Almost a month has passed since what appeared to be “Day 1 of bear markets” which in hindsight has turned to be 17 sessions of uninterrupted, and as yet unbroken rampaging green streak at pf level. I will not delude myself to think this was the only possible outcome although it was a likelier outcome I felt at that time (can’t afford to not be optimistic). The panic was brief and passing when the pf drawdown crossed -10% and hit -11% briefly. Did not expect the swiftness and ferocity of bounceback though which has led to biggest gains in any month for me, which I doubt will be matched in a long time. In terms of emotional capital, June 4th has given more than the financial capital gained in the month perhaps.

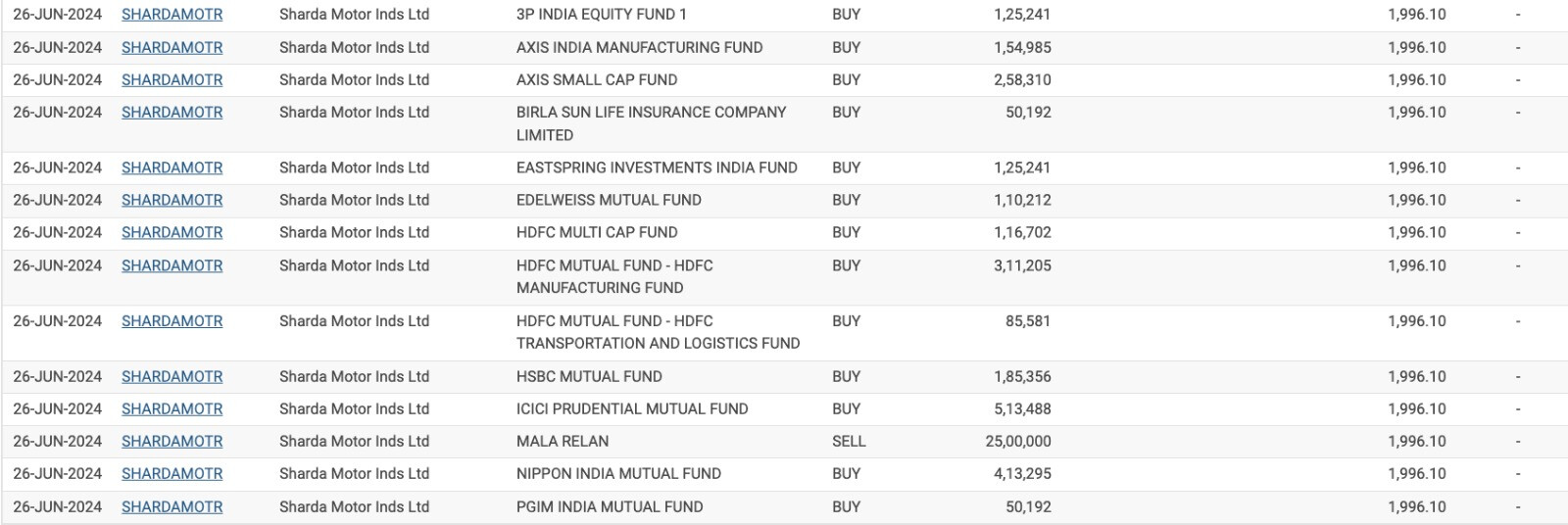

Sharda Motorsm Weekly - Long tail on week 1, followed by 3 weeks of gains. What’s also special is the breakout from that upwards sloping trendline which was dictating rate of gains previously. This breakout should set in motion a new trendline yet to be established.

Parabolic moves like this generally lead to more gains. The chart reminds me of what VBL went through in June '22 when I took position. The buyback at 1800 is completed which has taken the lid off the prices. There’s also lot of institutions which have got into Sharda this month, taking their ownership from 0% to ~10%.

Despite all this, and doubling since initial breakout, it continues to remain very cheap.

Wockhardt, Monthly - Some good updates from the AGM and the dispatches. Nafithro could do 100 Cr sales in FY26. Emrok could double the sales, WCK 5222 has been used to treat a cancer patient with CRPA (NDM-MBL producing) in the US successfully which is a big deal as FDA has indirectly approved the drug in its “Extended Access” program which is like DCGI’s compassionate use. It also tells us that NDM-MBL producing bugs which were specific to developing countries are now present in Developed countries as well (WCK 5222 is the only drug capable of treating NDM-MBL producing Pseudomonas Aeruginosa based on papers I have read). CLSI has awarded an investigational breakpoint of 64 mg/L. @Sanjay_Kumar_E has dissected it beautifully in this post.

The short answer is higher breakpoint increases market size and applicability. Some of the papers for eg. thought acineto was resistant to WCK 5222 based on their notion of Cefepime’s breakpoint. Now CLSI has agreed that the way WCK 5222 works is different and thus awarded the higher breakpoint which makes the drug usable in even Acineto that few papers classified WCK 5222 as resistant. It also makes it a better drug against existing ones as its MIC is several dilutions away than competetion.

Resistance development also will take time against WCK 5222 - so simple interpritation would suggest a bigger market size for longer. The CLSI verdict also potentially brings the “best-in-class” and 'first-in-class" that blockbuster molecules that do things differently than the rest get. Current drugs are Beta-lactamase Inhibitors (BLI) while WCK 5222 also enhances the function of Cefepime by bringing its T% > MIC down and thus forges a new category called BLE (Beta-lactamase Enhancer) which could again potentially increase value of the drug.

Shaily, Weekly - Another breakout from an upwards trendline, similar to VBL in Jun '22 I mentioned above in Sharda section. Fundamentally nothing more to discuss than what’s done in earlier posts. This too could get a move on.

Ceinsys, Weekly - Closed above 20 WMA and has set itself up for resumption in direction of uptrend from brief correction. Fundamentally have discussed this in depth in multiple posts in this thread. There was one more order extension disclosed which could be ~50 Cr in value. Can pick up steam on a weekly close above 600 levels which should happen before Q1 numbers comes out. I presume Q1 should be a good quarter going by the deferrement of large order from Q4.

Genesys, Weekly - On the weekly chart, it has reversed its downtrend and closed above 20 WMA. The monthly chart shows the potential of a breakout above 650-700 levels. The company has inked a partnership with NNG Auto and Mobility Solutions which will bring AI powered ADAS navigation to vehicles in India (mostly high-end luxury cars). This is probably the first customer for the new HD Maps made for ADAS product.

Garware, Weekly - Has made a strong close above those pesky 2200 levels which was seeing lot of supply. Should help in continuation of trend.

Taal, Monthly - A close above 3000 would have been very positive here but it retraced back some of the gains. I still think it could surprise on the upside pre/post AGM as more clarity emerges on growth plans. May remain cheap until then.

Disc: Invested. No recent transactions in any of these