Strides Pharma is a Bangalore based formulation company, established in 1990, that operates largely into regulated markets like - US, UK, Europe, Australia. The company has had ups and downs spanning 2-3 years each over last 10 years. The promoters have not helped the cause with various M&A and raising of equity multiple times. The result is that several peer companies have gone on to become much larger organizations and also in market cap while Strides is still left behind.

Now Arun Kumar, 62 years old, seems to be making some changes which look like sort of the last stand and hoping to create wealth and secure his legacy. Some of the changes are that he is making is -

- Bringing all promoter level entities into public company (Strides - GLP-1 + Bio CDMO, SteriScience - Injectables).

- OneSource is designed in such a way that operating cash flows from Soft Gel Capsules + SteriScience can support funding for long gestation Bio CDMO business. i.e. no fundraising on adverse terms hopefully.

- Some glimpses of focusing on gross margins and cost efficiencies at Strides parent level - so the business creates value from operational strength as against some sort of financial engineering, M&A etc.

All of above changes are my observations and these things are work in progress. We need to track progress of above items quarter by quarter. But if Strides can deliver on above things, can it create significant wealth for public shareholders?

VALUATION

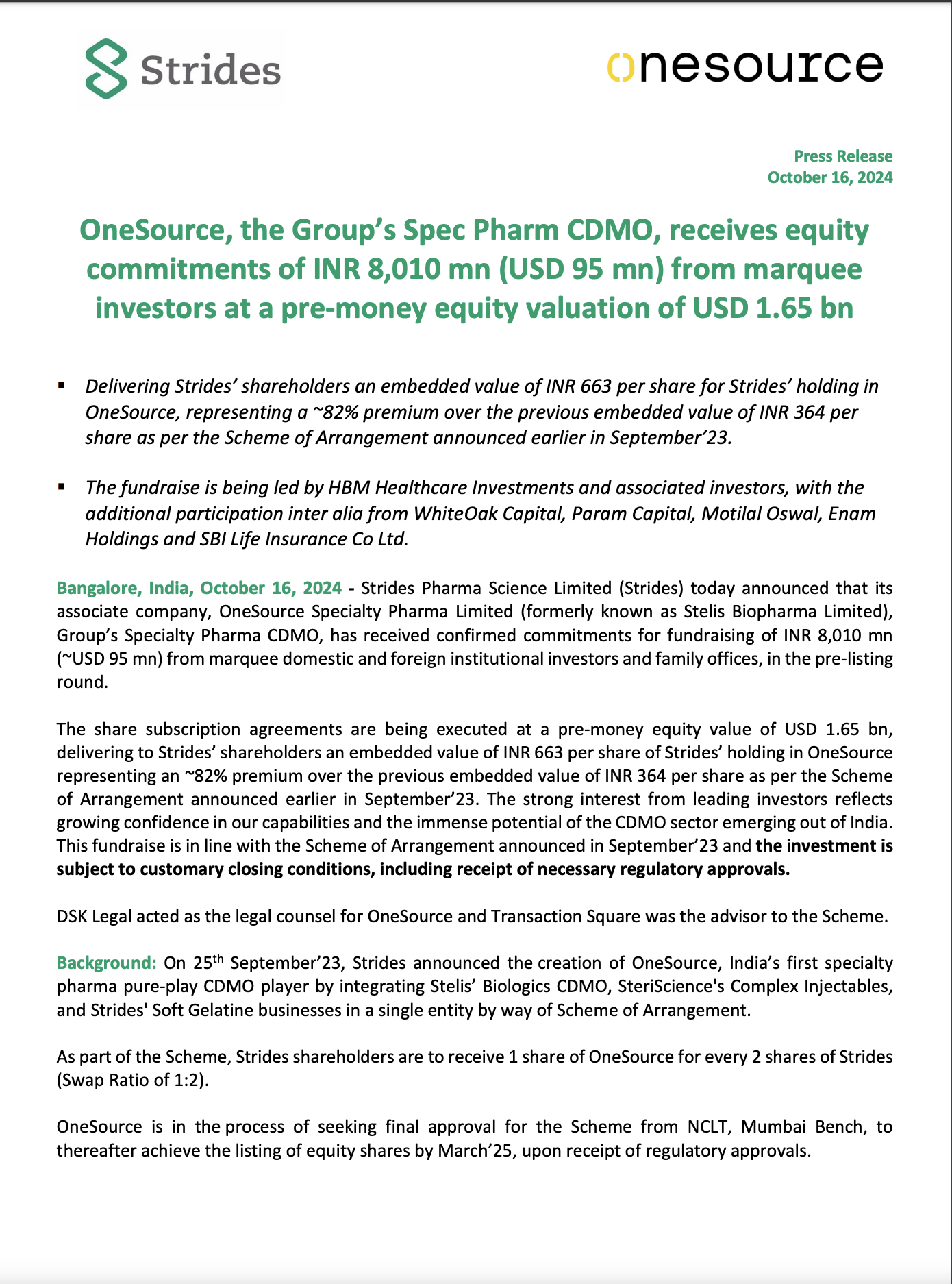

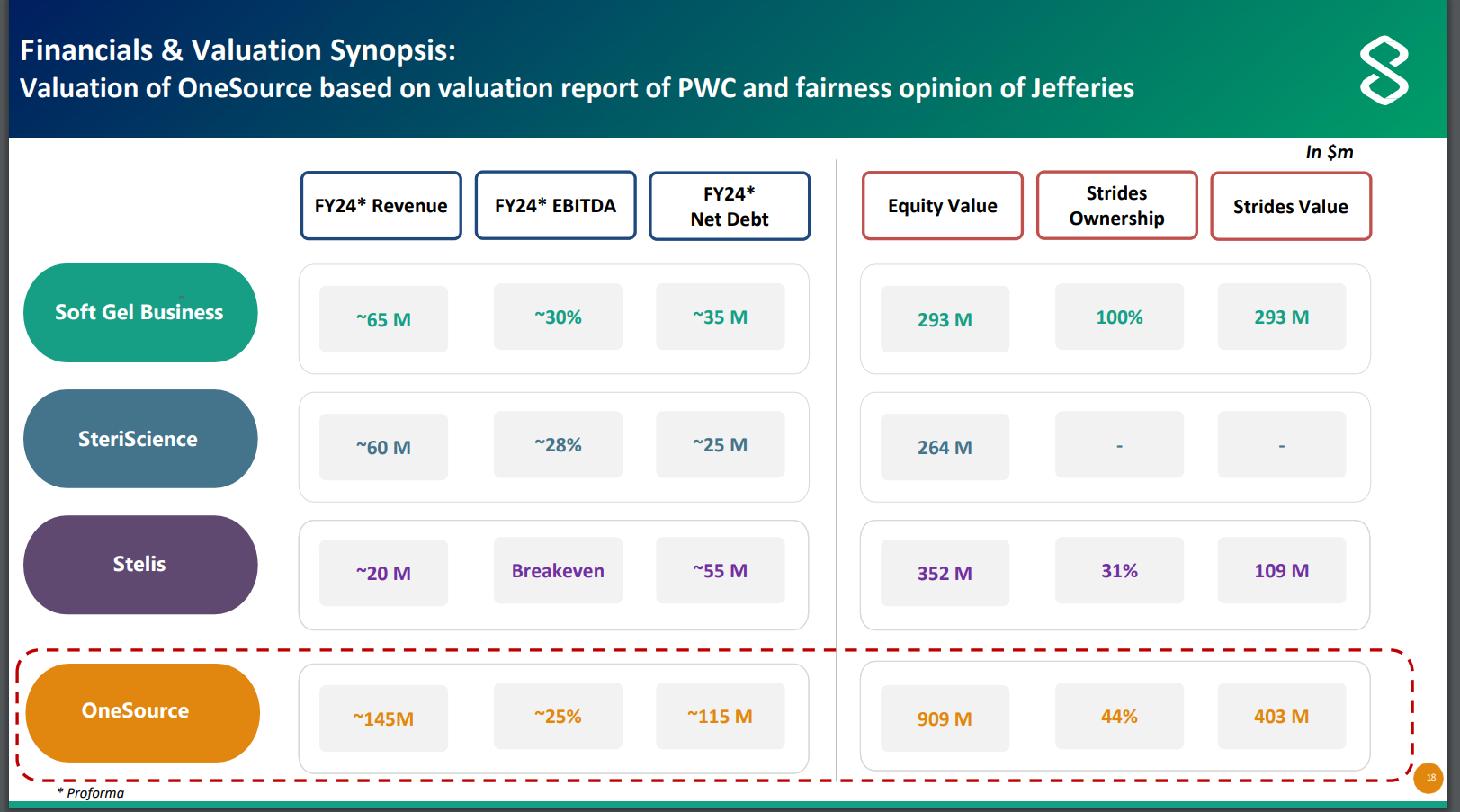

First things first, let us talk about OneSource and the expectation of management of where OneSource should be valued -

FY24 Projections

FY25 Projections

OneSource will have three business segments - Soft Gel Business, SteriScience and Stelis. Each of these businesses are supposed to have margins in excess of 20% and some of them can even have margins exceeding 30%.

For FY24, OneSource is supposed to have revenue of 145mn$ and EBITDA of around 36mn$ (i.e. 1200cr revenue and 300cr EBITDA roughly).

These numbers can significantly go up for FY25, management has given guidance of 190mn$ in revenue and 30% margins i.e. 1500cr revenue and 450cr EBITDA.

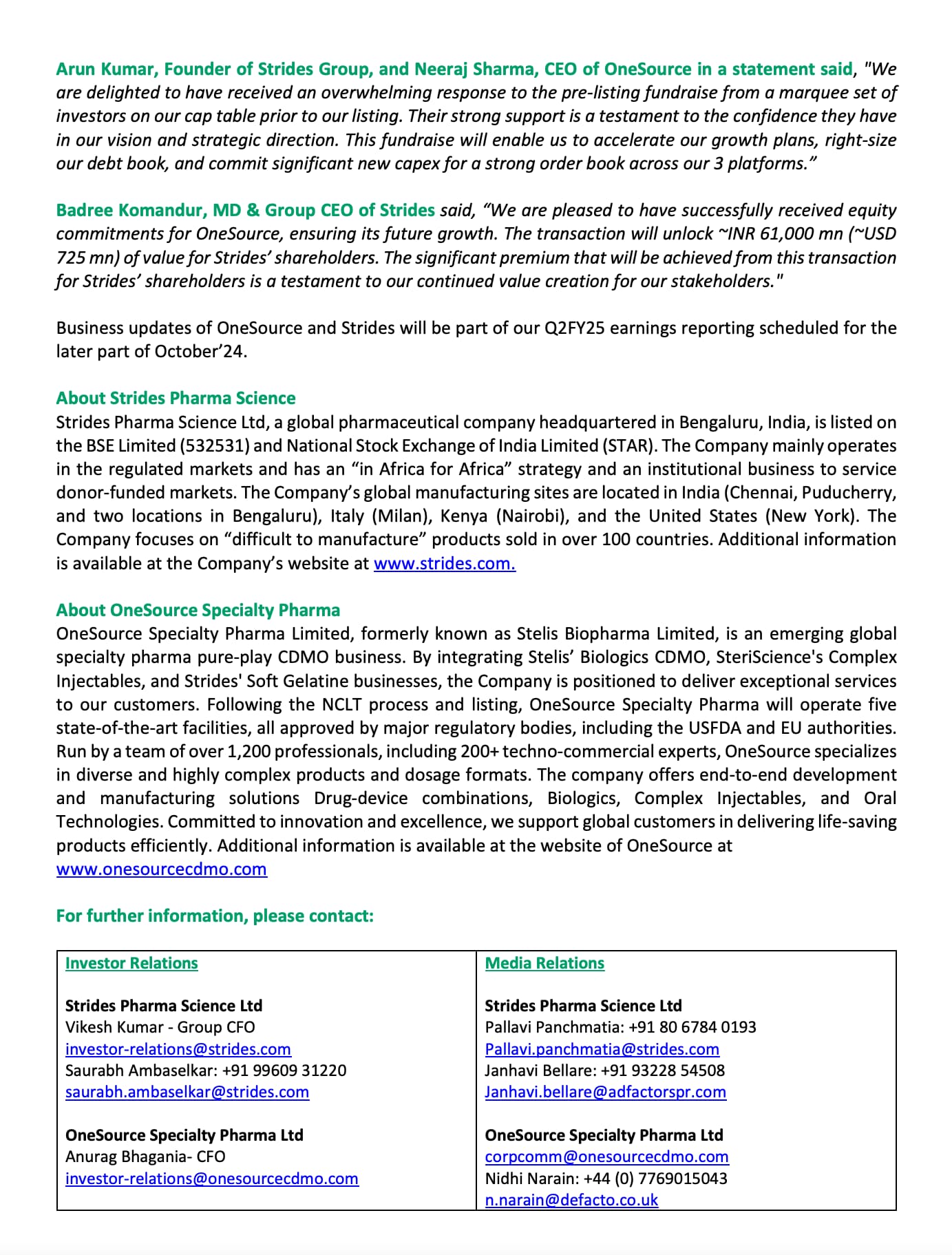

Management expects that this business will list at market cap of around 909mn$ and Strides owners will have equity value of 403mn$ i.e. EV value of 909mn$ + 50mn$ = 959mn$, or roughly around 8000cr. With 450cr EBITDA possible in FY25, that is EV/EBITDA of 17.

On per share basis, Strides will get value of 364 in OneSource.

Whether OneSource will list at 900mn$ or not, I do not know. But when I look at margin profile and business quality and underlying segments - things do seem favorable.

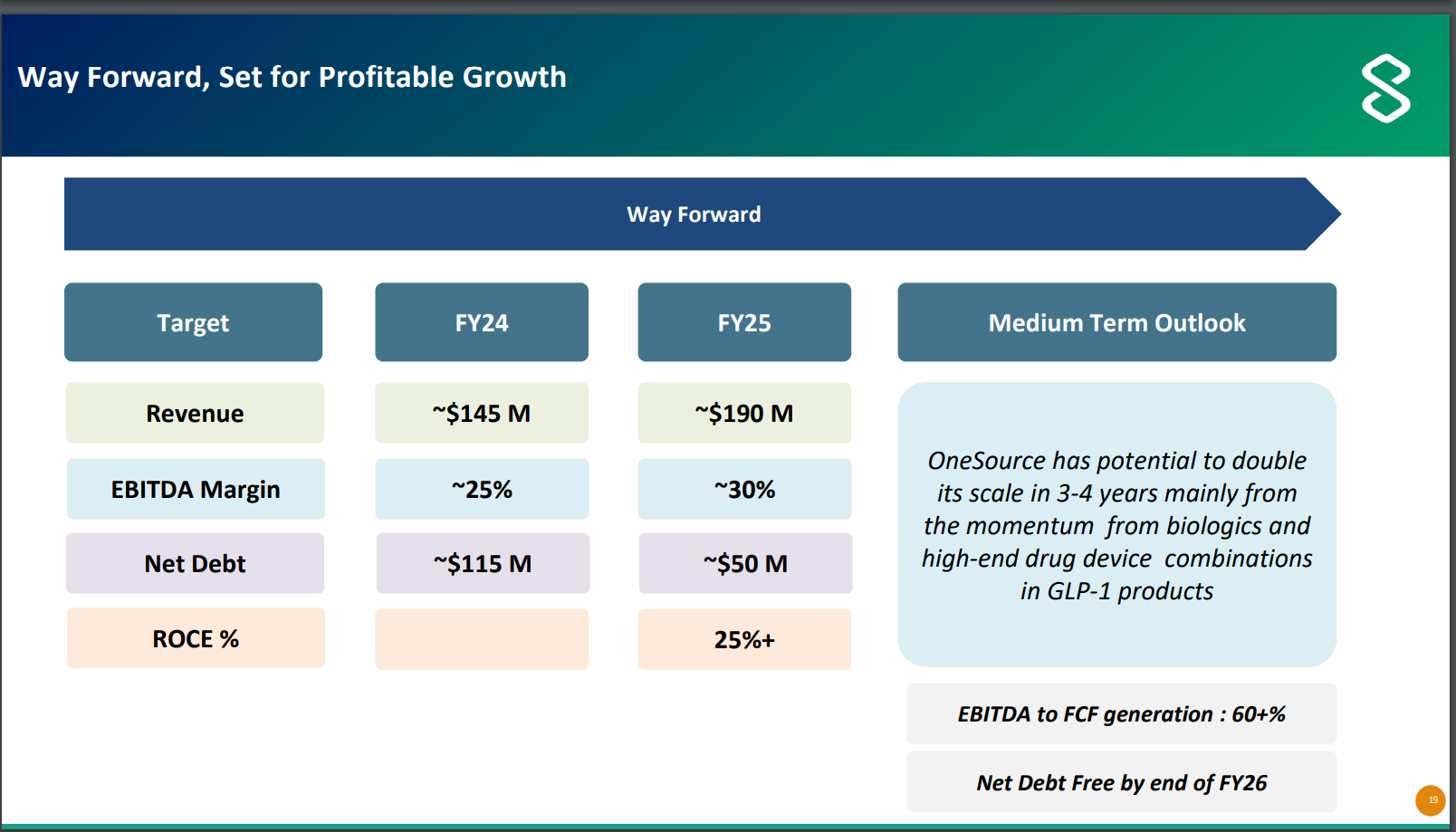

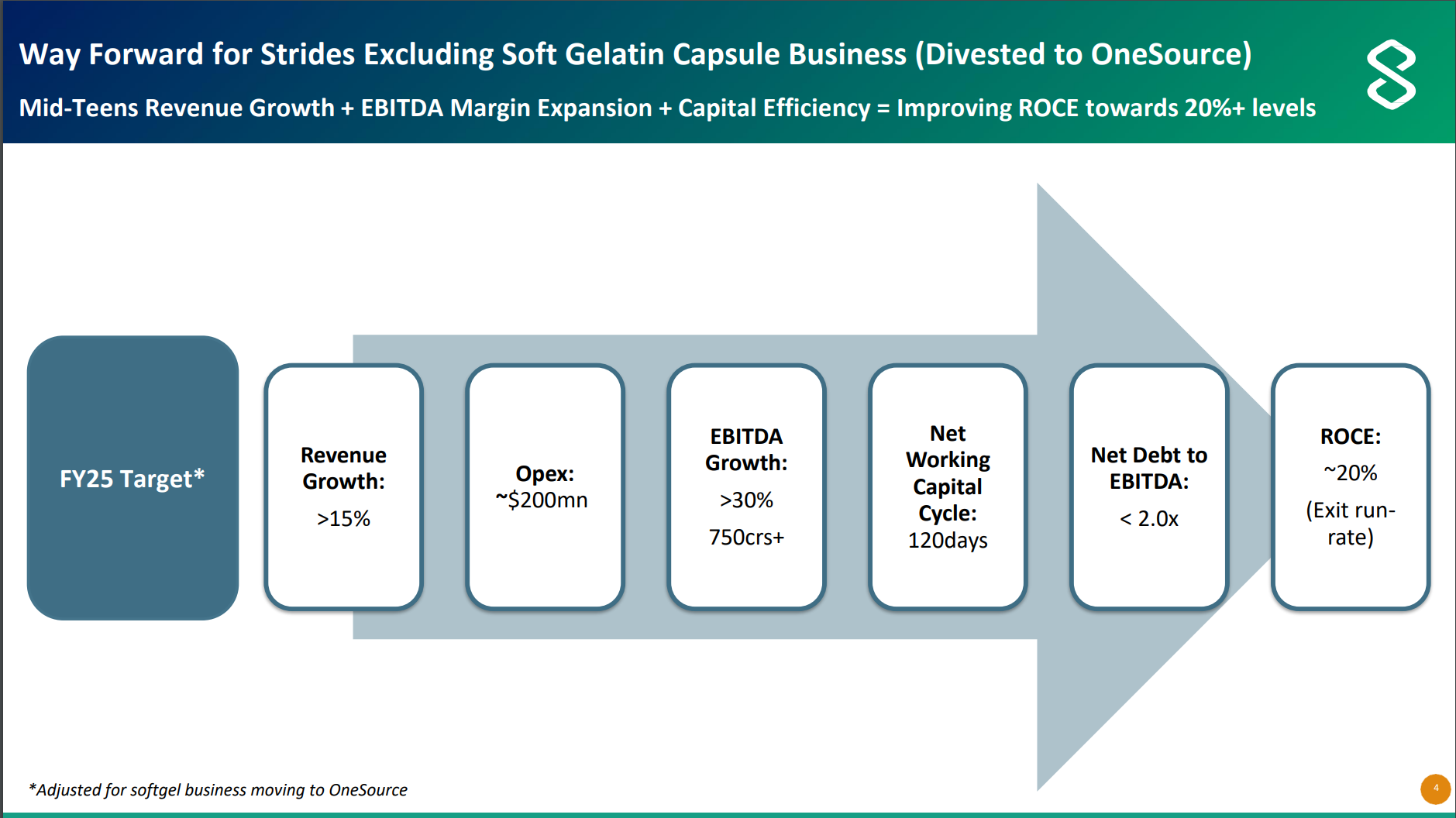

Parent company, Strides is trading at 890 rupees per share as of today. Net of OneSource, it is trading at 526 rupees per share or approx 4800cr m-cap.

Management has given guidance of 750cr EBITDA for Strides parent without soft gelatin business and Net Debt/EBITDA of < 2 i.e. net debt of around 1500cr.

So Strides is trading at EV/EBITDA for FY25 of - (4800cr + 1500cr)/750cr = 8.4.

If one looks at similar companies, like Alembic Pharma, they are trading at EV/EBITDA of 15-20.

We need to track execution towards above guidance quarter by quarter.

STELIS

There are two interesting parts in the Stelis story -

- First is GLP-1 order book and execution opportunity (Semaglutide/Liraglutide)

- Opportunity in Bio CDMO

GLP-1

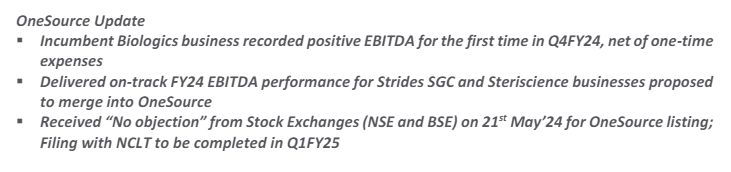

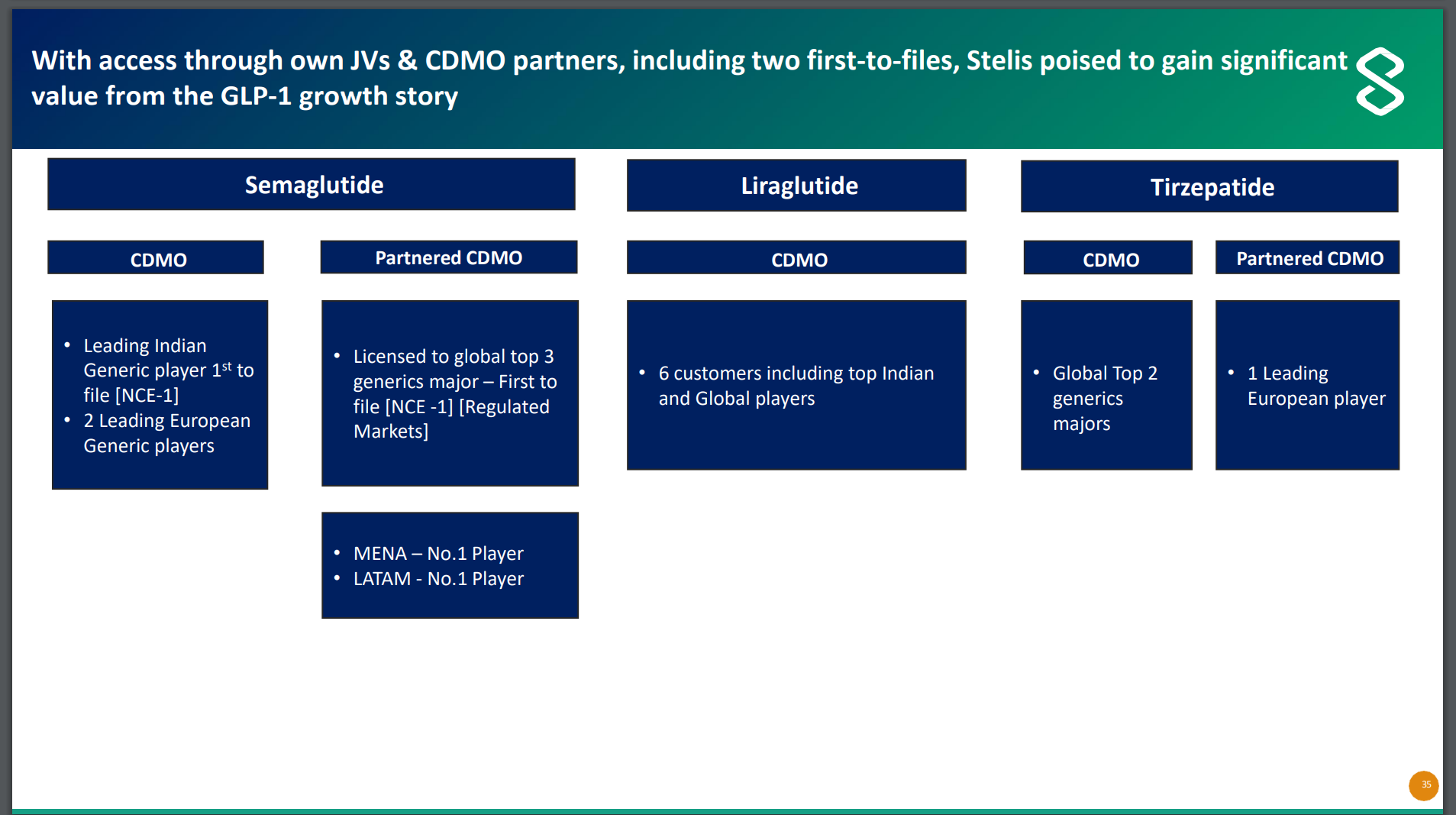

GLP-1 weight loss drugs is a large opportunity globally and it will start becoming meaningful for Indian players once patents start expiring. Liraglutide is first drug to go off patent in Nov 2024. For GLP-1 drugs, one needs drug API (lira/sema etc.), one needs device (manual injectors, auto injectors etc.) and one needs regulator approved facility to put drug and device together - which is called drug device. Creating this drug device is where Stelis comes into picture. Stelis seems to have spread its net deep and wide (all 3 drugs, all geographies etc.) and they have provided some details in below slide -

Another interesting thing to note in above PPT is that first to file generic player for Semaglutide are customers of Stelis.

Stelis came out with a credit rating in Jan 24 and it mentions the order book of 350mn$

Credit Rating -

Stelis Biopharma Limited (1).pdf (469.5 KB)

Stelis has 3 segments - namely Bio CDMO, GLP-1 and Small molecules. Bio CDMO is a long gestation and capital intensive industry (100-200mn$+ investment and 8-9 years). Stelis is in the early stages here where it is just securing projects for DS/DP (more on that later). Small molecules is not that large segment yet. So it is fair to assume that a large part of above 350mn$ order book is probably GLP-1 order book. This is also probably one of the reason for 190mn$ revenue guidance in OneSource in FY25.

Another point in this segment is that Stelis has USFDA/Europe approved facilities and no more inspections are needed for launching Liraglutide in FY25.

Final point I wish to make in GLP-1 vertical is that of shortage of capacity faced by innovators (and hope that similar thing might happen for generics and Stelis would be able to take advantage of it).

Novo Holdings (Holding Company of Novo Nordisk) has acquired Catalent and it will sell 3 fill-finish plants to Novo Nordisk.

One can google how Eli Lily is trying to question this deal and also its efforts to find alternate avenues to find fill-finish capacities.

BIO CDMO

I think the first point in this segment is the large opportunity size, high margins and significant value addition when one looks at global landscape.

Samsung Biologics, one of the largest player in Bio CDMO, has done revenue of 2939 KRW B (2bn$ +) and has EBITDA margins of 30-40%. They have order book of 12bn$+ and they are doing significant capex. SS biologics will have capacity of 700KL+ in 2025.

Aurobindo has a subsidiary in the space of biosimilars and it recently signed LoI with Merck for Mammalian CDMO contract.

Lonza recently bought Roche’s bio CDMO site having capacity of 330 KL for 1.2bn$.

Compared to that Stelis has tiny capacity of 16 KL.

So Bio CDMO/Bio similar business is a capex intensive (200mn$ starting capex) and long gestation (8-9 years) project.

Biosimilar development in itself is different from generic development and a quite investment heavy space. To develop biosimilar one has to do all the studies like - phase 1, phase 3, bio-equivalence, bio-kinetics, efficacy etc. The cost of developing a biosimilar is 50-100mn$+ in most of the cases.

The profit pools of Indian pharma companies did not allow such capex 10 years ago but things are changing now and slowly Indian pharma companies are investing into this space.

Stelis Bio CDMO part is probably into 5th or 6th year of above evolution and things would hopefully start to fall in place in year 8 or 9. Most other companies like Biocon, Dr Reddy, Aurobindo etc. have strong enough parent companies to support investments into Bio space. That is not the case with Strides with debt and other issues at parent level. So strides has invested whatever it could in Stelis. But Stelis had to find fund from other sources like promoter group entities or startup like funding rounds.

Final macro update in this space before we move to Stelis specific updates is recent BIOSECURE legislation in the US. This will raise barriers for Chinese biotech companies to operate in US and hopefully would open doors for Indian companies over time.

Now let us talk a little bit about bio products scale up process -

Drug Substance (DS) can be thought of as an API, Drug Product (DP) can be thought of as an Formulation. The source of the DS can be either mammalian or microbial.

Bio DS/DP product scale up can be though of as taking a bowl of curd and eventually producing a reactor (thousands of litres) full of curd. So one needs to take this mammalian or microbial source and express it at higher and higher volumes like - vial, beaker, reactor etc. In every stage, one needs to several tests to ensure that core properties are maintained. This scale up part is called as upstream.

Once you have KLs of DS/DP, then starts the purification process - where one needs to remove impurities. This process is called as downstream. The side effects of biosimilars are quite severe compared to chemical based products and hence downstream purification process is extremely critical.

With above basic understanding, one can see why margins of Bio CDMO players is that high.

Now let us talk about Stelis specific updates -

First thing is that Stelis has published annual report for AR23 and one can read it below -

Next part is that there are two types of agreements -

- First type is called as MSA - master service agreement. This part can be though of as CRO or development part of the agreement.

- Second type is called as CSA - commercial supply agreement.

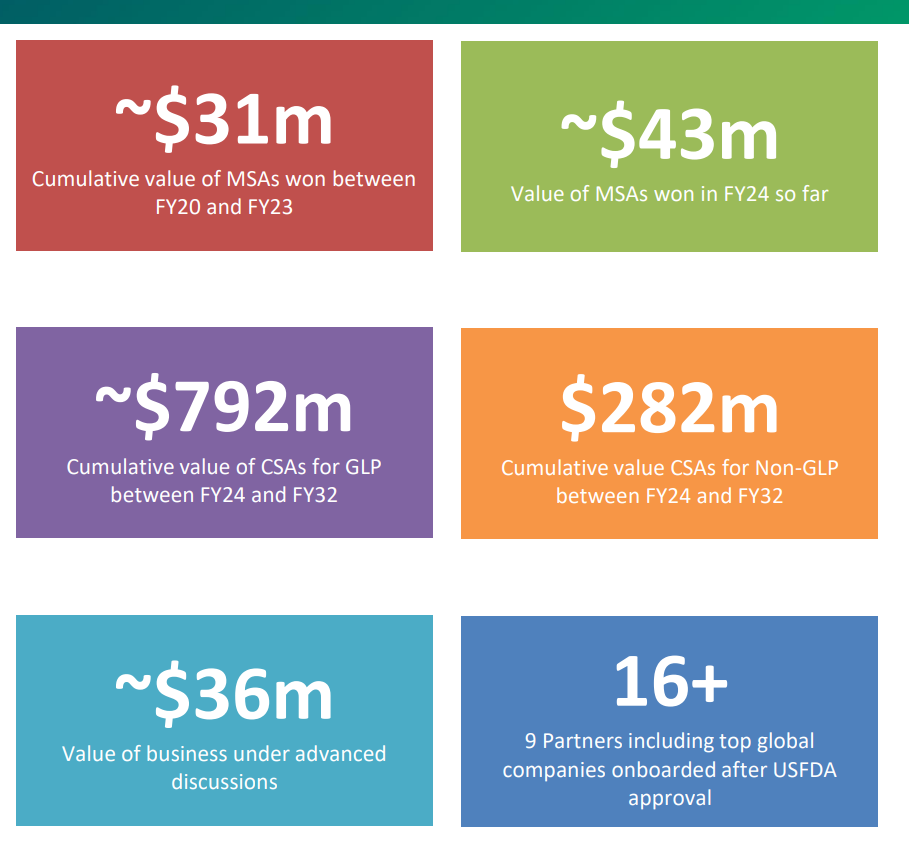

The company claims following values for their CSA and MSAs.

- First thing to note is that value of CSAs for GLPs is around 792mn$ for Fy24-FY32 duration. This ties back into 350mn$ order book in Stelis for FY24-28 duration.

- Second thing is that company’s plants got USFDA approved and post that, pace of MSAs has accelerated.

- The company has won MSAs of 43mn$ in FY24 and my assumption is that these are CRO projects where EBITDA margins would be very high.

- The company claims CSAs worth 282mn$ in non-GLP space for duration of FY24-32 duration.

- Another important announcement in q3 was that company has secured DS project from top 5 global generic company.

Outside of this, another product we need to talk about is Teriparatide. It is a biosimilar used in Osteoporosis. Innovators brand name is Forteo and sale was around 600mn$. Stelis has received approval for Teriparatide in European markets and it is looking to out-license this product to several European companies. As of now, these companies are in the process of acquiring registrations in their respective markets.

Several companies have received approval for Teriparatide now and it has become a crowded space (Apotex/Ambio, Accord/Intas, Teva etc.). How much of an opportunity this remains for Stelis needs to be seen.

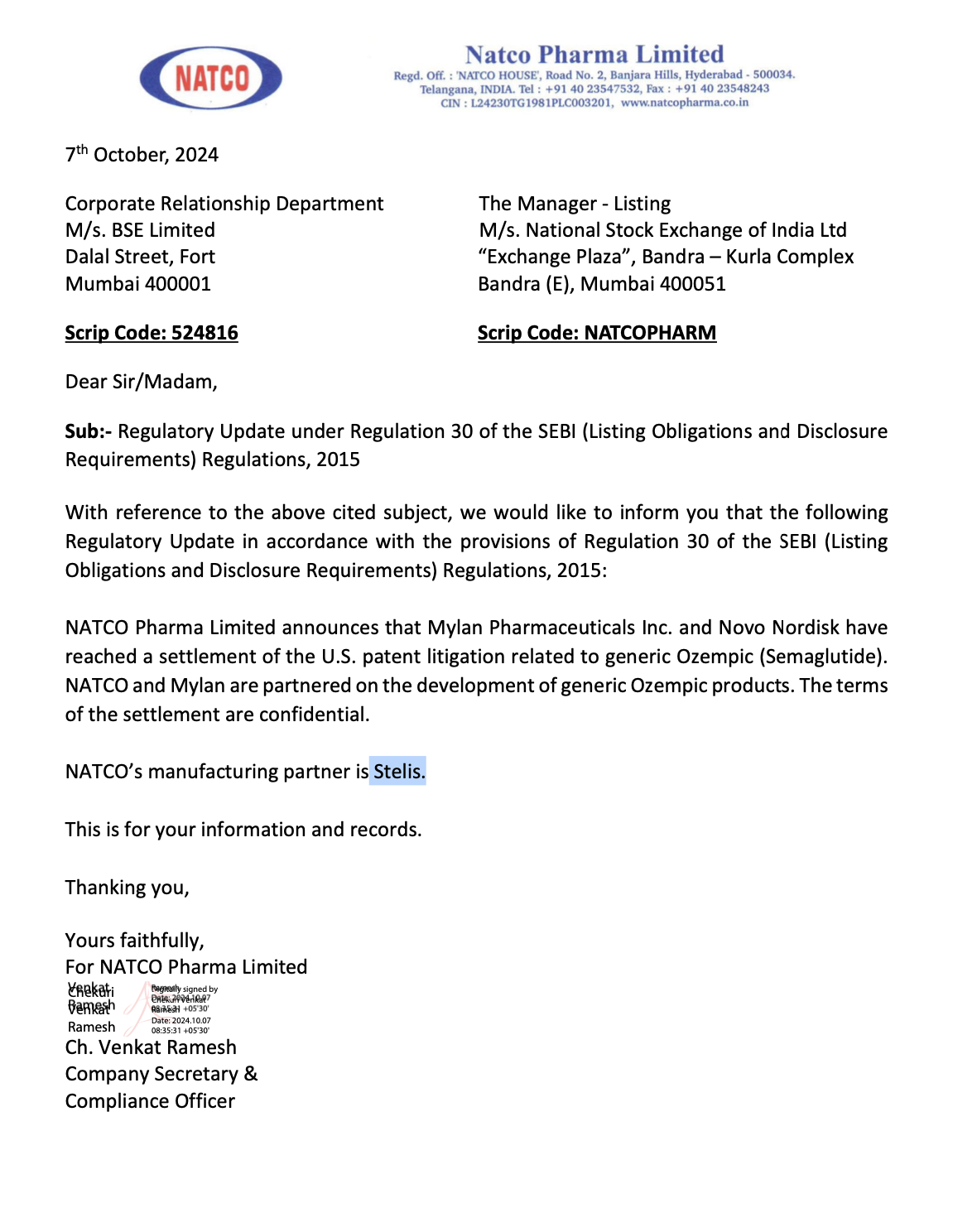

One final point (more like elephant in the room) that needs to be mentioned is write-off in Vaccine division -

- Stelis had signed contract with RDIF (Russian Direct Investment Fund) to manufacture some 200mn doses of Sputnik vaccine. But due to Russia-Ukraine war and sanctions on Russia, the deal fell through. Due to this, Stelis has to write off about 800cr worth of inventory.

- Stelis was in deep financial distress and eventually they had to sell their unit 3 to Syngene for about 710cr to save the day.

If one observes Sputnik story - few of the Indian companies have had inventory write downs (e.g. Wockhardt).

SOFT GEL CAPSULES BUSINESS

Now let us talk about softgel capsule business. First things first - let us try to understand promoter’s options when it was decided to move to OneSource.

- First thing is that OneSource is going to have decent amount of dent of its own (115mn$ net debt in FY24) and it is going to still need investments in Bio CDMO space and probably need capex in other two divisions. So instead of raising equity again and again, it probably was better to find the business piece that has good margins, steady cash flows which will form core of OneSource and it can fund all investments. So softgel business fits the bill and hence it was moved. (65mn$ sales, 30% margins - 533cr sales, 30% margins).

- There is significant possibility of value creation in OneSource, so promoter did not want to miss out on that probably. but at the same time, he did not want to increase only his shareholding and damage his reputation with public shareholding. In this delicate balancing, SteriScience and Softgel Capsule businesses are merged. Stelis shareholders now get 44% shareholding in OneSource instead of 30% in Stelis before. Promoter also does not miss out on value creation and two of his platforms (Stelis and SteriScience) get publicly listed and hopefully OneSource becomes a self sustaining entity.

There are only two more points that are worth mentioning in this vertical -

First, Strides is doing capex in Softgel business and they are taking the capacity from 800mn to 2.2bn units and the order books in this business are quite full and it is poised for growth.

Second, why are margins so high in this segment vs players like e.g. Natural Capsules? To me, it looks like this is because they are not into nutraceuticals but into pharmaceuticals and they operate in regulated markets like US/EU. The company like Lonza also has softgel capsule division and they make very high margins and this is because Lonza caters to innovator customers.

STERISCIENCE

Now let us move to other unlisted company of promoter which will be part of OneSource - SteriScience.

Strides group had injectable business and that business was called Agila and it was sold to Mylan for 1.6bn$ around 2013-14. The company had non-compete agreement with Mylan for 6-7 years. That expired in 2020 and the group reentered back into this space. Most of the old team seems to be back at SteriScience and they also bought back some plants from Mylan due to restructuring at Mylan level.

The details of injectable sites are present on their website at

https://steri-science.com/manufacturing/

SteriScience’s Dec 23 credit report was an interesting read -

Few points to be noted are -

First, capacities

Second part is that 50-60% revenues come from Mylan due to past relationships.

From above, it can be noted is that they are full on capacities for this year and next year. They have space to add another line - as and when they do it, it has potential to double the revenue.

Final point is a macro one. There seems to be injectable shortages in the US and this can act as an tailwind to this segment. This can also be observed based on large grants received by Jubilant Pharmova to build injectable lines in USA/Canada.

PARENT COMPANY, STRIDES

Finally, we come to parent Company Strides. Here I will make few quick points and then we can conclude -

-

First thing is that company has given guidance of const control with all the costs combines to stay around 200mn$ range. If they can achieve this, this will result in significant operating leverage. If we are to break this further, 2/3 sub factors can drive this -

i) Selling off High Cost Plant in Singapore

ii) Acquisition of ANDAs through Endo, so reduced R&D expenditure

iii) Optimizing operations at Endo Pharma, US. Rationalizing manpower, other cost initiatives.

iv) Optimized shipping, inventory management and reducing failure to supply, penalties etc. -

The second point is growth and possibility of improved gross margins. The company has recently received approvals for Icosapent Ethyl (Brand Name - Vascepa). This is a large product and company has entered into profit sharing agreement with Amneal.

The other product worth talking about is Suprep.

-

The company has been launching products of size 4-5mn$ over last few years. Over next 3 years, company plans to launch 60 products and plan to move the average size to 15-20mn$. Company has ~150 ANDAs which are yet to be commercialized.

-

The company bought a site from Endo Pharmaceuticals and approved ANDAs.

-

The company claims to be #1 in 19 products in the US. In the 70% of these products, the company claims hat there is no Indian competitor for many years.

RISKS

Let me quickly list out few risks to the thesis.

-

The biggest risk to the thesis is past track record of promoter. Although there are no integrity questions and also there are no regulatory approval questions (in my mind at least), there has been a record of M&A, buying/selling assets, restructurings etc. or some sort of overpromise and under-delivery. I would hope that promoters let the operations run on their own and let balance sheet improve.

-

The second issue so as to say is goodwill that will be carried in the books of OneSource. I think the net asset value of Softgel business would be 100-200cr. That business is valued at 2400cr type equity value, so there would be 2000cr worth of goodwill in the books of OneSource. A similar maths would hold for SteriScience as well as it is being valued at 2100-2200cr. Although this would be a non-cash expense, the reported PAT numbers would be significantly suppressed. One hopes that market values the business using EV/EBITDA or M-Cap/OCF.

SUMMARY

Strides + OneSource looks to be an interesting bet with turnaround, improving efficiencies at the parent level in the near term, growth in Softgel capsules + injectable business in the near term, significant opportunity in fast growing GLP space in the medium term, probability of some market share in fast growing, high quality Bio CDMO space in the longer term.

The key monitorables are execution by promoter without any M&As, continued status quo or improvement in formulations environment.

Disc - I am invested in the company from lower levels. There are no transactions in the last 30 days. This is not a buy or sell recommendation. I am not a SEBI registered advisor. I am positively biased as I own the shares of the company. I may decide to buy or sell at any time without informing the forum.