2 Likes

Earlier the company used to do business with related party (promoter owned company) MEBL. There was suspicion around it. Then they merged MEBL with itself. The merger was also suspicious. Please read dedicated thread on the company. You will understand how minority shareholders were taken for granted.

https://forum.valuepickr.com/t/associated-alcholols-breweries-ltd/

“There’s never just one cockroach in the kitchen” – Warren Buffett

3 Likes

Dhanlaxmi bank.

Fundamentally the bank isn’t showing much but the PA shows that something is brewing. Might be a takeover candidate.

IMO it’s a punter stock or an operator one i don’t know, what I know is to define my risk and play along. Simple horizontal line breakouts, relative strength and volumes on up days. ticks’ lot of right boxes.

plz do share if one has any funda inputs for the same.

disc : invested from levels of 42

1 Like

Shriram piston and rings

Mcap: 9211

Pe ratio: 20

Roce: 28%

Roe: 25%

Promoter holding: 46.75

Key triggers (fundamentally+ technically):

•Commencement of

manufacturing operations by SPR Engenious Limited, a wholly-owned subsidiary

of Shriram Pistons & Rings Limited (SPRL) on March 27

• Abakkus ( Sunil singhania) bought huge stake from Ks Kolbenschmidt Gmbh at rs1,104 on December 2023.

• diversification of product portfolio

•recently had been consolidating and broke its trendline

•strong management, stable business,healthy cash flows, 25% cagr sales growth (3 years) , 26% cagr net profit growth (5 years) and still trading at 20pe

Disclosure: invested last week

14 Likes

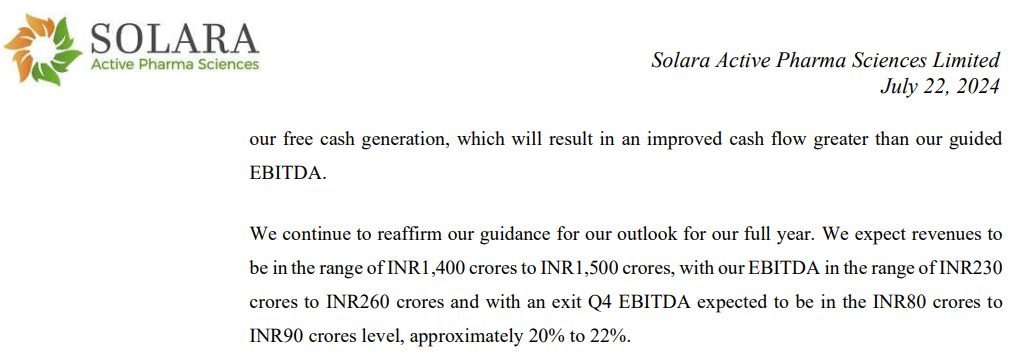

Solara Active Pharma - New 52 week high today. Technically, stock entering possibly in Phase 2 after a good Stage 1 basing period of 2.5 years.

Management has guided for 1400-1500cr topline and 230-260cr of EBITDA with Q4 EBITDA of 80-90cr. IF these numbers are delivered then current valuations are reasonable. IF their CRAMS business starts contributing - then this can become more than FY25 numbers play.

Disc: no position

10 Likes

@phreakv6 - I know you recently sold your holdings in Sharda Motor Corp but was wondering if you still tracked its recent results. If yes, would appreciate your views on it. Since its spectacular run up, the valuation gap seems to be closed to an extent for the time being. However, from a technical perspective, it seems to be consolidating in a range at 10DMA and 20 DMA with low volumes, which might be a good thing.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/75a73513-0bfb-48d0-bdda-97d1ef949eeb.pdf

Balaji Amines: All the moving averages have been contracting for 2.5 years. The stock looks good on a weekly timeframe and might be ready for a breakout.

Triggers lined up for the company:

Electronic Grade DMC: The existing DMC plant is under execution, which will be commissioned during FY 24-25. This has good demand for EV Batteries which has good potential in the coming years we are the only manufacturer of DMC in India right now with an installed capacity of 15,000 MTPA.

Dimethyl Ether: The project for the manufacture of DME is under execution at Unit-IV. The Plant is expected to be commissioned around March 2025. This has an application in the Aerosol industry apart from using as a replacement to LPG for Industrial and Commercial usage. The Bureau of Indian Standards (BIS) has initiated to blend DME 20% with LPG seeing the advantages of DME. The same is under final printing as Gazette Notification.

- New expansion of approximate Rs 750 crores in Subsidiary Balaji Speciality Chemicals Limited

More details are available in the latest quarterly presentation. It’s more of a contra call as the chemical sector is still out of favour. The company has posted not-so-good results in Q1FY25. It’s best to wait for the quarterly call before taking a position.

8 Likes

With all the results out, its a good time to review the trades.

Shaily, Weekly - Has formed a flag sort of formation on the weekly and is trading at near-term breakout levels. Any close above 910 levels should ensure a continuation.

Results here are good and with the 10 million own IP pen insulin order, things are looking very good on the healthcare business. There are signs that there could be more such orders with insulin space opening up after Novo and Lilly leaving it and moving capacities to GLP-1. Considering the base of 11.5 million pens which is fragmented with bulk of it under contract manufactured insulin pens (probably 60-70%) and rest as well under different platforms, mostly for clinical test batches, a single platform doing a 10 million volume should lead to good operating leverage and margins. Valuations don’t appear cheap on P/E basis but the potential here is huge if willing to hold over 2-3 years. The healthcare division growing topline at 50-60% CAGR and bottomline probably at 70-80% can backfill valuations very quickly. The company is also developing two new devices and has guided for 35-40% growth in Shaily UK as well (so new customer contracts should continue). Concall has more detailed info on the business.

Wockhardt, Monthly - At crucial levels around 8 year highs. Getting into 4 digits would be a big psychological boost (doubt if there are buyers from 2016/2018 still sitting here selling - its more a theoretical barrier than anything)

Results here are very good as well with standalone PAT turning positive and losses narrowing considerably on the consol. Though this was never a play on existing business, sometimes when things go right, they tend to go really right (munger’s lollapalooza). The insulin shortages mentioned above should also benefit Wockhardt’s insulin business. Any good news on the base business would be a big boost to valuations. 422 patients recruited for 5222 global trials and 33 compassionate usage cases with 100% recovery. The meropenem resistance trial also has 15 patients recruited as per the update on the press release. So looks like everything is on track so far.

Ceinsys, Monthly - After consolidating and failing to take out 620-650 levels for 6+ months, its trading above those levels.

Results are very good though geospatial has been a big drag on the numbers. Despite that the numbers are good because of AllyGrow. As per the concall, geospatial business had issues due to elections code of conduct but some of the costs are booked. Between Q2-Q4, this should turnaround and have lumpy profits that make up for it. On a whole year basis, management thinks both the geospatial and allygrow business should have 20-25% margins and should grow ~25% over next 2-3 years. A potential doubling of topline with margin expansion from 17% to 22% can mean a 3-4x from here if execution is good, considering starting valuations aren’t too demanding for the growth.

Orchid - Broke out last month and is trading at or around those levels of monthly close (~1400). Expansion in oral capacity and better utilisation in sterile would help base business grow, while cefiderocol would start contributing from FY26 and 7-ACA from FY27. DLL merger and Enmeta royalty is more near-term in FY25. Overall there are enough triggers for growth here to sit tight for a couple of years. Re-entry in US business should bolster margins in base business while volume growth in emerging markets will help improve operating leverage as it has done so far. The numbers are bit depressed for the quarter since the AMS division has had 50+ hires in sales and marketing so employee cost (to the tune of 2.5 Cr) is more a longer term investment in developing distribution.

Genesys - Good numbers though here too I think they have been affected by elections (As mentioned in the ceinsys call) and also the weather (as mentioned by Sajid in couple of tv interviews post NNG partnership). The numbers here should pick up steam H2 onward going by those interviews as he says that the payoff for last 2-3 years of product development will start contributing from H2. The press release also talks about several favorable market developments across sectors like renewables, urban planning, real estate, land records and disaster management. Technically taking out 750 on a monthly close is essential for continued strength.

Among smaller positions - Eimco, Tarachand, Strides, Garware, Sharda and Pix have all had good numbers as well. Garware especially was a blowout quarter with IPD turning out as well as better margins across value-added products and improved volumes. Sharda am not certain can sustain growth on the base of the last 4 quarters - i feel next lever of growth is a bit in the future with TREM-V (but valuations aren’t super demanding, so it might trade sideways?).

Disc: Invested and likely to be biased. I write to gather my thoughts and this is not advice and I am not qualified to advise. Please do your own due diligence

102 Likes

@phreakv6 - I always look forward to reading your posts here, as well as on the other one, where you post your book reviews, delight to read!

Ceinsys conducted their first ever con call, posting the link here: https://www.bseindia.com/xml-data/corpfiling/AttachLive/601a35d1-aa0b-42ac-8d5a-65b1a6b44e61.pdf

Some key takeaways:

• VTS acquisition might add 1M$ to topline of Q2. (Correcting this to 1M$, as 3-4M$ was the annual revenue of VTS)

• The overall fund raise will be in the range of around $25 to $27 (for new acquisitions, appointed Care rating agency for overseeing fund usage)

• Growth Potential: Sector growth expected to be around 20%-30%.

• Order Book: Current order book worth 750 crore to be executed in 2-3 years.

• Recent Acquisition: Acquired VTS, a US-based geospatial company with a top line of $3.5-$4 million.

• Future Growth: Planning to raise $25-$27 million for further acquisitions.

• Data Centers: Setting up tech-enabled data centers in Singapore.

• Revenue Expectation: Potential target revenue of 20-30 crore from new data centers.

• EBITDA Margins: Expected to maintain +20% margins, aiming for 25%-30%.

• Government Business: 65%-70% of business from government tenders.

• Seasonality: Q4 typically the strongest quarter due to financial year-end project completions.

• Government Project Payments: Generally prompt, with 15-20 days outstanding; occasional delays due to fund allocation.

• Joint Venture Performance: AllyGram contributes significantly with 26% margins and a projected 45 crore top line.

16 Likes

Here are Elliot wave counts for Ceinsys .

Target goes beyond 2000 if everything goes wall.

No buy/sell reco.

18 Likes

Hi stage investing,

I see its in minor wave 3 of major wave 3.I do use fibonacci ratio to calculate targets .can you explain the technique you use to calculate targets for learning purpose.

2 Likes

In EW , we assume that wave 3 would be equal to wave 1. It is calculated on logarithmic chart.

5 Likes

SWSOLAR

CMP 700

CAN THE COMPANY REALLY TURN AROUND ? Turned profitable in last 2 quarters. Con call was encouraging.

We tried to do the EW counts on the same.

Disclaimer: No buy/sell recommendation. Just sharing a technical chart.

8 Likes

Pharma as a sector has been on a tear for last couple of quarters and seems to be picking up good pace.

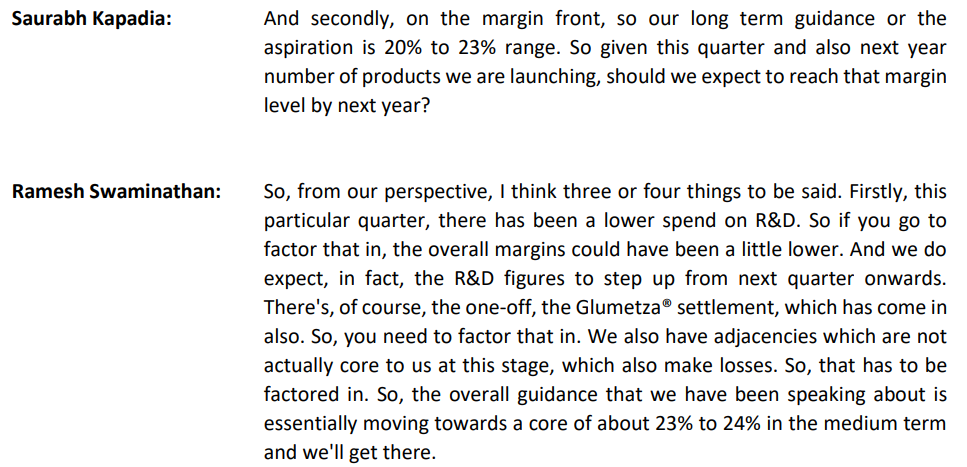

Lupin Weekly Chart. It made a new ATH lately after 9 years. If one notices, PAT was 2444 in FY15. Current TTM PAT is yet to cross FY15 PAT but stock has already moved higher. What a roller coaster in margins it has had. From 28% peak EBITDA to 1% in FY22 and now back to 20% for TTM.

Management guided to get back to 23%-24% EBITDA levels in medium term along with healthy topline growth. US, Non-US, India markets - all are doing well and company has a decent pipeline of products to be rolled out in next quarters.

Disc: trading position

22 Likes

Below are the charts for gold/ silver.

Gold 25 year chart

Silver 25 year chart

Both Gold/Silver follow similar upside /downside movements, the movements in gold are less volatile as compared to silver, but silver give big moves than gold.

Gold has already reached all time high, waiting to see a big upmove in silver also.

Hindustan Zinc is a key producer of silver

Seems to resume the upmove after testing support at Weekly 50EMA

Disc:Invested in both silver ETF and Hindustan Zinc.

14 Likes

Been a couple of months since last update here. Market has gone through its usual shakeout earlier this month and has bounced back just as it has done in the last few times. I saw people going into cash or going into banks and nifty - I think these are not so good moves.

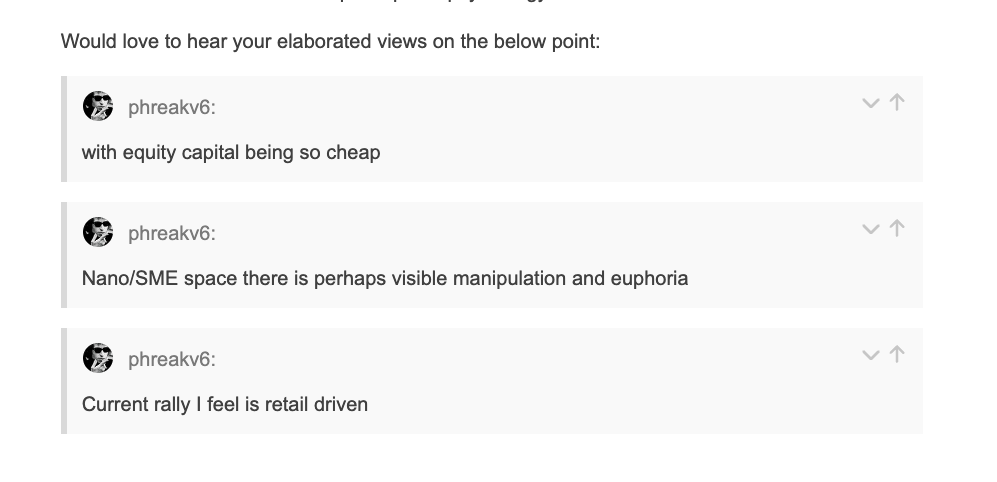

While Nifty companies and the banks are relatively cheap, they are so for a reason. India’s growth in the last couple of years has been driven by erstwhile underperforming sectors, mostly in manufacturing and infrastructure. Nifty and Banks are focused primarily on consumption and banks have a problem with both demand and supply with demand going down due to deleveraged balance sheets and supply from higher rates causing NIMs to shrink. Its hard to say how long this will go on with equity capital being so cheap - so much so that it feels like a structural shift (I will reserve my judgement on that but so far, it does seem so).

Growth will continue to be driven by manufacturing and infra and capital goods and businesses focused towards these sectors are mostly smallcaps barring a handful of midcaps. A lot of ancillaries catering to these manufacturing and infra smallcaps are the microcaps and nanocaps universe - I think this is what we should keep in mind when someone says smallcaps/microcaps have runup too much. In the Nano/SME space there is perhaps visible manipulation and euphoria and venturing there should be done very cautiously.

Even if there is a crash, I expect a situation similar to 2018 herding to happen. However, this time herding may not be into Nifty and Banks but into smallcaps with great growth visibility. 2018 herding was driven by large fund managers. Current rally I feel is retail driven so I find it hard to believe they will get into a HDFC Bank or Reliance. Also fundamentally the way the economy is growing, i expect a lot of microcaps to become smallcaps and smallcaps to become midcaps than mid and largecaps growing bigger. It is simply not that kind of economy at present.

No changes to pf, except scaling up Strides. But there are lot of business updates which are worth looking at

Shaily, Weekly - Running sideways last 2 months. Fundamentally, the insulin opportunity could be big and there could be more where the 10 million pen order came from - discussed in the Shaily thread

Ceinsys, Weekly - Strong breakout on the weekly. It reminds me of the breakout in Shilchar from 1500 levels where it doubled in a month. Showing similar sort of strength here.

Lot of order wins taking the orderbook from 750 Cr to 1150 Cr which is phenomenal for a company with 275 Cr topline at present. Another good thing is the order size itself is going up and crossing 300 Cr+. I have discussed the moat ceinsys has in detail in the Geospatial thread. There might even be another large order of 385 Cr for which Ceinsys is the L1 bidder (explained in the thread).

The company expanded seating capacity by 200 last month and has so many open hiring positions. There is clear hunger for growth here

Wockhardt, Weekly - Gap up and circuit close on Friday and expect strong week here

WCK 5222 trials seems to be progressing well and should be completed in a few months time. Nafithromycin has got approval from CDSCO and should be in the market in a few weeks. WCK 6777 has got fast track status from fda after its phase-1 completion as per recent update. The market opportunity for Nafithro in India alone seems to be 400 Cr opportunity as per the chairman. Another good thing is the insulin opportunity as mentioned in the last post in August. There is a structural shift to biosimilars for insulin glargine driven by WHO and African countries are making this shift already (as with Algeria’s Biocare as mentioned in the Shaily thread). In developed markets as well price controls have put an upper ceiling of $35 and there’s a drive to make insulin cheaper through biosimilars. In all, the base business for Wockhardt is becoming stronger even as the NCE molecules are nearing fruition.

Strides, Weekly - This is one of my favorite chart patterns and it played out very well in VBL.

Fundamentally, this is a play on GLP-1 fill-and-finish, alongside a demerger opportunity. Stelis/Onesource is the fill-and-finish partner for Natco who has FTF on Ozempic. I would suggest going through @rupeshtatiya 's excellent thread on Strides, along with his recent AGM notes post. I think a 50-70% upside at least exists here from current levels conservatively.

Genesys, Monthly - Breakout and re-test. It should successfully pull away and close higher this month, hopefully.

Order book stands at 550 Cr. Bid pipeline is strong at 3000 Cr. Near term as well company has guided for executing substantial portion of the BMC order this year (350 Cr). H2 here should be strong

Orchid, Weekly - Multiple re-tests of previous breakout levels so needs a close above 1500 for continuation. There are lot of triggers in the next FY so things should get priced in over time. No big update here.

Small positions in Eimco, Tarachand and Garware remain and all of them have very strong tailwinds as well. I think that in general is the gist of it - if you see the 6 stocks discussed as well, they boil down to just 3 themes with tailwinds - GLP-1 (Shaily and Strides), Antibiotics (Wockhardt and Orchid) and Geospatial (Ceinsys and Genesys) - there’s a sub tailwind in insulin within this (Shaily and Wockhardt).

Apologies for the long post. Will stop here ![]()

Disc: Have positions in all as disclosed before. I am not SEBI registered and just a novice writing for clarity. Please do you own due diligence

146 Likes

@phreakv6 : Thanks for an usual captivating note covering the entire spectrum of market, individual business and market participants psychology.

Would love to hear your elaborated views on the below point:

6 Likes

the way the economy is growing, i expect a lot of microcaps to become smallcaps and smallcaps to become midcaps than mid and largecaps growing bigger

Historically, this does not happen much though. A few will, but more often than not, most of them are unable to navigate roadblocks/changes well. Reasons could vary - recessionary impact, supply chain disruption, govt payment delays, leverage etc. Will it be different this time? Also, I find it hard to imagine people will herd into smallcaps with great growth visibility if there is a crash. Most of them are already richly valued - with relatively smaller float, a few key investors along with strong retail interest have pushed them up much too quickly in my view. Even assuming the growth triggers play out, it is hard to see funds get in even at slightly lower valuations to drive them further up. I could well be wrong, we will see.

That said, I wish I had taken your excellent Wockhardt note more seriously. I have been take by surprise by the rapid surge there. It’s not been a well-run firm for the longest time, so it’s a bit strange to see it take-off the way it has on the antibiotic breakthroughs narrative. A big miss for me, but I guess that’s part of the game.

Great post as always and thanks for all your contributions here. Fantastic food for thought.

11 Likes

Can you please elaborate?

4 Likes

I agree historically this hasn’t happened and probably won’t this time too but history doesn’t repeat but rhymes as they say. Pre 2008, capital goods, infra, manufacturing did quite well but post 2009, companies like page industries did very well and so on. When we look at different slices of history, smallcaps from different sectors have become midcaps/largecaps. There is a tendency for certain sectors to outperform others and this has more to do with what’s happening outside those companies as well though we tend to give them and their management all the credit.

Historically we havent had GDP growth without credit growth either - but now we are seeing govt. led capex even as private is sitting on lean balance sheets with cash - so there’s no credit growth though there’s GDP growth which is also confusing people.

So depending on how far back in history you go, you can always find some similarities to what’s happening currently. We have been a services and consumption driven economy in the recent 10-15 years which is why our Nifty today looks like this - heavy on financial services, fmcg, IT, Auto etc.

Our govt. has taken a bold step to tax heavily both direct and indirect and invest heavily in capex. This govt. driven capex is what is driving earnings in small/microcaps (To some extent midcaps too) but not in largecaps because these became large in the consumption driven economy in the first place (except a few like L&T, Cummins, Siemens, ABB etc). This has a precedent in a country like South Korea. I feel this is a fundamental shift in approach from the govt. and as long as this policy stance is in place, I will stand by what I said.

Why do I think this policy stance can continue? See the fiscal deficit print from today

Collections are higher, expense flat, capex is down (due to elections CoC, will pickup big time in H2 as we are seeing in tendering activity), < 30% of target for year means it will remain in control for full year. Our earlier concerns with this approach has been fiscal deficit and foreign capital fleeing and currency weakening and so on - now we have strong reserves, strong domestic flows if FIIs flee and deficits are well under control.

As long as there aren’t elections to win and votebase to appease, this might be the stance. What was nice was the govt. didn’t let up the stance even in election year which is telling us something. But this cannot come at the expense of consumption, so I would think a rate cut should come sooner or later which will ease consumption concerns (auto inventory, fmcg issues) but the govt. capex should resume full swing in H2.

So when people say correction is coming in smallcaps, the perception is that its completely driven by irrational flows. There’s always more to it when such simplified answers are provided. I think its a combination of govt. policy favoring these companies which were beaten down, the earnings driven performance bringing in more capital and of course the eventual fomo driven expensive valuations in some pockets - but as long as the policy stance remains intact there will be adequate spaces to fish in for a bottoms-up investor imo. As long as Nifty composition remains as it is, it may never reflect the actual economy which is a bit more accurately reflected in the smallcaps (re-rating is penciling in future growth as well, assuming policy stance continues, so of course it has overshot).

Equity capital is cheap as is evident from the number of QIPs and general market levels. Generally equity capital is more expensive than debt capital but the flood of equity capital has lowered perceived risk in equity causing this behavior. Nano/SME space - please read the dispatches some of these companies trading at 100x+ P/E or are loss-making are sending and check the noise on twitter or the buy calls on sms/telegram etc. Current rally being retail driven - I think you can see lot of supporting evidence on cnbc where they cover who sold/bought and how much retail is buying etc.

I think that’s enough with the macro gyan which is more likely to be wrong depending on how far from the future you look back at.

As for where I have put my money in, so far 3 results are out and all are stellar -

I have done some research on ceinsys and have added those inputs in the geospatial thread and the ceinsys thread. This one seems to be getting better and better, the more we unravel. Nothing new on Wockhardt as we wait for trials to complete in the next couple of months. Hopefully results in these two also would show good trajectory.

Other than this, have taken a new bet on Holmarc - covered in the Holmarc thread. Its a purely fundamental bet but technicals also look quite strong with a year long consolidation with volatility contraction and a breakout this month.

Disc: Have positions in all names mentioned. I am not qualified to advise.

78 Likes