Notes from Q1 call

-

2 new FMCG products, 2 new pen injector contracts (1 lanreo and 1 sema), 2 components for automotive customer

-

Getting into Human Factors Engineering to cater to big pharma

-

1 pen injector purchase order for 10 million devices per year (own IP insulin pen) - context is 11.5 million pens done in FY24 and most were contract manufactured

-

Revenue growth will be much higher over the next 5 years

-

Tirze clinical batches will start end of year or next year (tooling and design work going on now)

-

Teri/Lira launches this year in regulated markets in EU/US. Sema in '26 India/Brazil/Canada/China. Rest by 2029. Tirze 2030 RoW and 2036 in regulated

-

Every pen in the market except Novo’s FlexTouch and Shaily’s Neo are mechanical pens for Semaglutide and not spring driven - others have IP challenges

-

3 Exhibit batches (3 PQ batches) are supplied on each contract for pen injectors. Per batch is 10k so 30k total in PQ batches. For different strength, there are separate exhibit batches - so for sema, it could be 90-120k per customer. Then operational qualification, design verification, final assembly trials are extra

-

Of the 25 projects, most of Teri, Lira, Sema (Ozempic) exhibit batches have been supplied. Sema (Wegovy) is starting

-

Shaily UK will see above 35-40% growth in FY25. Pipeline is quite strong

-

Two new projects in Shaily UK for two new type of drug delivery devices - which aren’t yet generating revenue but under active development (Premium Reusable device, Nasal soft-mist inhaler)

-

Working with some consumer electronics companies - very early stages

-

Home furnishing 50 Cr, Pharma new applicator 35 Cr and Engineering plastics for GE around 40 Cr have started and on track in Q2 (no delays)

-

Home furnishing demand in plastics and carbon steel - no big growth expected but some growth will be there from new projects. Carbon steel there will be some growth

-

Q1 healthcare business had a lower growth because of a technical issue which has got resolved and supplies have resumed in Q2

-

CDMO fill/finish partner has no involvement in verifying design (limited knowhow in India). Shaily’s contracts are with pharma companies and verification happens there

-

Working on Monoclonal Antibodies using autoinjectors but its too soon.

-

18-24 months to capacity expansion. Currently at 40 million devices (some platforms might need expansion)

-

Ypsomed moving away from Insulin towards GLP-1 opening up the space. So several ongoing discussions underway and order pipeline is getting stronger. (The 10 million order could be a precursor for more such)

-

2-3 million pens in Lira possible by FY26/FY27 - could be more depending on launches and Customer’s success rates

-

70% of sema generic market can be captured by Shaily. Working with MNCs and small biotechs as well, alongside Indian generic players

-

Consumer electronics - will be working with HPP (High-performance Engineerig polymers) than ABS.

-

Shaily devices won’t infringe - $180k spent to conduct FTO (freedom-to-operate) to ensure same

One of the informative pieces I came across from Ypsomed. Highlighting a few things I found interesting

The market is much beyond glp-1. Pretty much anything that’s a biological is a potential market and this market is growing. Some of the existing interferons, monoclonal antibodies are offered through pre-filled syringes (most generic humira launched last yr for eg.) and due to patient preference might migrate to auto-injectors as well. It is nice to know Shaily is working on auto-injectors for monoclonal antibodies as well.

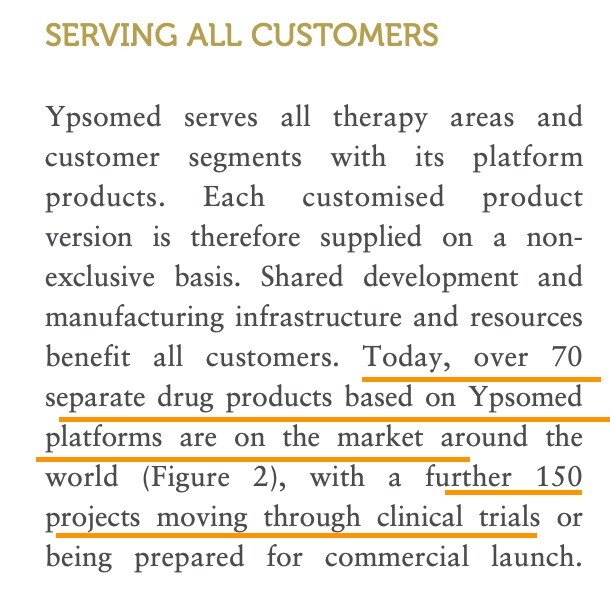

Ypsomed has 220 projects (commerliased + pipeline) and shaily is today at 25 total. Shaily is picks and shovels player in the generic market which means a lot more projects for same molecule/therapy than a device maker that primarily works with innovators

Disc: Invested. Added in the last 30 days and likely to be biased