Different levels of recovery this week. Nifty < Mids < Smalls < Micros. Sort of emphasizes the point I have been making.

60 Likes

Cannot agree more, since yday we are witnessing recovery in Small and Micro

2 Likes

i dunno if i can recollect a better example of either DI, or ‘a picture tells more than a thousand words’ (and we have 4 pictures here).

thanks for the summary.

additionally, have been toying with the idea of an sme basket. great input to think about.

4 Likes

Thanks for the reply. You make some good points - quite possible my perception about the smallcap correction is incorrect. However, I don’t think the GDP numbers are all that accurate and while govt capex has supported, it’s not as great as it’s touted to be either. Part of it is shifting things around too - e.g. NHAI off-budget debt being stopped (which is still extremely high) and budgetary allocations increased instead. The ex-finance secretary had a recent column about it (edit: actually, last year - not recent) - Hype and reality of Modi government’s capital expenditure. Some of his inferences I am not sure add up, but broadly, true capex increase is not as much as touted.

Regarding the points about the govt adopting the Korean model and the taxation policy, I have quite different views about the wisdom of such policies. Rather than bold, I would call some of that misguided, if not foolhardy. But this is not the forum to discuss that and who it favours, so won’t go into it.

If, as you think, they are capable of continuing with such policies, then you are probably right in terms of what it means in terms of stock picking. I don’t think they will be able to, but will review my hypothesis. And, of course, we will know anyway as things play out.

6 Likes

Thank you for your valuable insights. Any view on genesys promoter selling a large block (almost 4% ) last week? Kinda surprising that promoters are selling with such large growth potential ahead

Promoter can sell for any reason hence it is not as definitive signal as buying is because when you buy you expect it to go up but when you sell it can be better opportunity to profit booking to personal deleveraging to enjoying the fruits of earlier hard work to anything else. If still it worries you then rather than taking indirect signal like promoter selling as negative you can take collective opinion of market by focusing on price.

But that seems to be holding up well despite such market.

7 Likes

Rocket labs at resistance now after strong run up. Have written a detailed thread here

2 Likes

Fundamentals

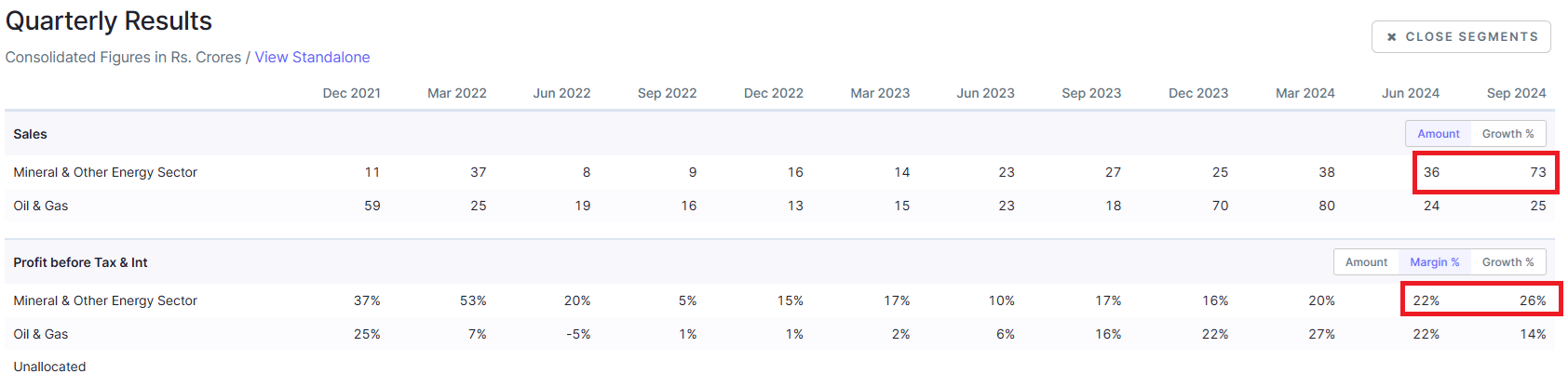

Asian Energy Services has found encouraging momentum in the Coal Handling business which has seen 100% QoQ growth with good set of 26% EBIT margins.

Government has mandated that all coal mines with at least 2mn MT of coal mining capacity must mechanize the Coal Handling Process in the next 5 years. https://coal.gov.in/sites/default/files/2024-08/PIB2043611.pdf

Coal India alone has more than 120 mines with more than 2mn MT capacity. Out of which currently 20-25 coal mines have been mechanized with the Coal Handling Plant (CHP) and 20 more are in commissioning phase. About 80 mines are still to be mechanized. This is about Rs. 10,000 crore opportunity which is going to come up in the next 5 years.

Opportunity size can increase to additional 100 coal mines and other minerals also bringing total size of possible opportunity to be north of Rs. 20,000cr.

Guidance of 450-500cr revenue for FY25.

First ever con-call done yesterday is worth listening.

Technicals

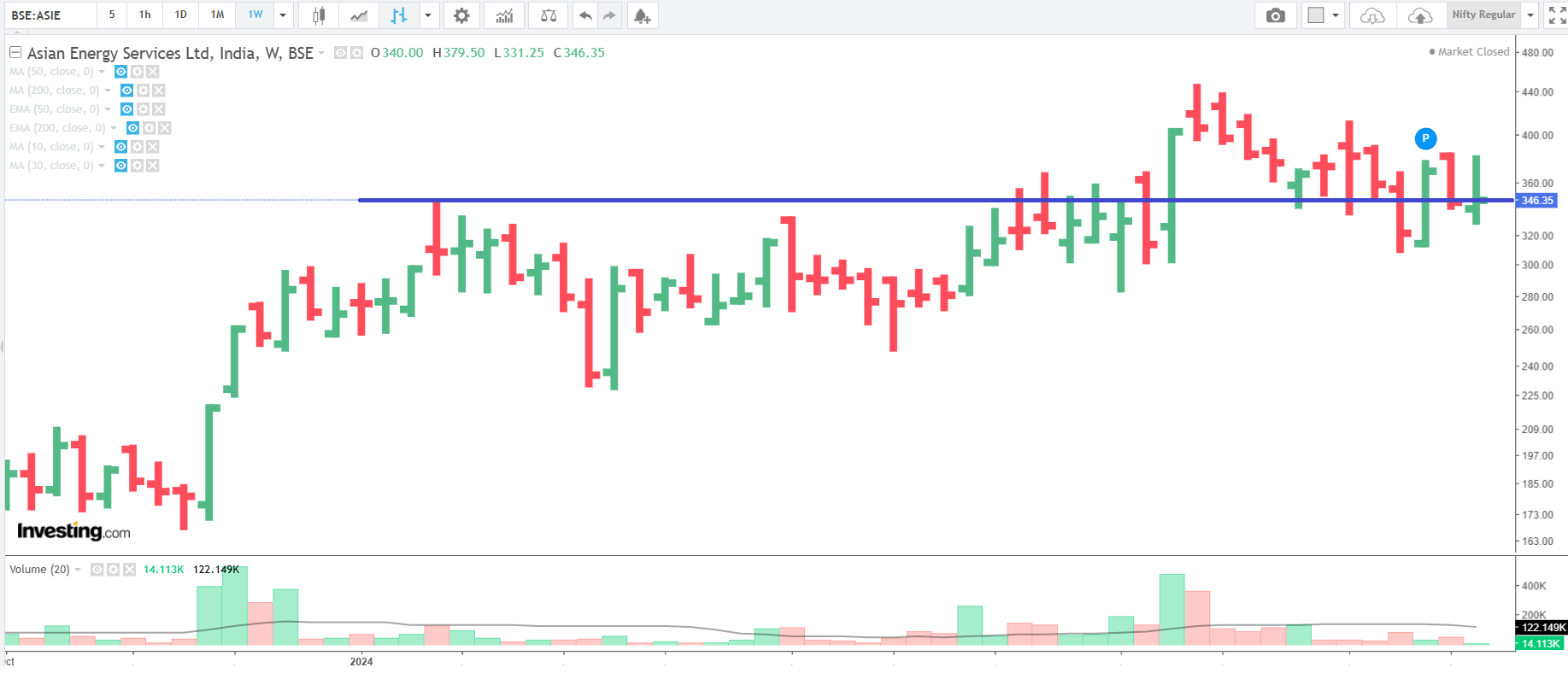

Monthly Chart - recent up move faced resistance at 2008 ATH of 446 levels.

Weekly Chart - stock tried to BO in August from January highs of 344 levels. Went till 444 and found resistance around 2008 ATH levels. It’s back to retesting BO level and possibly gives a good opportunity to accumulate.

Risks: company is blacklisted by ONGC and ONGC might contribute about 2-3% of FY25E revenue.

Disc: trading bet

15 Likes

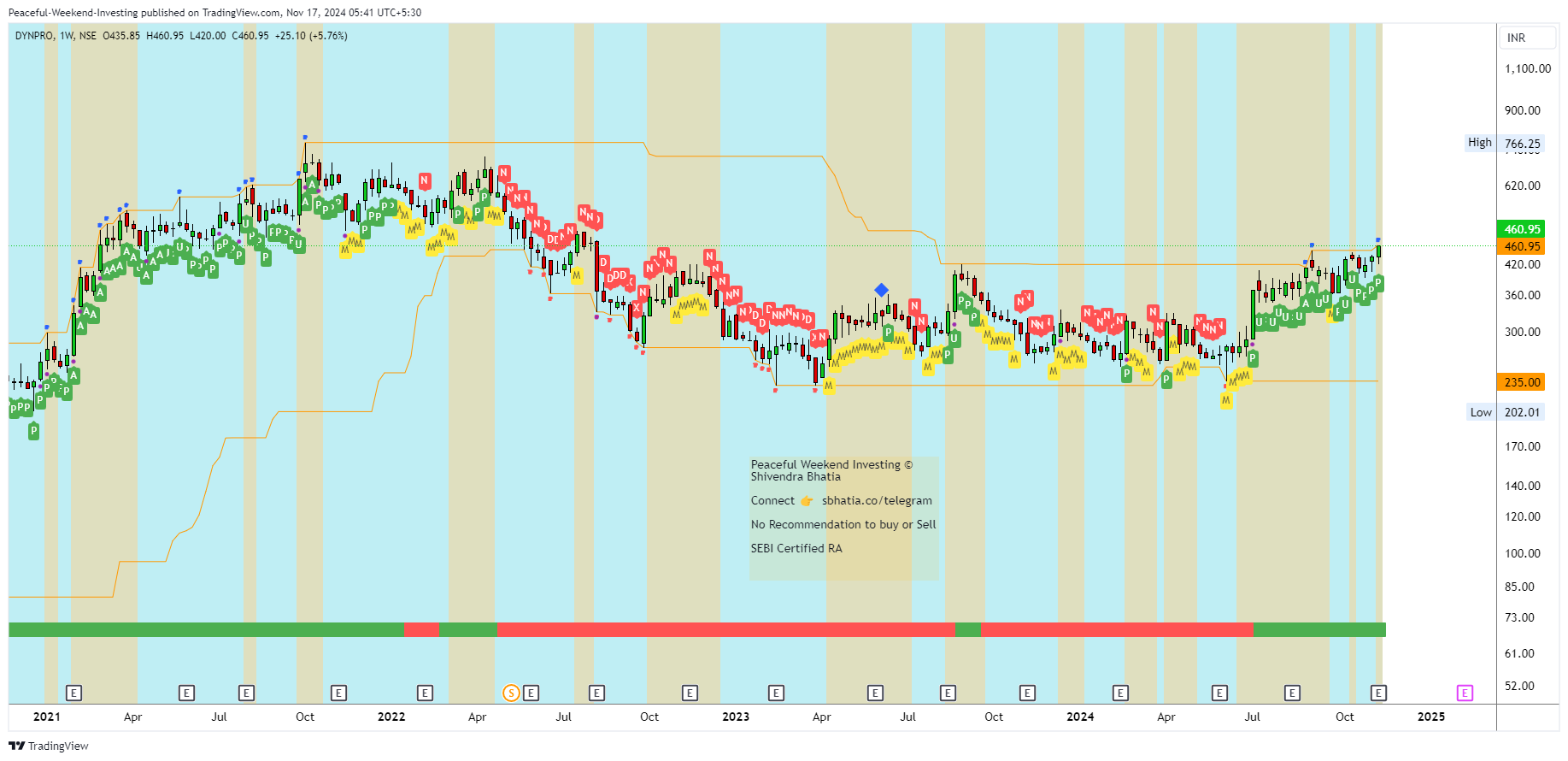

Fundamentals

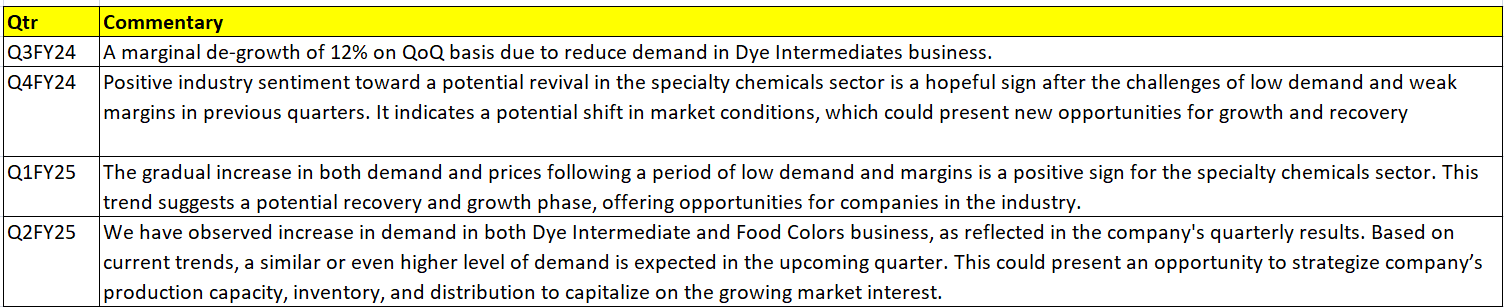

Dynemic Products seems to be coming out of the low business cycle phase. It reported encouraging Q2FY25 quarter numbers. EBITDA margins have stabilized on the lower end and company has reported highest quarterly sales of 98cr. Below is the trajectory of their commentary for last 4 quarters. Latest commentary hinting that worst is possibly behind for them (take it with a pinch of salt because every management gives a ray of hope every quarter - that’s their job).

Technicals

Stock has had very good support around 260 levels for last 2 odd years. It tested 260 support area almost 7 times. It was quick to bounce back after breaking down from 260 levels shaking out the weak hands.

Volatility compressed nicely after July till October before attempting BO from upper resistance at 420 levels. Nifty and Smallcaps have been under pressure since end of September but Dynemic has been showing relative strength and moving higher. Market was probably too smart to sniff out that worst is possibly behind them and that it was relatively much cheaper compared to many hot moving stocks in mid and small cap space.

Disc: no position yet but watching very closely

18 Likes

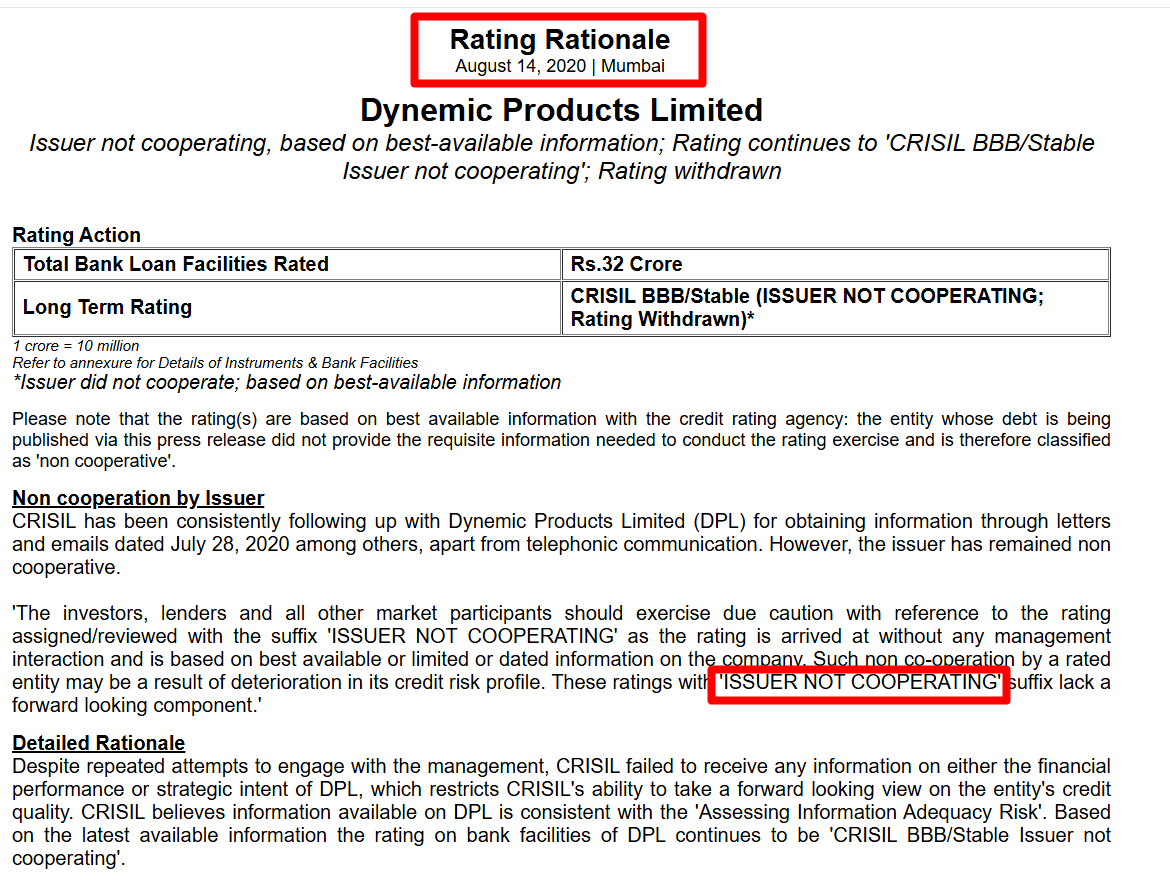

Price action is looking good no doubt , seems you following this company - what iwas 2020 where Company wasn’t coperating with rating agency - red flag

3 Likes

It is definitely not a red flag. In valuepickr you will come across many companies who wouldn’t have cooperated with rating agencies. A company which needs capital (desperately) will co-operate with rating agencies. Otherwise there’s no need to co-operate with them.

13 Likes

What is the Right to Win in Coal Handling ? Couldn’t find any evidence though this business is growing well.

1 Like

To be honest - its a new business (Coal Handling) and I myself have been trying to learn the intricacies of Coal Handling as a business and the competitive landscape.

Most of the times we don’t have all the information. If we have all the information then its too late and very well priced into the stock price.

Management confirmed on the con-call that CH is a new business for them which is about 2-3 years old. They have been refining and fine-tuning the processes to get better in this business. According to my first level thinking - they seem to be early entrants and at right place at right time.

Below mentioned dots gave me a feeling that something interesting is brewing with CH business of Asian Energy:

-

Size of opportunity seems to be very big. Ministry of coal has just recently announced on 9th Aug 2024 their plan to accelerate the development of Coal Evacuation Infra for achieving coal production target of Vision 2030 and beyond. All larger coal mines producing more than 2 million tons (MT) per annum will be required to implement mechanized coal handling facilities within the next five years. Size of opportunity is north of 10,000cr.

-

Recently raised capital of about Rs. 157cr by allotting preferential warrants. Well reputed investor has participated in this fund raise. Company would not raise funds if they don’t see a good potential to earn good return on the incremental capital.

-

First ever concall. Generally companies start to conduct con-calls only when they are confident of the future prospects of the business and are inclined towards creating shareholder value.

-

Numbers don’t lie. Latest quarterly earnings numbers confirm that CH business seems to having good tailwind with 100% QoQ growth - which means something is going right for CH business and the momentum has just started. Plus management has given FY25 guidance of 450-500cr which should be >50% YoY growth.

It’s always better to get just one foot in the door (starting position) instead of large scale position when one is dealing with incomplete information. Monitor the quarterly execution and one can average up with good business execution. If the CH thesis is to playout well, it might have some tailwinds for 2-3 years and shouldn’t fizzle out in a quarter or two. If the business execution falters, one should quietly book the loss and take it as a learning lesson and look for other opportunities.

disc: same as above

42 Likes

Result season is over. Can you please share your comments for educational purposes.

2 Likes

Aditya Birla Money breakout with high volumes, have explained my investment thesis here:

5 Likes

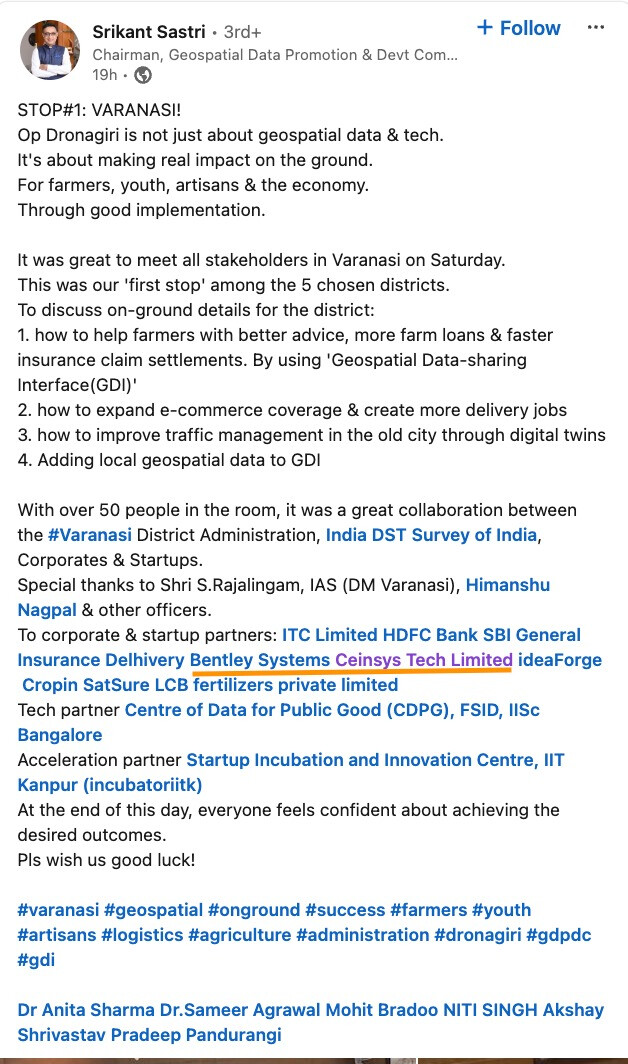

Apologies for being late here. I know results season got over long ago. The last time I wrote, Shaily, Genesys, Strides results had come and I had taken a position in Holmarc. Ceinsys and Wockhardt had not come out with results.

I have been writing in individual company threads as I felt the deep dives belonged there, rather than here. Ceinsys result is discussed here. Since then the concall as well happened and most of these assumptions were confirmed by the management. I made some mistakes in my split calculation though my general assumption on how to look at the numbers were right. The wainganga-nalganga river linking and IDDP for MMRDA summing up to 500 Cr must still be in the works as they are not yet disclosed. Orderbook should be strong around 1700 Cr once these are confirmed.

I was also quite surprised by the way market reacted post Mumbai elections. It clearly was a large hurdle going by market reaction. Now that its out of the way, we can focus on the fundamentals. The company announced a 330 Cr order from JJM MH extending last year’s order of 248 Cr. It looks like there might be lot more to come here just in MH. Going by the TPI (third-party inspection) work they are doing for JJM in UP in Lucknow, Chitrakoot and Devi Patan, I wouldn’t be surprised if they land some IoT work there also in JJM.

Recently noticed that Ceinsys is a corp partner for the recently launched Operation Dronagiri.

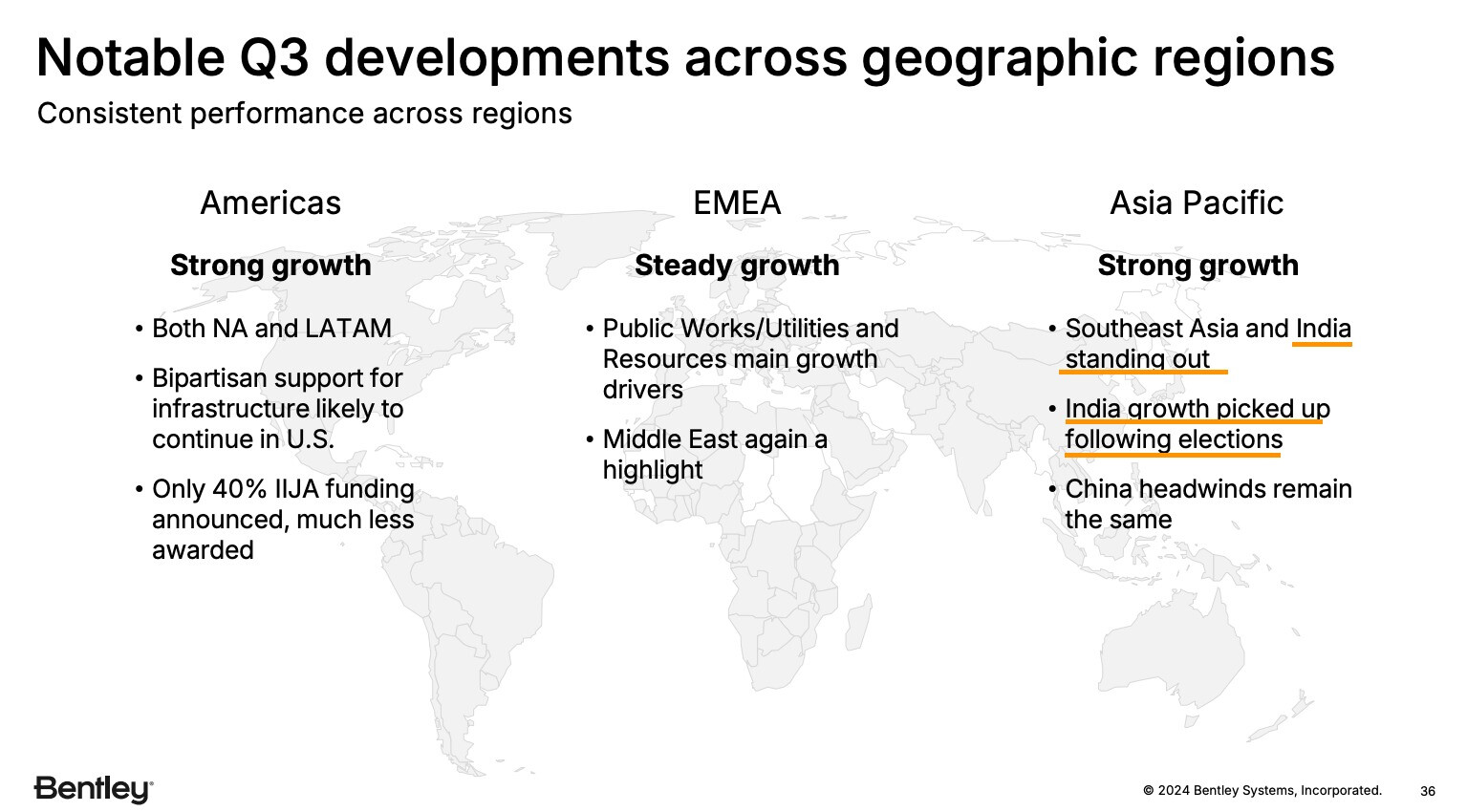

Also noticed how much importance Bentley systems who Ceinsys partners with for geospatial software and licenses is giving India

Other than this, on Wockhardt, I have summarised my thoughts on holding it for a year in the company thread. Everything is going as it should and as per the recent dispatch, there’s another case in US where WCK 5222 has been used on compassionate basis on a cancer patient to counter NDM-producing pseudomonas and Kleb with IMP, OXA-48 resistance mechanisms and the patient recovered subsequently to undergo liver transplant and resume chemo. Also interesting is the fact that the failed therapy included Cefiderocol which is not known to work well in NDM producing strains. This reasserts the superiority of WCK 5222 over CFD that we were seeing in studies (2nd post in the Wockhardt thread) in the real world as well. Presence of these strains in US, increases potential value of WCK 5222 - to put it in perspective, Cefiderocol is $16k per treatment if I remember right.

Made some more headway in Holmarc as well as the causes for tailwind is now apparent. Have couple more posts in the thread as well discussing results and capabilities.

Most of the stocks in the pf have done phenomenally well, backed by strong fundamentals.

Market has refused to listen to bearish views and views claiming that largecaps are cheap. Small/Microcaps have held up quite well this time as expected since fundamentally they are the ones benefitting the most from govt. policies. Post elections, there’s a pickup in tendering and order flow across sectors benefitting from govt. capex from geospatial, defence, railways, infra, space etc. This is going to be the age where the wheels come off globalisation and there’s more local production and that means getting rid of efficiency of global supply chains to put up local capex and put tariffs to protect it. Holding on to consumption stocks and waiting for tax cuts to spur consumption which used to work in the past may not be the govt.'s priority.

Disc: Invested in mentioned names.

P.S. I might stick to writing in company threads since my style has changed so much since I started writing here few years back. Will also attempt to start own thread to write about things that interest me, and about value in general, not just financially

105 Likes

@phreakv6 , I think you missed out on writing on Strides ??

5 Likes

Axiscades, Monthly - After a runup in Jan '24 which was undone in Feb '24, it spent the rest of the year wallowing between 500-650. So this upper end of the range (650) is strong resistance. A breakout above this level should help hit ATH

Fundamentally the company is into Defence, Aerospace, ER&D (Auto), Heavy Engineering, Semi-conductor and Energy verticals. Auto ER&D is currently a drag due to Volkswagen not doing well as we all know. Heavy Engineering (partnership with Caterpillar) is a low margin business so both ER&D and Heavy Engineering are somewhat of a drag currently on overall performance of the company.

What excites me is the Defence vertical under Mistral and ACAT. This is where the company is guiding for high growth and restructuring and synergies. The semi-conductor business as well under the C2P (Chip-to-product) approach can show good growth going forward.

The company held a call to discuss restructuriung the defence vertical and also discuss prospects of defence, aerospace and semi-con. I think the first 12 pages of this transcript are worth several re-reads to understand what is being planned under the mentorship of Dr.SRN. There’s a lot of management shake-up as well at the top and there’s lot of intension and hunger to do well (Very similar to what Ceinsys went through last 2 years).

Key highlights

-

The company has a large foothold in anti-drone warfare having supplied 100+ of these systems. There’s value-add to these systems to make them portable, vehicle-mounted etc. This could be a big driver for the company going forward. Additionally, spoofers, directed energy weapons, RF detectors and 3D radars are also being planned which can be a huge value-add for the company.

-

They also have a good presence in defence logistics (30-80 kg payloads using drones)

-

Capability in drone controller which is used in an American company already (plans to get it NATO certified). It can sell this across the world to various OEMs

-

Preferred offset partner for weapons package for new Marine Rafale. OEMs are higher margin so company is focusing on weapon package, submarine and avionics to sell to OEMs. Already has foothold in 1 company and is trying to engage two more for these.

-

Missile capability in new missile program post Russia and Israel war. They are also participating in upgradation of existing missile systems.

-

Focus on products - Direction finder, direct RF (eliminates few stages in radar signal processing making equipment light-weight), X band radar used in submarine and marine systems

-

Expand foothold with Airbus programs running in India - like MRTT

-

Space - in launch vehicles in partnership with AgniKul (NGLV and Bharatiya Space Station)

-

Semi-conductor C2P - Chip-to-product strategy across 6 verticals - defence and aerospace (drone controllers), automotive (autonomous driving), healthcare (protein synthesizer), consumer (product to teach age 5+ kids using AI), industrial and hyperscalers

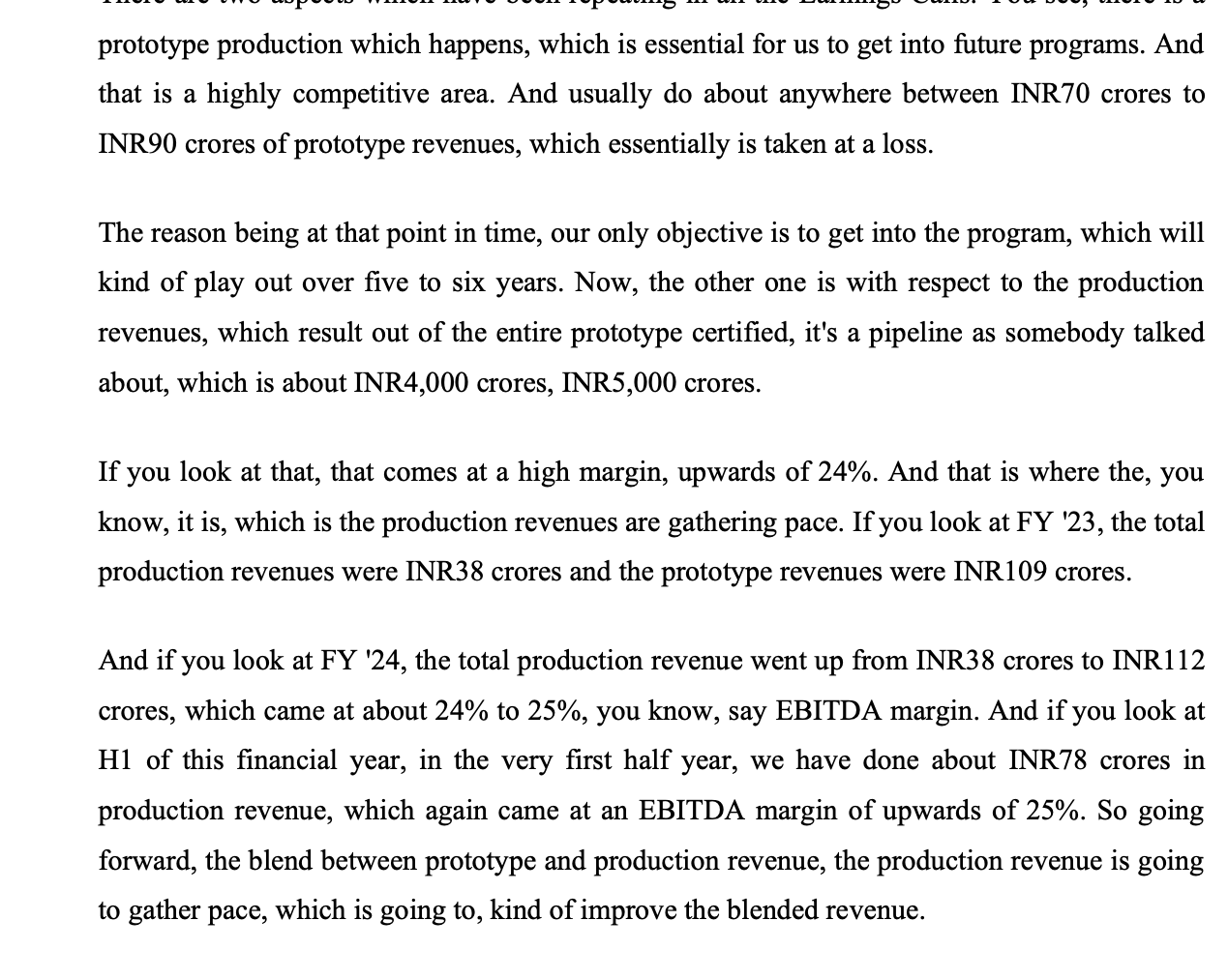

The company has 5000 Cr of approved design wins which can go into production. Bulk of these (~60%) is for LCA Tejas (130) and Sukhoi (250) aircraft programs which are currently delayed. While these play out perhaps in FY27, there’s still enough in the pipeline for Anti-drone systems, new missile program, Akash Mark-II and QRSAM meanwhile which will contribute in the near-term.

There’s definitely lot of technical capability across the company and it seems to be keyed into the direction MoD is going in with AI and IOBT (Internet of Battle Things), swarm drones etc.

Margins will trend up because the contribution from production revenues will trend up here on. The prototypes are barely breakeven or loss-making as its very competetive but production margins can be 25%

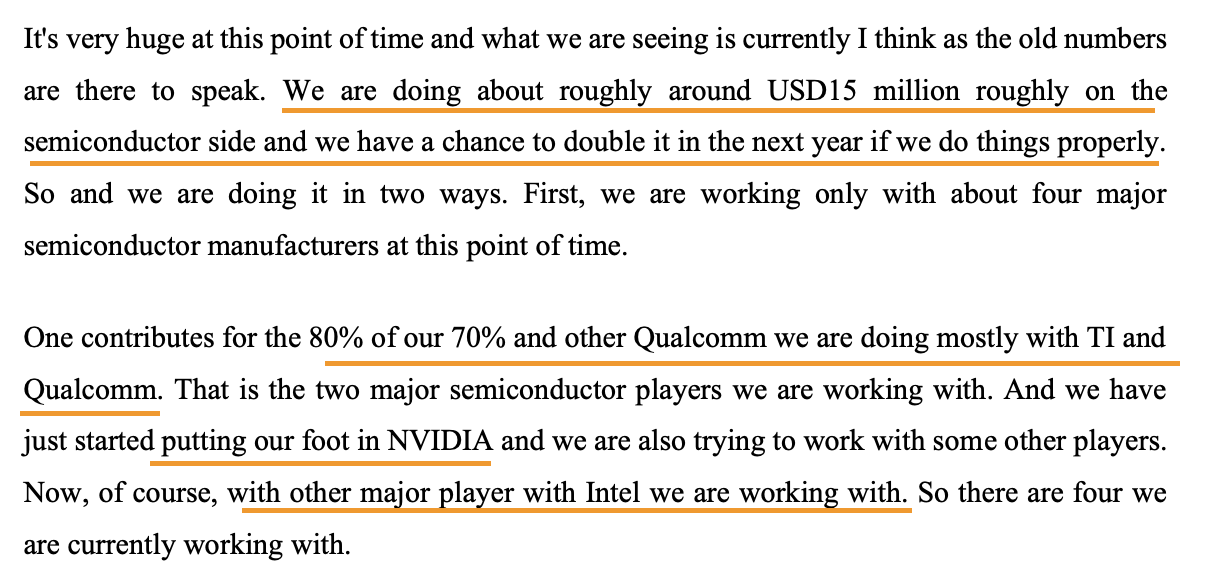

On the semi-con business - they currently work with TI, Qualcomm, Nvidia and Intel (this business is based out of US currently but some part of work will be done in India going forward)

Interest cost in FY '24 was 58 Cr. This will reduce to 20-30 Cr.

So overall for this level of capability, 2500 Cr market cap seems cheap though P/E basis it looks expensive. Profitability should continue to trend up from here.

Risks

- Auto ER&D will continue to be a drag this year

- Execution risk with so much management overhaul

- Capex and WC requirement might be high for fulfilling all these aspirations

- Politically connected promoter (Rajeev Chandrashekar’s PE firm owns bulk of the company)

Disc: Have positions between 620-650

Credits to @rupeshtatiya thread on Axiscades and to @nirvana_laha and @Sanjay_Kumar_E for helping me in understanding the story better

84 Likes

CARTRADE

Cartrade recently breached their all time high of c.1500 recorded during listing in Aug 21 and is looking quite strong . The recent triggers being the following .

-

Overall buoyancy in auto sales (Both Car and bike) : As per the management commentary the current scenario is a goldilocks situation (Not too hot or cold) as there is sufficient demand but there is also ample supply unlike covid times where there was supply crunch leading to OEMs not spending on marketing.

-

Growth in OLX revenue after integration : Both on Auto and Non auto segment . The co. was initially focused on auto part of OLX business as its their forte , management is planning to focus on the non auto side as well. OLX already is a 25% margin business with strong network effects and moat. Peers like Craiglist in the US boasts of margins upwards of 70% if I am not wrong. This is the business I am most bullish about. If the management can get their act right on this one they can rap rich rewards.

-

Bounce back of the Remarketing business : Management thinks that SAMIL has kind of hit the bottom and can only move upwards from here.

Pasting below a report that I prepared about Car trade in September 2024. The basic premise remains the same while the prices have run up a bit.

Cartrade Tech Ltd : Why does this new age platform demand a fresh look ?

Legendary Investor Mr. Ramesh Damani told an interesting anecdote about his purchase of United Spirits (Then Mc Dowells) in early 2000s.

“No doubt there were issues and that’s the reason these stocks gave you the opportunity. McDowells was 50% of the Indian spirits market and it was available for 160 Cr. People will swim across the sea with alligators and whales in it to buy this company and the stock market is giving it to you for Rs 160 Cr. At that price everything is captured -there couldn’t be a downside but only an upside. With 100 crore you could have bought 10-20% in Indian liquor industry or 2 flats in NCPA in Mumbai – that was the value proposition. You could have seen what Anheuser- Busch in US or San Miguel in Philippines is valued”.

Source : Master Class with Super Investors; Vishal Mittal/Saurabh Barsar

I believe Cartrade tech now presents with such a unique opportunity.

About the Business

Cartrade tech is a platform company predominantly in the automotive space (Cars, Bikes, Used and New). They have 3 broad verticals.

Consumer Group : Houses Carwale, bikewale and Car trade.com platforms .

Consumer group offerings:

Consumer group generates revenues from Auto OEMs, Auto Dealers, Used Car dealers , Finance companies , Auto Ancillary companies who generate traffic and inturn sales from Cartrade Platforms.

Google Trends : Relative Search Interest

Despite deep pockets invested competitors like Cars 24, Car Dekho , Spinny and Droom entering into the space , Carwale still maintains the lead in google trends.

Remarketing Group : Cartrade exchange, Shriram Automall and Adroit Auto

The remarketing business ( Shriram Automall, Cartrade exchange) gives an opportunity for finance companies , hire purchase companies and banks to display and auction their repossessed vehicles . This business has a phygital (Physical+digital) presence. This business has not been firing offlate due to reduced number of repossessions due to lower delinquencies.

Management is expecting that this business has bottomed out and should improve from here on.

Classifieds Business : OLX Business

Cartrade tech acquired the India business of OLX (OLX classifieds platform and OLX C2B business) from Sobek Auto Pvt Ltd for Rs. 535 Cr. OLX is owned by Naspers across the world .(Cartrade subsequently discontinued C2B business of OLX due to unfavourable unit economics).

OLX is the no:1 classifieds portal in India with 10 Cr app down loads and c. 4 cr unique visitors. Think about it : when you and I want to buy or sell used stuff which is our first port of call?

OLX has massive network effects:

That’s the reason why the whatsapp, facebook, VISA, Master cards of the world survive and thrive.

And to build sufficient network effects all platform companies throw money with little concern for profits.

OLX acquisition is the reason for giving the story about Ramesh Damani and Mc Dowells. If you think about it a profitable company with 24% margins with 10 Cr+ app installs and 4 cr unique visitors per month and is the first port of call for the country in classifieds is available for 3800 Cr (4400 Cr mkt cap - 700 Cr cash) .

45 % of the OLX business is used cars and rest 55% is categories like Real estate, Mobiles, Furniture, electronics, jobs etc.

Excerpts from the Concall :

OLX has 2 types of revenue streams :

- Consumer Paid Listing

- Dealer Paid Listing.

OLX is a profitable entity with 24% adjusted EBITDA margins.

(Craigslist, one of the pioneers in classifieds business is operating at a revenue of C.700 Mn $ with 80% profit margins !!!)

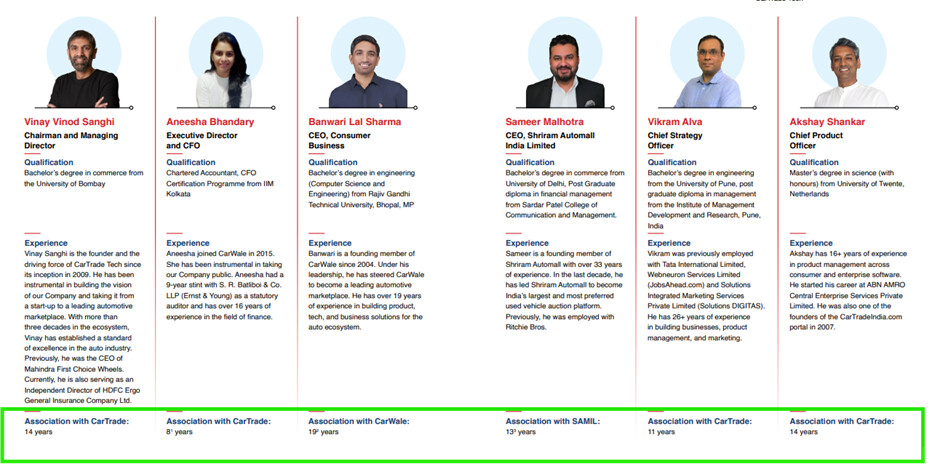

About the Management :

As evident from the above the entire management is with Cartrade for several years. Infact Cartrade in the current form was created by acquiring several companies like Carwale/Bike Wale , Shriram AutoMall , Adroit Auto , OLX etc. It’s a testimony to the vote of confidence in the Chairman Mr. Vinay Sanghi that all these entrepreneurs decided to stick on with Cartrade (Any patterns that you recognize there? ![]() )

)

The jockey Vinay Sanghi hails from a family which is traditionally into automobile space. They used to import cars for the Maharajas in pre independence era. Then they set up dealership business.

- Vinay Sanghi joined family dealership business post his studies.

- Then he wanted to do something on his own and incubated a company called Automart in 1999, which eventually became Mahindra First Choice .

- After associating the with Mahindra and HDFC bank in Mahindra First choice for 10 yrs plus running this business, Vinay quit

- In 2009 he started B2B and C2B auction platform and subsequently started Cartrade exchange and Cartrade.com, the first auto exchange platform in India.

- Acquired Carwale and Bike wale in 2016

- Acquired Shriram Automall (SAMIL) in 2018

- Acquired India business of Olx in 2023

Financials

The revenues have grown substantially post OLX acquisition so has the Operating margins. We can assume an annual run rate of c. Rs 100 cr.

If you look at segment wise results both consumer and Classifieds business are high margin businesses with Remarketing a bit of a drag .

Valuation

Current Price : Rs 940 (As on 5th Sep 2024)

Market Cap : Rs 4450 Cr

PE : 56.4

Cash in hand : c. 700 Cr.

Avg quarterly run rate PAT (Forward) : Rs 25 Cr.

Annualized PAT = 100 Cr

Forward PE = 37.5

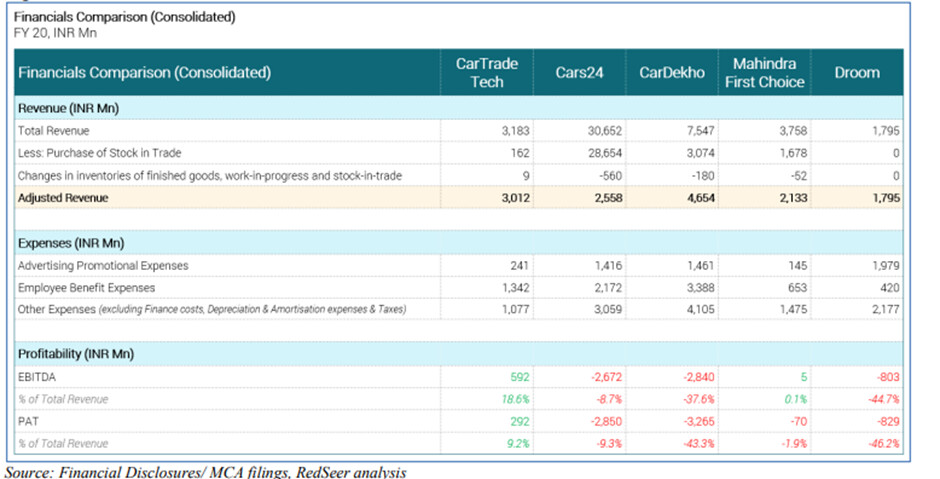

Financials Comparison with Unlisted Competitors (FY 20)

- Cartrade is the only profitable company among its peers (Unlisted).

- Cars 24 have a gross revenue recognition policy and hence their revenues look optically high.

- Cars 24 is valued in the private market upwards of 3 bn $ (c. 25k Cr Rs) followed by Spinny, Car Dekho and Droom !!!

Relative financials with other New Age Listed Platform Companies

| Relative Valuation | Cartrade Tech Ltd | Info Edge (India) Ltd | PB Fintech Ltd | Zomato Ltd |

|---|---|---|---|---|

| Market Cap | 4,453 | 96,767 | 78,561 | 2,25,098 |

| Current Price | 941 | 7,479 | 1,722 | 255 |

| Stock P/E | 56.4 | 151 | 767 | 374 |

| Book Value | 441 | 2,339 | 130 | 23.1 |

| Dividend Yield | 0 | 0.29 | 0 | 0 |

| ROCE | 4.79 | 3.65 | 1.75 | 1.14 |

| ROE | 2.86 | 2.44 | 1.14 | 1.12 |

| Face Value | 10 | 10 | 2 | 1 |

| Debt to equity | 0.05 | 0.01 | 0.04 | 0.04 |

| Interest Coverage | 12.1 | 46.5 | 5.46 | 7.9 |

| Dividend yield | 0 | 0.29 | 0 | 0 |

| Sales growth | 48.5 | 6.71 | 39.2 | 72 |

| Profit growth | 77.5 | 55.3 | 135 | 177 |

| Enterprise Value to EBIT | 38.5 | 85.1 | 539 | 361 |

| Free cash flow 3years | 112 | 1,574 | -2,016 | -1,251 |

| Return on assets | 3.39 | 2.09 | 0.99 | 0.99 |

| Sales growth 3Years | 25.2 | 31 | 57.1 | 82.5 |

| Profit growth 3Years | -14 | 60.6 | 33.2 | 34 |

| Profit growth 5Years | 48 | 49.9 | 16.8 | 16 |

| Sales | 545 | 2,587 | 3,783 | 13,904 |

| OPM | 17.5 | 28.1 | -3.98 | 1.92 |

| YOY Quarterly sales growth | 64 | 8.11 | 51.8 | 74.1 |

| YOY Quarterly profit growth | 68.7 | 56.8 | 321 | 12,550 |

| Price to Free Cash Flow | 120 | 184 | -117 | -540 |

Conclusion (To cut the long story Short ):

- The markets are generally efficient and is a continuous discounting machine. Yet this New age platform business is valued presently valued at 4400 Cr market cap (with c. 700 Cr cash in books).

- This same company was listed at a price of c. Rs 1600 and c. 7600 Cr market cap when they were barely profitable and OLX was not part of the deal.

- I believe a confluence of factors like sweet ESOP deals, general fatigue towards new age companies over the last few years, market focus towards other sectors like defense , PSU , Reale estate , electrification and heavy industries shifted the focus from this company.

- This is a platform company which is cornering the used car space (with a foot in the door in new car segment) with excellent and prudent capital allocation available at descent valuations.

- OLX is a feather in the cap with exceptional network effects. It is profitable with excellent Operating margins and huge runway ahead. What remains to be seen how Mr. Vinay and co is able to capitalize the Non-auto business too.

Source :

Company Presentation, Concalls, DRHP

Value Pickr Forum: CarTrade Tech - A Multi-Channel Auto Platform - #39 by GARP_niveshak

Master Class from Super Investors: Vishal Mittal and Saurabh Barsar

Other Web resources

Disc: Invested around Rs 950 . Looking to add more. Current allocation is small.

Not qualified to advice. Please DYDD.

28 Likes