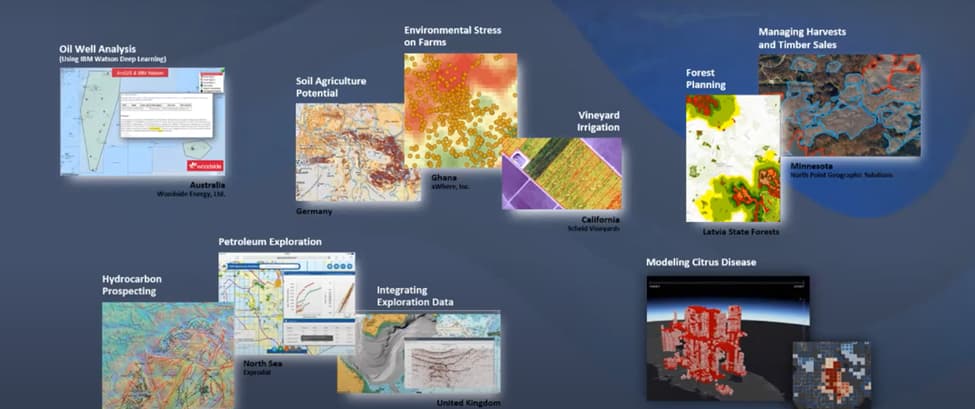

ESRI one of the largest GIS software company has been talking about a lot of AI/ML uses in GIS analytics.

In a ESRI webinar they have been talking about using IBM watson deep learning for woodside energy’s oil well analysis.

Python scripts can be used in Arcgis to automate some of the work flows.

Geospatial artificial intelligence (GeoAI) is the application of artificial intelligence (AI) fused with geospatial data, science, and technology to accelerate real-world understanding of business opportunities, environmental impacts, and operational risks.

A lot of machine learning is going to be used in GIS analysis.

Some of the projects where ESRI was used

Machine learning and deep learning is widely used in Geospatial analytics.

It may not definitely warrant a name change. But it would be essential to build these capabilities.

And if someone wants to have a look at use cases. ESRI has a lot of case studies in their blog.

Amazing results !!!

I was just expecting 55 to 60 Cr bottom line(year) .

it turned out to be ~ 1.4 times my conservative estimates.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0891d93b-aab5-4082-b888-9a1d6928c679.pdf

Good results but any idea why trade receivables increased so much? Operating cashflow dropped significantly due to this.

Yes same is the case with Genesys. CFO is quite low between the two

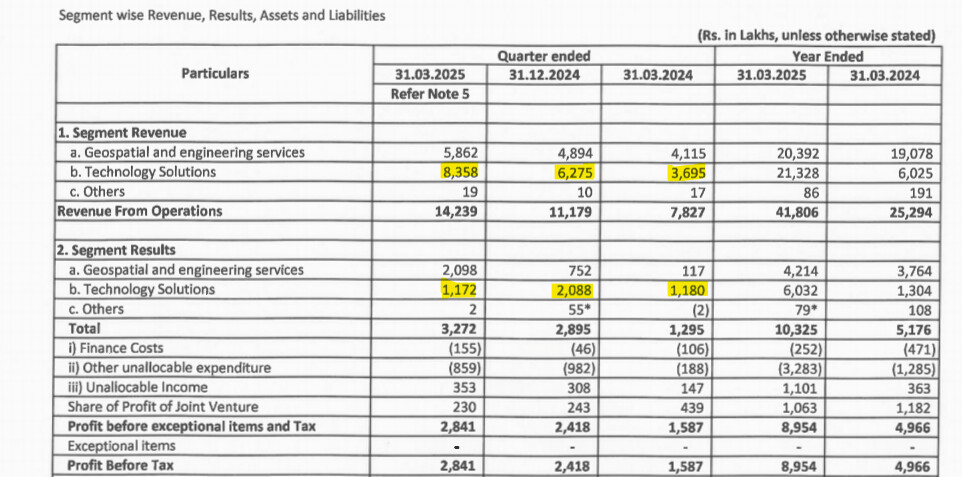

There is too much variation in margins of Technology solutions.

Wild swings are not good

Margins are improved for Geospatial but they were tad low in Dec Qtr.

They need to stabilize the segments to get the attention of the Market.

Good Thing is Revenue has been growing for Technology Solutions May be due to acquisitions ,Margins need to be improved for better bottom line.

Disc: Invested